Annual Report 2018

The year at a glance

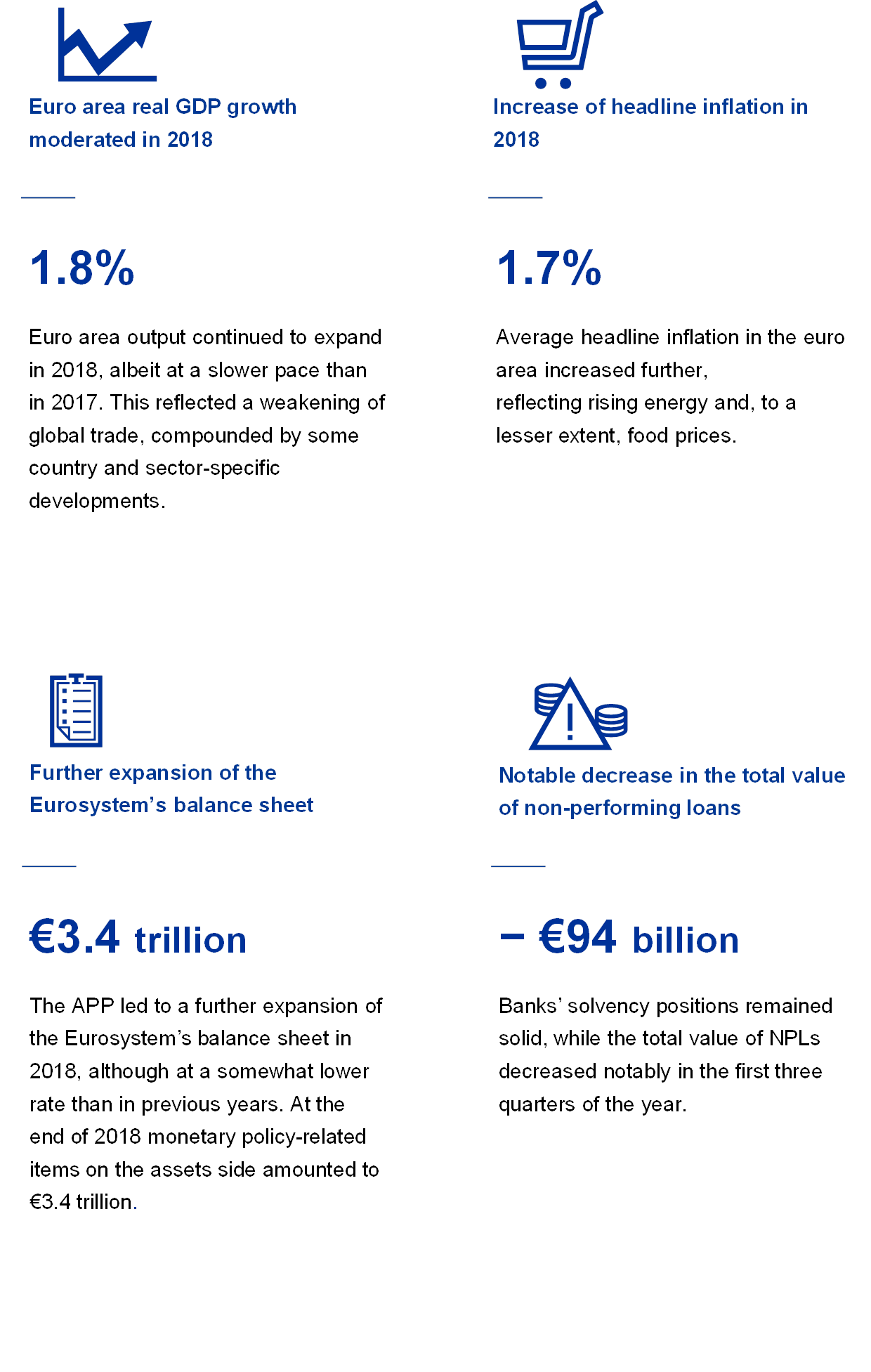

While the economic expansion in the euro area continued in 2018, the economy experienced a loss of growth momentum. Growth decelerated from 2.5% in 2017 to 1.8% in 2018 as a series of headwinds emerged over the course of the year. A significant weakening of world trade, coupled with a number of country and sector-specific factors, weighed on the external sector and manufacturing in particular.

The domestic economy nonetheless remained relatively resilient, buoyed by a continuing recovery in the labour market. Employment has increased by 10 million people since the trough in mid-2013 and the unemployment rate fell to 7.8% in December, the lowest rate since October 2008. Strong labour market dynamics translated into steady and broad-based wage growth, which reached 2.2% in the last quarter. Rising employment and wages in turn helped underpin consumer spending.

Headline inflation increased relative to the previous year, averaging 1.7% over 2018, although this mostly reflected higher energy prices. Measures of underlying inflation moved broadly sideways throughout the year. However, the outlook for domestic demand, the labour market and wage growth gave us confidence that inflation would continue to converge towards our objective over the medium term.

As a result, the Governing Council anticipated in June 2018 reducing the monthly pace of net purchases under the asset purchase programme (APP) to €15 billion from September and – subject to incoming data confirming its medium-term inflation outlook – ending net purchases in December. At the same time, the Governing Council communicated that it expected the key ECB interest rates to remain at their present levels at least through the summer of 2019[1] and in any case for as long as necessary to ensure that the evolution of inflation remained aligned with expectations of a sustained adjustment path.

In December, the Governing Council reviewed the economic outlook and concluded that the June assessment remained broadly accurate. On that basis, it ended net asset purchases under the APP and confirmed the enhanced forward guidance on the path of interest rates. In parallel, it confirmed the need for continued significant monetary policy stimulus to support the further build-up of domestic price pressures and headline inflation developments over the medium term.

That stimulus would be provided by forward guidance on key interest rates, reinforced by reinvestments of the maturing principal payments of the sizeable stock of assets acquired under the APP. The Governing Council conveyed that such reinvestments would continue for an extended period of time past the date when key interest rates rise, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The Governing Council also confirmed that, in any event, it stood ready to adjust all of its instruments, as appropriate, to ensure that inflation continued to move towards our aim in a sustained manner.

The continued domestic recovery and micro- and macroprudential actions also helped support financial sector resilience in 2018. The aggregate Common Equity Tier 1 ratio of significant institutions reached 14.2% at the end of the third quarter of 2018. Outstanding non-performing loans (NPLs) declined by €94 billion in the first three quarters of 2018, and euro area significant institutions’ aggregate NPL ratio stood at 4.2%, down from 5.2% a year earlier.

Risk-taking in parts of the financial and real estate markets contributed to mild signs of overstretched valuations in some areas, with marked cross-country differences, while risks continued to grow in the non-bank financial sector. In this environment, macroprudential measures were implemented in euro area countries to mitigate systemic risks: during 2018 the ECB assessed 103 notifications of macroprudential policy decisions by national authorities.

The ECB continued to support the benchmark reform in the euro area, developing a new money market reference rate during 2018. The ECB published the methodology for the euro short-term rate (€STR) in June 2018 after it received broad support in two public consultations. The €STR is based on average daily volumes of approximately €32 billion as traded by around 32 banks. The private sector working group on euro risk-free rates recommended the €STR as the replacement for EONIA in September 2018. The €STR will be available in October 2019, following a period of thorough internal testing by the Eurosystem.

2018 also marked a significant step forward in euro payments. In November, the Eurosystem launched the TARGET Instant Payment Settlement (TIPS) service, which offers instant payments around the clock in less than ten seconds.

As shown by the December Eurobarometer, support for the euro in 2018 rose to 75%. The ECB continued its efforts to connect with euro area citizens and to improve its accountability and transparency by engaging with the European Parliament, but also by expanding our “Youth Dialogues” and by fostering the use of our website, social media and Visitor Centre.

Turning to the coming year, substantial monetary policy stimulus remains essential to ensure the continued build-up of domestic price pressures over the medium term. In view of the persistence of uncertainties related to geopolitical factors, the threat of protectionism and vulnerabilities in emerging markets, the conduct of monetary policy in the euro area will continue to require patience, prudence and persistence.

Frankfurt am Main, April 2019

Mario Draghi

President

The year in figures

1 Economic activity continued to expand at rates above potential, while cost pressures strengthened and broadened

Following the exceptionally strong growth dynamics in 2017, the euro area economic expansion continued in 2018, albeit at a more moderate pace as external demand weakened and some country and sector-specific factors dampened growth. At the same time, the underlying drivers of domestic demand remained in place. Further improvements in the labour markets supported private consumption, while business investment continued to benefit from favourable financing conditions and improving balance sheets. The ongoing expansion and tightening of labour markets also translated into a continued strengthening and broadening of domestic cost pressures. At the same time, measures of underlying inflation remained generally muted. However, looking ahead, underlying inflation is expected to increase over the medium term, supported by the ECB’s monetary policy measures, the ongoing economic expansion and rising wage growth.

1.1 A less balanced global expansion

Global growth continued at rates close to its long-run average

The global economic expansion continued at a steady pace of 3.6% in the first three quarters of 2018, a rate similar to that in the preceding year and close to its long-run average (see Chart 1). However, compared with previous years, the upturn in economic activity became more uneven and less synchronised across countries. While growth remained robust in the United States, it faltered in a number of other economies, including Japan and some emerging markets, in particular Turkey and Argentina. Activity also decelerated in China in the second half of the year. Looking at the different components, growth in industrial production and world trade weakened, while private consumption growth remained solid.

Chart 1

Global GDP growth

(annual percentage changes; quarterly data)

Sources: Haver Analytics, national sources and ECB calculations.

Notes: Regional aggregates are computed using GDP adjusted with purchasing power parity weights. The dashed lines indicate the long-term average (between March 1999 and September 2018).

Unemployment rates stood in many countries at post-crisis lows

As the ninth consecutive year of the current global expansion began, unemployment rates across both advanced economies and emerging market economies continued to decline and, in many countries, stood at post-crisis lows. In some cases, they even stood at historical lows, such as in the United Kingdom and in Japan. Labour shortages became evident in several advanced economies, especially among specialised and highly skilled workers.

There are increasing signs that the ongoing decline in slack in both productive capacity and labour markets at the global level has been gradually, albeit only slowly, translating into higher wage growth and higher underlying inflation. In the OECD area, underlying inflation (excluding energy and food) increased to 2.1% in 2018. Headline inflation increased much more strongly, reaching 2.6% in annual terms, although it subsided in the second half of the year mostly on account of lower oil prices (see Chart 2).

Chart 2

OECD inflation rates

(annual percentage changes; monthly data)

Sources: Haver Analytics, OECD and ECB calculations.

Supply-side developments were a key factor driving oil prices in 2018, in an environment of continued solid global demand and tight inventories. In the first half of the year oil prices rose gradually from around USD 67 per barrel to USD 79 per barrel, following a greater than expected compliance by the 22 OPEC and non-OPEC producers with their agreed production cuts. Oil prices fluctuated between USD 70 and USD 86 per barrel until early autumn, but declined thereafter to around USD 52 per barrel by year-end. The rise to a high of USD 86 per barrel by early October was related to fears of a steep decline in Iranian oil exports, following the reintroduction of sanctions by the United States. However, oil prices significantly moderated by the end of December owing to a combination of weakened demand prospects and concerns over excess supply as the United States, some OPEC members and the Russian Federation increased their production. In addition, there were some exemptions from the sanctions imposed on the Islamic Republic of Iran. Meanwhile, non-oil commodity prices decreased overall in 2018 (in US dollar terms).[2] Food and metal prices remained broadly stable in the first half of 2018. Food prices declined during the second half of the year amid both ample global food supply and concerns about US tariffs and the risk of retaliation by affected countries. Metal prices also retreated since the summer due to lower demand from China, as well as concerns about an escalation of trade tensions.

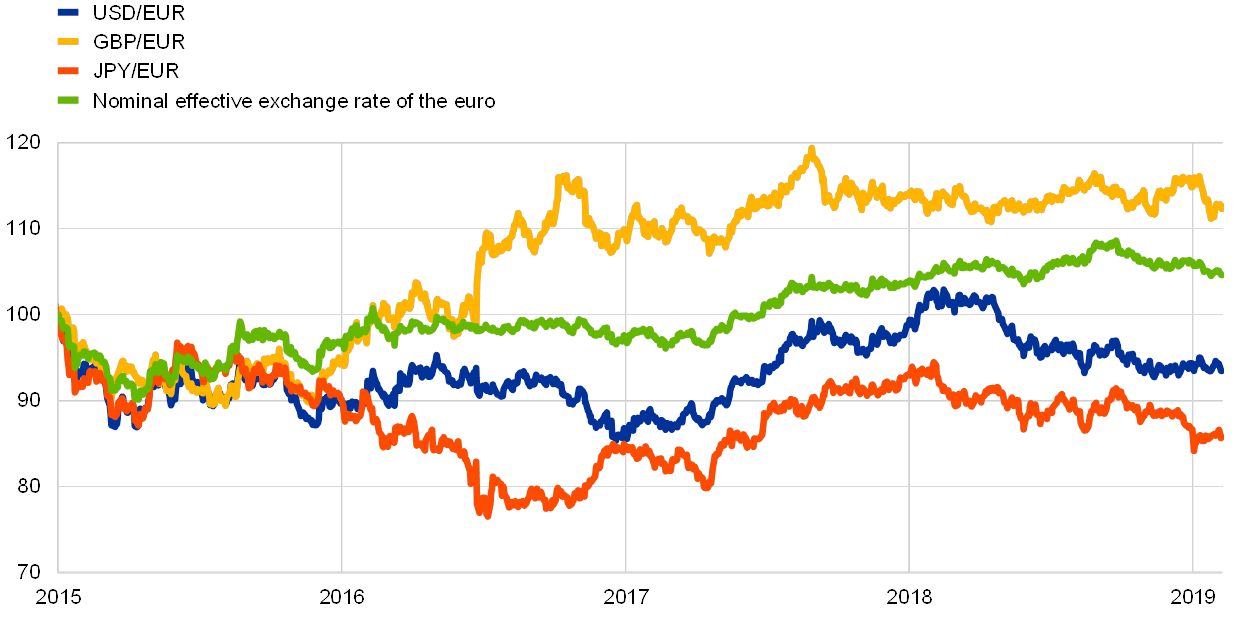

The effective exchange rate of the euro appreciated

The exchange rate of the euro appreciated in nominal effective terms (see Chart 3) since the beginning of 2018. In bilateral terms, the euro depreciated vis-à-vis other major currencies. The depreciation of the euro was particularly pronounced against the US dollar, the Japanese yen and – albeit to a lesser extent – the Swiss franc. At the same time, the euro appreciated significantly against most emerging market currencies, in particular the Chinese renminbi and, as a result of domestic headwinds, the Turkish lira and the Argentinian peso.

