The COVID-19 pandemic and access to finance for small and medium-sized enterprises: evidence from survey data

Published as part of the ECB Economic Bulletin, Issue 4/2020.

The outbreak of the coronavirus (COVID-19) pandemic has dramatically affected global economic activity. In an attempt to slow the spread of COVID-19 infections, governments around the world have introduced social-distancing measures and lockdowns and cancelled public events. Borders have been closed, even within Europe. In addition, uncertainty surrounding the future development of the pandemic and the disruption of supply chains may have contributed to amplifying the impact of the combined demand and supply shock. The business activity of many companies has been severely disrupted, leading to an unprecedented adverse impact on economic growth globally.

The latest Survey on the Access to Finance of Enterprises (SAFE) documents a deterioration in the business activity of small and medium-sized enterprises (SMEs) in the reporting period from October 2019 to March 2020.[1] As the survey was conducted between 2 March and 8 April, firms were able to account for the impact of the ongoing crisis to some extent. However, the survey results with regard to the backward-looking questions may only show some partial effects of the crisis, as the reporting period had almost come to an end before the escalation of the crisis.

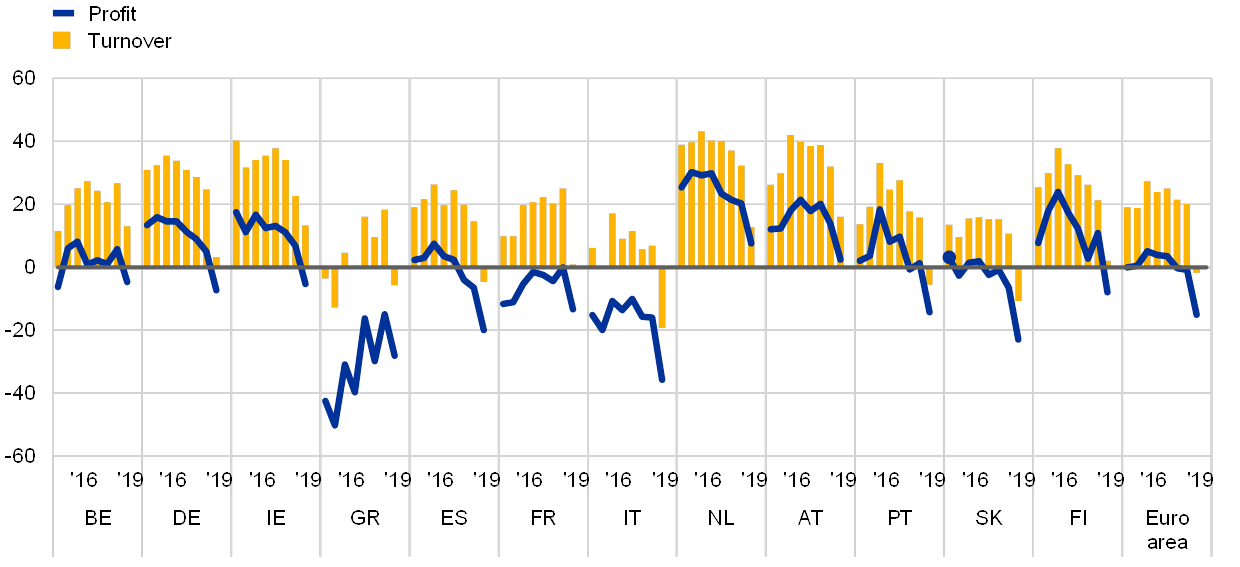

Looking backwards, euro area SMEs signalled a decline in turnover for the first time since the beginning of 2014. In net percentage terms,[2] the reported change in turnover was -2% (down from 20% in the previous round) for the euro area as a whole (see Chart A). Notwithstanding some differences across countries, the deterioration was widespread. The sharpest declines were experienced in Italy, followed by Slovakia, Greece and Spain, while in Germany and France a much smaller percentage of SMEs indicated, on balance, an increase in turnover.

Chart A

Change in turnover and profit of SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Source: ECB and European Commission, SAFE.

Notes: Base is all SMEs. Figures refer to rounds 15 (April-September 2016) to 22 (October 2019-March 2020) of the survey. The net percentage is the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease.

SMEs’ profitability also weakened across countries and economic sectors. Amid deteriorating turnover, high labour (reported by 46% of firms in net terms) and other input costs (45%) took a toll on SMEs’ profits across the euro area (-15%, from -1%), despite accommodative financing conditions. The decline in profits was particularly strong among Greek, Spanish, Italian and Slovakian SMEs. At the sectoral level, industry appears to have been the worst hit by the deterioration in profits (-20%, from -7%), notably in Italy. In the trade sector, a net 19% of euro area SMEs also reported decreasing profits, with the percentage reaching 37% in Italy and 30% in Spain.

