- SPEECH

The future of the EU fiscal governance framework: a macroeconomic perspective

Panel intervention by Philip R. Lane, Member of the Executive Board of the ECB, at the European Commission webinar on “The future of the EU fiscal governance framework”

12 November 2021

I welcome the opportunity to contribute to the discussion on the future of the EU fiscal governance framework. In what follows, I will offer some personal observations.[1]

I will focus on the macroeconomic role of the Stability and Growth Pact (SGP), taking a euro area perspective. The SGP is of course just one component in the overall institutional architecture of the EU. In particular, the completion of the banking union and capital markets union would improve the euro area’s capacity to absorb macro-financial shocks, which would also serve to reduce fiscal tail risks.[2] A comprehensive and robust macroprudential policy framework can also significantly reduce the burden on national fiscal policies and monetary policy in terms of macro-financial stabilisation.[3] In addition, a permanent central fiscal capacity would enhance macroeconomic stabilisation by facilitating a common area-wide response to common shocks and (depending on its design) would also be complement national fiscal policies in managing large-scale country-specific shocks. Launched as a specific response to the pandemic crisis, the Next Generation EU (NGEU) initiative is testimony to the effectiveness of (at the least) a state-contingent type of central fiscal capacity in the face of large adverse shocks.

At a conceptual level, it is clear that both price stability and macroeconomic stability simultaneously require that fiscal positions are sustainable and that fiscal policy operates in a countercyclical manner. Over the past twenty years, the macroeconomic performance of the euro area has suffered both from episodes of fiscal sustainability problems in some member countries and from fiscal procyclicality (in both good and bad economic times). Of course, fiscal sustainability and fiscal countercyclicality are interconnected: it is not possible to respond counter-cyclically to a recessionary shock if debt sustainability is called into question. In turn, debt sustainability requires the commitment to act counter-cyclically also during periods of strong economic performance by reducing debt ratios and building up fiscal buffers. The procyclical nature of fiscal policy in the euro area during substantial phases of the first two decades of the euro (pre-pandemic) is clearly evident in Chart 1.[4]

Chart 1

Euro area aggregate fiscal stance, output gap, inflation and current account balance

(percentages of GDP)

Sources: AMECO and ECB staff calculations.

Notes: The fiscal stance is measured as the change in the cyclically adjusted primary balance. The solid vertical line refers to the beginning of the forecast period.

An efficient SGP framework can make an important contribution to the macroeconomic performance of the euro area. In particular, the counterfactual of a full decentralisation of fiscal policymaking is not desirable from a euro area wide perspective. In particular, national policy makers are unlikely to internalise the implications of their decisions for the aggregate euro area fiscal stance and to fully take into account the spillover effects of their domestic policy on the other member countries in a monetary union. In particular, adverse spillover effects arise if any member country has an unsustainable fiscal position, operates a pro-cyclical fiscal policy or reduces potential output through structural policies that are anti-growth. Moreover, continuous assessment of the appropriateness of national fiscal policies also facilitates the effective operation of the European Stability Mechanism (ESM), especially in scenarios in which fiscal stress might arise quite suddenly due to large-scale macro-financial shocks. In an environment in which central banks must turn to asset purchase programmes in order to ensure an appropriate monetary policy stance in the neighbourhood of the effective lower bound, such programmes can operate more smoothly if there is an effective and transparent fiscal framework to simultaneously underpin fiscal sustainability in each Member States and an appropriate euro area fiscal stance.

The desirability of an efficient SGP has been reinforced by the pandemic: public debt in the euro area has increased by some 14 percentage points of GDP since 2019, reaching about 100 per cent of euro area GDP in 2020 (Chart 2). This aggregate number masks significant cross-country heterogeneity, with debt ratios ranging from around 18 per cent of GDP to more than 200 percent of GDP (Chart 3). Along one dimension, the legacy of higher public debt ratios implies an inherent increase in vulnerability and a greater scope for adverse spillovers across member countries; along another dimension, a full recovery from the pandemic also requires fiscal policy to be sufficiently countercyclical. In view of the fundamental role of growth dynamics in determining fiscal sustainability the increase in public debt ratios has also reinforced the importance of growth-enhancing reform policies and a growth-friendly composition of fiscal policy.