Chart 3

The euro exchange rate

(daily data; 1 January 2015 = 100)

Sources: Bloomberg, HWWI, ECB and ECB calculations.

Note: Nominal effective exchange rate against 38 major trading partners.

Trade uncertainty clouded the global outlook

While global growth continued at a solid pace, risks and uncertainties increasingly clouded the outlook. In particular, trade uncertainty rose following actions by the US administration and responses by its trading partners. This culminated with two announcements by the US administration of tariffs targeting USD 250 billion of Chinese exports in the summer, and China announced retaliation on USD 110 billion of exports from the United States. In addition, doubts over Brexit also weighed on the trade outlook. While the direct impact of these tariffs should remain contained at the global level, such protectionist threats have the potential to erode confidence, disrupt global value chains and adversely affect investment, and in turn constitute a downside risk to the global economic outlook. By the end of the year there were already signs that trade uncertainty had started to affect the conduct of business. If trade disputes escalate further, global growth could be severely impaired.

1.2 Economic growth moderated, but remained consistent with an ongoing expansion

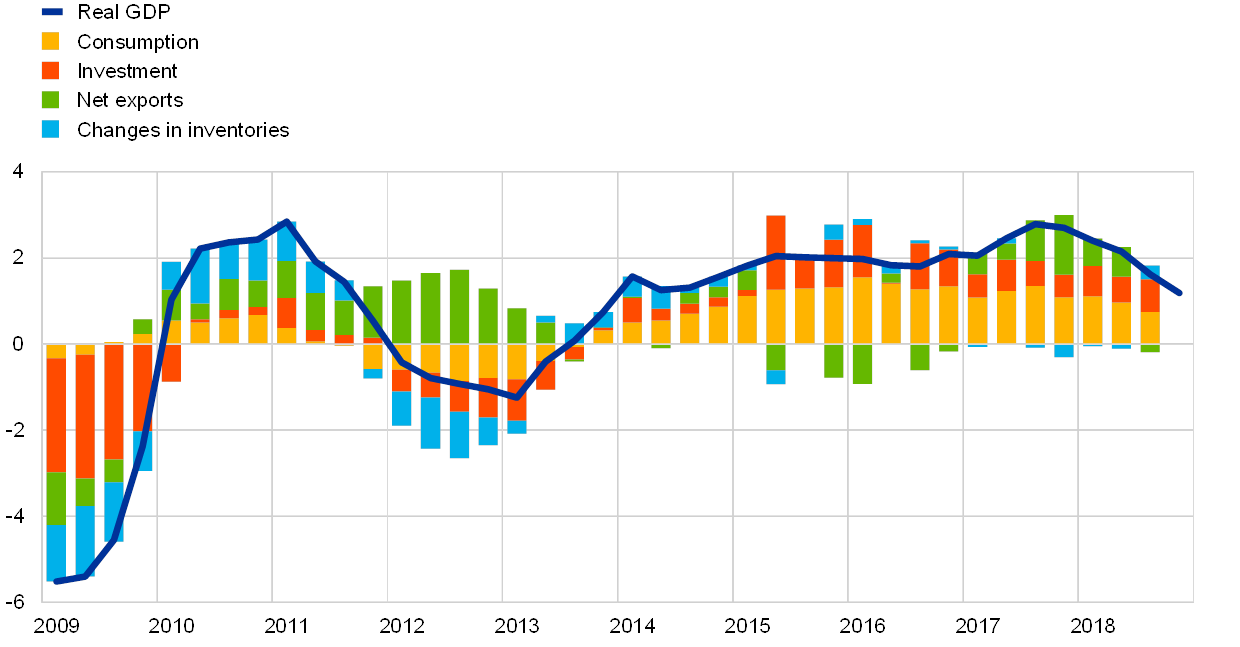

Following the exceptionally strong growth dynamics in 2017, euro area real GDP growth moderated to 1.8% in 2018 (see Chart 4). Although this slowdown was mainly attributable to a weakening in global trade, other factors of a more transitory nature also played a role. In the first half of 2018 weather-related disruptions and industrial action, especially in the transportation sector, affected output in a number of countries. In the second half of the year, and in particular in the third quarter, there was a significant disruption of automobile production following the introduction of the Worldwide Harmonised Light Vehicle Test Procedure on 1 September. Furthermore, the decline in growth may have been compounded by an increase in political uncertainty, particularly in relation to the prospect of increasing protectionism.

Chart 4

Euro area real GDP

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: Annual GDP growth for the fourth quarter of 2018 refers to the preliminary flash estimate, while the latest observations for the components are for the third quarter of 2018.

At the same time, the underlying growth momentum remained solid

At the same time, the underlying growth momentum remained solid, supported by a robust labour market and steady income and profit growth. Spillovers from the weakness of and heightened uncertainty about external demand to domestic demand have so far remained contained.

Euro area private consumption increased in 2018 at an average annual growth rate of around 1.3%, supported by stronger labour income and favourable financing conditions. At the same time, the gradual increase in oil prices since mid-2017 did not significantly dent the growth of real disposable income. As the economic expansion progressed, the contribution of taxes and transfers became somewhat more negative in 2018. In good times, automatic fiscal stabilisers tend to have a dampening effect on the growth of real disposable income.

Domestic demand growth, favourable financing conditions and corporate profitability continued to support euro area business investment in 2018. Investment increased also in sectors facing capacity constraints such as the transportation sector. However, the less dynamic external environment and the heightened global uncertainty, in particular in relation to trade policies, weighed on the investment activities of firms, particularly those more exposed to the external environment. Going forward, business investment growth is likely to moderate in view of the less supportive external environment and more moderate final demand, and the expected gradual tightening of financing conditions.

Construction investment, both residential and non-residential, also continued improving, albeit from low levels, alongside the recovery in euro area housing markets. This, in turn, reflected growing domestic demand, which was supported by real income growth, a low interest rate environment and favourable lending conditions. Nevertheless, bottlenecks in the labour market appear to have limited growth in the construction sector in the course of 2018.

In 2018 the contribution of the external sector to the overall euro area performance was particularly modest, at any rate significantly weaker than in 2017. Waning foreign demand, especially from Asia and in particular for capital goods, due to increased uncertainty and heightened trade tensions undermined euro area exports to the region and acted as a drag on the total net trade contribution to GDP. Exports to the United Kingdom and China suffered the most from the changing international environment, while exports to the United States benefited, probably from anticipation effects in relation to the risk of the US administration also enforcing tariffs on imports from the EU. Supported by positive economic developments in the area, the trade momentum within the euro area initially proved resilient. However, it weakened significantly in the second half of 2018 as trade uncertainty and new car emission standards took a toll on trade in capital goods and cars. Some headwinds may also have arisen from past euro exchange rate appreciations.

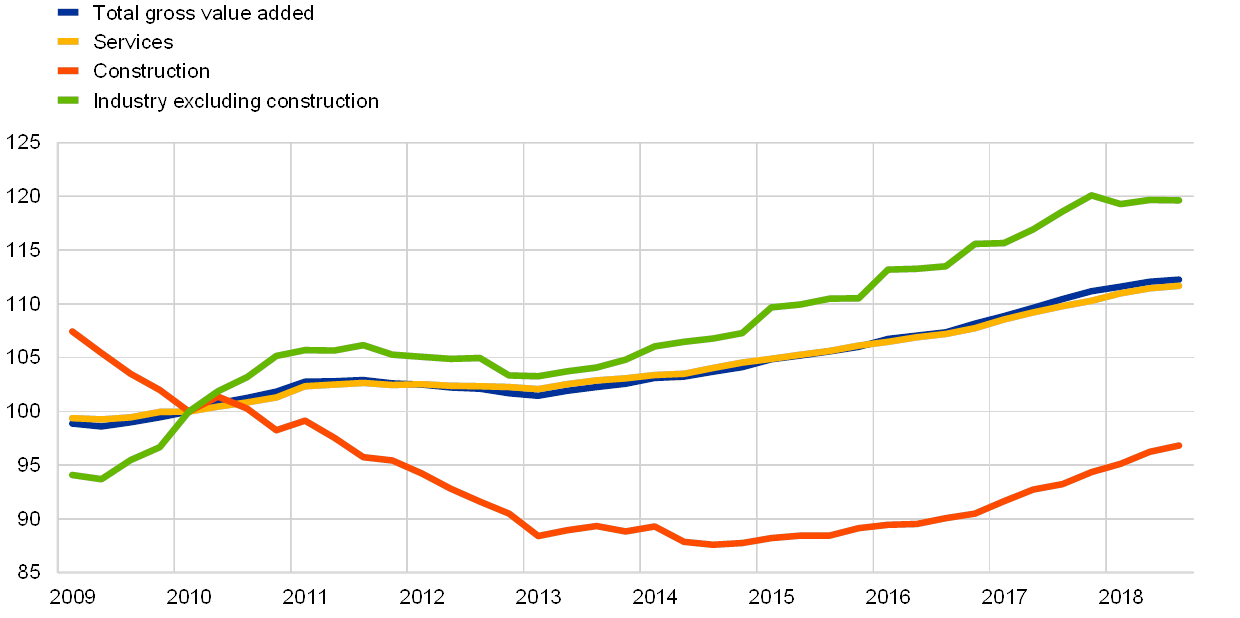

Output growth in 2018 continued to be broad-based across economic sectors (see Chart 5). Total gross value added rose further, by around 2%, which was somewhat lower than in the previous year, but close to the growth rates recorded in 2015 and 2016. Value added in industry (excluding construction) and value added in the services sector both increased by around 2% in 2018. At the same time, value added in construction, albeit still below its pre-crisis level, continued its expansion, rising by around 4%. This again confirmed that the construction sector is increasingly recovering from the protracted period of contraction or slow growth that followed the onset of the financial crisis in 2008.

Chart 5

Euro area real gross value added by economic activity

(index: Q1 2010 = 100)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for the third quarter of 2018.

Euro area labour markets continued to improve, while the age composition of employment changed

Euro area labour markets recovered further in 2018; since the trough in 2013, employment has increased by around 10 million persons

Euro area labour markets recovered further in 2018 (see Chart 6). The unemployment rate continued to decline in 2018 and stood at 7.8% in December, the lowest rate since October 2008. The decline in unemployment, which started in the second half of 2013, has been broad-based across gender and age groups, while levels of the unemployment rate continue to differ significantly across euro area countries. By the fourth quarter of the year the number of persons employed in the euro area stood 1.3% above the level at the same time in 2017, or 6.7% above the last trough in the second quarter of 2013. Over the whole recovery period, employment has increased by around 10 million persons. This has taken the level of employment above its pre-crisis peak reached in the first quarter of 2008. Employment growth over the recovery has been broad-based across countries and sectors, and has occurred against the background of further increases in labour supply.

Chart 6

Labour market indicators

(percentage of the labour force; quarter-on-quarter growth rate; seasonally adjusted)

Source: Eurostat.

Notes: The latest observations are for the fourth quarter of 2018. Quarterly employment growth for the fourth quarter of 2018 refers to the preliminary flash estimate.

A closer look at the composition of employment growth over the recovery reveals that the growth has been concentrated among older persons.[3] Indeed, about three-quarters of the cumulative employment growth has come from those aged between 55 and 74. The increasing employment of the older population during the recovery is primarily due to the rising participation rate of this group. This can be assumed to largely reflect the impact of past pension reforms, as well as increasing education levels in this group. The significant increase in the share of older workers in employment may give rise to far-reaching changes in the economy, through impacts on patterns in consumption, savings and investment, as well as on wage and productivity developments.[4] Over the recovery, about one-third of employment growth has come from part-time employment, which is closely linked to the longer-term upward trends of increasing labour supply by female and older workers, as well as of continuing concentration of employment growth in the services sector.[5] Looking ahead, labour shortages in some countries and sectors can be expected to contribute to a moderation in these continuing trends.

