Eurosystem staff macroeconomic projections for the euro area, June 2020

Overview

The coronavirus (COVID-19) pandemic has dramatically affected global economic activity since taking hold in early 2020 and the euro area economy is no exception. Mainly due to the strict lockdown measures implemented in most euro area countries around mid-March, euro area real GDP registered a record decline of 3.8% in the first quarter of 2020. A further decline in GDP of 13% is expected for the second quarter even though most countries have started to loosen their strict lockdowns. What will happen after that is subject to unprecedented uncertainty.

The baseline rests upon a set of key assumptions about the future evolution of the pandemic as well as the necessary containment measures and the behaviour of households and enterprises. Namely, the baseline assumes only partial success in containing the virus, with some resurgence in infections over the coming quarters, necessitating persistent containment measures until a medical solution becomes available, which is assumed to happen by mid-2021. These containment measures are expected to weigh on supply and demand. Elevated uncertainty and worsened labour market conditions are expected to induce households and firms to cut back their spending further. Substantial support from monetary, fiscal and labour market policies should help maintain incomes and limit the economic scars the health crisis would leave behind. Such policies are also assumed to be successful in preventing adverse amplifications through financial channels. Under these assumptions, real GDP in the euro area is projected to fall by 8.7% in 2020 and to rebound by 5.2% in 2021 and by 3.3% in 2022. This implies that by the end of the projection horizon, the level of real GDP would be around 4% below its level expected in the March 2020 staff projections.

The recent collapse in oil prices implies a sharp drop in HICP inflation to levels around zero for the coming quarters. Base effects in the energy component would then cause a mechanical rebound in early 2021. HICP inflation excluding energy and food is also expected to decline over the short-term but by less than headline inflation. Disinflationary effects are expected to be broad-based across the prices of services and goods as demand will remain weak. However, these effects are expected to be partly offset by cost and price pressures related to supply side disruptions and shortages. Over the medium term, inflation is expected to increase as it is assumed that the oil price will pick up and as demand recovers. Overall, the baseline foresees HICP inflation declining from 1.2% in 2019 to 0.3% in 2020 and rising to 0.8% and 1.3% in 2021 and 2022, respectively.[1]

In view of the unprecedented uncertainty about the evolution of the pandemic and its impact on economic behaviour, as well as the associated containment measures and the success of the policy measures, two alternative scenarios have been prepared. The mild scenario sees the shock as temporary, with a fast and successful containment of the virus allowing restrictions to be removed swiftly. In this scenario, real GDP would decline by 5.9% this year, followed by a strong rebound in 2021. By the end of the horizon, real GDP would almost reach the level of the March 2020 staff projections. Inflation in this scenario would reach 1.7% by 2022. In contrast, a severe scenario, with a strong resurgence of infections, implies more stringent containment measures that significantly weigh on economic activity. In this scenario, real GDP falls by 12.6% in 2020 and, by the end of the projection horizon, stands around 9½ % below its level in the March 2020 staff projections, with the inflation rate at only 0.9% in 2022.

1 Key assumptions and policy measures underlying the projections

The baseline rests on a number of critical assumptions concerning the evolution of the pandemic. As the strict lockdowns are gradually relaxed across euro area countries, the baseline assumes only partial success in containing the virus, with some resurgence in infections over the next few quarters, requiring persistent containment measures. Nevertheless, the latter are expected to entail lower economic costs than those during the initial strict lockdowns, due to learning and behavioural responses by authorities and economic agents. The economy is expected to be revived gradually, in phases, during the post-lockdown “transition” period. The main focus is expected to be on manufacturing and certain services sectors, while other services, e.g. the arts, entertainment, accommodation and recreation, would continue to be partly restricted. The transition period lasts until a medical solution becomes available, which is assumed to happen by mid-2021.

Similar assumptions about the evolution of the pandemic underlie the international projections which suggest a collapse in euro area foreign demand in 2020. Global real GDP (excluding the euro area) is projected to decline by 4% in 2020 before rebounding by 6% in 2021 and 3.9% in 2022. Global trade will be more adversely affected than global GDP, as logistic disruptions and closed borders amplify the impact. Moreover, trade developments tend to respond more strongly to economic activity in economic downturns. As a result, euro area foreign demand is expected to fall by 15.1% in 2020 and then to grow by 7.8% and 4.2% in 2021 and 2022 respectively.

Significant monetary, fiscal and labour market policy measures will help support incomes, reduce job losses and bankruptcies, and will also succeed in containing adverse real-financial feedback loops. In addition to the monetary policy measures taken by the ECB since March 2020, the baseline includes discretionary fiscal measures amounting to 3.5% of GDP in 2020. These measures include extensive short-time work schemes and wage subsidies which should cushion the impact of the collapse in activity on employment and labour incomes. Firms receive substantial subsidies and capital transfers. Almost all the currently implemented emergency fiscal measures are, however, assumed to be temporary and to expire by the end of 2020, thereby implying a drag on the subsequent recovery.[2] In addition, loans and guarantees or capital injections, partly or wholly provided by governments and amounting to a total envelope of close to 20% of GDP, should contribute to alleviating liquidity constraints. Importantly, both the monetary policy measures as well as the government credit and capital instruments act as backstops, reducing the tail risks of adverse real-financial feedback loops.

2 Real economy

Real GDP registered an unprecedented decline in the first quarter of 2020. According to the Eurostat flash estimate, real GDP fell by 3.8% in the first quarter of 2020, bringing an end to almost seven years of expansion. Nearly all euro area countries recorded negative quarterly growth rates in that quarter, in particular France, Italy and Spain, among the larger euro area countries.[3] The decline in activity in the first quarter was the steepest recorded to date. Available data suggest that retail trade, transport, as well as arts, entertainment and recreation activities incurred the largest losses, albeit to a different extent across countries.

Chart 1

Euro area real GDP

(quarter-on-quarter percentage changes, seasonally and working day-adjusted quarterly data)

Note: This chart does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, in order to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Box 3.

