- PRESS RELEASE

Results of the June 2024 Survey on credit terms and conditions in euro-denominated securities financing and over-the-counter derivatives markets (SESFOD)

10 July 2024

- Credit terms and conditions eased somewhat over the period from March to May 2024

- The maximum amount of funding, maximum maturity of funding and demand for funding increased across many types of collateral

- Improved liquidity and trading conditions for foreign exchange, interest rate and credit derivatives referencing both sovereigns and corporates

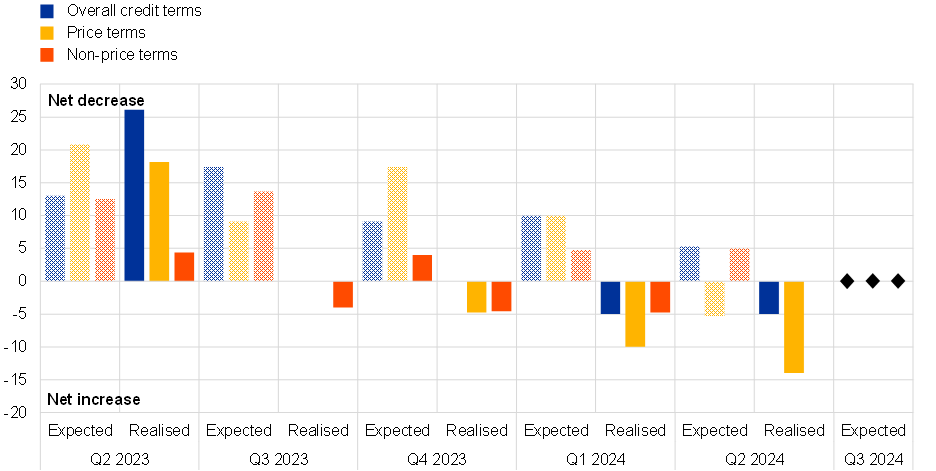

Overall credit terms and conditions eased somewhat between March and May 2024. This outcome was in line with the expectations of a further easing of overall credit terms and conditions that had been expressed in the March 2024 survey. While overall price terms eased more than expected, non-price terms – contrary to expectations – did not tighten and instead remained unchanged. The overall easing of conditions in general, and of price terms in particular, was reflected across all counterparty types. Respondents mainly attributed the easing of price terms to an improvement in general market liquidity, competition from other institutions and improvements in the current or expected financial strength of counterparties. For the first time since the start of the survey in 2013, survey respondents expected overall, price and non-price terms to remain unchanged across all counterparty types for the three months ahead (in this case for the period from June to August 2024).

Chart 1

Realised and expected quarterly changes in overall credit terms and price/non-price terms offered to counterparties across all transaction types

(Q2 2023 to Q3 2024; net percentages of survey respondents)

Source: ECB.

Note: Net percentages are calculated as the difference between the percentage of respondents reporting “tightened somewhat” or “tightened considerably” and the percentage reporting “eased somewhat” or “eased considerably”.

Respondents reported that changes in the practices of central counterparties (CCPs), including margin requirements and haircuts, had not affected price and non-price terms. The amount of resources dedicated to managing concentrated credit exposures increased over the review period, while the use of financial leverage declined somewhat. Respondents reported increases in the intensity of efforts to negotiate more favourable terms, in particular for insurance companies.

Turning to financing conditions for funding secured against the various types of collateral, respondents reported increases in the maximum amount and maximum maturity of funding secured against all collateral types. Respondents reported that haircuts had increased for convertible securities. Financing rates/spreads decreased for domestic and high-quality government bonds but increased for funding secured against all other types of collateral. Small net percentages of participants reported decreased use of CCPs for securities financing transactions involving collateral in the form of domestic and high-quality government bonds. Significant net percentages of respondents reported increases in demand for funding secured against many collateral types, particularly for funding secured against equities and domestic government bonds. Respondents reported mixed results as regards the liquidity and functioning of collateral markets.

Looking at credit terms and conditions for the various types of non-centrally cleared over-the-counter (OTC) derivative, initial margin requirements decreased slightly for commodity derivatives and credit derivatives referencing corporates. Survey respondents reported a mixed picture, with only a few changes as regards the maximum amount of exposure and the maximum maturity of trades. Meanwhile, they reported improved liquidity and trading conditions for foreign exchange, interest rate and credit derivatives referencing both sovereigns and corporates. They also reported that for most derivative types the volume of valuation disputes had decreased, although the duration and persistence of valuation disputes had increased. Terms in new or renegotiated master agreements remained mostly unchanged. Respondents reported no changes as regards the posting of non-standard collateral over the review period.

The results of the June 2024 SESFOD survey, the underlying detailed data series and the SESFOD guidelines are available on the ECB’s website, together with all other SESFOD publications.

The SESFOD survey is conducted four times a year and covers changes in credit terms and conditions over three-month reference periods ending in February, May, August and November. The June 2024 survey collected qualitative information on changes between March and May 2024. The results are based on the responses received from a panel of 25 large banks, comprising 13 euro area banks and 12 banks with head offices outside the euro area.

For media queries, please contact Ettore Fanciulli, tel.: +49 172 2570849.

Banco Central Europeo

Dirección General de Comunicación

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Alemania

- +49 69 1344 7455

- media@ecb.europa.eu

Se permite la reproducción, siempre que se cite la fuente.

Contactos de prensa