Chart 2

Euro area debt-to-GDP ratio

(percentages of GDP)

Source: AMECO.

Note: The solid vertical line refers to the beginning of the forecast period.

Chart 3

Debt-to-GDP ratios of euro area Member States

(percentages of GDP)

Sources: AMECO and ECB staff calculations.

Note: The solid vertical line refers to the beginning of the forecast period.

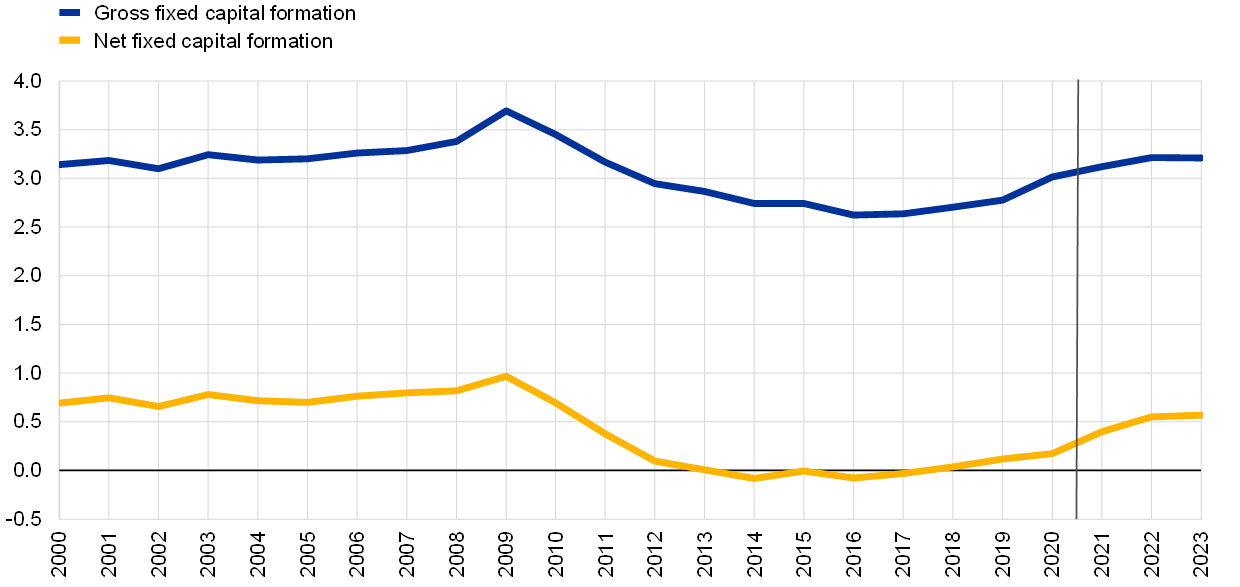

The pandemic has compounded an already-difficult fiscal agenda. All member countries must grapple with the macroeconomic and public finance implications of ageing societies. In addition, an efficient SGP also has to take into account that Europe cannot ignore or delay the necessity of the green transition and digital transformation. These imply considerable public investment efforts even beyond the horizon of the Recovery and Resilience Facility (RRF). The shortfall in the public capital stock has also been compounded by the low level of public investment over the last decade (Chart 4).

Chart 4

Euro area gross and net fixed capital formation

(percentages of GDP)

Sources: AMECO and ECB staff calculations.

Note: The solid vertical line refers to the beginning of the forecast period.

In relation to macroeconomic stabilisation, counter-cyclical fiscal policy is particularly important as a counter-cyclical stabilisation instrument if monetary policy is constrained by the effective lower bound on nominal interest rates. Chart 5 shows the pronounced trend decline in the equilibrium real interest rate (r*) over the last twenty years. While a lower value of r* improves fiscal sustainability, thereby creating fiscal space, a low value of r* also implies that the effective lower bound will more frequently constrain the ability of monetary policy to respond to adverse shocks.[5] In one direction, a procyclical tightening of fiscal policy during a downturn would not be fully offset by an easing of monetary policy if the effective lower bound is binding. In the other direction, the return to the two percent inflation target will be slower and will require a more persistent phase of monetary accommodation if fiscal policy is not countercyclically deployed in response to an adverse shock.

