- 20 FEBRUARY 2024 RESEARCH BULLETIN NO. 116

The unequal impact of the 2021-22 inflation surge on euro area households

The 2021-22 surprise inflation surge had a major impact on households in the euro area. It reduced the real incomes and net wealth of most households as there was no immediate increase in nominal wages and pensions, nominal house prices and the nominal value of bonds, deposits, cash and debt following the rise in the price level. This influenced households’ present and future consumption and therefore their welfare. Although poorer households suffered most from the reduction in the purchasing power of their income, overall welfare losses were especially large for retirees because of the fall in the real value of their relatively large holdings of nominal assets. Conversely, younger and heavily indebted households benefited from the reduction in the real value of their liabilities. In this sense, this inflation episode mimicked an age-dependent tax. Indeed, not everyone was a net loser: while about 70% of households suffered a loss, the rest enjoyed moderate gains.

Evaluating the effects of inflation on welfare

After three decades of low and stable inflation in advanced economies, prices rose sharply after the coronavirus (COVID-19) pandemic. In the euro area, inflation reached a peak of 10.6% in October 2022. The increase was marked and unexpected, and energy and food prices were its main drivers. The question is, did all households bear the costs of this surge in the price level equally, or was the burden shared unevenly?

In Pallotti et al. (2023), we estimate the different effects across households of the 2021-22 surprise inflation episode. We first describe a simple framework which illustrates all the various mechanisms through which this inflation episode affected household welfare, both on impact and over time (for related frameworks, see Fagereng et al., 2022; and Del Canto et al., 2023). We specifically take into account the fact that this episode featured both an increase in the price level and a change in relative prices, which meant that the effects differed across individual households because they purchase different consumption baskets. We then quantify the role of four different factors – nominal assets and liabilities; wages and pensions; capital gains; and consumption baskets – as well as the impact of ad hoc fiscal policies. To that end, we use several micro datasets – including the Household Finance and Consumption Survey and the Household Budget Survey – as well as aggregate time series.[2]

Throughout our analysis, we assume for simplicity that the inflation shock is transitory: after 2022 real wages and the prices of real assets return to their previous levels, and all relative goods prices go back to their pre-shock values. The welfare loss owing to the slow adjustment of nominal wages and nominal house prices is therefore transitory, and so too is the welfare loss for prospective house sellers (and the welfare gain for buyers), owing to the slow upward adjustment of nominal real estate prices.[3] By contrast, the welfare loss (gain) on all nominally denominated assets (liabilities) is permanent.

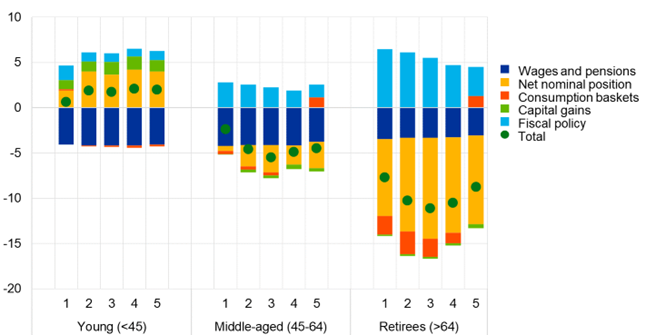

Figure 1

Welfare costs of the inflation surge across euro area households, by age groups and income quintiles (percentages of 2021-22 income)

Source: Authors’ calculations based on data from the Household Budget Survey and the Household Finance and Consumption Survey.

Notes: The x-axis shows quintiles of permanent income for each age group, which we proxy using household consumption, with 1 being the 20% of households with the lowest level of permanent income, and 5 being the 20% of household with the highest level of permanent income. The “wages and pensions” component comprises effects via wages of workers and pensions of retirees; “net nominal positions” comprises effects from total nominal assets net of nominal liabilities; “consumption baskets” denotes effects arising from differences across households in the goods they consume; “capital gains” is the effects from changes in the real value of real assets (housing and stocks); and the “fiscal policy” component comprises effects arising from fiscal interventions in energy markets and ad hoc direct transfers to households.

The welfare costs of the inflation surge and their distribution

The impact of the inflationary episode was large and it differed across households. In 2021-22 the welfare losses suffered by the median euro area household amounted to roughly 4% of disposable income – more than in a typical recession.

