Published as part of the Financial Stability Review, May 2022.

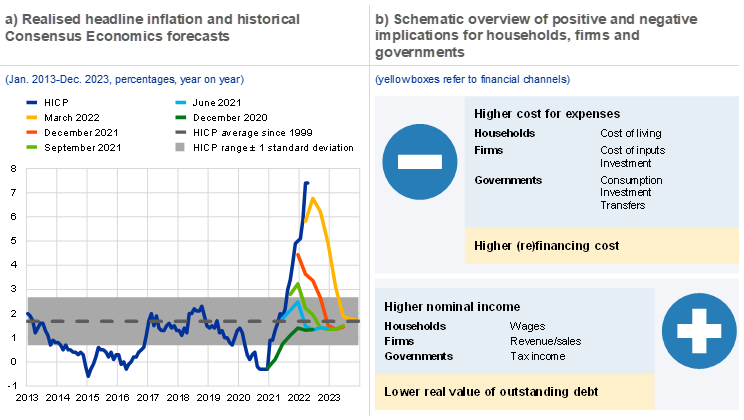

Global inflation rates have increased substantially over the past year, driven by high energy prices, supply chain constraints and a rebound in demand. Inflation in the euro area is expected to remain elevated throughout 2022. Since the end of 2020, professional forecasters have repeatedly revised up their inflation projections as outturns surprised to the upside (Chart A, panel a).[1] Future developments in terms of energy prices and supply bottlenecks present upside risks to inflation.[2] This box assesses the channels through which higher than expected inflation could affect financial stability, taking into account the effects for governments, firms, households and financial markets.

Significant inflation surprises can lead to market volatility, increasing the probability of a disorderly repricing of assets. When faced with an inflation shock, market participants try to anticipate the potential response of central banks as they seek to maintain price stability. This can prompt adjustments in market interest rates at the short and long end (depending on market participants’ expectations), followed by adjustments in other market prices. If nominal interest rates increase by more than (expected) inflation rates, (expected) real yields increase. All else being equal, higher real yields are typically associated with de-risking by investors. Over the past decade, search-for-yield behaviour has led to compressed risk premia and elevated asset prices. This increases the potential scale of adjustments when real yields start to rise. At the same time, in an inflationary environment, equities may be more attractive than fixed income products, as the coupon payments on nominal bonds do not offer protection against inflation. The ultimate impact on equity markets also hinges on economic growth prospects.

Higher than expected inflation also affects the capacity of different borrowers to service their debts, even as inflation may reduce the real value of outstanding debt. The real value of any nominal amount of outstanding debt decreases as prices increase. This means that, in aggregate, borrowers’ loan repayments are relatively smaller in real terms, such that they have to forego relatively fewer “consumption baskets” to repay their loans. However, borrowers could run into debt servicing problems if their income does not increase enough to offset the higher cost of consumption and investment (Chart A, panel b). This is more likely to happen if supply shocks result in both lower growth and higher inflation. Generally, borrowers with variable-rate debt contracts are more directly exposed to rising interest rates, with their debt servicing capacity hurt by more than that of borrowers with fixed-rate debt.

Chart A

Inflation can ease some aspects of debt burdens, but it can also create challenges for debt servicing and rollover

Sources: Eurostat, Consensus Economics Inc. and ECB.

Notes: Consensus Economics forecasts are at quarterly frequency; observations for months within the quarters are linearly interpolated.

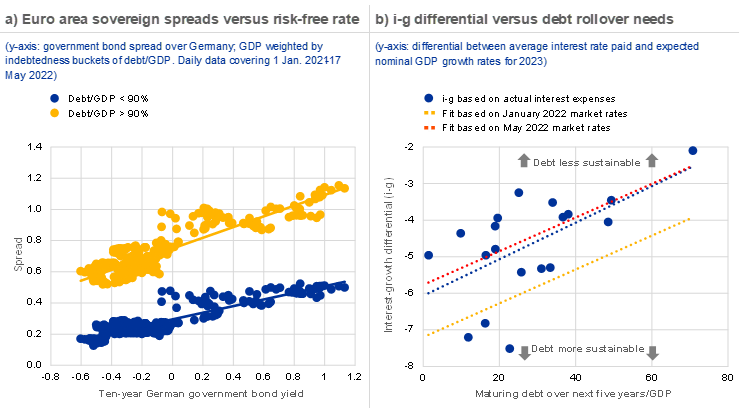

Highly indebted sovereigns could face a deterioration in debt servicing capacity if rising interest rates and risk premia drive a wedge between nominal interest rates (i) and nominal economic growth (g). The interest rate-growth differential (i−𝑔) is a key parameter in the analysis of government debt sustainability.[3] When interest rates exceed the growth rate, a primary surplus is needed to stop the debt ratio from rising. This pressure on governments’ balance sheets is also called the “snowball effect”. Theoretically, both nominal interest rates and nominal growth rates could increase with inflation. However, expected output growth will likely face downward pressures when nominal rates increase, everything else equal. A wedge could thus be driven between i and g, further exacerbated by increasing risk premia. An increase in risk-free rates may have a larger impact on the budget of more indebted sovereigns, and may therefore be accompanied by a widening of sovereign spreads (Chart B, panel a). This could be of greater concern for more indebted countries with relatively high short- to medium-term refinancing needs, as their interest rate-growth differential, which is already higher, might increase by more than that of countries with lower short- to medium-term refinancing needs (Chart B, panel b).

