Stablecoins’ role in crypto and beyond: functions, risks and policy

Stablecoins’ role in crypto and beyond: functions, risks and policy

Published as part of the Macroprudential Bulletin 18, July 2022.

Stablecoins are in the spotlight due to their rapid growth, increasing global use cases and potential financial risk contagion channels. This article analyses the role played by stablecoins within the wider crypto-asset ecosystem and finds that some existing stablecoins are already critical to liquidity in crypto-asset markets. This could have wide-ranging implications for crypto-asset markets if a large stablecoin were to fail and could also have contagion effects if crypto-assets’ interlinkages with the traditional financial system continue rising. To date, the speed and cost of stablecoin transactions, as well as their redemption terms and conditions, have fallen short of what is required of practical means of payment in the real economy. Their growth, innovation and increasing use cases, coupled with their potential contagion channels to the financial sector, call for the urgent implementation of effective regulatory, supervisory and oversight frameworks before significant further interconnectedness with the traditional financial system occurs.

1 Introduction

Stablecoins are currently in the spotlight of policymakers due to their rapid growth, increasing global use cases and potential financial risk contagion channels. Stablecoins are a segment of the wider crypto-asset ecosystem along with what is often referred to as unbacked crypto-assets.[2] They were developed to address the high price fluctuations of unbacked crypto-assets such as bitcoin and ether, and their comparatively low price volatility predestines stablecoins for a number of functions where this property is needed. However, events in early May showed that stablecoins may not be so stable after all. Their reserve assets (in the case of collateralised stablecoins) give them a direct link to the traditional financial sector, which warrants policymakers’ attention.

Stablecoins are digital units of value that rely on stabilisation tools to maintain a stable value relative to one or several official currencies or other assets (including crypto-assets).[3] Stabilisation tools include reserve assets against which stablecoin holdings can be redeemed, as used by so-called collateralised stablecoins, and algorithms that match supply and demand to maintain a stable value, as used by so-called algorithmic stablecoins.[4]

This article discusses the financial stability implications of stablecoins stemming from their current role in the crypto-asset ecosystem. First, it analyses the importance of stablecoins within wider crypto-asset markets before going on to examine whether they fulfil the requirements of practical means of payment in the real economy. The article finishes by highlighting what the current role of stablecoins implies for financial stability and the importance of their regulation.

2 Stablecoins’ role within the crypto-asset ecosystem

The uses of stablecoins within the crypto-asset ecosystem have multiplied in recent years. Initially, stablecoins were mainly used as a relatively safe “parking space” for crypto volatility and as a bridge to trade crypto-assets.[5] But with the rise of decentralised finance (DeFi) applications, stablecoins have gained new uses.[6]

Stablecoins account for only a small part of the total crypto-asset market, but the largest ones have assumed a critical role within the crypto-asset ecosystem. Although their market capitalisation increased from €23 billion in early 2021 to just under €150 billion in the first quarter of 2022, stablecoins still only account for below 10% of the total crypto-asset market. However, they have become a critical part of the crypto-asset ecosystem due to their frequent use in the trading of crypto-assets and as liquidity providers in DeFi. This holds specifically for the stablecoins dominating the market. Tether, USD Coin and Binance USD, which are all collateralised stablecoins, account for around 90% of the total stablecoin market. Other stablecoins with meaningful shares include the algorithmic stablecoins DAI and – until its crash on 9 May, which wiped out almost its entire market capitalisation – TerraUSD.

The largest existing stablecoin, Tether, has already become critical in crypto-asset trading. One major activity for which stablecoins are used is crypto-asset trading, where they function as a bridge between official currencies and crypto-assets. Driven by Tether, the trading volumes of stablecoins surpassed those of unbacked crypto-assets in the course of 2021, reaching average quarterly trading volumes of €2.96 trillion, almost on a par with those of US equities on the New York Stock Exchange (€3.12 trillion).[7] In addition, Tether is involved in half of all trades of bitcoin and ether, which is a higher proportion than the trades of bitcoin and ether against official currencies[8] (Chart 1, panel a), and accounted for around 65% of all trading on crypto-asset trading platforms in March 2022.[9]

Chart 1

Tether dominates trading volumes within the crypto-asset ecosystem, and stablecoins provide most of the liquidity for decentralised trading and lending

Sources: IntoTheBlock, CryptoCompare and ECB calculations.

