Céard atá i gceist le ANFA?

Tugtha cothrom le dáta an 13 Meán Fómhair 2024 (foilsíodh den chéad uair an 5 Feabhra 2016)

Is comhaontú é an Comhaontú maidir le Glansócmhainní Airgeadais (ANFA) idir bainc cheannais náisiúnta (BCNanna) an limistéir euro agus an Banc Ceannais Eorpach (BCE), arb ionann iad le chéile agus an tEurochóras. Leagtar síos sa chomhaontú rialacha agus teorainneacha maidir le sealúchais sócmhainní airgeadais a bhaineann le cúraimí náisiúnta na BCNanna. Áirítear ar shócmhainní airgeadais den sórt sin BCNanna, mar shampla, an chontrapháirt dá gcúlchistí caipitil agus cuntasaíochta nó dliteanais shonracha eile, a gcúlchistí eachtracha agus cistí pinsin fostaithe nó sócmhainní a shealbhaítear chun críocha infheistíochta ginearálta.

Is cuid dhílis de na feidhmeanna a fheidhmíonn bainc cheannais san Eoraip sócmhainní airgeadais a shealbhú nach mbaineann le beartas airgeadaíochta, agus tagann sé roimh an euro. Nuair a bunaíodh an t-aontas airgeadaíochta, chinn rialtais gan ach na feidhmeanna agus na cúraimí sin de chuid an bhainc ceannais is gá a fhrithpháirtiú chun beartas aonair airgeadaíochta a sheoladh don limistéar euro ina iomláine. Ag an am céanna, chinn siad BCNanna a choinneáil mar institiúidí neamhspleácha ar féidir leo leanúint de chúraimí náisiúnta a dhéanamh ar choinníoll nach gcuireann na cúraimí sin isteach ar an mbeartas aonair airgeadaíochta.

I bhfocail eile: Is institiúidí atá neamhspleách ó thaobh airgeadais de iad na BCNanna agus déanann siad cúraimí beartais airgeadaíochta a bhaineann leis an bpríomhról atá ag an Eurochóras cobhsaíocht praghsanna a choinneáil chomh maith le cúraimí náisiúnta. Bunaíodh ANFA chun teorainn fhoriomlán a shocrú do ghlanmhéid iomlán na sócmhainní airgeadais a bhaineann le cúraimí beartais náisiúnta, neamhairgeadaíochta, ionas nach gcuirfeadh siad isteach ar bheartas airgeadaíochta.

Cén chaoi a n-oibríonn ANFA?

Tá sócmhainní ag gach banc ceannais nach mbaineann le beartas airgeadaíochta. Sa limistéar euro, socraíonn Comhairle Rialaithe BCE beartas airgeadaíochta go lárnach do na Ballstáit uile. Nuair a bunaíodh an tAontas Eacnamaíoch agus Airgeadaíochta, leag rialtais amach sa Chonradh Eorpach go n-aistreofaí cúraimí a bhaineann le beartas airgeadaíochta chuig an leibhéal Eorpach. Taobh amuigh de bheartas airgeadaíochta, bheadh – agus tá – cead ag na BCNanna cúraimí náisiúnta a dhéanamh. Tá an prionsabal sin leagtha síos in Airteagal 14.4 de Reacht an CEBC agus BCE.

Go praiticiúil, tá sócmhainní ag na BCNanna faoi láthair nach mbaineann le beartas airgeadaíochta ná le seoladh oibríochtaí um malairt eachtrach an Eurochórais, amhail:

- ór nó cúlchistí malairte eachtraí;

- punanna infheistíochta, e.g. le haghaidh cistí pinsin na foirne;

- sócmhainní a shealbhaítear mar fhrithshuíomhanna do thaiscí ó chustaiméirí, e.g. rialtais intíre nó bainc cheannais eachtracha.