That said, several factors are alleviating the risk of elevated pressure on highly indebted sovereigns. Sovereigns in the euro area continue to benefit from relatively low interest rates. Despite recent increases, current market rates are still close to the average rate paid by many euro area countries (Chart B, panel b). Furthermore, governments have generally strengthened their debt structures over the last decade by increasing the average residual maturity, diversifying their portfolio of instruments and expanding the investor base. This means that any increase in the marginal cost of funding feeds through to the average interest rate relatively slowly. Consequently, the interest rate-growth differential could improve especially during the early stages of an inflationary shock if nominal GDP growth is boosted by inflation, whilst the average interest rate paid on the total debt stock adjusts gradually. Furthermore, since mid-2021 countries have benefited from the support offered through the Recovery and Resilience Facility, a centrepiece of the European Union’s Next Generation EU (NGEU) package. This support will continue until 2026, although the share of allocated grants and loans varies across countries. However, countries will face higher contributions to the EU budget to finance the NGEU package in the medium to long run.

Chart B

Indebted sovereigns are more vulnerable to a widening of the interest rate-growth differential

Sources: European Commission, Eurostat, Bloomberg Finance L.P., ECB and ECB calculations.

Notes: Panel a: interest rate spreads for euro area countries. Panel b: market rates are based on seven-year or nearest available to seven-year government benchmark bond yields. Market rates in January and May are computed as average over the available daily observations. Last observation 17 May 2022.

Households’ real disposable incomes could suffer if nominal wages do not offset price increases, with potential implications for residential real estate markets. A drop in real disposable income could lead to lower consumption as households try to continue servicing their debt. A serious deterioration in real disposable income could lead to bank loan losses, as households with weak balance sheets may struggle to repay debt, including mortgages and consumer loans, especially when rates on such loans are variable. As households have moved to long-term fixed-rate contracts in many euro area countries, they might be shielded to some extent against this effect. In addition, households’ borrowing capacity could deteriorate, potentially putting downward pressure on valuations of residential real estate. In aggregate, households still benefit from the sizeable volumes of liquid assets that they accumulated during the pandemic and that would, to some extent, relieve the debt servicing burden, which on aggregate is also low relative to disposable income. However, this masks the fact that liquid assets are unevenly distributed and that higher than expected inflation can have negative distributional consequences that affect low-income households the most. Finally, consumer confidence may erode in a high inflation environment, with potentially adverse consequences for consumption.

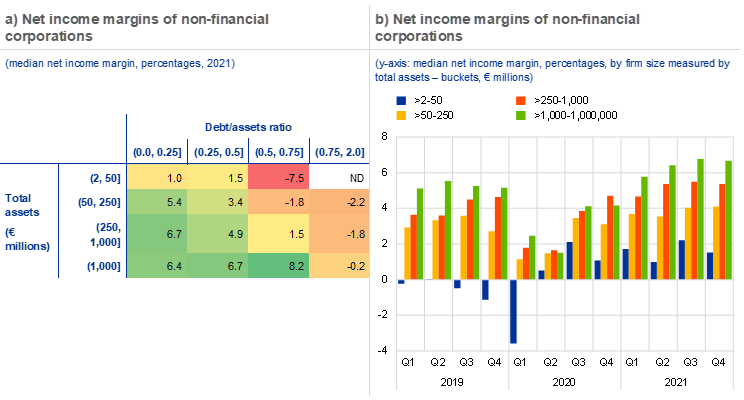

Vulnerable corporates with lower pricing power and higher debt are more exposed to pressure on debt sustainability from inflation shocks than other corporates. While some firms can pass on cost increases to consumers, other firms with less pricing power may face cost increases that outpace revenue growth. Smaller and more indebted firms might have lower pricing power, according to data on net income margins (Chart C).[4] Insolvency rates have been very low recently, but vulnerabilities have built up in the sectors worst affected by the pandemic. If higher inflation rates drive cost increases while revenue growth is subdued, insolvency cases may start to rise among vulnerable and indebted firms, raising creditor losses.

Chart C

Smaller and more indebted firms have lower net income margins, pointing to lower pricing power

Sources: S&P Global Market Intelligence and ECB calculations.

Notes: Net income margins vary by sector. Sample of 1,183 unique euro area non-financial corporations.

If higher inflation is accompanied by subdued growth, the negative impact of inflation on financial stability would be exacerbated amid limited scope for offsetting income increases. Inflation exists in different forms, such as demand-pull, cost-push, imported or wage/price-spiral inflation. When inflation is driven by more exogenous supply shocks or cost-push shocks generated by higher energy prices, the scope for higher income is more limited, the balance of risks is tilted to the downside and the i−𝑔 gap is more likely to widen.

While financial stability is a prerequisite for price stability, price stability also affects financial stability. The ECB monetary policy strategy review conducted in 2021 recognises that price stability depends on financial stability[5] and states that the preparation of monetary policy decisions will be enhanced with additional information on financial stability considerations. At the same time, the considerations presented in this box illustrate that financial stability is also influenced by price stability.

See, for example, the Eurosystem and ECB staff macroeconomic projections.

In response to these developments, the Governing Council has stated that “If the incoming data support the expectation that the medium-term inflation outlook will not weaken even after the end of its net asset purchases, the Governing Council will conclude net purchases under the APP in the third quarter [of 2022]” (ECB Monetary Policy Decisions, 10 March 2022). In addition, the Governing Council has stated that it “judged that the incoming data since its last [April] meeting reinforce its expectation that net asset purchases under the APP should be concluded in the third quarter” (ECB Monetary Policy Decisions, 14 April 2022).

For more details, see the box entitled “Sensitivity of sovereign debt in the euro area to an interest rate-growth differential shock”, Financial Stability Review, ECB, November 2021.

Lower net income margins do not necessarily point to lower pricing power. For example, margins for more indebted firms may simply be lower due to higher interest expenses. At the same time, this still leaves these firms vulnerable, as the “buffer” in terms of positive margins is already smaller to begin with, meaning that a compression of margins may result in realised losses more quickly.