A weakening financial position and a deteriorating macroeconomic environment raised concerns about access to finance among SMEs. The deterioration in turnover and in profits among euro area SMEs was seen as an impediment to obtaining external finance (-18%, from 5%) for the first time since September 2014, particularly among Spanish, Italian and Portuguese SMEs. In addition, SMEs also perceived developments in the general economic outlook to have negatively affected access to finance (-30%, from -13%), a percentage not seen since March 2013. The deterioration was widespread across countries – particularly in Germany, Italy and Finland – and sectors, with industry at -31%, construction at -21%, services at -31%, and trade at -30%. Moreover, compared with larger companies, SMEs, and micro firms in particular, appeared to be more concerned about the adverse impact that their own sales and profit outlook would have on their access to external finance.

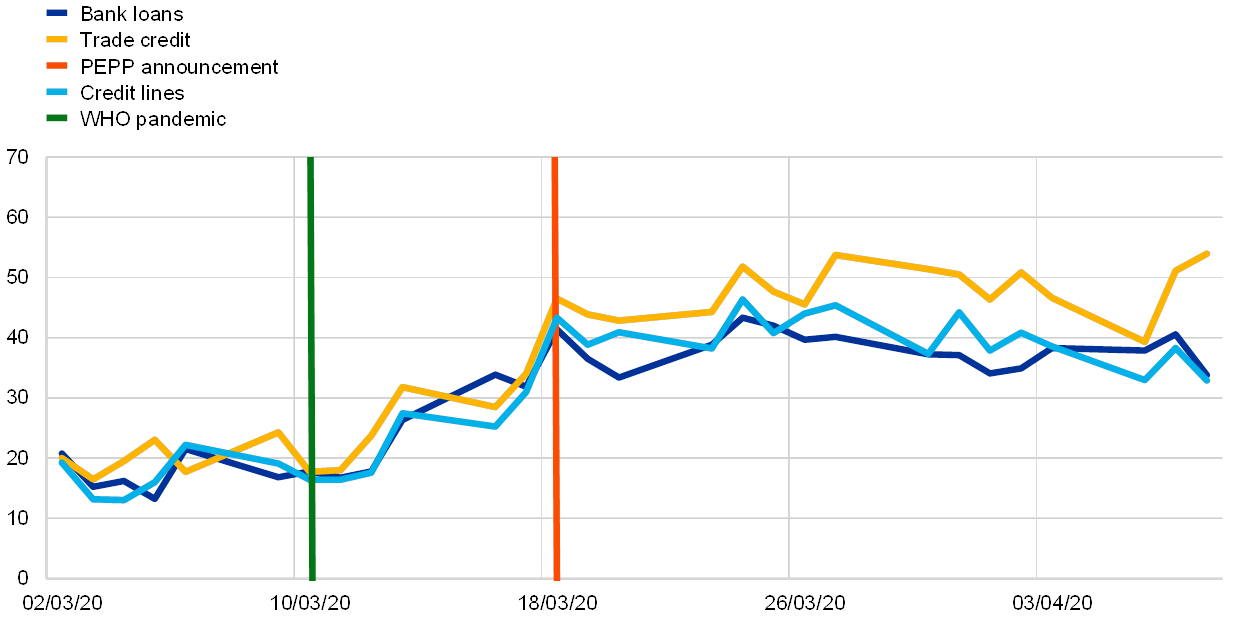

Firms’ expectations for access to finance in the near future shed more light on the severity of the COVID-19 crisis. The declaration of a pandemic by the World Health Organization (WHO) on 11 March and the subsequent intensification of confinement measures in the euro area largely coincided with the latest round of SAFE fieldwork. As a result, answers to backward-looking questions may only partially reflect the disruptions to business activity. However, the forward-looking component of the survey captured the ongoing and anticipated worsening of the economic conditions.

Focusing on the daily responses, expectations in the euro area started deteriorating rapidly shortly after the WHO declared a pandemic, which was followed by lockdowns and border controls across much of Europe. The reporting dates of firms surveyed during the fieldwork were used to analyse the change in firms’ expectations since the outbreak of the pandemic.[3] On the day of the WHO announcement, 17% of firms, on average, were expecting a deterioration in the availability of bank loans and credit lines, with 20% expecting the same for trade credit (see Chart B). By the time the ECB pandemic emergency purchase programme (PEPP) was announced on 18 March, the respective percentages were already at 41% for bank loans, 43% for credit lines and 46% for trade credit.

Chart B

Enterprises expecting a deterioration in the availability of external finance over the next six months during the fieldwork

(estimated percentages)

Source: ECB and European Commission, SAFE.

Notes: Estimated percentages refer to time fixed effects of a weighted least squares logistic regression controlling for time and country fixed effects. The last three observations (6-8 April) refer to a sub-sample of countries (Germany, Greece, Spain, France and Slovakia) as the interviews in the remaining countries were concluded by 3 April.

The deterioration in the expected access to finance appeared to level off after the PEPP announcement, at least with regard to bank loans and credit lines. Although it is not possible to infer the direct impact of the PEPP announcement on firms’ expectations, there seems to have been some mitigation of their pessimistic view of banking products starting from that date. By contrast, the deterioration of expectations regarding trade credit availability continued for somewhat longer, mostly reflecting the strains in supply relationships with expected delays in obtaining payables due to the crisis.