Ag an am céanna, tá dliteanais ag na BCNanna freisin nach mbaineann le beartas airgeadaíochta, lena n-áirítear na taiscí thuasluaite ó rialtais intíre, ó bhainc cheannais eachtracha nó ó institiúidí de chuid an AE. Is féidir leis na BCNanna na cúraimí náisiúnta sin a shaothrú fad is nach gcuireann a ngníomhaíochtaí isteach ar chuspóirí agus ar chúraimí an Chórais Eorpaigh Banc Ceannais (CEBC), go háirithe beartas airgeadaíochta. Ar an gcaoi chéanna, tá punann cistí dílse ag BCE a bhaineann lena chaipiteal agus lena chúlchiste cuntasaíochta, chomh maith le punann ciste pinsin foirne.

Bhí na punanna infheistíochta thuasluaite ag BCNanna cheana féin sula ndeachaigh siad isteach san Eurochóras, agus cuireann a n-ioncam le hioncam airgeadais na BCNanna. Nuair a bunaíodh an limistéar euro, tugadh faoi deara go gcuideodh na punanna sin leis an éileamh ar chóras baincéireachta an limistéir euro ar leachtacht a shásamh, ionas go gcuirfí san áireamh iad agus oibríochtaí beartais airgeadaíochta á gcalabrú. Ó thaobh an bheartais airgeadaíochta de, níor measadh go raibh fadhb ann go leanfadh na BCNanna de phunanna den sórt sin a bhainistiú, lasmuigh d'oibríochtaí beartais airgeadaíochta, agus go bhféadfaí ligean dóibh fás le himeacht ama ag an ráta céanna (nó níos moille) leis an éileamh ar nótaí bainc agus riachtanais chúltaca an chórais baincéireachta. Mheas an Chomhairle Rialaithe freisin, dá bhfásfadh punanna beartais neamh-airgeadaíochta, glan ó dhliteanais bheartais neamhairgeadaíochta, níos tapúla ná an t-éileamh ar leachtacht ar feadh tréimhse fhada ama, go bhféadfadh sé sin beartas airgeadaíochta a chur i mbaol. Bunaíodh ANFA chun an fás seo a bhainistiú agus a theorannú.

