- THE ECB BLOG

Too leveraged to reduce emissions?

29 November 2023

This post is the second in our series accompanying COP28.

European firms need to invest in new technologies to reach carbon neutrality by 2050. This often requires them to take on debt. But what if a company is already highly leveraged? The ECB Blog looks at the relationship between firms’ indebtedness and their success in reducing emissions.

With the passage of the European Green Deal and the Fit for 55 plan, firms subject to the EU Emissions Trading System (ETS) that produce a lot of carbon emissions must drastically cut them to avoid paying large amounts for emission allowances. To achieve this, companies need to invest in low-carbon technologies and emission reduction projects. Since debt financing is the primary source of external funding for European firms, it plays a vital role in these investments. Borrowing more can help firms reduce their carbon emissions, especially given that debt financing has tax advantages. But what happens if firms have already taken on a lot of debt to finance other activities? High levels of indebtedness can make it more expensive for companies to pay down their existing debt and constrain their ability to borrow more. These firms may struggle to raise the money needed to invest in low-carbon technologies. This suggests that there may be an inverted U-shape relationship between how leveraged firms are and how much they invest in green technologies. Firms with intermediate levels of leverage would, according to this theory, perform best in transitioning towards carbon neutrality (Chart 1).

Chart 1

Theoretical relationship between firm’s leverage, investment, and transition performance

Sources and notes: The figure shows the non-linear relationship between leverage and investments, which affects the transition performance of firms: leverage can help firms to channel funding towards profitable investment opportunities to reduce their emissions, but if indebtedness becomes too high, this may hold back investments and transition performance.

Leverage is a double-edged sword

Indeed, our study of firms subject to the EU ETS over the period 2013-2019 confirms this theory. We examine the relationship between companies’ leverage – as measured by the debt-to-assets ratio – and their ability to reduce both their absolute emissions and their emissions efficiency (the revenue generated for each unit of emissions). The average leverage of firms in our sample is about 20%, but it varies across industries, being highest for manufacturing textile companies and lowest for oil and natural gas extraction companies.

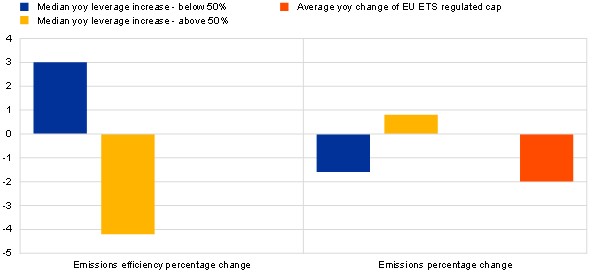

In a sample of nearly 4,000 firms which produce about a quarter of the EU’s greenhouse gas (GHG) emissions, we find that, up to a certain point, firms that are or become more leveraged significantly reduce their emissions in subsequent years. They achieve this without constraining their economic activity: they reduce their carbon footprint through cleaner production. When leverage exceeds about 50%, further increases are associated with worse performance in terms of emissions reduction, which we capture under the term “transition performance” (Chart 2). The group of firms with leverage below 50% performed significantly better than the firms with leverage above 50%. A median increase in the leverage of the first group, which amounts to 1.4%, was associated with a decrease in emissions of 1.6%. By contrast, a median increase in leverage in the already highly leveraged group, corresponding to a 4.5% rise, was associated with higher emissions – specifically, an increase of 0.8%. This finding suggests that highly leveraged firms may face challenges in undertaking profitable and green investment opportunities.

Chart 2

Magnitude of the impact of an increase in firm leverage on transition performance

Sources and notes: The figure shows the economic magnitude of the relationship between leverage and transition performance when the leverage of the median firm increases by the median yearly leverage change (in yellow, the median firm with leverage above 50% and in blue, the median firm with leverage below 50%). This is compared against the yearly average reduction in the emissions cap imposed by the EU ETS (in red). Emission efficiency is measured as the ratio between firms’ revenues and emissions, and it indicates how much revenue the firm generates for each unit of emissions.

The introduction of stricter emissions caps in the EU ETS Directive in March 2018 offers a further way to test the causal role of high indebtedness in constraining firms' capacity to reduce their carbon emissions. This policy change increased the carbon costs of all firms exceeding their emission allowance. Segmenting these firms according to their leverage, we find that highly indebted firms, with leverage above 75%, subsequently reduced their emissions by less than firms with leverage below 25%. This is despite both groups of firms having similar emission trends prior to the policy change. So high leverage does indeed appear to hamper firms’ efforts to cut their emissions in the face of rising carbon costs. It also suggests that there is a group of European firms that is too leveraged to finance their green transition. For these firms, the EU ETS might not be sufficient on its own to incentivise emissions reduction.

Green debt markets can support the transition

How can highly indebted firms finance emission-reducing investments in the face of increasing carbon costs? Research suggests that green debt – borrowing that is explicitly tied to green investment – helps firms to reduce their carbon emissions. Further improving green bond and loan markets, for example through greater transparency and international standards, should support the low-carbon transition. Investor appetite for green debt is strong and growing, which gives more highly-leveraged companies the chance to borrow at reasonable premiums for their green investments. By earmarking funds for green investments, such companies may also find it easier and cheaper to access finance despite struggling to increase borrowing more generally as lenders may be more confident that their finance will increase the profitability and financial stability of the companies over the medium term.

This may also be supported by tax incentives, such as making the tax advantages of debt financing only applicable to green debt. Firms with high leverage and low growth prospects may still have to cede the market to more emission-efficient firms. But greater availability and stronger standards for green debt instruments could help firms with high leverage and high growth prospects to get the necessary financing for the green transition.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.