Forward-looking indicators suggest an even steeper decline in activity in the second quarter of 2020. Surveys compiled by the European Commission as well as the Purchasing Managers’ Indices have fallen to close to, and in many cases below, historical troughs. The composite output PMI collapsed to 13.6 in April and, despite recovering to 31.9 in May, it signals a much worse decline in real GDP than during the financial crisis in 2008-09. High frequency indicators, such as electricity consumption and GPS-based mobility indicators, suggest steep declines in activity in April in most euro area countries. While they have started to recover recently, as the euro area countries have started to gradually lift the strict lockdowns, these indicators still point to a strong fall in real GDP in the second quarter. Overall, activity in the second quarter is expected to fall by 13%.

Despite ongoing containment measures, a rebound in activity is projected to start in the second half of 2020. National authorities are assumed to loosen and improve the efficiency of the containment measures and allow businesses across sectors to restart production. Therefore an 8.3% rebound in real GDP is projected for the third quarter, with a recovery in foreign demand, supportive policies and some pent-up demand continuing to stimulate activity thereafter. Nevertheless, some ongoing containment measures and an only gradual waning of high uncertainty will continue to constrain economic activity until a medical solution becomes available, which is assumed to happen by mid-2021. As a result, real GDP will only gradually recover towards pre-crisis levels. This implies that, by the end of the projection horizon, real GDP would stand around 4% below the level expected in the March 2020 staff projections.

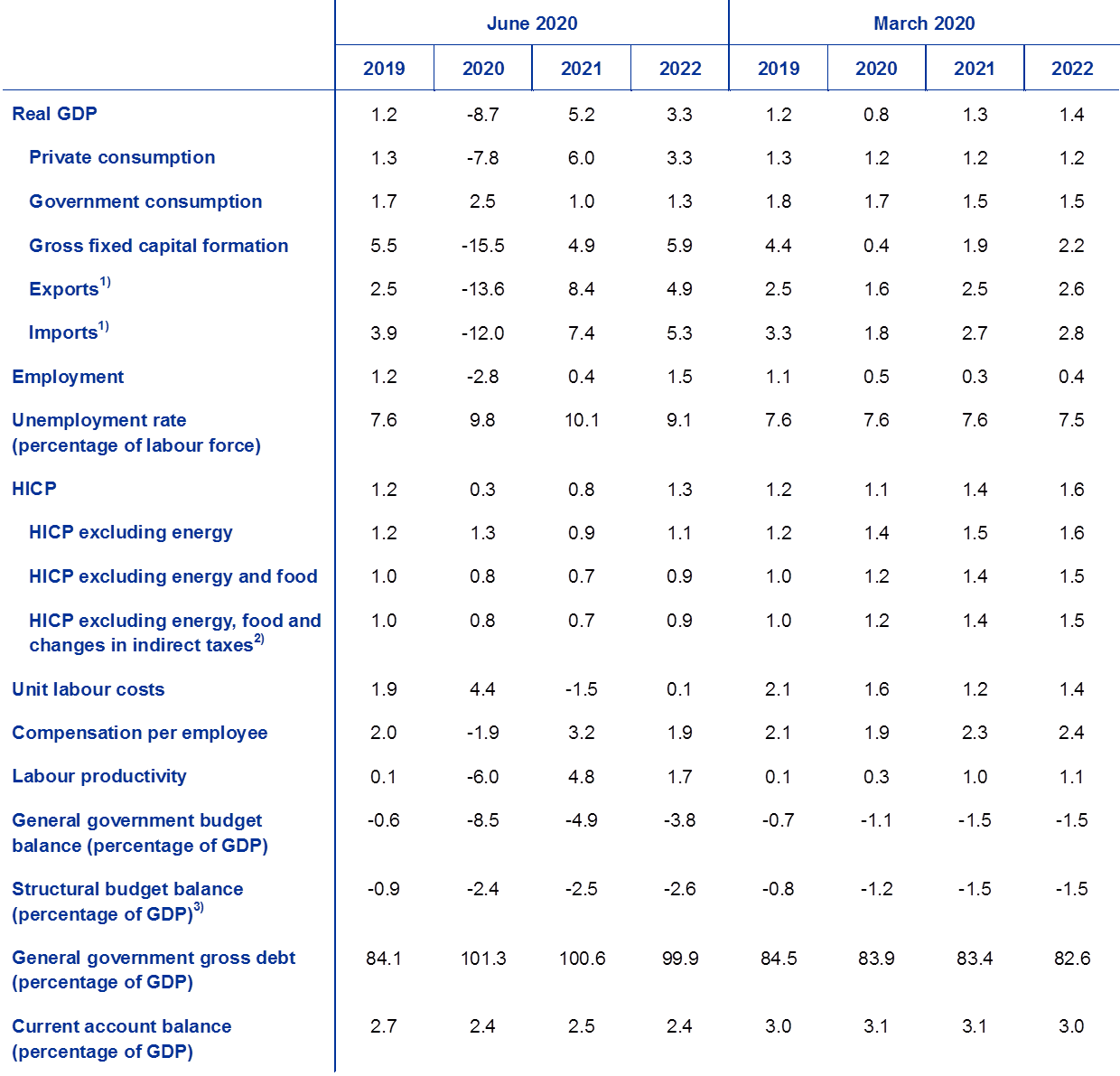

Table 1

Macroeconomic projections for the euro area

(annual percentage changes)

Note: Real GDP and components, unit labour costs, compensation per employee and labour productivity refer to seasonally and working day-adjusted data. This table does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, in order to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Box 3.

1) This includes intra-euro area trade.

2) The sub-index is based on estimates of actual impacts of indirect taxes. This may differ from Eurostat data, which assume a full and immediate pass-through of tax impacts to the HICP.

3) Calculated as the government balance net of transitory effects of the economic cycle and temporary measures taken by governments. The structural balance does not reflect the budgetary impact from temporary measures related to the COVID-19 pandemic.