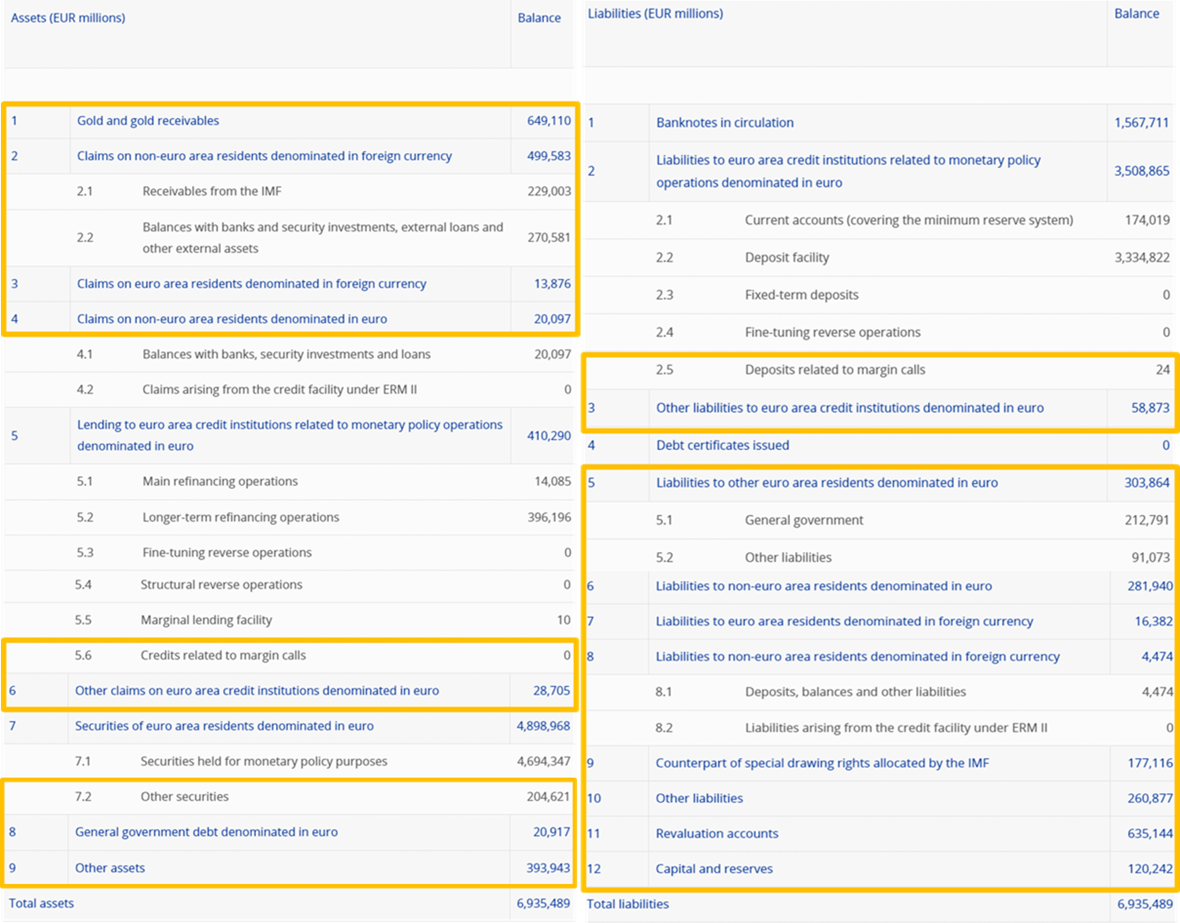

Ar an tsócmhainn agus ar thaobh dliteanais chlár comhardaithe bainc ceannais, tá suíomhanna ann nach mbaineann go díreach le beartas airgeadaíochta. Sainmhínítear an difríocht idir an dá shraith suíomhanna mar ghlansócmhainní airgeadais nó NFA. Léirítear an coincheap seo thíos, ag baint úsáide as clár comhardaithe ráiteas airgeadais seachtainiúil an Eurochórais amhail ón 29 Nollaig 2023, mar a foilsíodh ar shuíomh gréasáin BCE. Tugtar sainmhíniú beacht in Iarscríbhinn I de ANFA.

Léirítear sa léaráid go n-áiríonn NFA, ar thaobh na sócmhainne, suim de mhíreanna 1 go 4, 5.6, 6, 7.2, 8 agus 9 sa chlár comhardaithe. Ar thaobh an dliteanais tá míreanna 2.5 agus 3 go 12 san áireamh. Má dhealaíonn tú suim na ndliteanas seo ó shuim na sócmhainní thuasluaite (i.e. na codanna faoi seach a aibhsítear in oráiste thíos), gheobhaidh tú glansócmhainní airgeadais an Eurochórais.

Amhail an 29 Nollaig 2023, sheas NFA an Eurochórais ag -€28 billiún. Sna blianta roimhe sin, bhí laghdú leanúnach tagtha ar NFA an Eurochórais, go mór mór mar gheall ar an taobh dliteanais méadaitheach den chlár comhardaithe a rinne níos mó ná forbairtí dearfacha lena mbaineann ar thaobh na sócmhainne a fhritháireamh, mar a mhínítear thuas. Aisiompaíodh an treocht sin in 2023, áit ar tháinig méadú ar NFA an Eurochórais i gcaitheamh na bliana, rud a spreag laghdú suntasach ar thaobh dliteanais an chláir chomhardaithe den chuid is mó. Laghdú ar thaiscí beartais neamhairgeadaíochta ba chúis leis sin go príomha, agus rinne an Chomhairle Rialaithe luach saothair na dtaiscí sin a choigeartú roinnt uaireanta le blianta beaga anuas, lena n-áirítear i Meán Fómhair 2022 agus i mí Feabhra 2023.