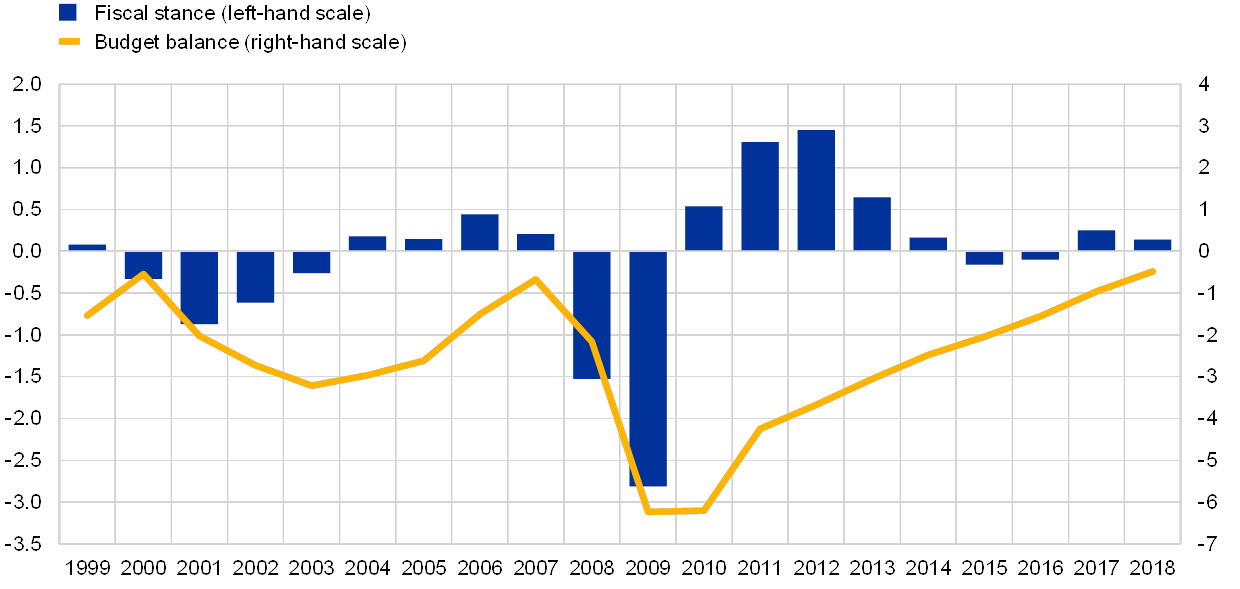

Government deficit continues to fall, but uneven risks remain

The euro area general government deficit ratio declined mainly on account of favourable cyclical developments

The euro area general government deficit ratio continued to decline in 2018 and reached 0.6% of GDP, a level rarely seen since the start of Economic and Monetary Union (EMU) in 1999 (see Chart 7). As has been the case over the last few years, the fall in the overall deficit was to a large extent the result of favourable cyclical developments, in combination with falling interest expenditures as maturing high-cost debt continued to be replaced with new debt issued at lower interest rates. The euro area fiscal stance[6] was broadly neutral in 2018, although the euro area aggregate masked significant differences across countries, with large windfalls in a few countries compensating in the aggregate for procyclical fiscal loosening in vulnerable countries.

Chart 7

General government balance and fiscal stance

(percentage of GDP)

Sources: Eurostat and ECB calculations.

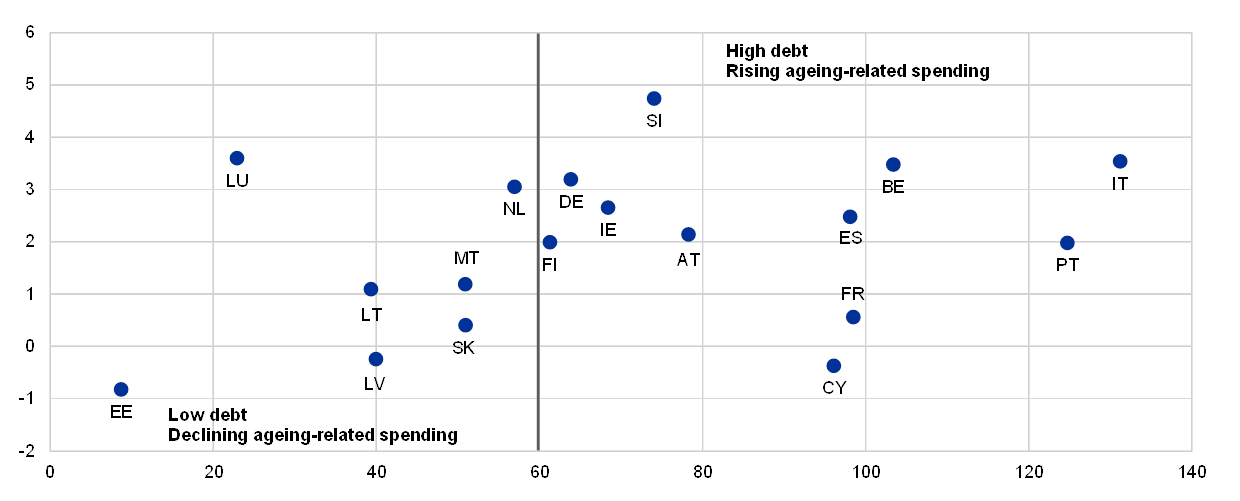

In a context of expanding economic activity, the falling government deficit contributed to sustaining a decline in the ratio of gross debt to GDP, from 86.6% in 2017 to 84.8% in 2018. While the debt ratio is projected to decline also over the coming years, it should be kept in mind that it remains significantly higher than at the start of EMU. High debt levels constitute a vulnerability, and particularly so in countries that suffer from low potential output growth and face growing demographic challenges (see Box 1). Such countries would have limited margins to adjust fiscal policies in the event of a deterioration in economic activity or increasing interest expenditures. Vulnerable countries would therefore be well-advised to build up buffers now that economic conditions allow it.

Box 1

Population ageing and its fiscal impact

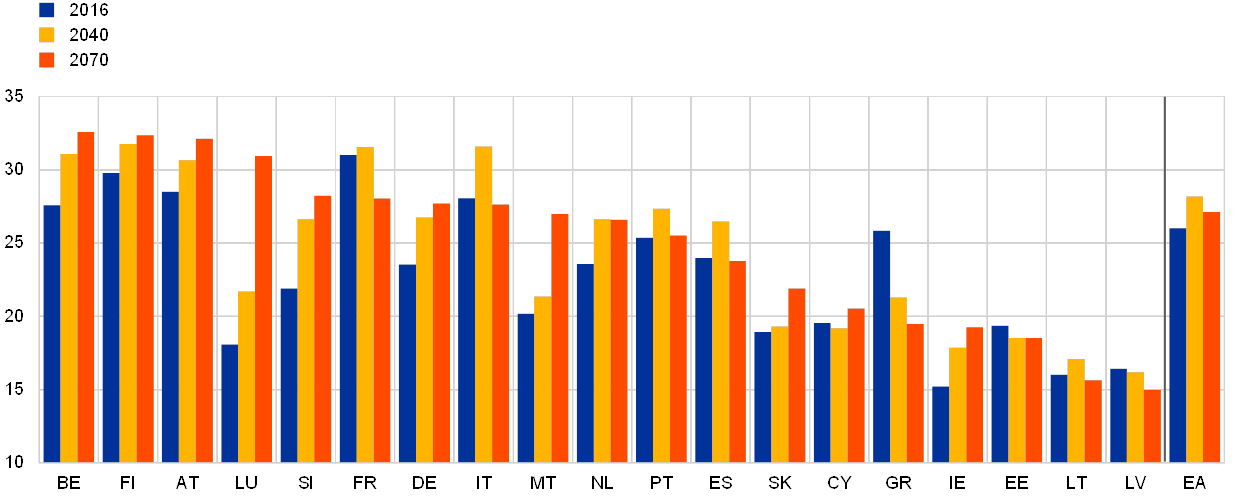

Population ageing is a challenge for the sustainability of public finances in the euro area. Societies are ageing, as people live longer and have fewer children. The demographic change is well captured by the rising old-age dependency ratio, which gives the number of people aged 65 or older relative to the working age population. Eurostat projects the ratio to increase from 31% in 2016 to 52% in 2070 in the euro area as a whole. The bulk of the increase will take place in the next two decades, as the baby boom generation is approaching retirement age. While population ageing also potentially has major adverse macroeconomic implications, for example for productivity, the labour force and the equilibrium real interest rate, this box solely focuses on its fiscal impact.

Population ageing will substantially impact public finances over the decades to come. Ageing-related public expenditures in the euro area, which amounted to one-quarter of GDP in 2016, are already elevated by international standards. According to the 2018 Ageing Report, they are projected to increase further to 28% of GDP in 2040 and to decline slightly to 27% of GDP by 2070 (see Chart A).[7] The aggregate picture masks considerable heterogeneity across countries. The projected changes in total ageing-related expenditure range from an increase of 12.9 percentage points of GDP in Luxembourg to a decline of 6.4 percentage points of GDP in Greece over the period 2016-70.[8] If the increases in ageing-related expenditures are left unaddressed, they will swell to very large amounts over the medium-to-long term. This would pose a challenge to fiscal sustainability already in the medium term, in particular in countries with already high public debt levels today (see Chart B). However, in several countries, in particular in France, Italy and Spain, the ageing-related cost pressures are projected to diminish from their peak in the medium term by 2070 (see Chart A).

Chart A

Total ageing-related expenditure in the euro area

(percentage of GDP)

Source: 2018 Ageing Report.

Chart B

Ageing-related spending pressures and current debt levels across countries

(x-axis: government debt-to-GDP ratio in 2017; y-axis: change in total ageing-related expenditures as a percentage of GDP, 2016−40)

Sources: 2018 Ageing Report and Eurostat.

Note: Greece is excluded as it is an outlier with a public debt ratio of 176.1% of GDP in 2017 and a decline in total ageing-related spending by 4.6% of GDP.

Public spending affected by ageing includes in particular expenditures on pensions, as well as on health care and long-term care. With an increasing number of beneficiaries of public pension schemes facing a declining number of contributors, deficits in pension systems, and ultimately in overall fiscal balances, will rise unless parameters are adjusted. Moreover, health and long-term care systems are expected to burden public finances in the coming decades, as these services are mostly financed by public systems. The impact of ageing on public revenues is less straightforward, as its effects on the various tax bases (for example on consumption, labour income and capital) are partially offsetting and expected to vary over time.

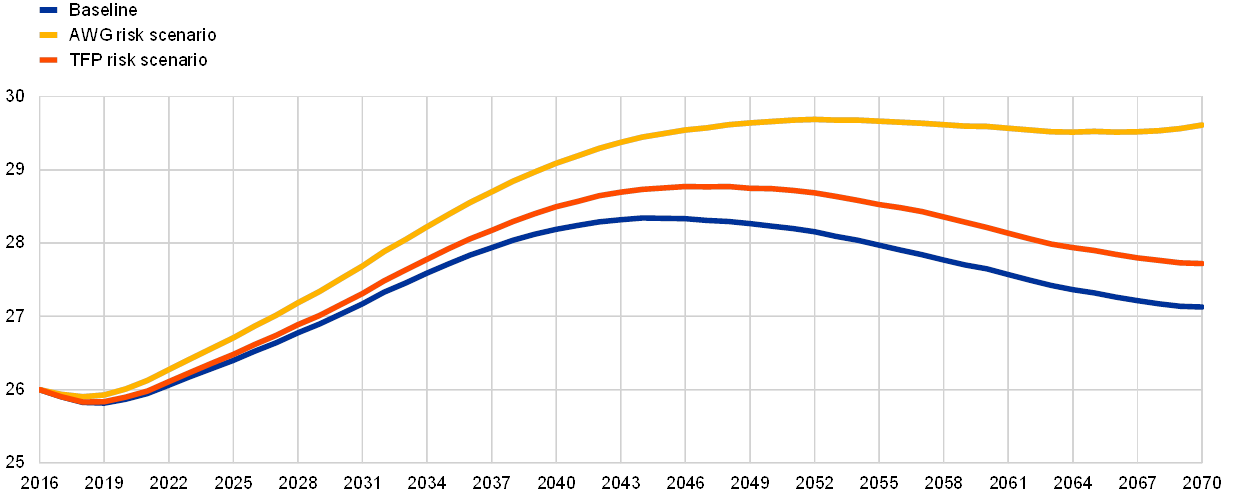

To capture some of the uncertainty surrounding the ageing-related spending projections, the Ageing Report includes several adverse sensitivity analyses and risk scenarios, which indeed suggest higher cost pressures (see Chart C). One risk scenario implies higher costs for health and long-term care, on the grounds of an increased use of expensive medical equipment and a stronger upward convergence in living standards. In this scenario, the increase in total ageing-related expenditures would be more than twice as large as in the baseline scenario at the end of the projection horizon in 2070. A lower total factor productivity (TFP) growth rate than assumed in the baseline projections would also imply considerably higher costs in the long term.

Chart C

Ageing-related spending scenarios in the euro area

(percentage of GDP)

Source: 2018 Ageing Report.

Notes: The TFP risk scenario assumes convergence to a lower TFP growth rate by 2070 (i.e. to 0.8% instead of 1%). The AWG risk scenario assumes a higher income elasticity of healthcare spending (due to increased use of expensive medical technology) and higher long-term care costs (due to increasing coverage of recipients of long-term care and upward convergence in real living standards).

To address future ageing-related spending pressures, most euro area countries have implemented pension reforms in recent years, in some cases complemented by more limited reforms to health and long-term care systems. Such reforms reflected in particular fiscal sustainability concerns stemming from the sovereign debt crisis. Pension reforms were particularly substantial in countries subject to macroeconomic adjustment programmes. While these reforms have helped countries to partly contain their risks to pension sustainability, more recently the pace of reforms has stalled and, in a few instances, reform efforts have even been reversed or face a significant risk of being reversed.