Turning in more detail to the components of GDP, private consumption is expected to decline by 7.8% in 2020 and recover gradually by 2022. Private consumption is estimated to have declined steeply in the first half of 2020. At the sectoral level, sales of motor vehicles as well as spending on holidays and restaurants have been hit the hardest. While losses in real disposable income have partly been cushioned by public transfers, the decline in consumption stems from a combination of enforced savings (as households whose income was unaffected were not able to buy non-essential goods and services) and precautionary savings in the context of a steep decline in consumer confidence and an unprecedented increase in uncertainty about the economic outlook. Looking forward, as countries gradually loosen the lockdown measures, private consumption is expected to rebound from the second half of 2020 onwards but only surpass its pre-crisis level during the course of 2022. This rebound is supported by an expected gradual decline in uncertainty as well as the unwinding of some pent-up demand. At the same time, elevated unemployment and an unwinding of net fiscal transfers will act as a drag on the recovery.

Box 1

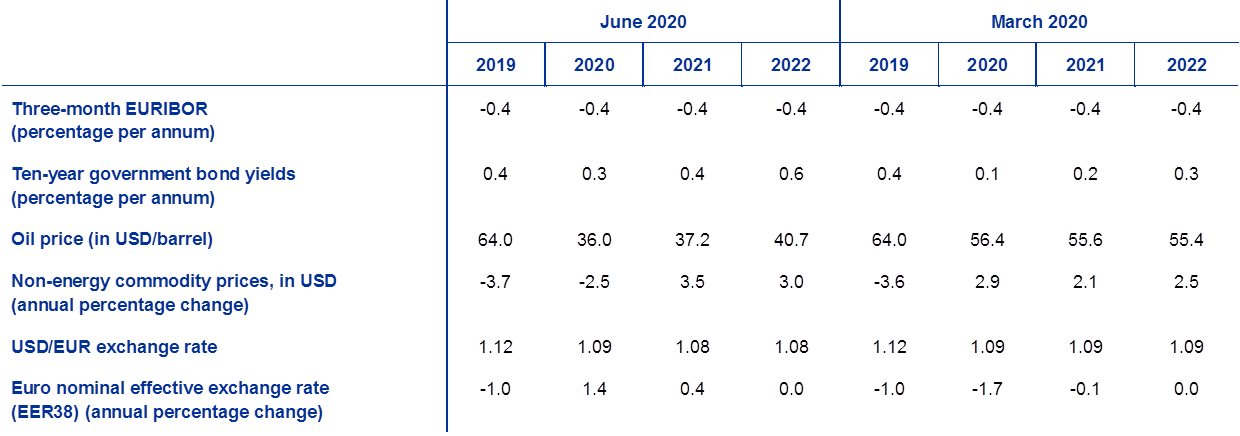

Technical assumptions about interest rates, exchange rates and commodity prices

Compared with the March 2020 staff projections, the technical assumptions include significantly lower oil and stock prices, a stronger effective exchange rate of the euro and higher long-term interest rates. The technical assumptions about interest rates and commodity prices are based on market expectations with a cut-off date of 18 May 2020. Short-term interest rates refer to the three-month EURIBOR, with market expectations derived from futures rates. The methodology gives an average level for these short-term interest rates of -0.4% over the entire projection horizon. The market expectations for euro area ten-year nominal government bond yields imply an average level of 0.3% for 2020, 0.4% for 2021 and 0.6% for 2022.[4] Compared with the March 2020 staff projections, market expectations for short-term interest rates remain broadly unchanged, while euro area ten-year nominal government bond yields have been revised up by around 20 basis points for 2020-22.

As regards commodity prices, we consider the path implied by futures markets by taking the average of the two-week period ending on the cut-off date of 18 May 2020. On this basis, the price of a barrel of Brent crude oil is assumed to decline from USD 64.0 in 2019 to USD 36 in 2020 and to increase to USD 40.7 by 2022. This path implies that, in comparison with the March 2020 staff projections, oil prices in US dollars are significantly lower over the entire horizon. The prices of non-energy commodities in US dollars are estimated to decline further in 2020 and to rebound over the subsequent years.

Bilateral exchange rates are assumed to remain unchanged over the projection horizon at the average levels prevailing in the two-week period ending on the cut-off date of 18 May 2020. This implies an average exchange rate of USD 1.08 per euro over the period 2021-22, which is slightly lower than in the March 2020 staff projections. The effective exchange rate of the euro (against 38 trading partners) has appreciated by 3.6% since the March 2020 staff projections.

Technical assumptions

A sharp and sudden contraction in housing investment is expected for 2020. Housing supply is expected to be severely hit by the COVID-19 shock in 2020. The adverse effects on housing demand of lower disposable income, weaker consumer confidence and higher unemployment are expected to lead to persistently subdued housing investment. At the end of the projection horizon, it is expected to stand well below its pre-crisis level.

Business investment is expected to collapse in 2020, falling much more sharply than GDP, recovering only gradually and remaining well below pre-crisis levels until 2022. Business investment is estimated to have collapsed in the first half of 2020 because of the lockdowns, vanishing global and domestic demand, and soaring uncertainty. A rebound is expected to start in the second half of 2020, with the speed of the recovery diverging substantially across countries, reflecting the differences in the size of the initial collapse. Faced with heightened uncertainty, firms are likely to postpone investment. As such, business investment for the euro area is expected to stand well below its pre-crisis level at the end of the projection horizon. It is projected to remain subdued due to elevated levels of spare capacity and concerns about longer-term demand trends in aging and shrinking populations. At the same time, the gross indebtedness of non-financial corporations (NFCs) is projected to increase significantly in 2020, from an already elevated level, before declining moderately. The initial increase in NFC gross indebtedness is attributable to the marked fall in corporate profits in the first half of 2020 and the resulting increased recourse to debt financing to compensate for liquidity shortfalls. The observed increase in the corporate debt ratio is expected to limit business investment growth over the projection horizon, as firms have to restore the health of their balance sheets. Nevertheless, NFCs gross interest payments have declined to record low levels in the past years and are expected to increase only gradually in the next few years, easing possible debt sustainability concerns.