Forbairt NFA i gcomparáid le nótaí bainc agus íoscheanglais chúltaca (MRR) (in € billiún)

Cuireann ANFA teorainn leis an méid NFA is féidir le bainc cheannais náisiúnta a shealbhú. Tá sé seo riachtanach chun a áirithiú nach gcuirfidh na hathruithe ar leachtacht a bhaineann le gluaiseachtaí in NFA na BCNanna isteach ar chur chun feidhme éifeachtach an bheartais airgeadaíochta. Roimh ghéarchéim airgeadais 2007-08, ba é an bealach ba éifeachtaí chun beartas airgeadaíochta a chur chun feidhme ná trína chinntiú go raibh ar na bainc leachtacht a iarraidh ón Eurochóras. Bhí ganntanas leachtachta maidir leis an Eurochóras, dá ngairtear “easnamh leachtachta” freisin, mar bhonn le cur chun feidhme an bheartais airgeadaíochta. Chosain ANFA an t-easnamh leachtachta seo. Nuair a bhuail an ghéarchéim airgeadais, bhí sé riachtanach níos mó leachtachta a chur ar fáil do na bainc ná mar a bhí ag teastáil uathu i ndáiríre chun na híoscheanglais chúltaca a chomhlíonadh. Anois, in ionad oibriú le heasnamh leachtachta, tá an córas baincéireachta ag feidhmiú le róleachtacht. Sa timpeallacht sin, cinntíonn ANFA nach sáraíonn róleachtacht an leibhéal a mheasann an Chomhairle Rialaithe a bheith iomchuí dá seasamh maidir le beartas airgeadaíochta.

Ní hea, a mhalairt atá fíor. Socraíonn ANFA teorainn donn uasmhéid NFA is féidir le NCB a shealbhú chun a chinntiú nach gcuirfidh athruithe ar a shócmhainní agus ar a dhliteanais airgeadais nach mbaineann le beartas airgeadaíochta isteach ar bheartas airgeadaíochta an Eurochórais.

Mar gheall ar an méadú atá ag teacht ar luach iomlán na nótaí bainc atá i gcúrsaíocht agus ar mhéid na gcúlchistí íosta nach mór do bhainc a choinneáil sa bhanc ceannais, cruthaítear gá le leachtacht a shásaíonn oibríochtaí beartais airgeadaíochta an Eurochórais agus NFA na BCNanna. Tríd an íosmhéid a shocrú d'oibríochtaí beartais airgeadaíochta, cinntear uasteorainn do NFA na BCNanna mar iarmharach.

Cruthaíonn gach sócmhainn ar chlár comhardaithe bainc ceannais airgead nó leachtacht bainc ceannais. Tarraingíonn gach dliteanas ar a chlár comhardaithe leachtacht siar. Trí ghlanluacháil a dhéanamh ar na sócmhainní agus dliteanais uile a bhaineann le beartas neamhairgeadaíochta, tomhaistear an leachtacht fhoriomlán arna soláthar ag oibríochtaí beartais neamhairgeadaíochta bainc ceannais. Chun beartas airgeadaíochta a chur chun feidhme go héifeachtúil, ní mór teorainn a chur leis an méid leachtachta a sholáthraíonn oibríochtaí beartais neamhairgeadaíochta BCNanna. Dá bhrí sin, chun tionchar oibríochtaí na BCNanna ar staid leachtachta oibríochtaí na BCNanna a rialú, tá glansócmhainní airgeadais seachas ollsócmhainní airgeadais teoranta.

Déantar calabrú ar theidlíochtaí NFA gach trí bliana ar a laghad, cé gur féidir calabrúcháin ad hoc a dhéanamh arna iarraidh sin d'aon pháirtí sa chomhaontú. I gcás gach calabrúcháin, socraíonn an Chomhairle Rialaithe na paraiméadair bheartais airgeadaíochta is gá chun cur chun feidhme is éifeachtaí a beartais airgeadaíochta a bhaint amach. Cinneann an Chomhairle Rialaithe leibhéal leachtachta an Eurochórais, socraíonn sí an cóimheas cúltaca íosta agus cinneann sí méid an bheartais airgeadaíochta punanna glan amach. Ina theannta sin, cuireann an Chomhairle Rialaithe forbairtí i méid na nótaí bainc atá i gcúrsaíocht san áireamh. Is iarmhair de na fachtóirí thuasluaite é an t-uasmhéid de NFA an Eurochórais chomhiomlán.