Chart 5

Estimates of the euro area natural rate of interest

(percentages)

Sources: Brand, C., Bielecki, M. and Penalver, A. (eds.) (2018), “The natural rate of interest: estimates, drivers, and challenges to monetary policy”, Occasional Paper Series, No 217, ECB, December.

Notes: Ranges span point estimates across models to reflect model uncertainty and no other source of r* uncertainty. The dark shaded area highlights smoother r* estimates that are statistically less affected by cyclical movements in the real rate of interest. The latest observation is for the third quarter of 2019.

Countercyclical fiscal policy requires determined action during large recessions, but it also requires buffers to be rebuilt once the economy is firmly back on track, so as to ensure debt sustainability and enable fiscal policy to also respond to subsequent adverse shocks. Moreover, it should be appreciated that while fiscal expansion during a recession should have a significant multiplier effect (especially if the effective lower bound is a constraint), the multiplier impact of a fiscal expansion during a phase of strong economic performance is likely to be much more muted, with crowding-out effects amplified by the likely need to tighten monetary policy if pro-cyclical fiscal expansion posed a threat to the two percent inflation target.

In relation to fiscal sustainability, lower average interest rates have significantly reduced debt servicing costs, from almost 4 per cent of GDP at the start of Economic and Monetary Union to around 1.5 per cent of GDP in 2020 (Chart 6 and Chart 7). While lower debt servicing costs surely create additional fiscal space to a significant degree, a full treatment of the implications for optimal fiscal policy should take into account the causal determinants of low equilibrium real interest rates. In particular, the contributions of lower trend productivity growth and demographic trends to the decline in interest rates have different fiscal implications than other sources of low rates.

Chart 6

Ten-year euro area bond yields: GDP-weighted and selected countries

(percentages)

Sources: Bloomberg, Reuters and ECB staff calculations.

Chart 7

Euro area interest payments on government debt

(percentages of GDP)

Source: AMECO.

Note: The solid vertical line refers to the beginning of the forecast period.

A reform of the Stability and Growth Pact should tackle its main weaknesses in order to support the attainment of the twin objectives of macroeconomic stabilisation and fiscal sustainability.