Notes: Panel a: trading volume data are based on CryptoCompare’s real-time aggregate index methodology (CCCAGG), which aggregates transaction data from more than 250 exchanges. The chart reflects the sum of trading volumes involving bitcoin or ether (monthly average), as well as the respective percentages of the volume of trades occurring between bitcoin/ether and listed assets or asset groups. “Other stablecoins” includes USD Coin, DAI, Pax Dollar, TerraUSD and 12 other large stablecoins. “Other crypto-assets” includes 29 of the largest unbacked crypto-assets after bitcoin and ether. “Official currencies” includes USD, EUR, JPY, GBP, RUB, PLN, AUD, BRL, KRW, TRY, UAH, CHF, CAD, NZD, ZAR, NGN, INR and KZT. “Other” consists of remaining assets not included in the preceding categories. Panel b: stablecoin liquidity in DEXes is approximated based on the ten most liquid pairs on Curve, Uniswap and SushiSwap as of 17 May 2022. Curve, Uniswap and SushiSwap represent approximately 50% of total value locked in DEXes. “Stablecoins (collateralised)” includes Tether, USD Coin and True USD. “Stablecoins (algorithmic)” includes DAI, Magic Internet Money and three further stablecoins. “Other crypto-assets” includes ether, PAX Gold and FNK wallet. “DeFi Tokens” includes wrapped bitcoin, Uniswap’s governance token UNI, SushiSwap’s governance token SUSHI and 16 other tokens of different DeFi protocols.

Stablecoins provide most of the liquidity in DeFi applications such as decentralised exchanges and lending protocols.[10] Stablecoins provided around 45% of the liquidity in decentralised exchanges (DEXes) in May 2022 (Chart 1, panel b).[11] About half of this amount was provided by collateralised stablecoins. However, for collateralised stablecoins like Tether and USD Coin, liquidity provision for decentralised trading or lending is relatively low compared to their total market capitalisation (less than 8%). This suggests they are still mainly used for other purposes in the crypto-asset ecosystem. By comparison, for algorithmic stablecoins like DAI (more than 30%) and TerraUSD (more than 75% before its crash), liquidity provision in DeFi represents a substantial share of their total market capitalisation.[12] For these particular stablecoins, usage in DeFi is thus quite important.

3 Stablecoins as means of payment

Stablecoins fall short of what is required of practical means of payment for the real economy. Below, several technical aspects on how stablecoins fall short of the requirements needed for real economy payments are elaborated, although without including a detailed comparison with traditional payment systems that offer other benefits such as legal certainty, settlement finality and operational resilience.

European payment service providers (PSPs) are not very active in stablecoin markets and offer limited stablecoin payment services. One reason for this lack of activity could be regulatory uncertainty pending the adoption of the Markets in Crypto-assets (MiCA) Regulation. Most service providers active in stablecoin markets in the EU are registered in the EU, with only a few authorised as PSPs, while the majority are registered as virtual asset service providers (under the current anti-money laundering/countering the financing of terrorism (AML/CFT) framework). Activity varies considerably between EU Member States. Services related to stablecoins in the EU mainly consist of acquisition, holding or selling via different means, while the availability of services for spending stablecoins at merchants is currently limited. Most stablecoins offered by EU PSPs are still USD-pegged, with only a few offering EUR-pegged stablecoins.