Nuair a shocraítear an uasteorainn chomhiomlán don NFA, déantar é a dháileadh ar aon dul le scair gach BCN i gcaipiteal an BCE, ag cur san áireamh freisin staid tosaigh gach BCN, chun teidlíochtaí NFA na BCNanna don bhliain dár gcionn a chinneadh, agus an teidlíocht NFA seo i bhfeidhm ar feadh suas le trí bliana. Mura bhfuil sé beartaithe ag BCN a theidlíocht a úsáid go hiomlán, cuireann ANFA an rogha ar fáil chun an chuid nár úsáideadh a athdháileadh go sealadach chuig BCNanna eile ar mian leo uasteorainn NFA níos airde a bheith acu. Déanfar an chuid nár úsáideadh a athdháileadh trí mheicníocht lárnach arna shainiú in ANFA. Leis an athdháileadh seo, socraítear uasteorainneacha NFA na BCNanna. Caithfidh NFA na BCNanna fanacht faoi bhun a n-uasteorainneacha ar bhonn meánach bliantúil.

Is féidir le tarscaoiltí tionchar a imirt ar dháileadh uasmhéid an NFA san Eurochóras. Ach ní mhéadaíonn siad an t-uasmhéid sealúchais NFA de BCNanna an Eurochórais.

Sainmhíníonn tarscaoiltí teidlíocht íosta NFA is féidir le gach BCN a shealbhú. I bhfocail eile, tá sé de cheart ag gach BCN scair áirithe den uasmhéid NFA de chuid an Eurochórais a shealbhú, bunaithe ar scair BCN sin i gcaipiteal an BCE, agus is é an méid a fhreagraíonn don tarscaoileadh ná íosteidlíocht an BCN sin (d’fhéadfadh sé seo a bheith níos airde ná an méid arna ríomh de réir a scair i gcaipiteal an BCE). Ar ndóigh, má shealbhaíonn roinnt BCNanna NFA a fhreagraíonn dá dtarscaoiltí a sháraíonn a gcuid scaireanna caipitil, laghdófar an méid NFA a cheadaítear do na BCNanna eile a shealbhú ionas nach sárófar riamh an t-uasmhéid NFA de chuid an Eurochórais.

Tá trí chineál tarscaoilte ann:

- Cinntíonn an tarscaoileadh stairiúil (mar a shonraítear in Iarscríbhinn III de ANFA) nach gá do na BCNanna a NFA a laghdú faoi bhun leibhéal atá nasctha lena suíomh tosaigh stairiúil.

- Cosnaíonn an tarscaoileadh sócmhainn-shonrach sealúchais sócmhainní áirithe (a shainmhínítear in Iarscríbhinn IV de ANFA) nach féidir leis an BCN a dhíol go héasca mar gheall ar shrianta conarthacha nó srianta eile.

- Leis an tarscaoileadh dinimiciúil, coigeartaítear tarscaoileadh stairiúil na BCNanna beag le himeacht ama i gcomhréir le fás nó meath NFA uasta an Eurochórais.

Ní bhaineann ach an ceann is mó de na trí tharscaoileadh leis an BCN faoi seach.

Má tá sé beartaithe ag roinnt BCNanna níos lú ná a dteidlíochtaí a shealbhú, agus más mian le daoine eile níos mó a shealbhú, déantar an chuid nár úsáideadh a athdháileadh le meicníocht lárnach a shainítear in ANFA. Déantar é sin i gcomhthéacs chalabrú tréimhsiúil uasteorainneacha NFA. Is athdháileadh sealadach é athdháileadh an tsaoirse neamhúsáidte, agus déantar é a athríomh le linn an chalabraithe ina dhiaidh sin. Níl aon tionchar ag an athdháileadh ar mhéid comhiomlán an NFA uasta atá i seilbh BCNanna uile an limistéir euro, a chinntear le cinntí na Comhairle Rialaithe maidir le beartas airgeadaíochta.

Braitheann sé sin ar roghanna institiúideacha. Tá srianta dlíthiúla sonracha ag roinnt dlínsí ar na hinfheistíochtaí beartais neamhairgeadaíochta a dhéanann BCNanna; tá forálacha dlíthiúla ag roinnt eile lena n-iarrtar ar BCNanna leasanna a scairshealbhóirí a chur san áireamh a luaithe a chomhlíonfar a gcúraimí beartais airgeadaíochta. Ina theannta sin, tá taiscí móra cliant agus/nó rialtais ag roinnt BCNanna ar thaobh an dliteanais, a imríonn tionchar ar a sealúchais punainne beartais neamh-airgeadaíochta.

