European Pension Funds Congress

Speech by Gertrude Tumpel-Gugerell, Member of the Executive Board of the ECBEuro Finance WeekFrankfurt am Main, 18 November 2008

Introduction

Ladies and Gentlemen:

It is with great pleasure that I accepted your invitation to deliver the Keynote address at this year’s European Pension Fund Congress.

The ECB is well aware of the growing social and economic importance played by private pension funds for household wealth accumulation and securing the income of an ageing population. Individually, we are all still only getting older at a rate of 1 day every 24 hours, but what we are now seeing is that collectively our societies are also getting older.

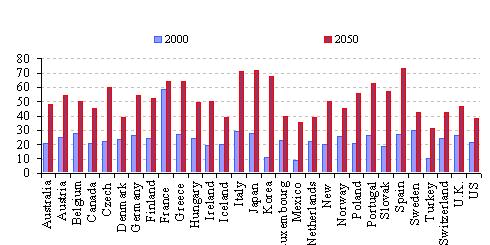

This ageing of the population is well illustrated by the development in the so-called “old age dependency ratio”, which captures the ratio of the population aged 65 and above to persons between 20 and 64 years. According to ECB calculations, by 2050, this ratio will increase to 55% from the current level of around 26% in euro area (see Chart I). Despite some differences across countries, the challenges posed by ageing societies are common to all euro area countries.

Pension funds therefore play a pivotal role in providing income to a substantial part of the population, and thus will be instrumental in shaping the standard of living in the future.

In order to fulfil this role, private pension funds invest over long horizons and need predictable nominal trends. Pension funds thus have a great interest to see the purchasing power of money preserved and the risk of inflation minimised, as there are sufficient uncertainties over these horizon without adding an extra and unnecessary one in the form of high and volatile inflation.

A stable, non-inflationary macro-economic environment is thus essential in providing for an ageing society. In turn, private pension funds thus must have a vital interest that the ECB fulfils its mandate of preserving price stability in the euro area over the medium to longer-term.

At the same time, the ECB takes great interest in the private pension fund industry as, in many segments of financial markets, pension funds have become key institutional investors.

As such pension funds shape the way financial markets work by enhancing the efficiency, the depth and therefore the liquidity of the market. This contribution to improving the overall functioning of the financial system may in turn foster a smoother transmission of monetary policy. In the current environment, with many financial market participants in need to adjust their portfolio, the presence of longer-term oriented investors such as private pension funds on financial markets can play an important stabilising force for the financial system as a whole.

An insight into the importance of funded pensions in the OECD countries is provided by the market size. In 2006, this market was valued at approximately EUR 20 trillion: two thirds of which were invested in pension funds, compared to 18% provided by banks and investment management companies and 14% in life and pension insurance contracts. This large share reflects the dynamic growth of pension funds’ assets in recent years. Indeed, over the period 2004-2006, the latest available data indicates that euro area pension fund assets grew on average with 13.6%, compared with 9.0% for all OECD countries. Notwithstanding the current period of turbulences, this dynamic growth is likely to have continued in many economies.

In my speech today, I will touch on three issues. First, I would like to emphasise the role of private pension funds in an ageing society. Second, I will briefly describe the role of private pension funds in financial markets in general and look more specifically at their role as long-term oriented investors in the current environment.

Thirdly, I will reflect on the impact of institutional investors on the transmission of monetary policy and the ensuing consequences for the conduct of monetary policy.

The role of private pension funds in an ageing society

Let me start with a piece of good news: between now and 2040, we are all expected to live longer as life expectancy increases. For this we all wish to have a financially secure retirement. This, however, requires that we will all have to save more or work longer. Confronted with population aging, governments are finding it increasingly challenging to maintain the entitlements of the existing public pension schemes. Many governments are moving in the direction of reducing benefits relative to contributions to public pension schemes, reducing the ratio of the post-retirement income to the net pre-retirement income. Mandatory private pensions also operate as substitutes for part of the public pension provision, but in some countries, mandatory private pension saving has been added on top of existing public plans.