Across households, the largest losses were experienced by retirees because they tend to hold larger amounts of nominal assets (such as cash and deposits) and the real value of these assets is sensitive to price increases (Figure 1; see also the classic work by Doepke and Schneider, 2006). In contrast, households with long-term debt (such as mortgages) benefited from the higher price level because of the reduction in the real value of their liabilities. This “net nominal position” channel particularly hurt middle-income retirees, who suffered welfare losses equivalent to 11% of their 2021-22 income. In comparison, retirees with low incomes, who hold less wealth, and retirees with high incomes, who own more real assets such as housing, had smaller welfare losses.[4]

The slow adjustment of nominal wages and pensions was a key driver of welfare losses across all age groups. As nominal wages and pensions did not immediately adjust to higher inflation, labour market income lost purchasing power. In 2021-22 nominal wages grew by less than 3% on average for most countries, age groups and consumption groups, which is much less than the respective average inflation rates over the period. Pensions grew only slightly more than wages. This channel generated welfare losses amounting to 4% of 2021-22 income for the median household.

The varied inflation rates experienced across households owing to differences in their consumption baskets produced smaller effects. On the one hand, poorer households suffered larger losses than richer households because a larger share of their budget is spent on food and energy, which recorded sharp price rises (Bobasu et al., 2023). At the same time, these changes in relative prices were partly compensated by the decline in the real value of property rents. As a result, this consumption basket channel had a more muted impact than the devaluation of all nominal wealth and the drop in real labour market income. Changes in the real value of housing and stocks (the “capital gains” channel in Figure 1) had only a small effect.

The sum of these four channels represents the welfare change that households would have experienced if governments had not intervened. However, during this period several ad hoc policies were introduced in response to the shock (see, for example, Dao et al., 2023). Some of these policies, such as energy price caps, energy subsidies and reductions in taxes on fuels, reduced the actual prices faced by consumers. Others consisted in transfer payments to vulnerable demographic groups (see, for example, Basso et al., 2023 and Freier and Ricci, 2023). Although these measures were deficit-financed, they had limited inflationary effects (Dao et al., 2023). We find that these unconventional fiscal policies were key to cushioning the effects of the shock on households, particularly the most vulnerable, and reduced by 2% of 2021-22 income the welfare losses caused by the inflation surge for the median household. Retirees benefited the most from these policy interventions, principally because they were the largest losers from the inflationary episode, but also because they consume a relatively larger share of energy. Most of the cushioning effect came from policies related to energy prices, while direct transfers to households had less impact.

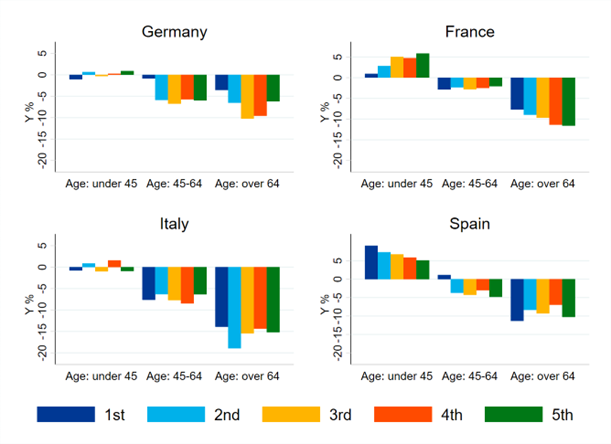

Figure 2

Welfare costs of the inflation surge across households in the four largest euro area countries, by age groups and income quintiles (percentages of 2021-22 income)

Source: Authors’ calculations based on data from the Household Budget Survey and the Household Finance and Consumption Survey.

Notes: The x-axis shows quintiles of permanent income for each age group, which we proxy using household consumption, with 1st being the 20% of households with the lowest level of permanent income, and 5th being the 20% of household with the highest level of permanent income.

We also find substantial differences in welfare costs across the larger euro area countries. The welfare losses for the median household ranged from 3% of disposable income in France and Spain, to 8% in Italy (Figure 2). Cross-country differences were mostly caused by the differences in national inflation rates and by differences in the distribution of net nominal wealth, together with the different fiscal policies. Younger indebted households experienced net gains because the real value of their debt dropped. This effect was stronger in France and Spain, where many young households have mortgages. However, not all young households benefited: on average, those who were not homeowners with a mortgage also suffered welfare losses.