Tá cúis stairiúil ann freisin: sular tugadh an euro isteach i 1999, bhí cúlchistí eachtracha sách mór ag roinnt banc ceannais Eorpach chun a rátaí malairte a bhainistiú, go háirithe i leith Deutsche Mark. Ba chás é sin a bhí inchomparáide leis an uair a chuaigh Ballstáit an Aontais isteach sa limistéar euro tar éis 1999, áit a raibh cúlchistí eachtracha measartha mór ag na BCNanna freisin chun a ráta malairte i leith an euro a bhainistiú sula ndeachaigh siad isteach sa Eurochóras. Mínítear i suíomhanna tosaigh éagsúla na BCNanna na difríochtaí suntasacha idir comhdhéanamh an chláir chomhardaithe, a mhair, i gcásanna áirithe, ar feadh roinnt blianta tar éis dá dtír dul isteach sa limistéar euro.

Dá sáródh BCN a uasteorainn do NFA go comhsheasmhach, d'fhéadfadh sé sin difear a dhéanamh do chur chun feidhme an bheartais airgeadaíochta. Ar an gcúis sin, déanann BCE faireachán ar cibé an gcloíonn na BCNanna le ANFA ar bhonn bliantúil. Más gá, mar atá sonraithe in Airteagal 14.4 de Reacht CEBC agus BCE, féadfaidh an Chomhairle Rialaithe na hoibríochtaí arna ndéanamh ag na BCNanna lasmuigh den bheartas airgeadaíochta a thoirmeasc, a shrianadh nó a theorannú má chuireann siad isteach ar chuspóirí agus ar chúraimí CEBC, lena n-áirítear beartas airgeadaíochta an Eurochórais. Go dtí seo, ní raibh aon imeacht gan údar ó uasteorainneacha an NFA.

Tá bonn cirt le diall más rud é, mar shampla, gurb é is cúis leis ná gealltanais idirnáisiúnta don CAI nó soláthar cúnaimh leachtachta éigeandála (ELA) de chuid BCN dá chóras baincéireachta (mar is cuid den NFA é ELA, mar atá sainmhínithe in ANFA). Má tharlaíonn sé seo, caithfidh an BCN a NFA a laghdú a luaithe is féidir chun cloí le ANFA arís. Tá bliain amháin aige chun é sin a dhéanamh más rud é gur tarraingtí ón CAI is cúis leis an sárú.

Ní fadhb í má fhanann NFA faoi bhun an uasleibhéil ríofa. Bhí sé seo amhlaidh go ginearálta, ach d'éirigh sé níos suntasaí ó 2014 i leith. Ciallaíonn sé seo go bhfuil na riachtanais leachtachta ar fud an limistéir euro a ghintear le nótaí bainc i gcúrsaíocht níos airde ná an éifeacht soláthair leachtachta a ghineann NFA Eurochórais. Ina ionad sin, clúdaítear na riachtanais leachtachta trí úsáid a bhaint as uirlisí beartais airgeadaíochta, oibríochtaí rialta athmhaoinithe an Eurochórais, ceannacháin iomlána an bheartais airgeadaíochta nó oibríochtaí droim ar ais struchtúracha.

Níor tharla sé seo riamh agus ní dócha go dtarlóidh sé. Is comhaontú d’aon toil é ANFA idir na BCNanna agus an BCE; agus tá gealltanas tugtha ag gach páirtí cloí leis. Ina theannta sin, laghdaítear arís an riosca go bhfuil méid foriomlán NFA ró-mhór trí úsáid a bhaint as toimhdí coimeádacha agus uasteorainneacha NFA á gcinneadh. Ciallaíonn sé seo, fiú dá mbeadh NFA níos mó ná an t-uasmhéid agus, dá bhrí sin, go raibh oibríochtaí beartais airgeadaíochta níos lú ná mar a samhlaíodh ar dtús, is dócha go mbeadh an staid leachtachta struchtúrach inmhianaithe fós ann. Mar sin d’fhéadfadh oibríochtaí beartais airgeadaíochta a bheith níos lú ná mar a bheadh inmhianaithe chun beartas airgeadaíochta a chur chun feidhme go héifeachtach i gcás den sórt sin, ach ní bheadh géarchéim sa ghearrthéarma agus dhéanfadh BCE beart ceartaitheach. Más gá gníomhaíocht leasúcháin, tá uirlisí éagsúla ar fáil don Chomhairle Rialaithe chun a áirithiú gur leor méid na n-oibríochtaí beartais airgeadaíochta. Mar shampla, maidir le méid na n-oibríochtaí athmhaoinithe, féadfaidh an Chomhairle Rialaithe oibríochtaí ionsúite leachtachta a úsáid nó na híoscheanglais chúlchiste a mhéadú.