Thus it is clear that, individuals will be increasingly supporting their old-age consumption via alternative, private pension plans and life insurance policies. In this context, I see a need for public authorities to foster conditions that encourage and are conducive to saving, particularly in countries with a strong ageing of the population.

Over the coming decades, as the “first pillar” of old-age provision will increasingly need to be complemented by a strong “second pillar” of occupational pension funds, a significant increase in the value of assets managed by the retirement savings industry can be expected. This will particularly need to be the case in countries where this industry is less developed and in countries with underfunded public pension systems with defined benefits.

At present the share of total wealth invested by euro area households with insurance corporations and pension funds is much smaller than is the case for US households. This largely reflects the larger weight of real estate in euro area households’ portfolios (both in value and relative to GDP). The strong rise in property prices experienced in recent years by some euro area countries contributed to increase the share of housing wealth in total household wealth.

At the same time, with the normalisation of house price dynamics, the accumulation wealth through institutional investors should come to the fore more strongly in the future. At just under 30%, the share of financial wealth invested with insurance corporations and pension funds is currently very close to the share observed for the US. Furthermore, this share has gradually risen from 24% in early 1999 in part, reflecting a shift in the preference of households with respect to asset holdings from direct holdings of securities to professional asset managers.

Looking across the euro area, the size of the private pension fund industry differs extensively with the spectrum going from the Netherlands with a very large sector of 1.3 times GDP to France and Germany with much smaller ones below a tenth of GDP. Several factors have contributed to this cross-country variation in the design and importance of pension funds: the past demographic structure of the population, the fiscal position of governments and socio-economic trends.

The global pension landscape is also being affect by the shift, in particular by occupational pension plans, toward defined contribution plans, while often defined benefit plans have been closed to new entrants. Traditionally, private pensions have been employer-provided and been of the defined-benefit type, where the entitlement depends on some measure of individual earnings and years of service.

The pension benefit in defined-contribution plan depends on the value of individual and employer contributions, the investment returns that these earn and the terms on which accumulated capital can be converted into a flow of pension benefits.

Potentially, this shift in the type of the private pension schemes may have repercussions on to financial markets and portfolio allocation. Maturing defined benefit plans and newly set up defined contribution schemes may have different propensities to invest in risky assets, and thereby affecting the relative price of the assets.

Looking at available data does indeed suggest many factors impacting on the asset allocation of the different types of pension schemes. At the same time, the shift between types of pension schemes transfers the longevity risk of the individual into a future income risk for the individual. In the defined contribution pension system, a longer life can only be counterbalanced by either saving more, working longer or through unrealistically high rates of return on investments. None of these remedial options are available ex post.

Individuals with retirement income stemming from such pensions schemes therefore run the risk of outliving their resources, leaving only a reduction their standard of living when they are old. Furthermore, as retirement income becomes subject to a greater number of risks, plan beneficiaries will have to provide for these challenges, thus putting them in a less good position to bear risk in their remaining portfolio behaviour and altering their behaviour as investors on financial markets.

In this context it is noteworthy that most people have substantial problems giving a reasonable estimate of how much money at retirement they will have had to accumulate in order to sustain their current standard of living. Few people realize how large the capital stock will need to be and how low the rate of withdrawal has to be, irrespective of the asset allocation chosen. Individuals have a poor appreciation of the financial implications of longevity.

It is the responsibility of public authorities to further promote financial education programmes aimed at enhancing not only the awareness of citizens on the financial risks they face in their decisions but also the ability to judge the options at their disposal.

For instance, the rate of return on the investments is crucial to the value of defined-contribution pension schemes at retirement. This raises a number of challenging questions with respect to the structuring of the payout options for these schemes. The main options include lump-sum payments, programmed withdrawals and annuities.

The choice amongst them depends on the balance to strike between flexibility and protection from longevity risk, and is most certainly subject to the country context. To this regard, financial markets need to be sufficiently developed and to offer adequate financial products, which enable individuals to convert the accumulated assets into a stream of income at retirement. It requires the ability from individuals to carefully assess their situation and make important financial choices for themselves.