Looking ahead, countries with already high public debt levels in particular need to safeguard against the upcoming demographic challenges. To contain the potential spending pressures coming from social security systems, countries should adopt further reforms if they do not build up fiscal buffers, while reform reversals should be avoided. In terms of concrete policy action, the reforms required may vary across countries, also reflecting differences in the starting position and societal preferences. In fact, some countries may favour reforms to entitlements and boosting private sector provision of pensions beyond what has already been achieved. Other countries may favour linking retirement ages to life expectancy, while maintaining the pension benefit ratio of the system. Yet other countries may opt for higher contribution rates, although this may put a heavy burden on younger generations. These options are not mutually exclusive and can be implemented in combination. When designing pension reforms, it is also important to be mindful of their possible implications for labour supply and the supply side of the economy, as higher levels of potential growth are essential to improve social welfare. Ideally pension reforms should be complemented by labour market reforms fostering in particular the participation of elderly workers. Finally, an important challenge for fiscal policymakers is to avoid raising uncertainty regarding the risk of reform reversals that could undermine fiscal sustainability.

Compliance with the SGP is weakest in the most vulnerable countries

In this light, it is of concern that compliance with the Stability and Growth Pact (SGP) is weakest for those countries that are most vulnerable to shocks. In fact, according to the European Commission projections, most of the countries that have not yet reached sound budgetary positions missed their commitments under the SGP in 2018. Among the seven euro area countries that are assessed by the Commission to be at risk of a deviation from the SGP’s preventive arm in 2018, four countries – Belgium, France, Italy and Portugal – have debt ratios above 90% of GDP. In addition, while Spain – the only country subject to an excessive deficit procedure (EDP) in 2018 – is projected to meet its 2018 EDP correction deadline, this achievement masks a high and increasing structural deficit, as opposed to the recommended improvement. Furthermore, the European Commission’s assessment indicates that only ten countries intend to be compliant with the SGP according to draft budgetary plans for 2019. It is particularly worrying that most of the countries with high debt ratios are not included in this group.

Reform momentum in the euro area remains lacklustre

Reform progress has stalled; none of the 2017 CSRs has been fully implemented

The country-specific recommendations (CSRs) provide policy recommendations tailored to an individual country on how to enhance economic growth and resilience, while maintaining sound public finances. The CSRs are jointly endorsed by Member States in the European Council. Similarly to last year, the Commission concluded that the overwhelming majority – more than 90% – of reform recommendations given to euro area countries in 2017 have been followed by only “some” or “limited” progress in implementation, while none has been fully implemented (see Chart 8).[9]

Chart 8

Implementation of the country-specific recommendations by euro area countries

Sources: ECB calculations based on the European Commission’s Country Reports.

Notes: The chart shows the implementation of CSRs at the level of sub-headings for the year as assessed by the European Commission in the respective Country Report published the following year. “Full implementation” signifies that the Member State has implemented all measures needed to address the CSR appropriately; “substantial progress” signifies that the Member State has adopted measures that go a long way towards addressing the CSR, most of which have been implemented; “some progress” signifies that the Member State has adopted measures that partly address the CSR, and/or it has adopted measures that address the CSR but a fair amount of work is still needed to fully address it as only a few of the adopted measures have been implemented; “limited progress” signifies that the Member State has announced certain measures but these only address the CSR to a limited extent, and/or it has presented non-legislative acts, yet with no further follow-up in terms of implementation; and “no progress” signifies that the Member State has not credibly announced or adopted any measures to address the CSR. CSRs for implementation of the SGP are not included.

Well-designed structural reforms could yield substantial benefits for euro area citizens via stronger and more inclusive growth in employment and incomes. A recent Eurosystem analysis shows that there are ample opportunities for reforms that simultaneously enhance resilience, long-term growth and social fairness.[10] A case in point are reforms that address rent-seeking, in particular those strengthening product market competition and the quality of public institutions. Similarly, policies supporting education and life-long learning improve not only an economy’s long-term growth prospects, but also the employment opportunities of vulnerable groups of society.

1.3 Inflation on a higher path

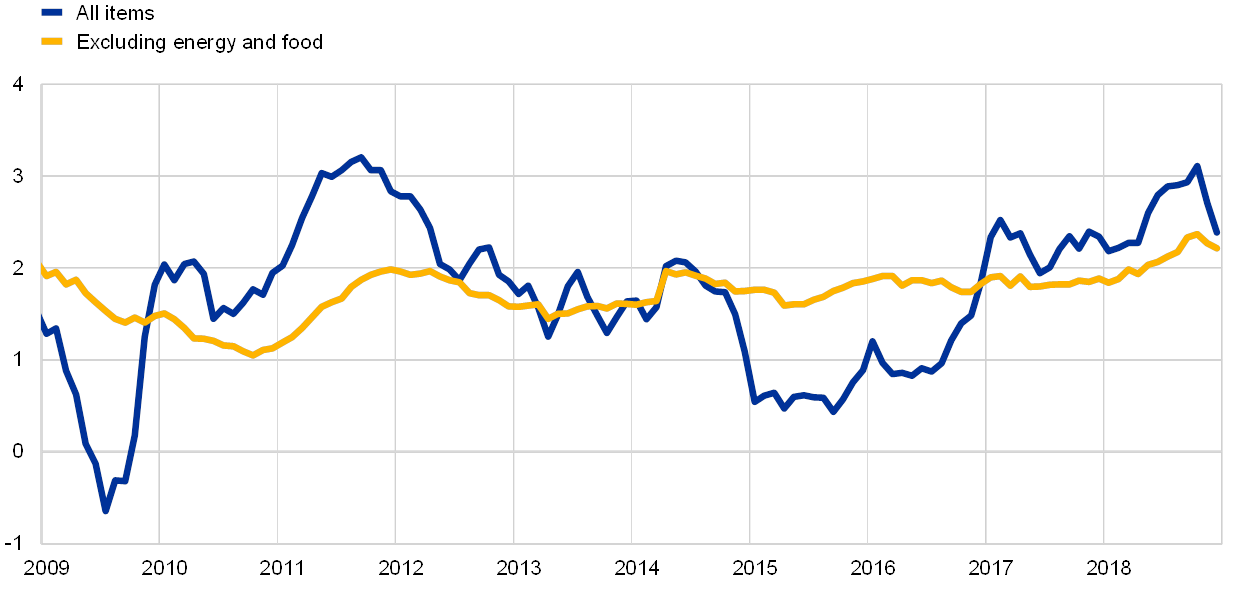

Headline inflation in the euro area, as measured by the Harmonised Index of Consumer Prices (HICP), rose to 1.7% on average in 2018, from 1.5% the year before. This increase largely reflected higher contributions from energy prices and, to a lesser extent, food prices. By contrast, the contribution of underlying inflation, as measured by HICP inflation excluding energy and food, remained broadly unchanged. This inflation measure remained subdued, moving essentially sideways around 1% throughout the year (see Chart 9).

Chart 9

HICP inflation and contributions by components

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Developments in energy prices strongly influenced the intra-year profile of headline HICP inflation. Driven by the rise in crude oil prices, energy inflation increased strongly between April and July and thereafter remained at high year-on-year rates of change (with a peak of nearly 11% in October 2018). Thus, the contribution of energy inflation to headline inflation rose from 0.2 percentage point in the first quarter of 2018 to 0.9 and 0.8 percentage point in the last two quarters of 2018. Developments in unprocessed food prices added to this intra-year profile due to the weather-related sharp increases in the annual rates of change of fruit and vegetable prices in the summer months, which however unwound in the last months of the year. This caused the contribution of unprocessed food to headline inflation to rise from zero in the first quarter of 2018 to more than 0.2 percentage point in September 2018, before declining somewhat in the last quarter of 2018.

Inflation excluding energy and food remained subdued

HICP inflation excluding energy and food remained unchanged compared with 2017, moving like other measures of underlying inflation broadly sideways throughout the year.[11] However, when also excluding the more volatile components related to clothing and travel, this underlying measure of inflation increased.

The rather subdued developments in HICP inflation excluding energy and food were observed in both main components, namely non-energy industrial goods and services. Non-energy industrial goods inflation showed some volatility, declining up to September 2018 before increasing somewhat thereafter, and stood at 0.4% in 2018, as in 2017. Looking at indicators for price pressures at different stages of the pricing chain, both the annual rate of change of producer prices for domestic sales of non-food consumer goods and that of import prices for non-food consumer goods increased in the course of 2018. In the case of import prices this essentially reflected the waning impact of the euro appreciation in 2017, while in the case of producer prices it likely reflected the growth in input costs and retail sales volumes. Services price inflation was broadly unchanged in 2018 at 1.3% and remained well below its long-term average. A modest pick-up occurred in the annual rate of change of services prices in the last quarter of 2018, but it largely reflected the base effect of rather weak developments in services inflation during the same months of 2017. Overall, inflation in services prices, which have a large labour cost content, has not yet mirrored the pick-up in wage growth.

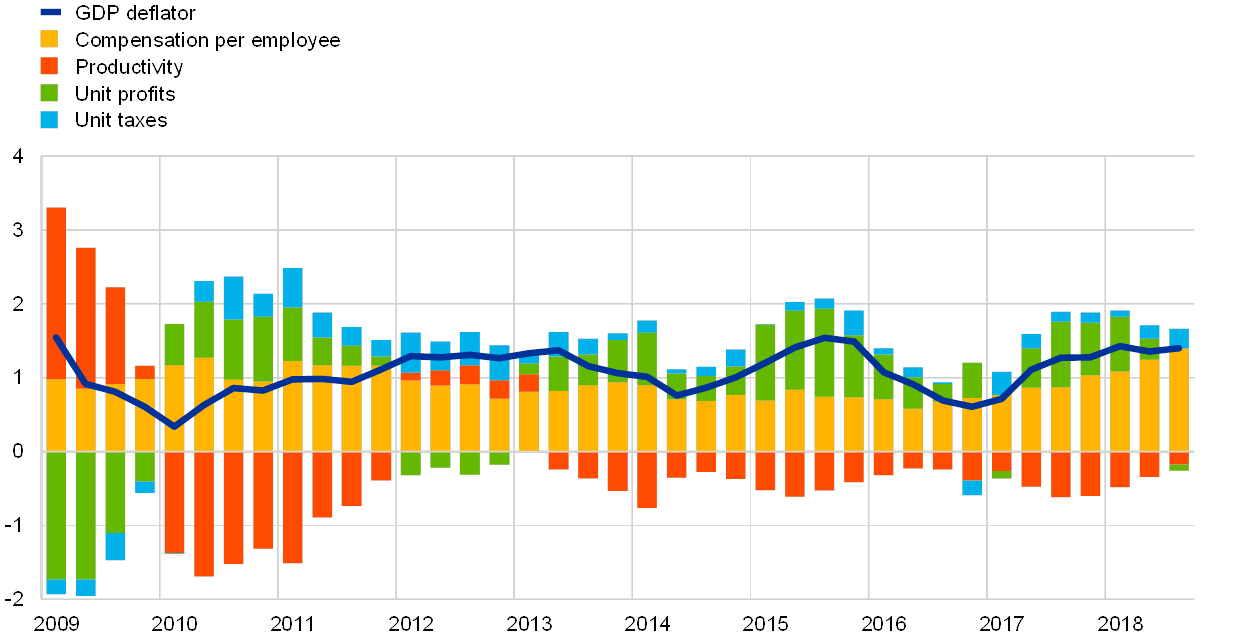

The annual growth of compensation per employee continued to increase

Domestic cost pressures as measured by the growth in the GDP deflator remained constant in the first three quarters of 2018, slightly above the rate reached in the second half of 2017 (see Chart 10). The annual growth in compensation per employee, which had reached a trough in mid-2016, continued to increase in 2018, standing at 2.5% in the third quarter of the year, which was above its historical average of 2.1% (since 1999). Overall, the pick-up in wage growth reflected improved labour market conditions (see Section 1.2 above) and the fading-away of the factors that had contributed to containing wage growth in the past, such as the impact of low past inflation as a result of formal and informal indexation schemes and the effects of labour market reforms implemented in some countries during the financial crisis. In a moderately favourable demand environment, the higher wage growth translated into higher unit labour cost growth, but the impact of this on domestic cost pressures was mitigated by profit developments (measured in terms of the gross operating surplus), which have weakened in recent quarters, partly reflecting the negative impact of the terms-of-trade deterioration related to higher oil prices.[12]

Chart 10

Breakdown of the GDP deflator

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Longer-term inflation expectations were somewhat higher in 2018 than in 2017. Expectations for inflation five years ahead from the ECB Survey of Professional Forecasters have remained unchanged at 1.9% for a succession of quarters, staying slightly higher than in 2017. Market-based measures of longer-term inflation expectations, such as the five-year inflation-linked swap rate five years ahead, showed some volatility, declining towards the end of the year, but remaining broadly unchanged on average compared with 2017.

1.4 Favourable financing conditions supported credit and money growth

In 2018 euro area financial markets were influenced by uncertainties regarding the global and domestic euro area economic outlook in combination with politically induced risk-off sentiment – in particular relating to Brexit, trade protectionism and uncertainty about the policy stance of the Italian government on public finances. Money market rates and longer-term bond yields remained at very low levels, in part thanks to the continued monetary policy accommodation provided by the ECB. Financing conditions supported business investment, while household wealth underpinned private consumption. Money growth declined, while growth in credit to the private sector increased further.