Transaction speeds differ by blockchain but are slow for stablecoins issued on the predominant blockchain. Transaction speeds as measured by the confirmation time for an average transaction vary by blockchain (Chart 2, panel a) and depend inter alia on the consensus mechanism used. Other factors such as the block time and size, transaction fees and network traffic also influence transaction speeds. The Ethereum blockchain is still the predominant blockchain on which many stablecoins operate, although this is changing.[13] The duration between transaction blocks of the largest stablecoins on the Ethereum blockchain, such as Tether, USD Coin and DAI, is comparable to that of ether and faster than for transactions of bitcoin (Chart 2, panel b). However, the transaction time is not near-instant or real-time as required for usage at the physical point of sale or in e-commerce. Additionally, transaction speeds differ between stablecoins on the same blockchain with smaller and less liquid stablecoins and those pegged to real assets like gold, which have longer transaction times.[14]

It is not clear if blockchain technology will ever be able to outperform non-blockchain payment technology. Private stablecoins are argued to be technologically superior to traditional payment systems because they use blockchain platforms. However, this superiority may be temporary. As an example, during testing for a central bank digital currency, the Federal Reserve Bank of Boston showed that a non-blockchain payment technology can perform ten times more transactions per second than a high-performance blockchain technology.[15] The necessary ordering of valid transactions to prevent double spending in the blockchain creates bottlenecks that limit scalability and may ultimately hamper fast payments.

Chart 2

Blockchain networks differ in their scalability, but even on the same blockchain, stablecoin transaction speeds may differ

a) Average transaction confirmation time and network scalability | b) Average duration between transaction blocks of bitcoin and stablecoins on Ethereum blockchain |

|---|---|

(left-hand scale: transactions per second (TPS), right-hand scale: seconds) | (Jan. 2020-Feb. 2022; seconds) |

|  |

Sources: Intotheblock, PhAmex Blog, Algorand Blog and Avalanche Support.

Notes: Panel a: the left-hand scale shows the number of TPS processed on average by each network that is below the maximum capacity claimed by each network. For Mastercard, only the network’s maximum capacity of transactions per second is available (5,000 TPS), so it is not included in the chart. BTC: bitcoin blockchain, ETH: Ethereum blockchain, SOL: Solana blockchain, TRON: Tron blockchain, AVAL: Avalanche blockchain, ALGO: Algorand blockchain. The right-hand scale shows the average transaction confirmation time in seconds. Panel b: average duration between transaction blocks of bitcoin and stablecoins in the Ethereum network; ETH: ether; USDT: Tether; USDC: USD Coin; BUSD: Binance USD; DAI: Dai; GUSD: Gemini Dollar; USDP: Pax Dollar; PAXG: PAX Gold; BTC: bitcoin.

Stablecoin transaction costs can vary substantially and do not show a clear-cut advantage compared with traditional payment schemes. Transaction costs of stablecoins vary depending on a number of factors, such as the complexity of a transaction or the congestion of the network, leading to higher fees.[16] Analysis of stablecoin transaction fees by Mizrach (2022) shows that, for a large portion of stablecoins, the transaction costs are higher than those of ATM transactions or the average costs of Visa or Mastercard schemes in Europe.[17] However, there are differences across stablecoins. While the median transaction fee for Tether is similar to the cost of an ATM transaction[18], it is three to four times higher if DAI or USD Coin is used. In addition, customers often use payment accounts with (flat) fees to cover most of their payment services. If these payment accounts remain essential for end users’ everyday payment use and end users need an additional account or wallet for stablecoins, then using stablecoins may represent another layer of fees and be unattractive for end users.[19]

Stablecoin issuers are moving to new blockchain technologies to address the scalability and efficiency issues of the current most-used blockchains.[20] The majority of stablecoins are minted on blockchains using proof-of-work (PoW) consensus mechanisms that require network participants (the so-called miners) to compete with each other on the network to solve the complex puzzles involved in validating new transactions and adding new blocks. This not only makes PoW blockchains slower and less scalable, but also highly energy-consuming.[21] New blockchain networks following proof-of-stake (PoS) or proof-of-history (PoH) consensus mechanisms increase speed by requiring less network participants (or “validators”), reducing the computational power needed to verify each block transaction.[22] These networks, including Tron, Avalanche, Algorand and Solana, enable more transactions to be performed per second than on the Ethereum or bitcoin networks, are more scalable and have lower transaction costs (Chart 2, panel a). However, there may be a trade-off between scalability, security and decentralisation.[23]

The largest stablecoins constrain users’ redemption possibilities. Users should be able to redeem their stablecoins at any moment and at par value to the referenced official currency. As is the case for traditional PSPs, users should also be able to easily access information about the redemption terms. However, stablecoin issuers constrain users in their redemption possibilities and offer insufficient public disclosure about their redemption terms. For example, the largest stablecoin issuers offer redemption only once per week or during business days.[24] In addition, the right to redeem at par value to the official currency of denomination is not always ensured, meaning redemptions are dependent on reserve valuation or must be made in-kind.[25] In some cases, holders of stablecoins also face limits or high minimum thresholds for redemptions. This makes them unredeemable for the majority of ordinary retail users.[26] In addition, consumer protection measures such as transparency requirements, refunds, protection from excessive fees and fraud compensation are currently not applicable for stablecoins.