From a public policy point of view, as the share of household wealth managed by professional asset managers increases, raises the need for good governance, more financial education, and transparency. There is a crucial need for adequate information to households. Recent developments in financial markets support the view that households may not be a position to make informed choices owing to a lack of financial sophistication.

They do not fully grasp the risks inherent to their investment decisions, even more so, if these investments have medium to long-term horizon.

Most households today simply do not have the time, skill or the access to the relevant information in order to manage themselves their long-term savings. They depend on professional asset management for these purposes. However, the interaction between sophisticated asset managers and financially unsophisticated households has its own risks (for both sides) - requiring supervision and consumer protection in order to avert contagion and reputation effects.

The role of private pension funds in financial markets

Let me now turn to the role of pension funds in the financial system and their interactions with and implications for monetary policy:

From a monetary policy viewpoint, given the interactions between financial market developments and monetary policy decision-making it is important to monitor and understand the factors driving the structures of the financial system.

Furthermore, a well-functioning, liquid and deep financial market is essential for central banks as it better ensures that high quality information about economic fundamentals can be extracted from financial market prices.

Owing to the fact that pension funds are stable long-term investors with sophisticated investment strategies implies that they potentially play an important role in the shaping of the financial market.

Hence, the growing importance of pension funds, as illustrated in the strong growth of pension fund assets, is therefore likely to enhance the efficiency, depth and liquidity of the financial markets. This may contribute to improving the functioning of the financial system and, in turn, may foster a smoother transmission of monetary policy.

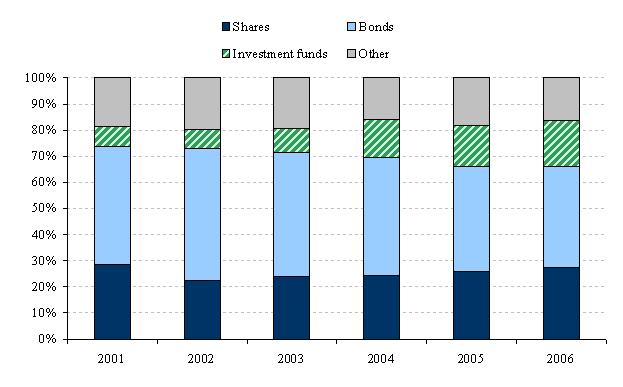

In this light, it may be useful to briefly dwell on the recent trends in terms of pension fund investment structures measured by the allocation of financial assets.

Chart II thus illustrates that bills and bonds issued by the public and private sectors is the predominant asset class constituting around 39% of total pension fund assets in 2006. However, the importance of bonds as an investment class has been waning somewhat in recent years reflecting a reallocation of pension fund assets towards allocations in shares and investment funds. Especially, pension funds’ investment in mutual funds increased markedly over the past years: from 8% of total pension fund assets in 2001 to 18% in 2006.

In general, we observe that over the past 5-6 years the pension fund sector has pursued an increasingly diversified investment strategy.

The increasing variety of pension fund assets is important not only for the pension fund sector’s risk and return characteristics, but crucially also affects the sources of financing available to the corporate sector.

By investing (directly or indirectly) in shares and private sector bonds, the pension fund sector may offer alternative sources of financing for the non-financial corporate sector, and hence may provide a substitute for bank financing, which remains the predominant source of corporate funding in the euro area. All things else being equal, this will contribute to improving the access to financing and lowering the cost of financing for the euro area non-financial sector.

In this context, pension funds – similar to other long-term institutional investors – may also contribute to the efficient monitoring of listed firms with favourable effects on transparency and corporate governance, which hence should enhance the market discipline of the euro area corporate sector.