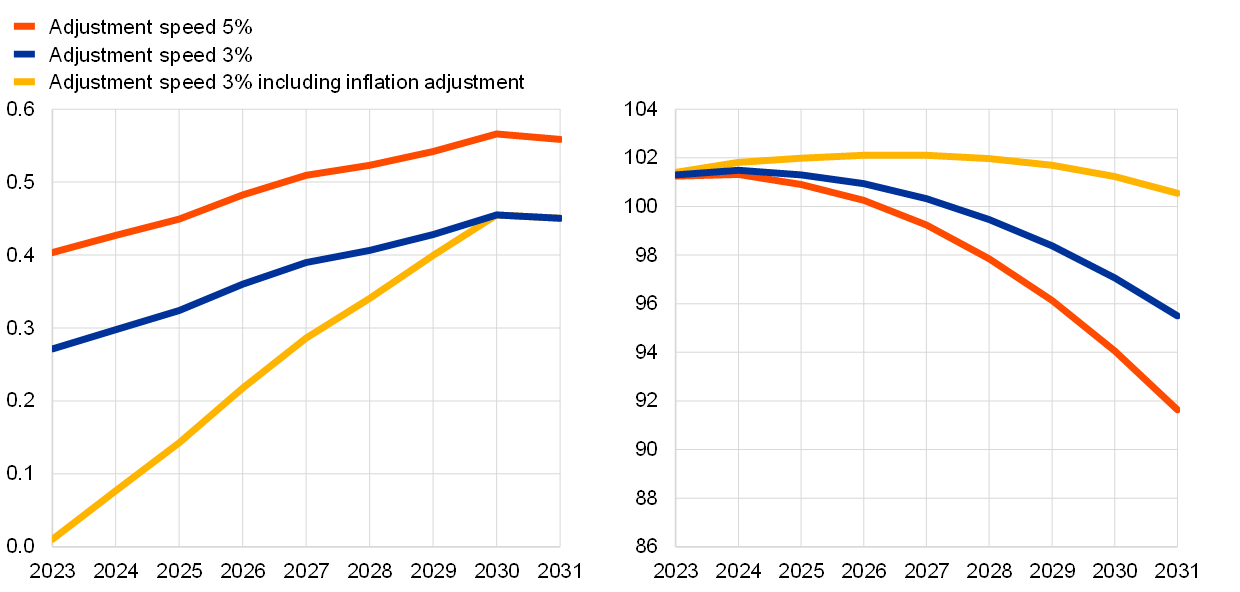

As proposed by the European Fiscal Board and other contributors, a simplified two-tier framework that consists of an expenditure rule linked to a debt anchor would both reduce the complexity of the fiscal rules and better align fiscal stabilisation with fiscal sustainability challenges. In terms of the debt anchor, simulation exercises indicate a sustainable adjustment path could take a more gradual path than the current 1/20th rule. Stylised simulations by ECB staff of the two-tier framework for the euro area suggest that a more gradual and sustainable adjustment of government debt would be possible through: (i) a reduction of the debt adjustment speed to 3 per cent per annum, from the current rule of 5 percent per annum, in relation to the gap to the 60 per cent debt reference level; and (ii) a longer averaging horizon of ten years, rather than three years under the current debt rule. Concretely, adjustment requirements could be calibrated to ensure compliance with the debt adjustment path over a ten-year forward-looking horizon.

In addition, accounting for the ECB’s symmetric two per cent inflation target in the expenditure rule would improve the counter-cyclicality of the framework by automatically increasing fiscal space in times of inflation below the target, and vice versa. In relation to the fiscal stance, this amounts to an intertemporal shift in the timing of fiscal adjustment: fiscal policy would be looser when inflation is running below the two percent target but tighter when inflation is running above target. By providing extra fiscal accommodation when inflation is running below target, this would also enable monetary policy to operate more effectively, especially in the shadow of the effective lower bound. More sophisticated variants could also be considered (albeit at the price of extra complexity) that duly differentiates between demand-driven and supply-driven inflation shocks. Chart 8 illustrates the fiscal dynamics under these alternative options.

Chart 8

Euro area fiscal adjustment (left side) and euro area government debt (right side)

(left side: percentage points of GDP, right side: percentages of GDP)

Source: ECB staff calculations.

Notes: Red scenario: annual adjustment of 5% of the distance of the debt ratio to 60% of GDP on average over 2023-31; blue scenario: 3% average annual adjustment over 2023-31; yellow scenario: 3% average annual adjustment over 2023-31; expenditure rule adjusted for country-specific inflation gap vis-à-vis 2% (as measured by GDP deflator), the expenditure growth allowed under the rule increases by the extent of the gap.

The two-tier framework would also improve transparency by being less reliant on unobservable indicators. While an expenditure rule still requires taking a stand on the underlying trend rate of potential output growth, the slow-moving nature of trend variables means that this is likely to be less volatile than the annual output gap that is employed as a key indicator in differentiating between structural and cyclical fiscal positions. Output gap revisions have been sizeable both on average and year-by-year over the 2007-2019 period (Chart 9).

Chart 9

Euro area output gap revisions

(percentages of potential GDP)

Sources: AMECO and ECB staff calculations.

Note: The solid vertical line refers to the beginning of the forecast period.