Tá calabrú tréimhsiúil ANFA bunaithe ar thoimhdí coimeádacha. Mar sin tá maoláin leordhóthanacha sna huasteorainneacha NFA chun déileáil le forbairtí gan choinne. Mar shampla, agus na huasteorainneacha á gcalabrú, glactar leis go bhfanfaidh nótaí bainc atá i gcúrsaíocht ag an meánleibhéal a breathnaíodh le linn an tríú ráithe den bhliain reatha.

Glacadh le ANFA ionas nach gcuirfeadh an NFA isteach ar bheartas airgeadaíochta. Dá sáródh méid an NFA an t-uasmhéid foriomlán, áfach, d’fhéadfadh go n-éireodh oibríochtaí beartais airgeadaíochta ró-bheag le cur i bhfeidhm éifeachtach an bheartais airgeadaíochta a cheadú.

Chomh maith leis an méid NFA, tá tábhacht lena gcomhdhéanamh freisin. Mar shampla, má dhéanann idirbhearta aonair beartais airgeadaíochta agus idirbhearta beartais neamhairgeadaíochta fritháireamh ar a chéile (e.g. ceannach urrús é ceann amháin agus díol urrús céanna é ceann eile), féadann sé seo comharthaí contrártha a sheoladh maidir le hintinn bheartais airgeadaíochta an Eurochórais nó laghdú a dhéanamh ar éifeachtacht an bheartais airgeadaíochta. Sampla eile is ea idirbhearta bainc cheannais in airgeadraí eachtracha, ar féidir leo dul i bhfeidhm ar rátaí malairte nó a mhíthuiscint mar idirghabhálacha ráta malairte. Chun a áirithiú nach gcuirfidh na himeachtaí sin isteach ar bheartas airgeadaíochta, tá bearta glactha ag an BCE a chomhlánaíonn ANFA, lena n-áirítear Treoirlíne an BCE ar oibríochtaí bainistithe sócmhainní agus dliteanais intíre ag na bainc cheannais náisiúnta (BCE/2019/7), agus cinneadh BCE maidir le clár ceannaigh sócmhainní na hearnála poiblí ar mhargaí tánaisteacha (BCE/2015/10). Cé go rialaíonn an chéad cheann, mar shampla, glanéifeachtaí leachtachta oibríochtaí na BCNanna, cuireann an dara ceann teorainn, i measc rudaí eile, le méid an urrúis shonraigh atá incháilithe do chlár ceannaigh na hearnála poiblí a choinnítear i bpunanna uile bhainc cheannais an Eurochórais.

Mar a mhínítear thuas, socraíonn ANFA uasmhéid do NFA na BCNanna. Ag an am céanna, cuireann sé seo teorainn leis an éifeacht leachtachta ó idirbhearta beartais neamhairgeadaíochta a dhéanann na BCNanna. Ar an dara dul síos, ina n-idirbhearta neamhairgeadaíochta beartais, gníomhaíonn na BCNanna agus an BCE mar infheisteoirí institiúideacha. Nuair a cheannaíonn BCNanna do phunanna beartais neamhairgeadaíochta, leanann siad critéir chomhchosúla le hinfheisteoirí institiúideacha eile agus breithníonn siad a gcinntí ar leithligh ón mbeartas airgeadaíochta. Caithfidh siad na rialacha a leagtar amach in ANFA agus treoirlínte eile lena mbaineann a leanúint. Cuirtear an BCE ar an eolas go rialta faoi (1) idirbhearta beartais neamhairgeadaíochta na BCNanna, agus ní mór cead a fháil roimh ré ón BCE do chuid acu; (2) a sócmhainní agus a ndliteanais; agus (3) a NFA ionchasach agus iarbhír. Féadfaidh BCE beart ceartaitheach a dhéanamh má chuireann na hidirbhearta neamhairgeadaíochta tuairiscithe isteach ar sheasamh an bheartais airgeadaíochta. Ar deireadh, is féidir leis an gComhairle Rialaithe bearta sonracha a ghlacadh atá ina gceangal ar na BCNanna.