Euro area government bond yields remained broadly unchanged

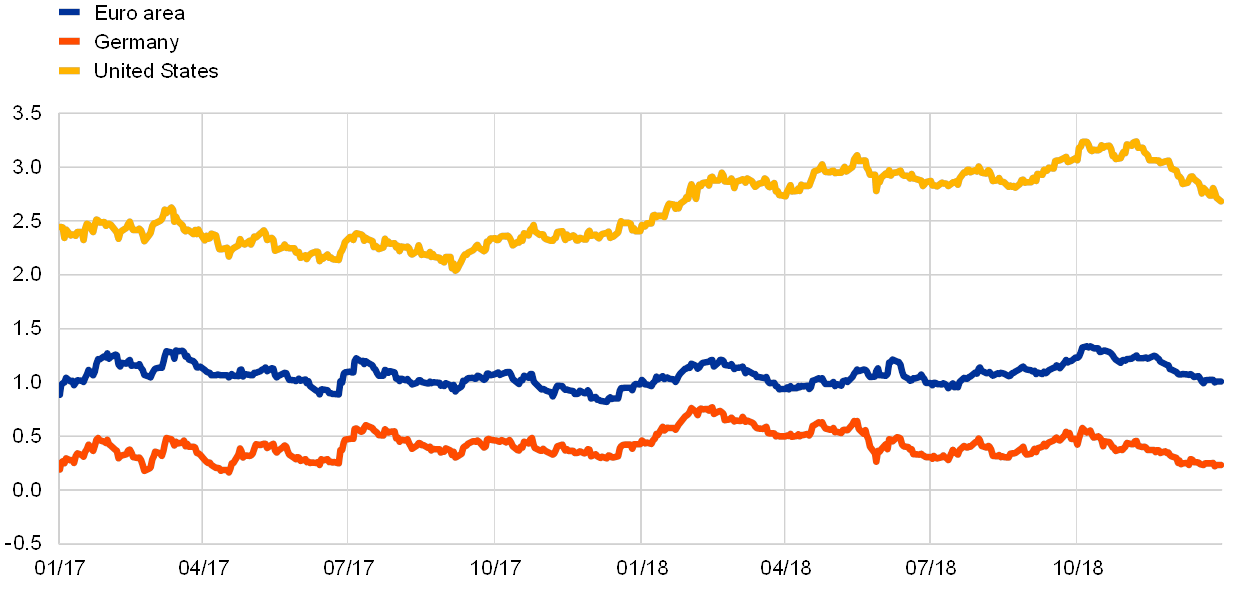

Euro area government bond yields remained broadly unchanged in 2018, albeit rising slightly towards the end of the year (see Chart 11). This largely reflected spillovers from the gradual withdrawal of monetary policy accommodation in the United States, as well as the widening in Italian spreads, which has so far had limited spillovers to other euro area sovereign bond markets. The euro area GDP-weighted average of ten-year sovereign bond yields stood at 1.01% on 31 December 2018, broadly unchanged from the average level in 2017. The spread of euro area countries’ ten-year sovereign bond yields against the German ten-year Bund yield increased moderately, against the background of prevailing fiscal policy uncertainty.

Chart 11

Ten-year sovereign bond yields in the euro area, the United States and Germany

(percentages per annum; daily data)

Sources: Bloomberg, Thomson Reuters Datastream and ECB calculations.

Notes: The euro area data refer to the ten-year GDP-weighted average of sovereign bond yields. The latest observations are for 31 December 2018.

Euro area equity prices decreased significantly

Euro area equity prices decreased significantly in 2018, amid increased global tensions, Italian political uncertainty and the gradual normalisation of monetary policy accommodation in advanced economies (see Chart 12). More specifically, a broad index for equity prices of euro area non-financial corporations (NFCs) declined by 12.6% over the course of 2018, while an index of euro area bank equity prices decreased by 33.3%. Equity prices of NFCs in the United States were more resilient than those in the euro area owing to the strong macroeconomic momentum, which was in part related to the procyclical fiscal stimulus.

Chart 12

Equity market indices in the euro area and the United States

(index: 1 January 2017 = 100) Source: Thomson Reuters Datastream.

Notes: The EURO STOXX banks index and the Datastream market index for NFCs are shown for the euro area; the S&P banks index and the Datastream market index for NFCs are shown for the United States. The latest observations are for 31 December 2018.

Financing conditions supported business investment

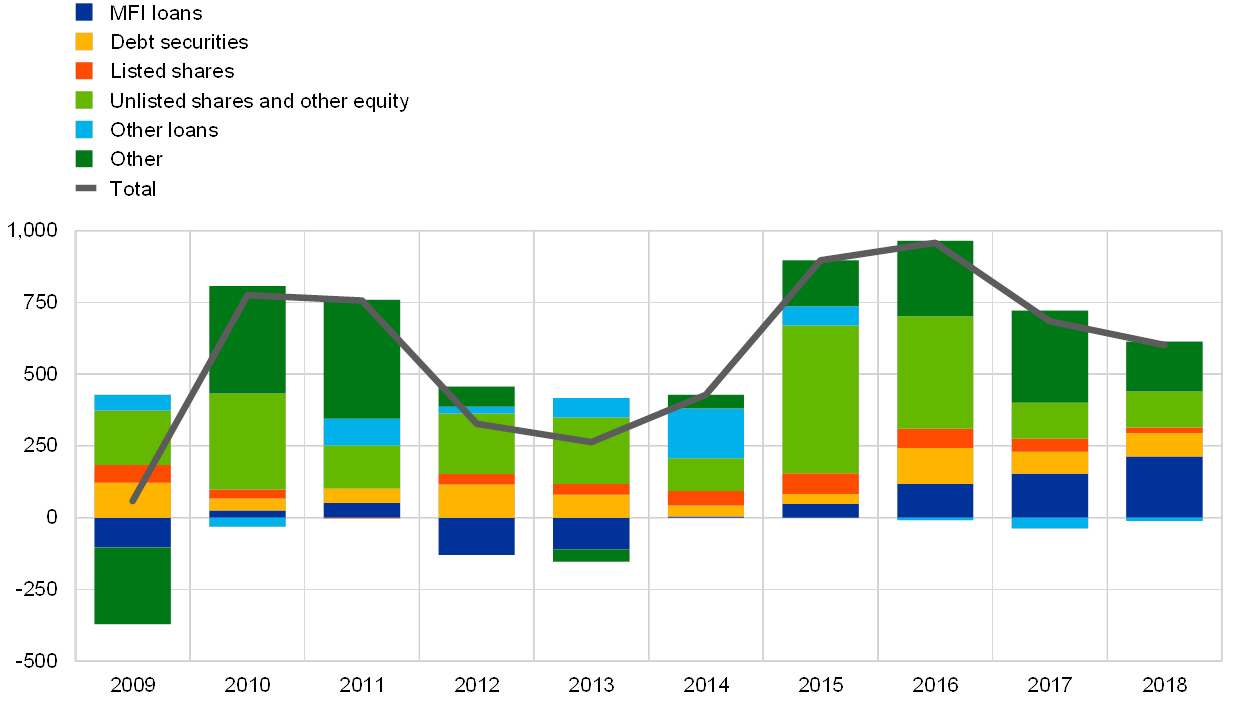

Overall, favourable financing conditions for NFCs continued to support business investment in 2018, although NFCs’ external financing flows decreased somewhat (see Chart 13). This decrease mainly reflected a moderation in “other” sources of financing (including inter-company loans and trade credit). At the same time, the net issuance of listed shares, unlisted shares and other equity was dampened by special factors and the relatively high cost of equity financing. Notwithstanding a gradual increase in corporate bond spreads over the course of 2018, debt securities issuance continued to be supported by the corporate sector purchase programme (CSPP), which was introduced in June 2016 (see Box 3). Moreover, the annual growth rate of bank loans to NFCs increased further in 2018. The recovery in loan growth has been supported by the significant decline in bank lending rates across the euro area since mid-2014 (see Section 2.1), which continued in 2018. This was in no small part due to the ECB’s non-standard monetary policy measures, which have brought about overall improvements in the supply of and demand for bank loans. In addition, banks have made progress in consolidating their balance sheets, although the volume of non-performing loans remained high in some countries.

Chart 13

Net flows of external financing to non-financial corporations in the euro area

(annual flows; EUR billions)

Sources: Eurostat and ECB.

Notes: “Other loans” include loans from non-MFIs (other financial institutions, insurance corporations and pension funds) and from the rest of the world. MFI and non-MFI loans are adjusted for loan sales and securitisations. “Other” is the difference between the total and the instruments listed in the chart. It includes inter-company loans and trade credit. The latest observations are for the third quarter of 2018.

Household wealth underpinned private consumption

Turning to households, their net wealth increased in the first three quarters of 2018, thus underpinning private consumption. In particular, continuous house price increases resulted in significant valuation gains on households’ real estate holdings. At the same time, decreases in share prices led to valuation losses on households’ financial asset holdings. While the annual growth rate of bank loans to households for house purchase remained moderate from a historical perspective, loan origination was strong.[13] Household gross indebtedness – measured as a percentage of household nominal gross disposable income – stood well above its average pre-crisis level.

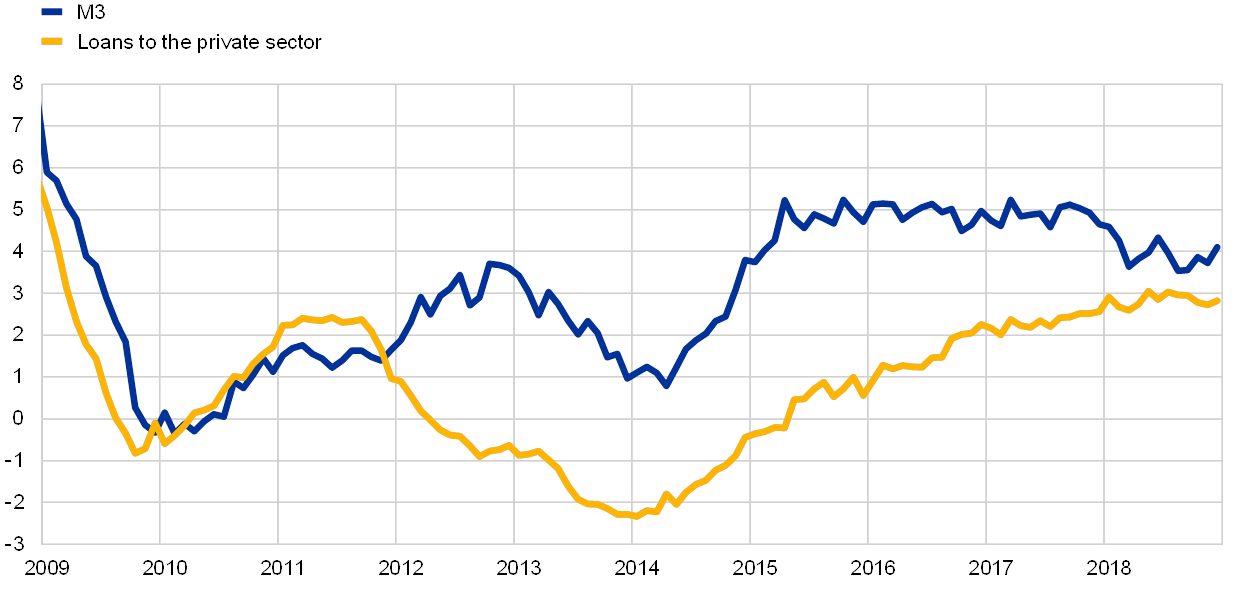

M3 growth was increasingly supported by credit growth

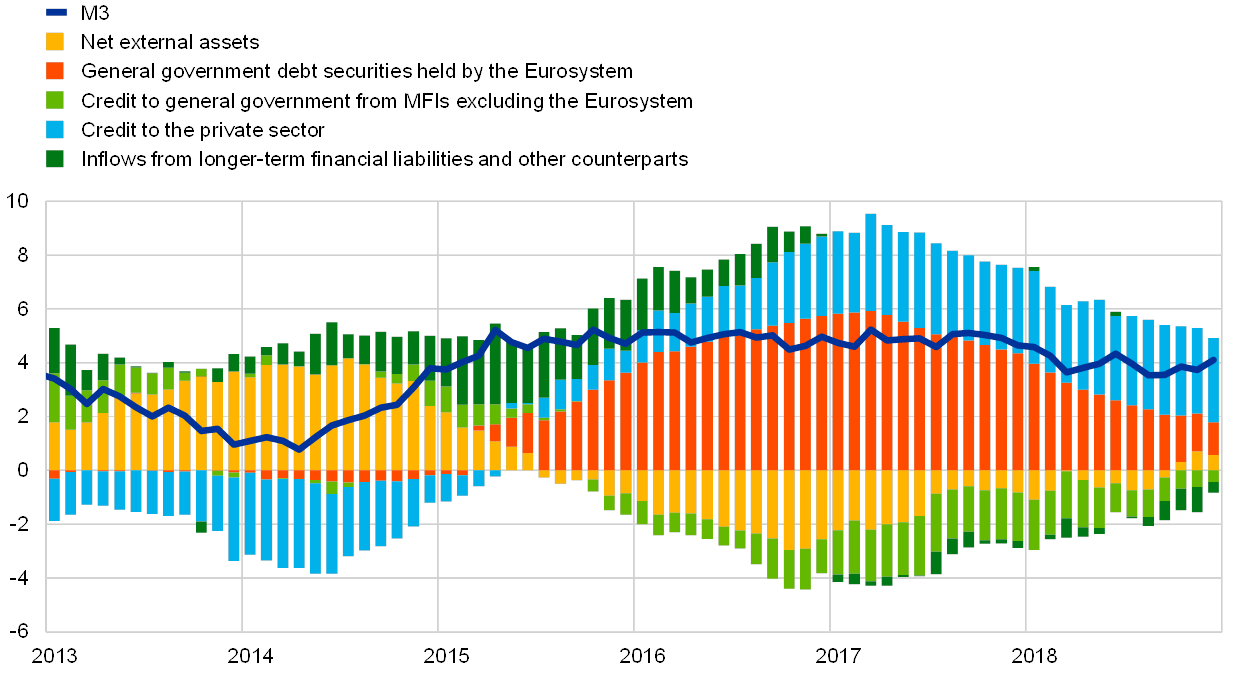

Overall, growth of loans to the private sector continued on the gradual upward trend observed since the beginning of 2014. The annual growth rate of MFI (monetary financial institution) loans to the private sector (adjusted for loan sales, securitisation and notional cash pooling) increased to 3.4% in December 2018, from 2.9% in December 2017 (see Chart 14). Credit growth therefore consolidated its role as a significant driver of broad money growth (see the blue parts of the bars in Chart 15), which nevertheless moderated compared with the steady pace of around 5% observed since mid-2015 (see Chart 14). Annual M3 growth stood at 4.1% in December 2018, compared with 4.6% at the end of 2017. The reduction in Eurosystem net asset purchases (from €80 billion to €60 billion in April 2017, to €30 billion in January 2018, to €15 billion in October 2018 and then to zero at the end of December 2018) has meant that the asset purchase programme had a smaller positive impact on M3 growth (see the red parts of the bars in Chart 15). At the same time, net government bond sales by euro area MFIs excluding the Eurosystem dampened M3 growth (see the light green parts of the bars in Chart 15). Despite the widening interest rate differential vis-à-vis non-euro area assets, the contribution from net external assets turned positive in net terms in October 2018 (see the yellow parts of the bars in Chart 15).