4 Potential risks to financial stability stemming from stablecoins

Stablecoins may pose risks to financial stability through different contagion channels. These channels include: (i) financial sector exposures; (ii) wealth effects (i.e. the degree to which changes in the value of crypto-assets might affect their investors, with subsequent knock-on effects on the financial system); (iii) confidence effects (i.e. the degree to which developments concerning crypto-assets could affect investor confidence in crypto-asset markets and potentially the broader financial system); and (iv) the extent of crypto-assets’ use in payments and settlements.[27]

Issuers of collateralised stablecoins need to ensure robust reserve asset management to instil confidence, ensure the stability of the peg and avoid a run on the coin with possible contagion to the financial sector. Like money market funds (MMFs), reserve assets of stablecoins need to be liquid to allow users to redeem their stablecoins in fiat currency. Adequate management of reserve assets underpins users’ confidence in stablecoins. A loss of confidence could trigger large-scale redemption requests – especially if there are limited redemption possibilities (Section 3) – leading to the liquidation of reserve assets with negative contagion effects on the financial system. It is worth noting that the largest stablecoins have already reached a scale comparable to large prime MMFs domiciled in Europe.[28]

While the transparency of reserve asset composition has increased somewhat over the last year, details are still scarce. Reserve asset disclosures have become more transparent since early 2021, and there has been a shift towards more liquid assets.[29] However, Tether still holds large investments in commercial paper despite a 20% reduction by the end of 2021, as well as positions in MMFs and digital tokens.[30] The lack of granular information on the geographical origin or exact size of Tether’s commercial paper holdings – as they are not separated from certificates of deposits – impedes a clear view on the liquidity of these reserves and the contagion effects for short-term funding markets. In addition, it is difficult to compare the composition of reserve assets across stablecoins given the lack of disclosure and reporting standards.

Recent developments show that stablecoins are anything but stable, as exemplified by the crash of TerraUSD and the temporary de-pegging of Tether. Amid a general downturn in the crypto-asset markets, TerraUSD lost its peg to the US dollar on 9 May and crashed to a price below USD 10 cents after 16 May. At the same time, its market capitalisation fell from around €18 billion to less than €2 billion (Chart 3, panel a). Amid the ensuing crypto market stress, the price of Tether came under pressure, with the largest stablecoin temporarily losing its peg on 12 May (Chart 3, panel b). Since then, Tether has seen outflows of more than €8 billion, equivalent to almost 10% of its market capitalisation. This episode shows that stablecoins cannot guarantee their peg and, if it is lost, there is a risk of contagion within the crypto-asset ecosystem. It seems the market has differentiated between stablecoins. In the case of Tether, shortcomings in its redemption possibilities and a loss of confidence potentially related to the opacity of its reserve composition may have played a role in the de-pegging and continuous outflows observed.[31] The other two major collateralised stablecoins, USD Coin and Binance USD, have instead seen small inflows (Chart 3, panel a).

Chart 3

Since temporarily losing its peg to the US dollar, Tether’s market capitalisation has fallen alongside that of the failed stablecoin TerraUSD, while the market capitalisation of other large stablecoins has slightly increased

a) Market capitalisation of selected stablecoins | b) Intraday price development of Tether on 12 May 2022 |

|---|---|

(9 May 2022-8 Jun. 2022; EUR billions) | (12 May 2022; US dollars) |

|  |

Sources: CryptoCompare, Glassnode and ECB calculations.

Note: Panel b: intraday resolution of prices at ten-minute intervals.