Poiblítear sócmhainní agus dliteanais bheartais neamhairgeadaíochta na BCNanna i gcomhréir le rialacha náisiúnta agus Eorpacha. De réir na rialacha seo, cinneann na BCNanna cibé an bhfoilseoidh siad faisnéis ar a sócmhainní agus a ndliteanais beartais neamhairgeadaíochta, lena n-áirítear comhdhéanamh a bpunanna beartais neamhairgeadaíochta. Nochtann formhór na BCNanna sonraí breise ina dtuarascálacha bliantúla nó i bhfoilseacháin eile agus ar a suímh ghréasáin, áit a léiríonn siad, mar shampla, miondealú ar a sócmhainní i bhfiachas rialtais agus neamh-rialtais. Díreach cosúil le hinfheisteoirí eile, ní nochtann BCNanna faisnéis a d’fhéadfadh ligean do dhaoine eile tátail a dhéanamh faoina n-iompraíocht infheistíochta sa todhchaí.

Níl aon sainordú ag an Eurochóras comhdhéanamh sócmhainní agus dliteanais bheartais neamhairgeadaíochta na BCNanna a nochtadh.

Tá an BCE freagrach as faireachán a dhéanamh go n-urramaíonn bainc cheannais CEBC an toirmeasc ar mhaoiniú airgeadaíochta, mar atá sonraithe sa Chonradh ar Fheidhmiú an Aontais Eorpaigh agus i Reacht an Chórais Eorpaigh Banc Ceannais agus BCE freisin. Ní thugann ANFA aghaidh air seo, nach mbaineann ach leis an staid leachtachta struchtúrach atá ag teastáil chun beartas airgeadaíochta a chur chun feidhme agus, mar sin, a shainíonn méid an NFA. Ní thugann ANFA aghaidh ar chomhdhéanamh sócmhainní agus dliteanas beartais neamhairgeadaíochta ná ar an mbealach ina bhfaightear iad.

Chun faireachán a dhéanamh ar chomhlíonadh an toirmisc ar mhaoiniú airgeadaíochta, ceanglaítear ar BCNanna an ESCB an Banc Ceannais Eorpach a chur ar an eolas faoina sócmhainní agus déanann an Banc Ceannais Eorpach faireachán nach ndéanann na BCNanna maoiniú ar rialtais trína bhfiachas a cheannach ar an mbunmhargadh. Déanann an Banc Ceannais Eorpach monatóireacht freisin ar cheannacháin ar an margadh tánaisteach. Foilsítear torthaí na seiceálacha agus na measúnuithe sin i dTuarascáil Bhliantúil BCE.

Níl sé seo clúdaithe ag ANFA ach faoi Airteagail 123 agus 124 den Chonradh ar Fheidhmiú an Aontais Eorpaigh (i.e. de réir an chineáil dlí Eorpaigh is airde rangú). Chinn Comhairle Rialaithe BCE rialacha maidir le hoibríochtaí infheistíochta uile an BCN chun a chinntiú nach sáraíonn siad an toirmeasc ar mhaoiniú airgeadaíochta. Tá cosc ar fhiacha rialtais a cheannach ar an mbunmhargadh agus ní mór do na BCNanna a n-idirbhearta a thuairisciú ar an margadh tánaisteach. Déanann BCE faireachán ar chomhlíonadh an toirmisc ar mhaoiniú airgeadaíochta agus tuairiscíonn sé ar thorthaí a fhaireacháin ina Thuarascáil Bhliantúil.