Box 2

The international environment

The COVID-19 pandemic has paralysed the global economy. Measures taken by governments across the globe to contain the spread of the virus imply sharply declining economic activity in the near term. Such measures were introduced in China as early as late January, while other countries enacted them later, as the virus spread around the world. While several countries have recently started easing strict containment measures, this process is likely to be very gradual. Economic activity, especially in emerging market economies (EMEs), is also being adversely affected by sharply lower commodity prices, tighter financial conditions and substantial capital outflows. These severe global shocks hit the world economy at a time when signs of stabilisation, following a period of lacklustre performance last year, were increasingly evident. In particular, a nascent recovery in manufacturing activity and trade led by large EMEs had been under way at the turn of the year. Moreover, favourable global financial conditions at the time, as well as a partial de-escalation of the trade conflict between the United States and China following the signing of the “phase-one” deal, had the potential to strengthen this recovery before the pandemic struck.

Survey data confirm that the economic fallout of the pandemic and containment measures will be heavy and far-reaching. Looking at sectoral PMI data, three patterns emerge. First, output across sectors plummeted as stringent containment measures were put in place. Second, the impact on the services sector was greater than that on manufacturing. As the measures to contain the virus suppress demand and supply globally, sectoral output in both manufacturing and services has deteriorated much more rapidly now than in the global financial crisis. Third, as production resumes, output recovers from its depressed levels. Yet, for several reasons this recovery is only partial. Restrictions are still in place for businesses requiring close social interaction, consumer behaviour has changed amid worries about a second wave of infections, and high uncertainty is hindering investment decisions, which in turn lowers demand in the near term and weighs on productive capacity further ahead.

The pandemic and related strict containment measures have triggered a synchronised and deep global recession. Sectoral value-added data have been used to quantify the potential economic losses resulting from these measures for key advanced economies and EMEs. The strict containment measures were implemented in line with government announcements regarding their modalities, including, among other things, their timing, duration and severity in each country.

In 2020 as a whole, world real GDP excluding the euro area is projected to decline by 4.0%. This pace of contraction is faster, and its magnitude much larger, than during the global financial crisis of 2008-09. As a result, activity will decline sharply in the first two quarters of this year and is projected to recover as of the third quarter. As strict containment measures are lifted, it will rebound initially, but the pace of recovery will be more gradual in the following quarters. This profile implies that world real GDP excluding the euro area is projected to increase by 6.0% in 2021 and 3.9% in 2022. Compared to the March 2020 staff projections, global growth has been revised significantly down for this year, while growth over the medium-term horizon is expected to be slightly stronger. These revisions also imply that the level of global output remains below the trajectory projected in the March 2020 staff projections. For EMEs, a more subdued economic recovery is projected compared to previous downturns. This reflects a combination of negative shocks affecting them at the current juncture, including the health crisis, tight financial conditions, negative terms of trade shocks for commodity exporters, and substantial capital outflows.

Global trade will be affected more severely, as logistic disruptions and closed borders amplify the impact of falling supply and demand. Moreover, trade developments tend to respond more to economic activity, especially in downturns. As a result, global real imports excluding the euro area are projected to decline by 12.9% this year, before increasing by 8.0% and 4.3% in 2021 and 2022, respectively. Euro area foreign demand is projected to contract by 15.1% this year and grow by 7.8% and 4.2% in 2021 and 2022, respectively. The impact of the pandemic on trade is substantial, with world imports excluding the euro area projected to return to their levels of the fourth quarter of 2019 only towards the end of the projection horizon. Euro area foreign demand remains below this level over the whole projection horizon.

The international environment

(annual percentage changes)

1) Calculated as a weighted average of imports.

2) Calculated as a weighted average of imports of euro area trading partners.

Euro area exports are projected to be severely affected by the COVID-19 pandemic in 2020 and expected to recover most of the losses by the end of the projection horizon, starting from a low level reflecting trade tensions and weak foreign demand. Exports are projected to be severely impacted in the first half of 2020. Lockdown measures to contain the pandemic heavily affected the export sector of the euro area, as well as imports. Most sectors experienced a rapid decline in their exports at the end of the first quarter of 2020 which is expected to continue into the second quarter. Exports of travel and transport services are among the most affected by the pandemic. Supply chain disruptions linked to the COVID-19 outbreak have particularly affected the export-oriented automotive, machinery and chemical sectors. Imports are expected to decline less than exports in the second quarter of 2020, as major exporters are particularly badly affected by the global drop in demand for automobiles and investment goods. Therefore net exports should be negative. From the third quarter onwards, the rebound in exports is somewhat stronger than in imports, implying a positive contribution of net exports until the end of 2021, as the global cyclical sectors to which the euro area is exposed recover. Overall, euro area exports are expected to develop broadly in line with euro area foreign demand.

The labour market situation is expected to worsen substantially. While labour market conditions improved notably during the recent expansion, a sharp worsening is expected to materialise during the course of 2020. The decline in headline employment by 0.2% in the first quarter of 2020 according to Eurostat’s flash estimate is only a harbinger of markedly worse developments expected over the next few quarters. While the decline in employment in terms of persons is likely to be cushioned in some countries by an extensive recourse to short-time work schemes, total employment is expected to decline by 2.8% in 2020 before recovering gradually over the remainder of the projection horizon, thanks to a rebound in activity.

Total hours worked are projected to better track developments in the labour market during the COVID-19 pandemic than employment in terms of persons. Total hours worked per person are projected to reach a deep trough in the second quarter of 2020, while employment in terms of persons is projected to reach a less deep trough in the third quarter of 2020. The more limited impact of the crisis on employment developments in terms of persons is partly due to compensating labour market policies. Both total hours worked and employment in terms of persons stand at the end of the projection horizon somewhat below their levels in the fourth quarter of 2019. This is on account of hysteresis effects (e.g. due to firm bankruptcies and permanent job losses) in the euro area labour market.