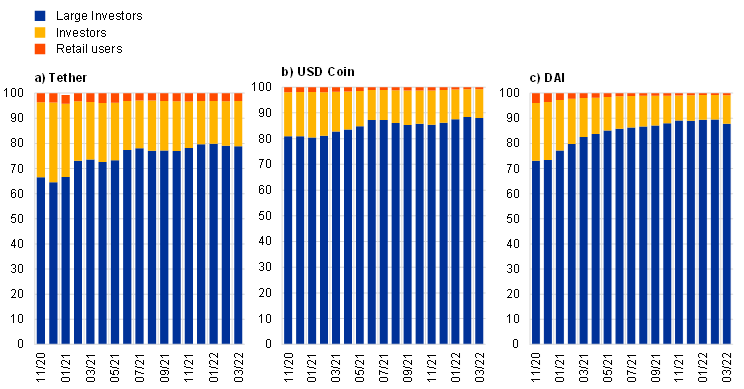

Holders of stablecoins may face losses in the event of a run on or failure of a stablecoin. Currently, holdings of Tether, USD Coin and DAI are concentrated among large investors, i.e. those holding more than 1 million coins (Chart 4). They account for more than 80-90% of the supply of these stablecoins on the Ethereum blockchain,[32] while retail investors, defined as having a balance of less than 10,000 units of each of these stablecoins, represent 3% or less. Data gaps do not allow for the identification of these large investors. Anecdotal evidence suggests that they may be specialised institutional investors, such as specialised crypto funds or hedge funds, in which case spillovers to the financial system would be limited.[33] In the specific case of TerraUSD, holders have suffered huge losses.

Growing interest by banks, PSPs and big techs in the issuance or use of stablecoins is likely to increase connections with the traditional financial system. In the United States, a consortium of banks insured by the Federal Deposit Insurance Corporation recently announced their plans to issue a stablecoin.[34] In the EU, banks and financial institutions may also be interested in issuing stablecoins or offering related services once the MiCA Regulation enters into force. In addition, the use of stablecoins may accelerate if large technology companies (big techs) start offering their own stablecoins or integrate existing stablecoins into their wallets.[35]

Chart 4

Stablecoins are mainly held by large investors

(monthly average percentage)

Sources: IntoTheBlock and ECB calculations.

Note: Large investors hold a balance of over 1 million coins, investors hold a balance of between 10,000 and 1 million coins, and retail users hold a balance of up to 10,000 coins.

Insofar as unbacked crypto-assets may pose a risk to financial stability in the future, the critical function some stablecoins play in the wider crypto-asset ecosystem is a concern for financial stability. The nature and scale of crypto-asset markets are evolving rapidly, and if current trends continue, unbacked crypto-assets will pose risks to financial stability.[36] As the analysis in Section 2 shows, stablecoins are closely intertwined with unbacked crypto-assets. If, for example, Tether were to fail, a substantial amount of trading liquidity in the crypto-asset ecosystem would dry up. This could disrupt trading and price discovery in crypto-asset markets. In turn, it could have contagion effects for the financial system if at some point in the future crypto-asset markets pose a risk to financial stability.

5 Regulating stablecoins

Given the potential risks and cross-border nature of stablecoins, a granular and robust global regulatory approach is essential. Important steps have already been taken in this direction. The Financial Stability Board (FSB) published high-level recommendations for the regulation, supervision and oversight of global stablecoins in 2020.[37] However, the FSB recommendations provide only high-level guidance. They are not granular enough on the specific requirements needed to ensure the stability of stablecoins (for example, the capital and liquidity requirements necessary for the credible management of reserve assets or public disclosure) and a level global playing field.

International standards will need to cover all relevant entities and functions in a stablecoin arrangement. Stablecoin arrangements are complex, consisting of a variety of functions and activities that in turn are performed by multiple entities across a range of sectors and jurisdictions. It will thus be important to adequately cover all relevant entities and functions in a stablecoin arrangement. Global groups such as the FSB could provide granular guidance to close gaps in areas where relevant standards or standard-setting bodies do not exist. Furthermore, the standards should ensure consistency in requirements, regardless of the sectoral origin of a stablecoin’s sponsors, functions and activities (for example, if it is issued by a bank or by other entities), in accordance with the “same business, same risk, same rule” principle.