Chart 14

M3 and loans to the private sector

(annual percentage changes)

Source: ECB.

Chart 15

M3 and its counterparts

(annual percentage changes; contributions in percentage points; adjusted for seasonal and calendar effects)

Source: ECB.

Notes: Credit to the private sector includes MFI loans to the private sector and MFI holdings of securities issued by the euro area non-MFI private sector. As such, it also covers the Eurosystem’s purchases of non-MFI debt securities under the CSPP. The latest observations are for December 2018.

M3 was supported by overnight deposits

Growth in M3 continued to be driven by its most liquid components, given the low opportunity cost of holding liquid deposits in an environment characterised by very low interest rates and a flat yield curve. Growth in M1, which benefited from the elevated growth of overnight deposits held by both households and NFCs, declined as well and stood at 6.6% in December 2018, compared with 8.7% in December 2017.

2 Monetary policy: patience, prudence and persistence remain paramount

On the grounds of substantial progress towards a sustained adjustment in inflation, together with the underlying strength of the euro area economy and well-anchored inflation expectations, the monthly pace of net asset purchases under the asset purchase programme (APP) was gradually reduced throughout 2018 and the net purchases finished at the end of the year. Nevertheless, monetary policy remained patient, prudent and persistent and retained the ample degree of accommodation that was still needed to ensure the continued convergence of inflation to levels below, but close to, 2% over the medium term. Accommodation was provided by the residual net asset purchases, by the sizeable stock of acquired assets and the associated reinvestments, and by forward guidance on the key ECB interest rates, which remained at historical lows. At the end of 2018 monetary policy assets accounted for 72% of the Eurosystem’s balance sheet. The size of the balance sheet reached a historical high of €4.7 trillion. Risks related to the large balance sheet continued to be mitigated by the ECB risk management framework.

2.1 Winding-down of net asset purchases, while keeping policy accommodation ample

The monthly pace of net asset purchases under the APP was reduced from the start of 2018 on account of an increasingly robust and broad-based economic expansion

By the end of 2017 the euro area economy was experiencing an increasingly robust and broad-based economic expansion. Strong external demand contributed to growth, and increasing domestic demand underpinned the expansion, supported by employment gains, rising household wealth and corporate profitability, as well as very favourable financing conditions. Underlying price pressures remained subdued, but the steady absorption of economic slack gave grounds for increased confidence in a sustained adjustment in the path of inflation. On this basis, the Governing Council announced in October 2017 that it intended to reduce monthly purchase volumes under the APP from the beginning of 2018.

Accordingly, the monthly pace of net asset purchases under the APP was reduced from €60 billion to €30 billion as of January 2018. The Governing Council anticipated that the new monthly pace would run until the end of September 2018, or beyond, if necessary, and in any case until it saw a sustained adjustment in the path of inflation towards levels that are below, but close to, 2% over the medium term.

Low key policy rates, ongoing net asset purchases and reinvestment of principal payments continued to keep policy accommodation ample

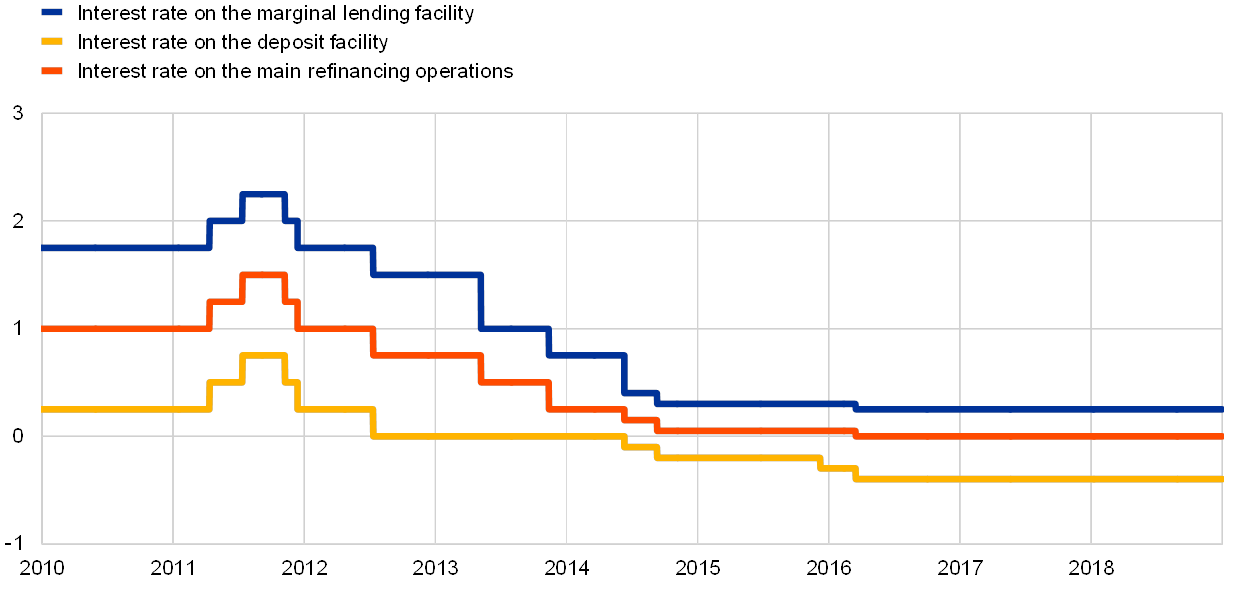

At the same time, the economic outlook and the path of inflation remained conditional on the continued support from the Governing Council’s policy measures. Monetary accommodation was provided by the ongoing net asset purchases. Moreover, the interest rate on the main refinancing operations and on the marginal lending facility and the deposit facility remained unchanged, at 0.00%, 0.25% and −0.40% respectively (see Chart 16). The monetary stimulus was further supported by the Governing Council’s forward guidance: key policy rates were expected to remain at their present levels for an extended period of time, and well past the horizon of net asset purchases. Additionally, the Governing Council intended to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of net asset purchases, and in any case for as long as necessary.

Chart 16

Key ECB interest rates

(percentages per annum)

Source: ECB.

Note: The latest observations are for 31 December 2018.

Despite some moderation from the very strong growth performance in 2017 on account of a weakening in export demand, domestic demand remained solid, supporting the broad-based expansion of the euro area economy through the first half of 2018. While risks of heightened financial market volatility and uncertainties relating to global factors, including protectionism, had gained prominence, the risks surrounding the euro area growth outlook remained broadly balanced.

High levels of capacity utilisation, labour market tightness and rising wage growth supported the further build-up of domestic price pressures. Measures of underlying inflation remained generally muted, but had increased from earlier lows. The June 2018 Eurosystem staff macroeconomic projections were consistent with a gradual convergence of inflation towards levels below, but close to, 2% over the medium term. Meanwhile, uncertainty surrounding the inflation outlook had been receding significantly and the risk of deflation had disappeared.

Confidence in the sustained convergence in the path of inflation

At its June meeting, the Governing Council assessed that progress towards a sustained adjustment in inflation had been substantial. The underlying strength of the euro area economy along with well-anchored inflation expectations provided grounds for confidence that the sustained convergence of inflation would continue, even after a gradual winding-down of net asset purchases.

In this context, the Governing Council at its June meeting decided to confirm that the Eurosystem would continue to make net asset purchases under the APP at a monthly pace of €30 billion until the end of September 2018. It was anticipated that, after September 2018, subject to incoming data confirming the medium-term inflation outlook, net asset purchases would be reduced to €15 billion a month for the period from October to December. After December net asset purchases were anticipated to end.

Recalibrated policy communication maintained monetary policy stimulus

At the same time, in the light of prevailing uncertainties, patience, prudence and persistence continued to be paramount as underlying price pressures remained contingent on a very substantial degree of monetary policy accommodation. Accordingly, credible and effective forward guidance on the use of the remaining policy instruments was provided as a means of further supporting the sustained convergence of inflation towards the ECB’s inflation aim:

- The Governing Council enhanced its forward guidance on the future path of policy rates: key policy rates were expected to remain at their then prevailing levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term. Adding an explicit date-based and state-contingent component to the guidance provided greater clarity on the future path of policy interest rates, thereby anchoring policy rate expectations more firmly to support the financial conditions underpinning a continued convergence of inflation towards the inflation aim. The state-contingent component of the forward guidance, explicitly linking a first policy rate rise to inflation evolving along a sustained adjustment path, was consistent with a forward-looking and medium-term-oriented monetary policy strategy and underscored the credibility of the Governing Council’s commitment to its price stability objective. At the same time, the enhanced rate forward guidance maintained adequate policy flexibility.

- Moreover, forward guidance on the reinvestment of the principal payments from maturing securities purchased under the APP was reconfirmed. The reinvestment horizon would continue for an extended period of time after the end of net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

In the light of still prevailing uncertainties and only gradually rising underlying inflation, monetary policy had to remain patient, prudent and persistent. Even if the net flows under the APP were coming to an end, monetary policy would have to remain highly accommodative. Meanwhile, the June decision initiated a rotation from net asset purchases towards the policy interest rates and forward guidance on their likely future evolution as a means of steering the monetary policy stance. All in all, communication had to be carefully balanced between anticipating a termination of net asset purchases by the end of 2018 and highlighting the continued commitment to provide sufficient monetary stimulus for as long as necessary.

Throughout the autumn new information came in weaker than expected, reflecting softer external demand but also some country and sector-specific factors. While some of these factors were likely to unwind, others could indicate a moderation in the growth momentum. At the same time, the underlying strength of domestic demand continued to underpin the expansion of the euro area economy and gradually rising inflation pressures. Domestic cost pressures continued to strengthen and broaden, amid high levels of capacity utilisation and tightening labour markets, which pushed up wage growth. Overall, risks surrounding the growth outlook were still assessed as broadly balanced. Nevertheless, the balance of risks was moving to the downside owing to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility, which had gained more prominence during the summer and remained prominent towards the end of the year.

The APP ended, but monetary policy needed to remain very accommodative

In December, on the basis of incoming information, the Governing Council reviewed the economic outlook and concluded that the overall assessment broadly confirmed the outlook from June. The underlying strength of domestic demand continued to support confidence that the sustained convergence of inflation to the ECB’s aim was proceeding and would be maintained even after the end of net asset purchases. On this basis, the Governing Council found it appropriate to end net asset purchases under the APP in December 2018, as previously anticipated. At the same time, the continued inflation convergence still required monetary policy to be patient, prudent and persistent. Therefore, the forward guidance on reinvestment was enhanced. Accordingly, the Governing Council intended to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation. Linking the reinvestment horizon to the interest rate lift-off confirmed that the key ECB interest rates and the associated forward guidance on their likely future evolution would remain the primary tool to adjust the monetary policy stance going forward. The rate forward guidance, reinforced by the reinvestments of the sizeable stock of acquired assets, would provide the necessary degree of accommodation for the sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

Policy measures continued to ensure very favourable financing conditions and support the economic expansion