The impact of the COVID-19 pandemic on labour force growth is expected to be moderate over the projection horizon. The labour force is expected to decline until the third quarter of 2020. In the very short term, the decline reflects that a share of employed workers will exit from the labour force due to the lockdowns – including the fact that some workers may be classified as available to work but as not seeking employment because of the related lockdown measures. Also, a reduction in hiring opportunities during the pandemic period may lead to discouragement, resulting in persons moving out of the labour force. Additional channels may also adversely impact the labour force, especially in the short term, such as a reduction in the projected net immigration of workers due to the COVID-19 pandemic and restrictions on international flights.

The unemployment rate is expected to react to the pandemic and peak at 10.8% in the third quarter of 2020. Similarly to the profile of employment, the unemployment rate is not projected to return to its pre-crisis level over the projection horizon, reaching 8.8% in the fourth quarter of 2022 (compared to levels of 7.3% in the fourth quarter of 2019). The trajectory of the projection for the unemployment rate remains below the path observed during the global financial crisis of 2008-09, due to the impact of the labour market policies adopted, which have focused on preserving jobs with a view to quickly restarting business operations after the end of the strict lockdown measures. In particular, short-time work schemes have limited spells of unemployment, with employees remaining on the firm payroll and receiving resources comparable to unemployment benefit schemes (with replacement ratios of the foregone wage varying across countries). Unemployment rates are expected to continue to exhibit substantial differences across the euro area countries. Overall, countries with a high share of temporary or self-employed workers are expected to witness a higher toll on unemployment rates and income losses.

Labour productivity growth is projected to decline in 2020 and then recover over the projection horizon. Given the fiscal measures that cushion the impact on headline employment, labour productivity per person is projected to decline sharply in 2020. There is a differential impact between labour productivity per person employed and labour productivity per hour worked. Productivity per person employed is more adversely affected in 2020, reflecting the large-scale use of short-time working schemes in euro area countries. By contrast, the response in productivity per hour worked is much more muted during the pandemic, as total hours worked are expected to closely follow GDP developments.

Compared with the March 2020 staff projections, the projection for real GDP growth has been revised downwards dramatically in 2020 and upwards for the rest of the horizon, especially in 2021. The downward revision in real GDP growth in 2020 masks a stronger downward revision in the first half of the year and some upward revisions in the second half. The resulting positive statistical carry-over effect, as well as some further catching up, implies an upward revision of real GDP growth in 2021 and in 2022. By the end of the projection horizon, real GDP would stand around 4% lower than projected in the March 2020 staff projections.

Box 3

Alternative scenarios for the euro area economic outlook

The high uncertainty surrounding the impact of the COVID-19 pandemic on the euro area economic outlook warrants an analysis based on alternative scenarios. This Box outlines two scenarios, representing alternatives to the June 2020 staff projections baseline, to illustrate the range of possible impacts of the COVID-19 pandemic on the euro area economy. These scenarios can be seen as providing an illustrative range around the baseline projection.

The scenarios vary according to a number of factors. These factors include the impact of the strict lockdown measures on economic activity, the behavioural responses by economic agents to minimise the initial strong economic disruptions, the economic effects of protracted containment measures during the post-lockdown transition period, and the longer-lasting effects on economic activity once all containment measures have been lifted. The broad narratives for the development of the aforementioned factors also determine the scenario-specific projections for euro area foreign demand as well as lending rates and fiscal policy responses.

The mild scenario assumes a successful containment of the virus, while the severe scenario assumes a strong resurgence of infections and an extension of strict containment measures until mid-2021. In the mild scenario, the strict lockdown period is followed by a gradual restart of the economies. The successful containment of the spread of the virus during the post-lockdown transition period is due to possible rapid advances in medical treatments and solutions, thus paving the way for a gradual return to normal activity. The mild scenario assumes no resurgence of the virus and very successful economic responses by authorities and economic agents. In the severe scenario, the strict lockdown period is assumed to have a more damaging impact on economic activity and is not successful in effectively containing the disease. Stringent, albeit gradually loosened, containment measures would remain in place during the post-lockdown transition period. The severe scenario envisages a strong resurgence of the virus, without necessarily speculating on its exact timing. A strong second wave of the virus would require stringent containment measures to be kept in place, but their economic costs would be lower than those of the initial strict lockdowns, due to learning and behavioural responses by the authorities and economic agents. The sustained efforts to prevent the spread of the virus would continue to dampen activity across sectors of the economy more strongly than in the baseline until a medical solution becomes available, which is assumed to happen by mid-2021. The weakness in activity across sectors is to some extent amplified by increased insolvencies, which lead to credit frictions that adversely affect the borrowing costs of households and firms.

These scenarios for the euro area are based on the same broad narratives for the global economy and thus for euro area foreign demand. The containment measures enforced by countries worldwide severely affect global economic activity and strongly curtail global trade. The COVID-19 pandemic and its fallout imply large losses in global real GDP. As a result of the high procyclicality of global trade with respect to global activity, euro area foreign demand would fall in 2020 by around 8% and 22% under the mild and the severe scenarios, respectively. Looking further ahead, under the severe scenario losses in euro area foreign demand persist up to the end of 2022 compared to its level at the end of 2019.

Compared with the severe scenario, the mild scenario entails both a smaller drop in economic activity in the second quarter and a stronger recovery in the third quarter (see Chart A). Real GDP would drop by around 10% and 16% in the second quarter under the mild and the severe scenarios, respectively. This would be followed by a recovery entailing quarterly growth rates of around 10% and 5% in the third quarter, respectively, and about 3% in the fourth quarter in both scenarios. The weaker rebound under the severe scenario is because it assumes stricter containment measures than in the mild scenario and in the baseline, which would be necessary in view of the very limited success in containing the virus and its strong resurgence.