Conclusions

Analysing the 2021-22 inflation surge in the euro area, we find large average welfare losses, especially compared with commonly estimated costs of a typical recession, and substantial differences across countries. Within countries, we find differences across age groups, but not across income groups. While this wide variation posed a challenge for monetary policy, we find that unconventional fiscal policy measures helped to substantially compress these inflation differentials across households. Therefore, this historical episode highlights the importance of fiscal policy in responding to country-specific dynamics within a monetary union, where monetary policy cannot be tailored to individual countries.

Although the heaviest burden fell on retirees, this group had previously benefited from a relatively long period of low inflation (in 2013-21) and many of them still held residual “excess savings” built up during the pandemic, which might have been used to limit the drop in their consumption. Additionally, euro area countries, like most advanced economies, have large amounts of public debt for which the repayment burden falls on future generations. In this sense, the “inflation tax” is transferred from retirees to the young, partially offsetting this looming fiscal adjustment.

References

Ampudia, M., Ehrmann, M. and Strasser, G. (2023), “The effect of monetary policy on inflation heterogeneity along the income distribution”, Working Paper Series, No 2858, ECB, October.

Basso, H. S., Flevotomou, M., Freier, M., Pidkuyko, M., Amores, A. F., Bischl, S., De Agostini, P., De Poli, S., Dicarlo, E., Maier, S., García-Miralles, E., Ricci, M. and Riscado, S. (2023), “Inflation, fiscal policy and inequality”, Occasional Paper Series, No 330, ECB, October.

Bobasu, A., di Nino, V. and Osbat, C. (2023), “The impact of the recent inflation surge across households”, Economic Bulletin, Issue 3, ECB.

Dao, M. C., Dizioli, A., Jackson, C., Gourinchas, P.-O., and Leigh, D. (2023), “Unconventional fiscal policy in times of high inflation”, paper delivered at the ECB Forum on Central Banking.

Del Canto, F. N., Grigsby, J. R., Qian, E. and Walsh, C. (2023), “Are Inflationary Shocks Regressive? A Feasible Set Approach”, NBER Working Papers, No 31124, National Bureau of Economic Research.

Doepke, M. and Schneider, M. (2006), “Inflation and the Redistribution of Nominal Wealth”, Journal of Political Economy, 114(6), pp. 1069-1097.

Fagereng, A., Gomez, M., Gouin-Bonenfant, E., Holm, M., Moll, B. and Natvik, G. (2022), “Asset-Price Redistribution”, working paper, London School of Economics.

Freier, M. and Ricci, M. (2023), “Fiscal policy to the rescue: How governments shielded households from inflation”, ECB blog, 23 November.

Pallotti, F., Paz-Pardo, G., Slacalek, J., Tristani, O. and Violante, G.L. (2023), “Who bears the costs of inflation? Euro area households and the 2021–2022 Shock, Working Paper Series, No 2877, ECB, November.

This article was written by Filippo Pallotti (University College London), Gonzalo Paz Pardo, Jiri Slacalek, Oreste Tristani (all Directorate General Research, European Central Bank) and Giovanni L. Violante (Princeton University). The authors gratefully acknowledge the comments of Ana Maria Borlescu, Alexandra Buist, Michael Ehrmann and Alexander Popov. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.

Specifically, we estimate household-level expenditure shares allocated to different goods and services from the 2015 wave of the Household Budget Survey. The corresponding price changes are available from the disaggregated data underlying the Harmonised Index of Consumer Prices (HICP) for each euro area country. For information on ad hoc government support, we use the dataset on national fiscal policy responses to the energy crisis from the Bruegel think tank. We obtain information on household wealth and income from the Household Finance and Consumption Survey. Counterfactual prices, estimated as if no government interventions had been implemented, are based on the IMF methodology (from Dao et al., 2023). Finally, we estimate the response of wages, house prices, stock prices and bond prices over 2021-22 using a combination of event studies and high-frequency identification on days of HICP inflation announcements.

Given that real wages did not fully recover during 2023, our estimates of the welfare loss implied by the loss of purchasing power of labour market income during 2021-22 are a lower bound to the total losses over a longer time horizon.

A related paper by Ampudia et al. (2023) analyses the heterogeneous effects of monetary policy on households along the income distribution.