Smooth implementation of net asset purchases

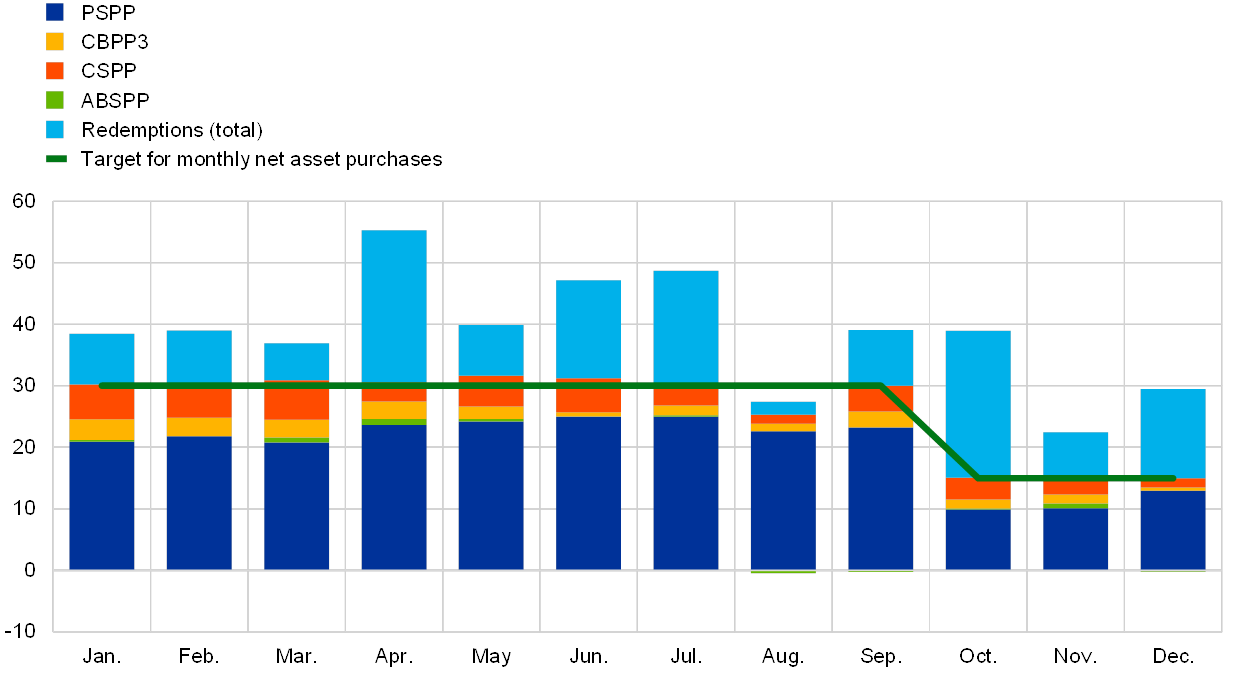

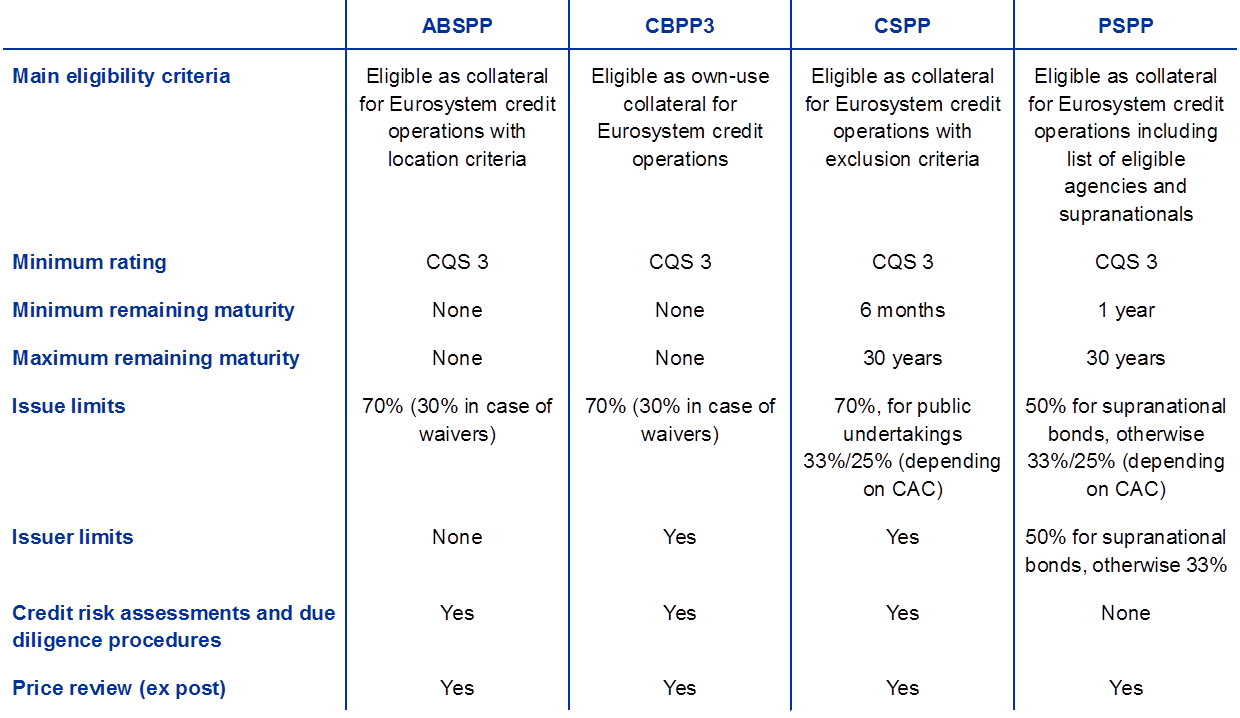

The implementation of the APP proceeded smoothly, both in the public sector purchase programme (PSPP) and in the private sector purchase programmes, encompassing the asset-backed securities purchase programme (ABSPP), the corporate sector purchase programme (CSPP) and the third covered bond purchase programme (CBPP3). Monthly net purchase volumes were, on average, in line with the monthly targets set by the Governing Council, at €30 billion per month from January to September and at €15 billion per month from October to December (see Chart 17). Net purchase volumes were below the monthly target in August due to seasonal fluctuations in market liquidity, but this was offset by slightly higher purchase volumes during the rest of the year. At the individual country level, redemptions of debt securities held in the various programme portfolios caused sizeable fluctuations in gross monthly purchases. Overall, net monthly purchases deviated only marginally from the target volumes in relative terms. The stock of PSPP holdings at year-end was broadly in line with the envisaged country allocation guided by the capital key. The implementation of the PSPP had not adversely affected euro area sovereign bond market liquidity conditions (see Box 2). The targeted longer-term refinancing operations (TLTROs) (see Section 2.2) contributed to favourable financing conditions, supporting the continued adjustment in the path of inflation.

Chart 17

Monthly net asset purchases and redemptions under the APP in 2018

(EUR billions)

Source: ECB.

Notes: Monthly net purchases at book value; monthly actual redemption amounts. Principal redemptions on securities purchased under the PSPP are reinvested by the Eurosystem in a flexible and timely manner in the month they fall due on a best-efforts basis, or in the subsequent two months if warranted by market liquidity conditions.

Box 2

Euro area sovereign bond market liquidity and implementation of the public sector purchase programme

The liquidity of euro area sovereign bond markets is important for the transmission of the ECB’s monetary policy. In particular, a liquid market fosters the link between the ECB’s monetary policy decisions, the yield curve, financial asset prices in general, and the overall funding cost and allocation of capital in the economy. The need to closely monitor the liquidity of sovereign bond markets has increased since the launch of the ECB’s PSPP, under which the Eurosystem has purchased a significant share of outstanding euro area sovereign bonds. Against this background, this box presents two of the market liquidity indicators that the ECB monitors regularly. Overall, these indicators suggest that liquidity conditions in sovereign bond markets did not react markedly to the start of the PSPP or to changes in the amount of monthly purchases.

A liquid market is typically characterised as one in which the execution of a standard transaction has a limited impact on prices. In other words, a liquid market has “deep” order books, which are quickly replenished once a trade has been executed. As a result, price changes following a trade would be minimal and temporary. Naturally, if an executed trade is believed to provide new information about the fundamental value of the asset being traded, there would be a commensurate adjustment in quoted ask and bid prices, but the order book around the new levels would still remain deep.

Market liquidity indicators commonly focus on one or more aspects of the cost of transactions, market depth and/or resiliency. The simplest indicator is the quoted bid-ask spread, which provides information on how costly a transaction is expected to be. More informative indicators can be constructed by combining this spread information with, for example, order book depth, which is a gauge of the volume of transactions that the market can comfortably absorb at a given point in time. Measures of market depth are typically based on information obtained from limit order books[14], which are the real-time volume and price schedules available to traders. Resiliency is a function of market dynamics, such as how long it takes for order books to be refilled after a trade has been executed, i.e. it focuses on the time dimension of market liquidity.

This box looks at euro area sovereign bond market liquidity based on an order book liquidity indicator[15] and an execution-based liquidity indicator[16]. Although these indicators are based on different sets of market data (limit order books and quotes respectively), they mainly focus on the cost and depth dimensions of liquidity.

Both the order book liquidity indicator and the execution-based liquidity indicator suggest that the liquidity situation in euro area sovereign bond markets has not deteriorated since the start of the PSPP (see Chart A). While both indicators have displayed quite some volatility within the observed time period, they have not recorded a sustained upward trend, notwithstanding the significant build-up of PSPP holdings over time. In the same vein, the indicators have generally not displayed a marked reaction to changes in the amount of monthly purchases under the PSPP, even though the aggregate may mask some cross-country heterogeneity.

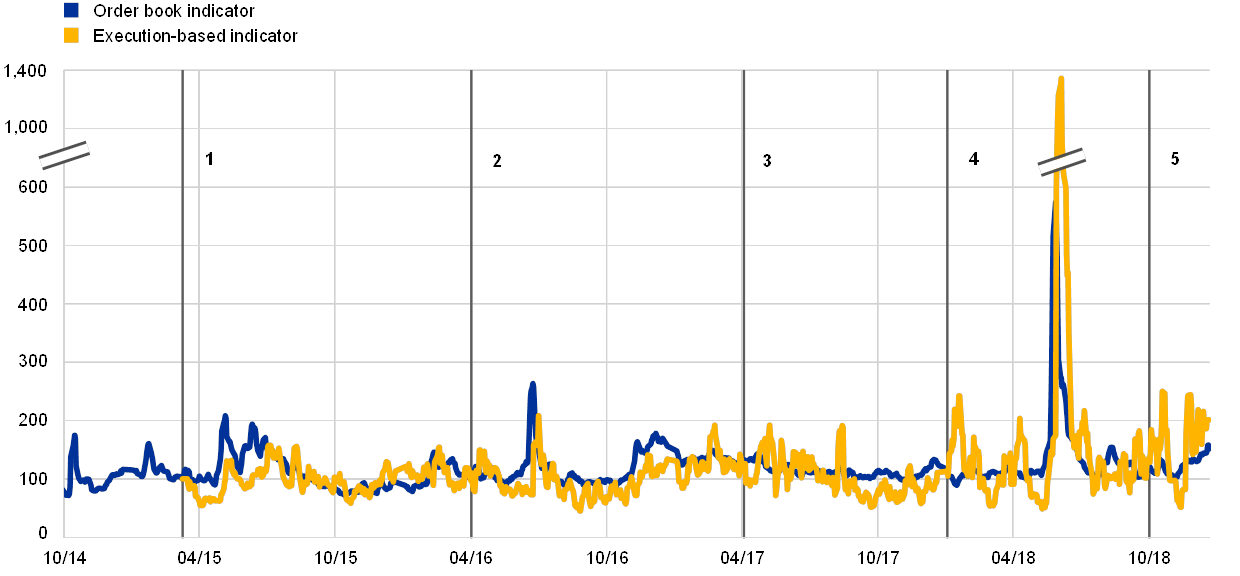

Chart A

Euro area sovereign bond market liquidity indicators since the start of the PSPP

(index: 100 = 9 March 2015)

Sources: Bloomberg, EuroMTS Ltd and ECB calculations.

Notes: An increase (decrease) in the indicators implies a deterioration (improvement) in the liquidity situation. The chart shows the five-day moving average of the indicators. The order book indicator is a euro area-wide GDP-weighted average of ten-year sovereign bonds and the execution-based indicator is a volume-weighted average for sovereign bonds traded under the PSPP. They are normalised to 100 on 9 March 2015, when purchases under the PSPP began. The vertical lines denote the following volume changes in asset purchases under the PSPP: (1) the start of the programme, with a monthly volume of €60 billion (9 March 2015); (2) the increase in net monthly purchases to €80 billion (1 April 2016); (3) the decrease in net monthly purchases to €60 billion (3 April 2017); (4) the decrease in net monthly purchases to €30 billion (2 January 2018); and (5) the decrease in net monthly purchases to €15 billion (1 October 2018). The latest observations are for 21 December 2018. Values above 600 are scaled down by a factor of 4.

Chart A shows that these liquidity indicators tend to spike around political and economic events associated with an expected deterioration in market liquidity. For instance, spikes were observed during the “Bund tantrum”[17] period (commencing on 28 April 2015) and following the United Kingdom’s referendum on EU membership (23 June 2016). The presidential elections in the United States (8 November 2016) and France (23 April 2017) were also marked by higher readings of these indicators. The largest spike in illiquidity can, however, be observed during the period of political tensions related to the formation of the new Italian government (period commencing on 28 May 2018), when liquidity deteriorated especially in the Italian market. These spikes reflect mostly country-specific deteriorations in liquidity with limited spillovers to other markets. Moreover, liquidity usually deteriorates during the summer and around the year-end, although this is less obvious in the chart, given the wide scale. Finally, movements in the execution-based indicator resemble those seen in the order book indicator, but appear to reflect more noise. A composite indicator constructed using robust weighting methodologies or aggregating across a broad set of measures could mitigate the noise in the individual measures.