Existing international sectoral standards may leave gaps in terms of adequately mitigating the inherent risks of stablecoins. International sectoral standards were designed at a time when stablecoins did not exist. As a result, the regulatory treatment of exposures to stablecoins and the prudential requirements to be applied when assuming any stablecoin functions/activities have yet to be determined for the different financial sectors.[38]

Given the rapid growth of the stablecoin market, stablecoins need to be brought into the regulatory perimeter with urgency. A good example is the EU’s proposed MiCA Regulation, which needs to be implemented urgently.[39] The EU is leading international efforts to put in place a new, harmonised regulatory framework for stablecoins, building on the EU e-money directive and taking into account its limitations. The MiCA Regulation is a bespoke framework for the issuance and provision of services related to stablecoins and other crypto-assets. Under this regulation, stablecoin issuers and crypto-asset service providers are subject to the same set of minimum requirements, irrespective of their applicable licensing regime. For example, e-money institutions are one of two types of issuers allowed to issue stablecoins along with credit institutions. Their requirements are overlaid with additional requirements to address the bank-like risks arising from stablecoin issuance (for example, risks related to reserve assets). To address potential systemic risks, more stringent requirements are to be applied to “significant stablecoins” that could pose a greater threat to financial stability, monetary policy transmission and monetary sovereignty. Recent events around TerraUSD underline the need to distinguish between different types of stablecoins according to the risks they pose. The idea that stability can be created in an algorithmic stablecoin with no collateral or quasi-collateral consisting of unbacked crypto-assets that have no inherent value seems to be wishful thinking. Algorithmic stablecoins should be treated as unbacked crypto-assets, according to the actual risk of their collateral or lack thereof.

6 Conclusion

Financial stability risks from stablecoins are currently still limited in the euro area, but if growth trends continue at their current pace, this may change in the future. Stablecoins have grown rapidly to become an important part of the crypto-asset ecosystem, with some posing risks to liquidity in crypto-asset markets in the event of failure. The speed and cost of stablecoin transactions, as well as their redemption terms and conditions, fall short of what is required of practical means of payment for the real economy.

Effective regulation of stablecoins is critical for responsible innovation and financial stability. Appropriate regulation, supervision and oversight need to be implemented before stablecoins become a risk to financial stability and the smooth functioning of payment systems. Existing stablecoins urgently need to be brought into the regulatory perimeter, and new ones need a regulatory framework to be established. To cater for their specific risks, algorithmic stablecoins should be treated as unbacked crypto-assets. Where stablecoins are used for payment purposes, regulatory regimes need to provide further clarity with respect to other areas such as data privacy, consumer protection, market integrity, AML/CFT and tax rules. At the international level, it will be important to ensure a level playing field globally through a consistent, granular and robust regulatory approach. This includes both the regulation of stablecoins per se and the regulation of exposures of traditional financial sectors that are interlinked with stablecoins.

References

Adachi, M., Born, A., Gschossmann, I. and van der Kraaij, A. (2021), “The expanding functions and uses of stablecoins”, Financial Stability Review, ECB, November.

Basel Committee on Banking Supervision (2021), “Prudential treatment of cryptoasset exposures”, Consultative Document, June.

Born, A., Gschossmann, I., Hodbod, A., Lambert, C. and Pellicani, A. (2022), “Decentralised finance – a new unregulated non-bank system?”, Macroprudential Bulletin, Issue 18, ECB, July.

Bullmann, D., Klemm, J. and Pinna, A. (2019), “In search for stability in crypto-assets: are stablecoins the solution?”, Occasional Paper Series, No 230, ECB, August.

Buterin, V. (2021), “Why sharding is great: demystifying the technical properties”.

ECB Crypto-Assets Task Force (2020), “Stablecoins: Implications for monetary policy, financial stability, market infrastructure and payments, and banking supervision in the euro area”, Occasional Paper Series, No 247, ECB, September.

Financial Stability Board (2022), Assessment of Risks to Financial Stability from Crypto-assets, February.