Chart A

Alternative scenarios for real GDP and HICP inflation in the euro area

(index: Q4 2019 = 100 (left-hand chart); year-on-year rate (right-hand chart)

Real GDP is projected to rebound, on average over 2021-22, more strongly under the mild scenario than under the severe one (see Table A). This reflects the normalisation of activity, following the successful containment of the virus in the mild scenario. In contrast, in the severe scenario the uncertain epidemiology of the virus, the limited effectiveness of containment measures and the assumed persistent economic damage would continue to weigh on economic activity throughout the horizon. Real GDP is projected in 2022 to recover close to the level projected in the March 2020 staff projections in the mild scenario, while standing well below that level in the severe scenario (about 9½% lower).

Table A

Alternative macroeconomic scenarios for the euro area

Euro area labour markets would recover under the mild scenario, as policies largely succeed in preventing hysteresis effects that are only partially contained in the severe scenario. In both scenarios, employment will not fully recover back to its level in the March 2020 staff projections over the projection horizon. Compared to pre-crisis levels, employment losses are expected to be reabsorbed in the mild scenario, while in the severe scenario employment will not recover by the end of the projection horizon. Similarly to the profile of employment, in the severe scenario, the unemployment rate is not projected to return to its pre-crisis level. However it would come close to that level in the mild scenario by the end of 2022.

As regards HICP inflation, there is little difference between the two scenarios in the short term. This is mainly for two reasons. First, the oil price developments are assumed to follow the same path as the baseline in both scenarios and so they have a similarly strong downward impact through energy inflation. Second, underlying inflation shows marked persistence, as typically observed in the early stages of an economic downturn. As long as the downturn is expected to be relatively short-lived, there may be little inclination to immediately change price-setting – irrespective of the depth of the downturn. In 2020, headline inflation declines to 0.4% and 0.2% in the mild and severe scenarios, respectively.

Beyond the short term, inflation varies more between the two scenarios due to different real economic conditions. The shape of the real GDP path implies that in the mild scenario the economic slack associated with the downturn will largely unwind over the projection horizon, while this will only partly be the case in the severe scenario. Both downward demand and upward supply effects on inflation are expected to be larger in the severe than the mild scenario. However, excess supply is envisaged as rising much more in the severe scenario than in the mild one. HICP inflation excluding energy and food is therefore expected to return relatively quickly to a mean-reversion path in the mild scenario, while the severe scenario implies more protracted weakness in HICP inflation excluding energy and food. The assumption-driven rebound in energy inflation, by contrast, operates similarly in both scenarios. Overall, HICP inflation is projected to average 1.1% and 1.7% in 2021 and 2022 in the case of the mild scenario, and 0.4% and 0.9% in the respective years in the severe scenario.

These illustrative scenarios abstract from a number of factors that may also influence the magnitude of the recession and the subsequent recovery in the euro area. These scenarios have been prepared under the same market-based assumptions applied in the ECB/Eurosystem staff macroeconomic projections for monetary policy, stock prices, commodity prices and exchange rates. In addition, adverse real-financial feedback spirals are, to varying degrees, treated as being broadly contained by economic policy measures. Finally, although the announced fiscal measures included in the baseline are re-scaled in the scenarios, so as to better reflect the expected fiscal policy support in 2020, the same fiscal measures are broadly assumed across scenarios for the outer years.

3 Prices and costs

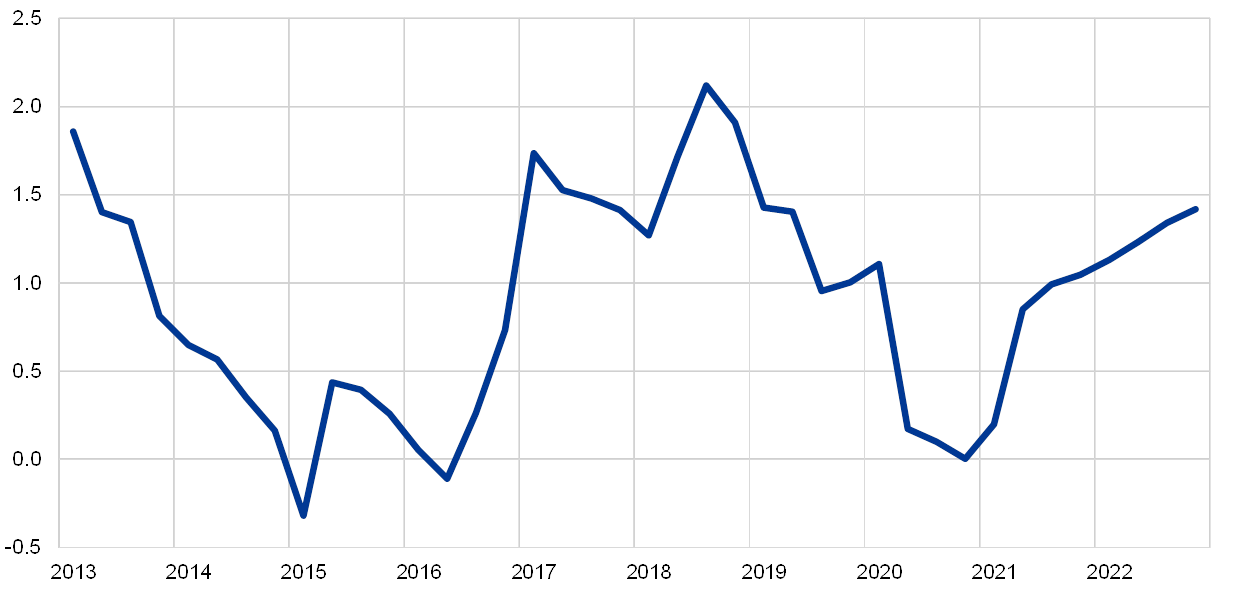

HICP inflation is expected to decline from 1.2% in 2019 to 0.3% in 2020, then rise to 0.8% and 1.3% in 2021 and 2022, respectively (see Chart 2). The weaker headline inflation rate in 2020 reflects, in particular, a sharp drop in HICP energy prices, given the fall in oil prices after the global COVID-19 outbreak. HICP energy inflation is expected to provide a large negative contribution of 0.8 percentage points to headline inflation in 2020. Increases in oil prices, as indicated by the positive slope of the oil price futures curve and some upward effects from energy related indirect tax increases, imply a rise in HICP energy inflation over the remainder of the projection horizon. HICP food inflation has increased significantly recently, as households’ demand for processed and unprocessed food rose in the context of the COVID-19 related containment measures and as some supply chain disruptions for fresh food emerged. Food price inflation is expected to remain elevated in the short term but to decrease in the course of the year and record lower rates in 2021 and 2022 than in 2020.