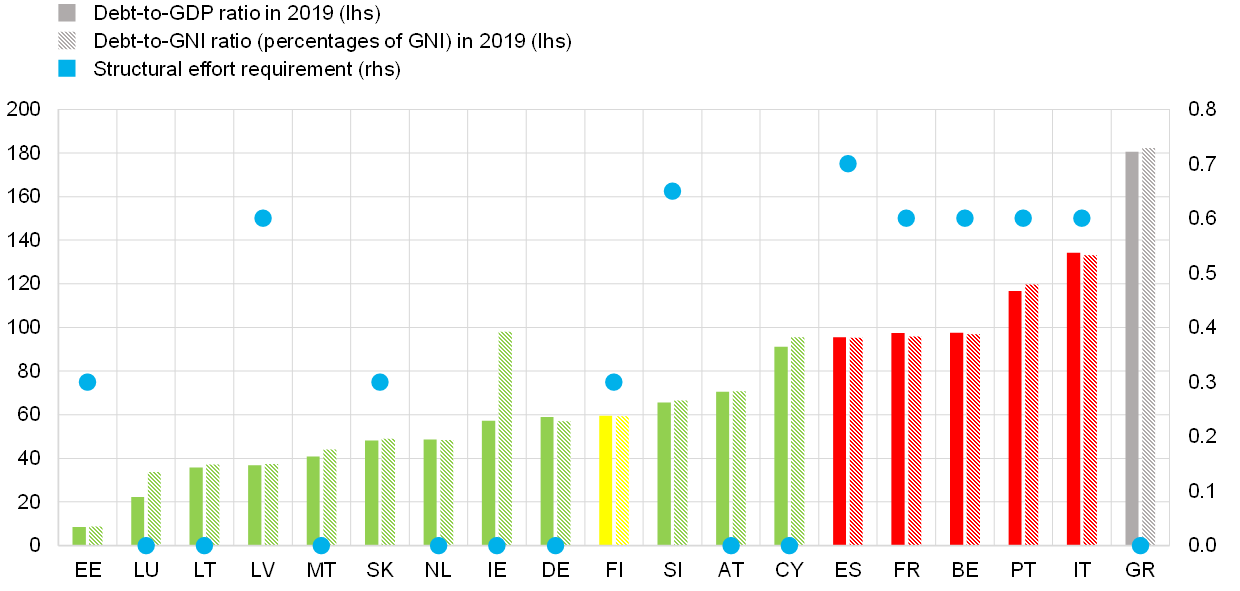

In addition, the two-tier framework would take greater account of differences in the level of outstanding debt in determining the appropriate rate of fiscal adjustment. The limitation of the current framework is well illustrated by the adjustment requirements for 2019 that resulted in Latvia, a country with debt well below the 60 percent of GDP debt reference level of the Treaty, facing the same adjustment requirements as countries with debt ratios at or above 100 percent of GDP (Chart 10).

Chart 10

Debt-to-GDP and debt-to-GNI ratios and structural effort requirements in 2019

(percentages of GDP)

Sources: AMECO, European Commission assessments of 2020 stability programmes and Central Statistics Office. The medium-term risk classification is taken from the European Commission Debt Sustainability Monitor 2019.

Notes: Greece is not covered by the regular European Commission debt sustainability assessment for 2019. For more details, refer to Box 3.3. of the Debt Sustainability Monitor. For Ireland GNI* (modified gross national income) is used as measure of GNI.

Finally, my assessment is that the role of independent fiscal institutions (IFIs) in the overall fiscal framework could be expanded. At a European level, the European Fiscal Board has been a very effective innovation. At a national level, the independent scrutiny of macroeconomic forecasts by national fiscal councils is helping to improve the reliability of budgetary plans and reducing scale of ex-post revisions. National fiscal councils could also contribute by also assessing the plausibility of budgetary plans. This would help to elongate the decision-making horizons of policymakers and a stronger focus on the longer term can be particularly beneficial in identifying unfavourable budgetary trends and stabilising public capital programmes.

- My individual views should not be construed as representing the institutional position of the European Central Bank or the Eurosystem. For a discussion of how the EU institutional framework has boosted the resilience of the euro area over the last decade, see Lane, P.R. (2021), “The Resilience of the Euro”, Journal of Economic Perspectives, Vol. 35, No 2, pp. 3-22..

- The ESM also constitutes a fundamental component of the overall institutional architecture by acting as a source of official lending (with appropriate conditionality) in the event of a member country losing market access. Most importantly, the very existence of the ESM acts as a stabilising force, since investors can rule out some tail risk scenarios in the knowledge that an official backstop is available if required.

- Martin, P. and Philippon, T. (2017), “Inspecting the Mechanism: Leverage and the Great Recession in the Eurozone”, American Economic Review, Vol. 107, No 7, pp. 1904-37.

- In terms of cyclical indicators, I include the current account balance as well as the output gap, in order to serve as a reminder that a complete assessment of economic slack should take into account the balance between domestic demand and net exports as drivers of output.

- The outcome of the ECB strategy review was published on 8 July 2021. See the ECB’s monetary policy strategy statement. and the extensive accompanying note Overview of the ECB monetary policy strategy, which includes a discussion of monetary-fiscal interactions. See also the strategy review workstream on monetary-fiscal policy interactions, “Monetary-fiscal policy interactions in the euro area”, ECB Occasional Paper 273, September 2021.

Banca centrale europea

Direzione Generale Comunicazione

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

La riproduzione è consentita purché venga citata la fonte.

Contatti per i media