Gorton, G. and Zhang, J. (forthcoming), “Taming Wildcat Stablecoins”, University of Chicago Law Review, Vol. 90, University of Chicago Law School.

Gschossmann, I., van der Kraaij, A., Benoit, P-L. and Rocher, E. (2022), “Mining the environment – is climate risk priced into crypto-assets?”, Macroprudential Bulletin, Issue 18, ECB, July.

Hermans, L., Ianiro, A., Kochanska, U., van der Kraaij, A. and Vendrell Simón, J.M. (2022), “Decrypting financial stability risks in crypto-asset markets”, Special Feature A, Financial Stability Review, ECB, May.

Liao, G. and Caramichael, J. (2022), “Stablecoins: Growth Potential and Impact on Banking,” International Finance Discussion Papers, No 1334, Board of Governors of the Federal Reserve System, January.

Lyons, R. and Viswanath-Natraj, G. (2020), “What Keeps Stablecoins Stable?”, NBER Working Paper Series, No 27136, National Bureau of Economic Research, May.

Medalie, C., Aubert, D. and Ryder, C, (2022), “What’s Driving Tether’s De-Pegging?”, Kaiko blog, 12 May.

Mizrach, B. (2022), “Stablecoins: Survivorship, Transactions Costs and Exchange Microstructure”.

Organisation for Economic Co-operation and Development (2022), Why Decentralised Finance (DeFi) Matters and the Policy Implications, January.

The authors would like to acknowledge comments and suggestions made by Anton van der Kraaij and Patrick Papsdorf.

The term “unbacked crypto-assets” as used in this article follows the terminology of the Financial Stability Board (FSB) and includes crypto-assets that are neither tokenised traditional assets nor stablecoins. However, it does not imply that stablecoins are fully backed or backed at all by assets. See FSB (2022).

See ECB Crypto-Assets Task Force (2020) and Bullmann et al. (2019).

In this article, the category of algorithmic stablecoins also includes stablecoins that are backed by crypto-assets such as DAI, sometimes called on-chain collateralised stablecoins.

See Adachi et al. (2021).

The share of investors holding their stablecoins for longer than a month but less than a year has risen recently, suggesting they are increasingly used as a hedge against unbacked crypto-assets’ high volatility and to generate interest by using them for liquidity provision in DeFi (see, for example, Lyons and Viswanath-Natraj, 2020).

Data for trading volumes of Tether comes from CryptoCompare, whereas data for US equities comes from “Historical Market Volume Data”, Cboe Exchange, Inc.

This includes either buying bitcoin and ether with official currency or exchanging bitcoin and ether into official currency.

See “Share of Trade Volume by Pair Denomination”, The Block.

For further analysis on DeFi, see Born et al. (2022) and the references therein.

Stablecoin usage in decentralised trading is approximated based on the most liquid trading pairs of the largest decentralised exchanges (DEXes) on the Ethereum blockchain, which include the Curve, Uniswap and SushiSwap protocols. Within the three DEXes under analysis, the offered trading pairs are initially ranked by liquidity, which is defined as the total USD amount supplied from both tokens in the trading pair. We then analyse the ten most liquid pairs for each decentralised exchange. As of 17 May 2022, the sum of liquidity provided by these pairs represents approximately 80% of the total liquidity provided within the DEXes. Due to the crash of TerraUSD in early May, liquidity in DEXes declined overall and equally across the different asset types used for liquidity provision (Chart 1, panel b). The share of stablecoins for liquidity provision remained relatively stable.

Shares for Tether, USD Coin and DAI are approximated based on their respective liquidity provision to the largest DEXes (Curve, Uniswap and SushiSwap) and one of the largest lending protocols (Compound) on the Ethereum blockchain. TerraUSD’s usage in DeFi primarily entails its liquidity provision to the lending and borrowing protocol Anchor, which runs on the Avalanche and Terra blockchains. Available data sources only allowed for in-depth analyses of lending protocols and DEX trading pairs running exclusively on the Ethereum blockchain.

See, for example, Chart A, panel b in Adachi et al. (2022).

- ↑

While the non-blockchain technology could perform 1.7 million transactions per second, the high performance blockchain technology could only perform 170,000 transactions per second. For more information, see Project Hamilton.