Banks’ very favourable financing conditions were passed on to firms and households

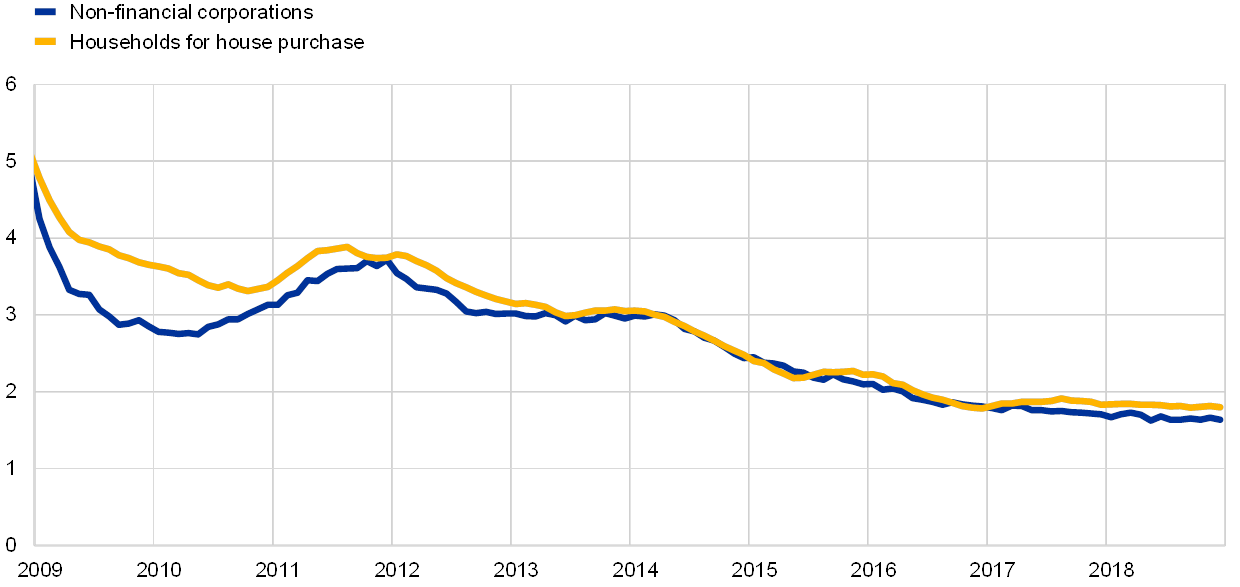

The accommodative monetary policy stance and the strengthening of bank balance sheets continued to contribute to low bank funding costs. Despite an increase in the dispersion of funding costs across euro area countries in the second half of 2018, these costs remained well below the levels seen prior to the adoption of the ECB’s credit easing measures in June 2014 (see Chart 18). Banks’ very favourable financing conditions were passed on to the wider economy, with borrowing conditions for firms and households continuing to be attractive across the euro area. Bank lending rates for non-financial corporations (NFCs) and households remained close to their historical lows. Between the beginning of June 2014 and December 2018, they declined by around 130 and 110 basis points, respectively, which is significantly more than the change in market reference rates (see Chart 19).

Chart 18

Composite cost of debt financing for banks

(composite cost of deposit and unsecured market-based debt financing; percentages per annum)

Sources: ECB, Markit iBoxx and ECB calculations.

Note: The composite cost of deposits is calculated as an average of new business rates on overnight deposits, deposits with an agreed maturity and deposits redeemable at notice, weighted by their corresponding outstanding amounts.

Chart 19

Composite bank lending rates for non-financial corporations and households

(percentages per annum)

Source: ECB.

Note: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes.

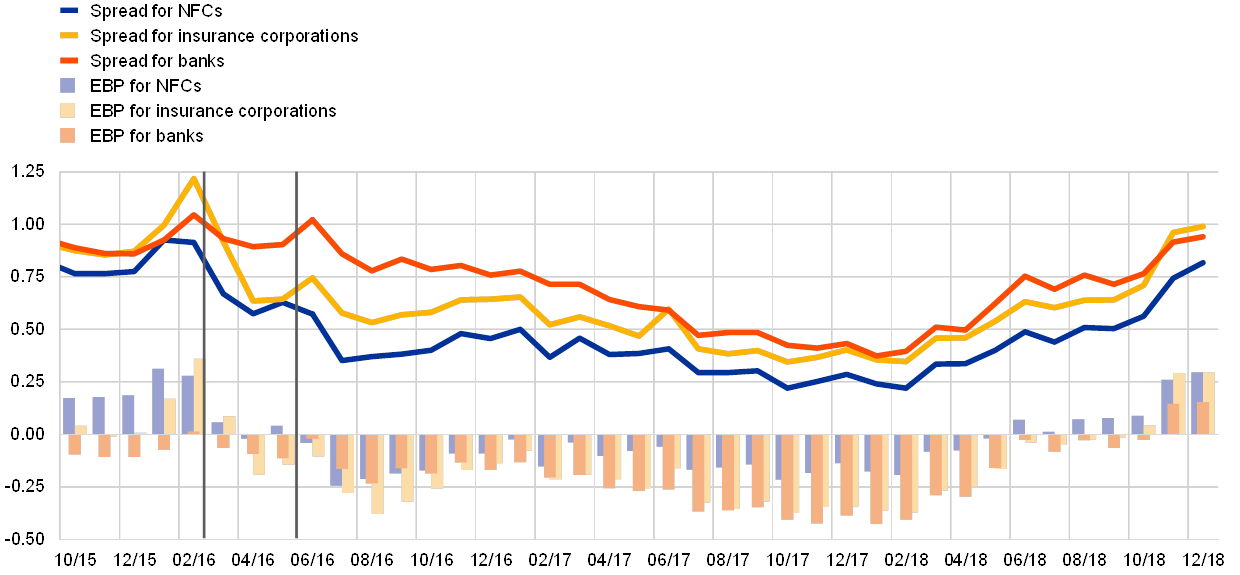

Market-based funding costs for NFCs also remained very favourable, supported by the continued spread-compressing impact of the CSPP net purchases (see Box 3). Nevertheless, investment-grade NFC bond spreads widened gradually and steadily throughout 2018 from post-crisis lows due to increasing uncertainties surrounding the euro area and global growth outlook.

Credit flows to the private sector continued to benefit from the very favourable financing conditions. The growth in bank lending to NFCs and households continued on the gradual upward trend observed since the beginning of 2014 (see Section 1.4). Net debt securities issuance by NFCs continued to be supported by the CSPP despite moderating somewhat compared with last year (see Box 3). According to the ECB’s securities issues statistics[18], net new issues denominated in euro amounted to €56 billion in the first eleven months of 2018, compared with €91 billion in the same period of 2017. Net new issues denominated in other currencies amounted to −€3 billion in the first eleven months of 2018, and −€7 billion in the same period of 2017, which is consistent with the CSPP providing an incentive to euro area NFCs to issue new debt in euro and redeem debt in other currencies.

Low policy rates and the APP increased lending volumes and eased banks’ conditions on new loans

Banks continued to report an easing of credit standards and overall terms and conditions on new loans, supported by the ECB’s monetary policy measures. According to the euro area bank lending survey, the APP continued to have an easing impact on banks’ overall terms and conditions on new loans to enterprises and households. Moreover, the ECB’s monetary policy measures had a positive impact on bank lending volumes. Low interest rates and the ongoing economic expansion in the euro area continued to support demand for credit (see Section 1.4). According to the latest Survey on the Access to Finance of Enterprises (SAFE)[19], the availability and conditions of external financing for small and medium-sized enterprises (SMEs) further improved in 2018, supported by the substantial monetary policy accommodation and the enhanced financing conditions of SMEs (see Box 3).

Box 3

The effect of the corporate sector purchase programme on the financing of non-financial corporations in the euro area

The aim of the corporate sector purchase programme, which forms part of the ECB’s asset purchase programme, is to ease the financing conditions of the euro area real economy. ECB analysis summarised in this box suggests that the CSPP led to a significant easing in financing conditions for euro area non-bank corporations. It did so by contributing to a decline in corporate bond spreads, as well as an improvement in the supply conditions in the primary corporate bond market. Furthermore, the CSPP may have contributed to increasing bank credit to NFCs that do not tap the corporate bond market.[20]

The CSPP is part of the APP

The CSPP consists of purchases by the Eurosystem of investment-grade euro-denominated bonds issued by non-bank corporations (i.e. non-financial corporations and insurance corporations) established in the euro area. It was announced on 10 March 2016 and purchases started on 8 June 2016. Since then the Eurosystem has purchased debt securities issued by NFCs in both the primary and the secondary markets. Those securities had to be eligible as collateral for Eurosystem refinancing operations and denominated in euro. By the time the net asset purchases under the APP ended in December 2018, the Eurosystem held €178 billion of corporate bonds, which represented slightly less than 7% of the total outstanding assets held as a consequence of APP purchases.

Impact on NFC financing costs: the tightening of corporate bond spreads

Since the announcement of the CSPP in March 2016, corporate bond spreads steadily tightened until the end of 2017, only to climb back up again gradually in the course of 2018 (see Chart A). Econometric analysis[21] shows that the steady decline of corporate bond spreads for CSPP-eligible bonds between mid-2016 and the end of 2017 can largely be attributed to the CSPP. The decline in eligible corporate bond spreads, in turn, induced portfolio rebalancing effects and resulted in a decline also in the spreads on corporate bonds that are not eligible for purchase under the CSPP[22]. In 2018 both global and domestic euro area uncertainties more than counterbalanced the impact of the CSPP and contributed to the gradual increase of credit risk and, therefore, of corporate bond spreads. The cessation of net asset purchases under the CSPP at the end of 2018, and the removal of the demand pressure which it implied, coincided with an increase in credit risk premia and corporate bond valuations towards values observed before the announcement of the programme.

Chart A

Investment-grade corporate bond spreads and “excess bond premia” in the euro area

(monthly data; percentage points)

Sources: Merrill Lynch indices and ECB calculations.

Notes: The “excess bond premium” (EBP) is the deviation of the corporate credit spread from the measured default risk of the issuer. The series shown only includes investment-grade bonds. The vertical lines indicate the Governing Council meetings of 10 March 2016 and 2 June 2016. See De Santis, R.A., “Credit spreads, economic activity and fragmentation”, Working Paper Series, No 1930, ECB, July 2016. The latest observations are for December 2018.

Impact on NFC debt securities issuance

The CSPP also contributed to improving supply conditions in primary corporate bond markets, particularly among eligible issuers. Net issuance by NFCs picked up in March 2016, coinciding with the CSPP announcement and the decline in corporate bond spreads. Since then it has remained stronger than in previous years. Furthermore, the newly issued CSPP-eligible bonds carried a longer maturity, which contributed to lengthening significantly the average residual maturity of outstanding senior unsecured investment-grade bonds issued by NFCs. Lastly, empirical evidence suggests that the CSPP continued to foster NFC issuance of new eligible bonds denominated in euro rather than in other currencies. The low-yield environment and low corporate bond spreads also seem to have fostered issuance by lower-rated issuers.

Impact on the NFC funding structure

The rising NFC bond issuance observed over the past two and a half years reflects, at least initially, a shift by some firms from loans to market-based debt funding.[23] ECB analysis covering the period from end-2015 until mid-2017 shows that in a large sample of euro area NFCs, those firms issuing bonds that were eligible for the CSPP recorded a rise in the share of bonds and a fall in the share of long-term loans in their total debt liabilities.

This micro evidence is confirmed by the aggregate financial accounts of euro area NFCs. Between the announcement of the CSPP and mid-2017 the share of new bank loans taken out by euro area firms relative to that of new net debt securities issued by them declined on an annual basis. Thus, euro area NFCs shifted their funding structure towards debt instruments. Despite this, since mid-2016 the net flow of bank loans to the NFC sector has been positive and has even accelerated. From mid-2017 euro area NFCs gradually reversed the temporary substitution of debt securities for bank loans and the relative share of new bank loans taken out increased again until the end of 2018.

Impact on banks’ loan supply

Finally, when combining the data with survey evidence, it seems that the CSPP may have contributed to freeing up bank balance sheet capacity that was subsequently used to expand lending to CSPP-ineligible (mainly smaller) firms.[24] The Survey on the Access to Finance of Enterprises shows that the net percentage of small and medium-sized enterprises reporting improvements in the willingness of banks to provide credit, which has exhibited an increasing trend since 2014, increased further somewhat in the first half of 2016, when the CSPP was introduced. This effect seems most evident in France where companies have accounted for a large share of the higher bond issuance seen since the CSPP announcement.

Monetary policy measures since 2014 contributed substantially to the improved economic performance of the euro area

The ample degree of monetary policy accommodation introduced since 2014 has contributed substantially to the improvement in the economic performance of the euro area, supporting the convergence of inflation towards the Governing Council’s inflation aim. Private consumption was supported by ongoing employment gains, which – in turn – partly reflected past labour market reforms, and by growing household wealth. Business investment was fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remained robust. Considering all the monetary policy measures taken since mid-2014, the overall impact on euro area real GDP growth and euro area inflation is estimated to be – in both cases – around 1.9 percentage points cumulatively between 2016 and 2020.[25]

2.2 Eurosystem balance sheet dynamics towards the end of net asset purchases

Since the onset of the global financial crisis in 2007-08 the Eurosystem has taken a variety of standard as well as non-standard monetary policy measures, which have had a direct impact on the size and composition of the Eurosystem’s balance sheet over time. The non-standard measures have included collateralised lending operations to provide funding to counterparties with an initial maturity of up to four years, as well as purchases of assets issued by private and public entities (under the APP), in order to improve the transmission of monetary policy and ease financing conditions in the euro area. Over the course of 2018 the Eurosystem’s balance sheet continued to grow on account of these non-standard policy measures and, by the end of 2018, its size had reached a historical high of €4.7 trillion, an increase of €0.2 trillion compared with the end of 2017.

The APP led to a further expansion of the Eurosystem’s balance sheet in 2018, although at a somewhat lower rate than in previous years as monthly net asset purchases were reduced (see Section 2.1). At the end of 2018 monetary policy-related items on the assets side amounted to €3.4 trillion, accounting for 72% of the total assets on the Eurosystem’s balance sheet (up from 70% at the end of 2017). These monetary policy-related assets include loans to euro area credit institutions, which accounted for 16% of total assets (down from 17% at the end of 2017), and assets purchased for monetary policy purposes, which represented around 56% of total assets (up from 53% at the end of 2017) (see Chart 20). Other financial assets on the balance sheet mainly consisted of: (i) foreign currency and gold held by the Eurosystem; (ii) euro-denominated non-monetary policy portfolios; and (iii) emergency liquidity assistance provided by some Eurosystem national central banks (NCBs) to solvent financial institutions facing temporary liquidity problems. These other financial assets are subject to internal Eurosystem reporting requirements and restrictions arising in particular from the monetary financing prohibition and the requirement that they should not interfere with monetary policy, which are set out in various legal texts.[26]