Given the significant increase in economic slack and the indirect effects of the steep fall in oil prices, HICP inflation excluding energy and food is expected to moderate to 0.8% on average in 2020 and to pick up only towards the end of the projection horizon. Declining but still ample economic slack is expected to weigh on HICP inflation excluding energy and food in 2021 and to a lesser extent in 2022, implying average annual inflation rates of 0.7% and 0.9%, respectively. Disinflationary effects are expected to be broad-based across the prices of services and goods, as consumer demand will remain weak due to income losses or hampered by government measures to contain the spread of the virus. Over the next few quarters, the downward pressures from weak demand are expected to be partly offset by price and cost pressures from supply side disruptions and shortages arising from, for example, disruptions in global value chains, or from social distancing measures in place (such as reducing the capacities of hairdressers and restaurants). Over the medium term, HICP inflation excluding energy and food is expected to pick up, with upward price pressures from rising demand expected to strengthen as the economic recovery progresses. While upward pressures from adverse supply side effects linked to the pandemic should diminish, pent-up demand and lower competition due to the exit of firms could push up markups in some markets beyond their cyclical improvements. In addition, indirect effects from the assumed increase in oil prices will contribute to the pick-up in underlying inflation.

Chart 2

Euro area HICP

(year-on-year percentage changes)

Note: This chart does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, in order to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Box 3.

Growth in compensation per employee is projected to turn negative in the short term, but to recover in line with economic activity in 2021 and display moderate growth rates in 2022. Compensation per employee is expected to decrease sharply in the second quarter of 2020. This reflects the massive and abrupt drop in hours worked per employee during the lockdowns and the only partial offset of the compensation losses by short-time work schemes. However, the developments in compensation per employee exaggerate the loss in labour income, as a number of countries do not statistically record the government support under compensation but under transfers. Subsequently, with the recovery in economic activity and in hours worked per employee, compensation per employee is expected to bounce back and to gradually rise further over the projection horizon. In terms of annual growth rates, these developments imply a sharp drop in growth in compensation per employee in 2020 to -1.9%, a bounce back to 3.2% in 2021 and more moderate growth in compensation per employee of 1.9% in 2022.

Growth in unit labour costs is projected to be subject to strong fluctuations over the projection horizon, reflecting the sharp movements in labour productivity growth. The loss in labour productivity in the second quarter of 2020 due to the large fall in real GDP relative to the smaller drop in employment pushes up unit labour costs significantly, and the subsequent rebound in labour productivity implies a strong fall in unit labour costs. Beyond the crisis-related volatility, unit labour costs are expected to rise only very slightly.

Profit margins are expected to broadly buffer the strong swings in unit labour costs over the projection horizon. As a result, they are envisaged to drop sharply in the second quarter of 2020 and bounce back markedly thereafter. A return to the pre-crisis level is expected towards the end of the projection horizon.

Import prices are expected to fall notably in 2020 but to rebound somewhat in 2021 and 2022. This profile is strongly determined by movements in oil prices, for which the slope of the oil price futures curve implies a large negative growth rate in 2020 but positive annual rates as of the second quarter of 2021 and in 2022. The positive import price inflation rates as of 2021 also reflect some upward price pressures from both non-oil commodity prices and rising underlying global price developments more generally.

Compared with the March 2020 staff projections, the outlook for HICP inflation is revised down significantly over the projection horizon. Strong downward effects on headline inflation from the lower oil price assumptions in 2020 are only partly offset by higher than previously expected developments in HICP food inflation related to the COVID-19 crisis. HICP inflation excluding energy and food is revised down notably over the whole projection horizon. It is dampened by the much larger than previously expected economic slack and, in the first part of the projection horizon, also by some downward indirect effects from the lower oil price assumptions.

4 Fiscal outlook

The fiscal stance[5] is assessed to become highly accommodative in 2020. This is mostly underpinned by the substantial fiscal measures which have been taken by all euro area countries in response to the pandemic. The biggest part of these measures is additional spending, in particular in the form of short-time work schemes, measures to support firms and households, as well as higher spending on health. Most of the pandemic-related measures recently implemented are temporary and expire at the end of 2020. Consequently, the fiscal stance for 2021 indicates a substantial tightening. In 2022, the measures related to the pandemic are assumed to have only a small impact on the fiscal stance, which is projected to be somewhat expansionary. Compared with the March 2020 staff projections, the inclusion of the new measures resulted in a much more expansionary fiscal stance in 2020 and a more contractionary one in 2021, while the revision for 2022 is limited.

The euro area budget balance is projected to decline substantially in 2020 and to recover somewhat in 2021 and 2022. The strong decline in the budget balance in 2020 stems from the fiscal emergency measures and the negative cyclical component, which reflects the worsening of the macroeconomic outlook. The improvement in 2021 mainly reflects the unwinding of the fiscal emergency measures, while the less detrimental cyclical component also has a somewhat positive effect. The surge in the debt ratio in 2020 to more than 100% of GDP is mostly due to a debt-increasing interest-growth differential as well as the high primary deficit. In 2021-22, the debt-increasing contribution from continued primary deficits is more than offset by a favourable snowball effect[6], leading to a somewhat declining debt ratio for the euro area.