See, for example, OECD (2022) or Mizrach (2022) for a discussion of fees on Ethereum and how it relates to the increase in transactions.

In the United States, the costs of USD Coin and DAI transactions are sometimes higher compared with the average range of payment scheme fees, ranging from 1.4% to 3.5% of the total transaction value. However, in Europe, the scheme fee, merchant service fee and interchange fee combined can be below 1% of the transaction value, making the comparison even less favourable. For data on fees in Europe, see the Scheme Fee Study by CMSPI and Zephyre in 2020.

Mizrach (2022) uses an average fee of USD 3 for out-of-network ATM transactions in the United States as a reference point.

Traditional payment accounts often have a flat fee for all credit transfer, direct debit or card transactions instead of individual transaction fees for the user. There may be specific cases such as money remittances where stablecoin transactions are attractive for payments in the EU.

For example, the supply of Tether on the Tron blockchain has now exceeded that on Ethereum, and the supply of USD Coin on Solana represents almost 10% of the total circulating supply of USD Coin.

See Gschossmann et al. (2022) for further discussion of the carbon footprint of PoW crypto-assets.

Ethereum is currently in the process of switching to PoS, which is due to be finalised by the end of 2022 (see https://ethereum.org/en/upgrades/merge/). For further information on PoS, see https://ethereum.org/en/developers/docs/consensus-mechanisms/pos/. For PoH, see https://solana.com/news/proof-of-history.

For example, bitcoin owners and miners generally continue to view PoW as the more secure and decentralised consensus mechanism, and the bitcoin network so far has not experienced security flaws or been hacked. See Buterin (2021), who refers to this trade-off as the scalability trilemma.

Tether only entitles redemptions once per week and reserves the right to delay the process in case of issues with reserve assets. USD Coin only permits redemptions during business days.

For the stablecoin E-Money Euro, the value of redemptions may be made dependent on the performance of reserves, while Tether reserves the right to in-kind redemptions of assets held in its reserves.

For example, the minimum redemption threshold for Tether is USD 100,000. See also Gorton and Zhang (forthcoming).

As defined by the FSB (2022).

See Chart B, panel a in Adachi et al. (2021)

For example, in September 2021, USD Coin moved its investment entirely to cash and cash equivalents, away from commercial paper holdings (about 10%) and positions in corporate bonds and US Treasuries.

Tether’s reserve assets included the following assets as of March 2022: cash/bank Deposits: 5.0%; US Treasury bills: 47.6%; non-US Treasury bills: 0.4%; secured loans: 3.8%; corporate bonds, Ffnds and precious metals: 4.5%; commercial paper and certificates of deposit: 24.4%; money market funds: 8.3%; other investments (incl. digital tokens): 6.0%. See Tether Assurance Consolidated Reserved Report, March 2022.

See Medalie et al. (2022).

The data for this analysis are only available for the supply of these stablecoins on the Ethereum blockchain, which represents the majority of supply in the case of USD Coin and DAI but only half of the supply in the case of Tether.

On the involvement of hedge funds or crypto funds with stablecoins, see for example https://www.bloomberg.com/news/articles/2022-03-11/hedge-fund-fir-tree-bets-big-with-short-of-stablecoin-tether.

For example, Facebook’s (Meta’s) wallet, Novi, has been launched in the United States and is partnering with an existing USD-denominated stablecoin (Pax Dollar). The move may promote stablecoins for daily payments across the Facebook ecosystem. See “Pilot Version of Novi Now Available”, Novi News, 19 October 2021.

See Hermans et al. (2022) and FSB (2022).

See Regulation, Supervision and Oversight of “Global Stablecoin” Arrangements. The FSB is currently reviewing these recommendations, including how any gaps identified could be addressed by existing frameworks.

Steps are already being taken to remediate this gap. For example, the BCBS has consulted on the prudential treatment of crypto-assets, including stablecoins (see BCBS, 2021). In addition, the FSB is considering the various regulatory and supervisory approaches that are being taken in relation to unbacked crypto-assets.

See Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on Markets in Crypto-assets, and amending Directive (EU) 2019/1937.