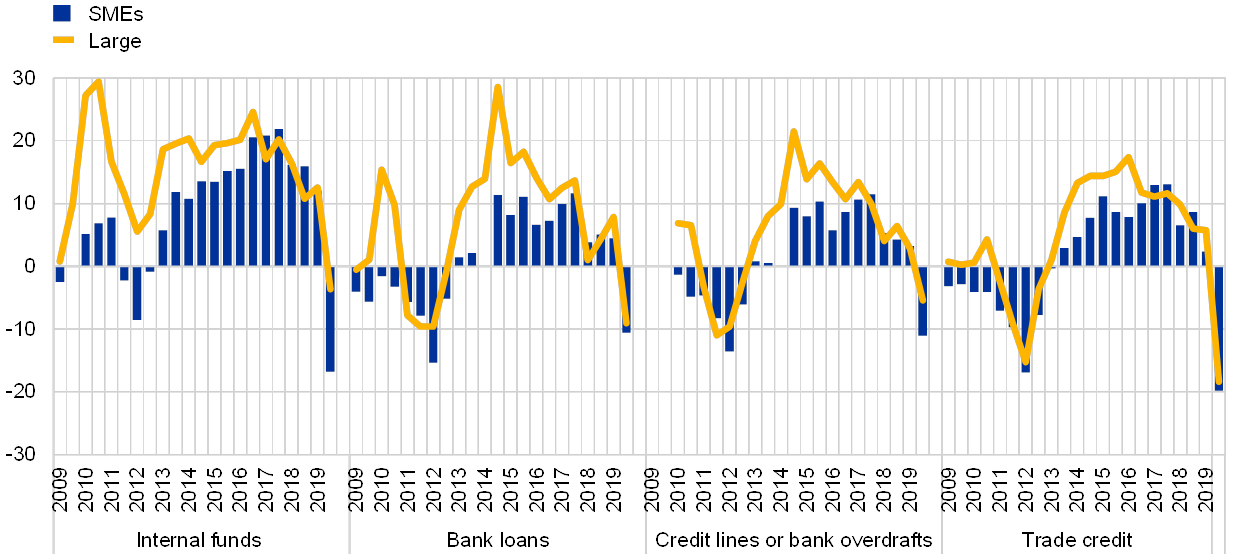

Firms’ expectations about the availability of financing over the next six months recorded a very sharp deterioration compared with the positive trend recorded since the end of the sovereign debt crisis (see Chart C). While worsening is evident for both internal and external financing sources, differences exist between the two.[4]

Chart C

Change in expected availability of financing for euro area firms

(over the next six months; net percentages of respondents)

Source: ECB and European Commission, SAFE.

Notes: Base is firms for which the respective instrument is relevant. Figures refer to rounds 1 (April-September 2009) to 22 (October 2019-March 2020) of the survey.

On internal financing sources, SMEs reported a substantial net decline in the expected availability of funds (-17%, from 12%). This is likely to reflect anticipated headwinds for economic activity, which has major implications for firms’ profitability. With the exception of the Netherlands, the deterioration is widespread across countries, with the highest percentages recorded in Portugal (-26%), France (-23%) and Italy (-21%). Overall, the deterioration in the availability of internal funds is more substantial than the lowest point indicated during the sovereign debt crisis (April to September 2012), when 9% of SMEs reported a decline.

Expected availability of external financing sources also registered a deterioration, although less than that of internal financing. Euro area SMEs reported net declines (-11%) for bank-related products, namely bank loans, credit lines and bank overdrafts. The relatively smaller deterioration compared to internal funds may reflect the positive effects of accommodative monetary policy measures and of the various government programmes that have been announced since the start of the pandemic. As for trade credit, SMEs on balance expect a significant reduction (-20%), which may point to the expected interruptions of regular business operations, in turn affecting relations between firms. The strongest declines in the expected availability of external financing were reported among SMEs from Spain, Italy, Portugal and Slovakia. The decline in future access to bank loans was still more limited than in 2012, when a net 15% of SMEs reported a deterioration in expected availability. For trade credit, however, the deterioration is already slightly more acute than in the previous crisis in 2012, when a net 17% expected a reduction.

- The 22nd SAFE round was conducted between 2 March and 8 April 2020 and covered the period from October 2019 to March 2020. The total euro area sample size was 11,236 enterprises, of which 10,287 (92%) had fewer than 250 employees. For a more comprehensive overview of the latest results, see Survey on the Access to Finance of Enterprises, ECB, May 2020. In addition, the accompanying article entitled “Access to finance for small and medium-sized enterprises since the financial crisis: evidence from survey data” in this issue of the Economic Bulletin provides additional evidence of survey results over the last ten years.

- Net terms or net percentages are defined as the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease.

- . These percentages reported in the chart are conditional on the single country effects to take into account the different degrees of emergency across countries.

- Firms from the service sector appear to be the most pessimistic of all, possibly reflecting particularly adverse effects of lockdown measures on them. Regarding the size of entities, micro firms are the most affected, according to the survey, with large firms reporting deterioration to a lesser extent.