The June 2020 fiscal projections show much higher budget deficits compared to the March 2020 staff projections. Due to the macroeconomic effects of the pandemic and the fiscal measures taken, the budget balance projection for 2020 has been revised down substantially by more than 7 percentage points. In the following two years, the downward revision is smaller since it is expected that the fiscal emergency measures will expire and the economy will recover, but the deficit is still expected to be higher by 2.3 percentage points compared with the March 2020 staff projections. The debt ratio is expected to remain on a much higher path, mostly due to its upward revision for 2020 and a higher primary deficit over the full projection horizon.

Box 4

Sensitivity analysis

Projections rely heavily on technical assumptions regarding the evolution of certain key variables. Given that some of these variables can have a large impact on the projections for the euro area, examining the sensitivity of the latter to alternative paths of these underlying assumptions can help in the analysis of risks around the projections.

This sensitivity analysis aims to assess the implications of alternative oil price paths. The technical assumptions for oil price developments underlying the baseline are based on oil futures markets. Following the recent steep drop, futures markets predict an increasing profile for oil prices, with the price per barrel of Brent crude oil reaching 40.7 USD by 2022. Two alternative paths of the oil price are analysed. The first is based on the 25th percentile of the distribution provided by the option-implied densities for the oil price on 18 May 2020, which is the cut-off date for the technical assumptions. This path implies a gradual decrease of the oil price to USD 25.8 per barrel in 2022, which is 36.7% below the baseline assumption for that year. Using the average of the results from a number of staff macroeconomic models, this path would have a small upward impact on real GDP growth (around 0.2 percentage points in 2021 and 0.1 percentage point in 2022), while HICP inflation would be 0.2 percentage points lower in 2020, 0.8 percentage points lower in 2021 and 0.4 percentage points lower in 2022. The second path is based on the 75th percentile of the same distribution and implies an increase in the oil price to USD 52.1 per barrel in 2022, which is 28% above the baseline assumption for that year. This path would entail HICP inflation higher by 0.4 percentage points in 2020, 0.6 percentage points in 2021 and 0.1 percentage point in 2022, while real GDP growth would be slightly lower (by 0.1-0.2 percentage points in 2020, 2021 and 2022).

Box 5

Forecasts by other institutions

A number of forecasts for the euro area are available from both international organisations and private sector institutions. However, these forecasts are not strictly comparable with one another or with the Eurosystem staff macroeconomic projections, as they are finalised at different points in time. They are also based on different assumptions about the likely spread of COVID-19. Additionally, these projections use different and partly unspecified methods to derive assumptions for fiscal, financial and external variables, including oil and other commodity prices. Finally, there are differences in working day adjustment methods across different forecasts (see the table).

The Eurosystem staff projections for real GDP growth and HICP inflation are in most years broadly within or relatively close to the range of recent forecasts from other institutions and private sector forecasters. The current projection for real GDP growth is lower than those of other forecasters in 2020 and higher in 2022, while the projection for HICP inflation is lower than those of other forecasters in 2021 and 2022.

Comparison of recent forecasts for euro area real GDP growth and HICP inflation

(annual percentage changes)

Sources: MJEconomics for the Euro Zone Barometer, 18 May 2020, data for the year 2022 is taken from the Euro Zone Barometer forecast of April 2020; Consensus Economics Forecasts, 11 May 2020, data for the year 2022 is taken from the Consensus forecast of 6 April 2020; European Commission Economic Forecast, Spring 2020; ECB Survey of Professional Forecasters, 2020Q2, conducted between 31 March and 7 April 2020; IMF World Economic Outlook, 6 April 2020.

1) The Eurosystem staff macroeconomic projections report working day-adjusted annual growth rates, whereas the European Commission and the IMF report annual growth rates that are not adjusted for the number of working days per annum. Other forecasts do not specify whether they report working day-adjusted or non-working day-adjusted data. This table does not show ranges around the Eurosystem staff projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, in order to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Box 3.

© European Central Bank, 2020

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISSN 2529-4687, QB-CF-20-001-EN-N

HTML ISSN 2529-4687, QB-CF-20-001-EN-Q

- The cut-off date for technical assumptions, such as those on oil prices and exchange rates, was 18 May 2020 (see Box 1). The macroeconomic projections for the euro area were finalised on 25 May 2020.The current macroeconomic projection exercise covers the period 2020-22. Projections over such a long horizon are subject to very high uncertainty, and this should be borne in mind when interpreting them. See the article entitled “An assessment of Eurosystem staff macroeconomic projections” in the May 2013 issue of the ECB’s Monthly Bulletin. See http://www.ecb.europa.eu/pub/projections/html/index.en.html for an accessible version of the data underlying selected tables and charts.

- Note that the impact of the European Union fiscal support is not included in the June 2020 baseline. This support is two-fold. The first part (EIB loans, SURE, Pandemic ECCL) is already available to alleviate the financing needs in 2020 and therefore constitutes an upside growth risk for 2020. The second part, the recently proposed “Next Generation EU” instrument is expected to be available as of 2021 and implies additional upside risks to growth for the outer years.

- Note that difficulties in the collection of data are affecting the quality of national accounts and other economic statistics and different procedures for handling these difficulties hamper the cross country comparability of data. For more information see the Eurostat note “Impact of the COVID-19 outbreak on national accounts” 30 April 2020.

- The assumption for euro area ten-year nominal government bond yields is based on the weighted average of countries’ ten-year benchmark bond yields, weighted by annual GDP figures and extended by the forward path derived from the ECB’s euro area all-bonds ten-year par yield, with the initial discrepancy between the two series kept constant over the projection horizon. The spreads between country-specific government bond yields and the corresponding euro area average are assumed to be constant over the projection horizon.

- The fiscal policy stance is measured as the change in the cyclically-adjusted primary balance net of government support to the financial sector.

- The snowball effect reflects the contribution of the interest rate-growth differential to government debt multiplied by the debt ratio in the previous period.

-

4 June 2020

-

18 June 2020