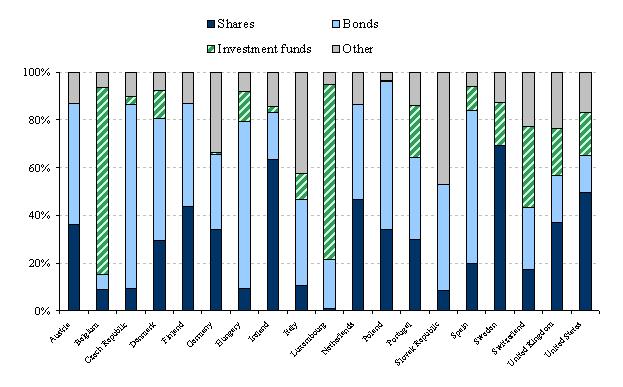

In spite of the overall trend towards a more diverse investment portfolio, the pension-fund asset allocation still differs significantly across countries, as illustrated in Chart III.

For example, investments in the bond market remain the pre-dominant option for pension funds in most of the Central and Eastern European countries, whereas stock market placements are particularly important in the Anglo-Saxon countries and notably in Sweden.

Moreover, pension funds in Belgium and Luxembourg allocate a predominant part of their assets to investment funds.

The widely different asset allocation strategies observed across OECD countries can to a large extent be ascribed to the diversity of legal and regulatory arrangements pertaining in the individual countries.

For example, in general, Anglo-Saxon countries adopt the prudent person rule (PPR) in pension fund investment. Under this approach assets should be invested ‘prudently’ rather than limited according to category, and there are few investment restrictions on any specific assets. In practice this appears to lead to a higher share of assets in equities.

Likewise, different quantitative asset restrictions (QAR) have traditionally been applied in many other countries and normally stipulate upper limits of investment in specific asset classes, e.g. equities and foreign assets. [1]

At the same time, there does not seem to be clear evidence that countries with predominantly defined-benefit pension plans invest more or less in risky assets, such as shares, than in countries where defined-contribution plans are dominant. [2]

Finally, in view of the cross-country differences in asset allocations even within the euro area monetary policy may affect pension fund asset returns in diverse ways across the euro area countries.

That being said, a credible and stability-oriented monetary policy focused on preserving price stability over the medium to longer-term is nonetheless the central bank’s most important contribution to ensure that pension funds accomplish stable and predictable returns on their investments and maintain their crucial role as an important source of funding for the rest of the financial sector.

However, policy makers should also be aware of the potential interactions between the development of the pension fund sector and the monetary policy transmission mechanism. This is the subject to which I now turn.

Changes to the monetary transmission mechanism and implications for monetary policy

In light of the changes to the financial system brought forward by the growing importance of institutional investors, and the pension fund sector in particular, let me now turn to some of the implications for monetary policy.

In terms of the effect of institutional investors on the monetary policy transmission mechanism, it may be recalled that monetary policy affects asset prices via the effect of changes in the policy rates on the yields on asset prices. Furthermore, changes in monetary policy may affect the risk perceptions of market participants, which will also feed into the pricing of financial assets. Changes in asset prices will in turn (via wealth effects) affect the saving and spending behaviour of economic agents.

Furthermore, financial innovation, for example in the form of new credit risk transfer products, created more investment opportunities for all market participants. This may have induced a more risk-taking investment behaviour and may have amplified asset price developments by the compression of risk premia. [3] Against this background, the turmoil observed over the past year may to some extent reflect a re-pricing of risks. [4]

In addition, it has been argued that the heightened importance of pension funds (and other non-bank financial intermediaries) has complicated the intermediation process. [5]

In a sense one could say that the chain of intermediating funds between savers and investors has become longer and more complex than in the past. A practical implication of this development is that although banks remain key players in this process, central banks can no longer limit themselves to the analysis of the banking sector when trying to interpret monetary developments.

The modern central bank clearly needs to broaden its focus and to analyse a much wider group of financial intermediaries than in the past. [6]

Moreover, with the growing importance of institutional investors, including pension funds, on pricing in financial markets central banks need to pay attention to certain risks emerging from these developments.

In particular, an “agency problem” will inevitably exist in the behavioural pattern of institutional investors arising from the difficulty of perfectly aligning the incentives of savers and those of the delegated portfolio managers. This may create issues of moral hazard, which are often resolved by judging the performance of portfolio managers against certain benchmarks. This could in turn lead to herd behaviour among investment managers and potentially to misaligned financial market prices that may blur the content of the information retrieved by the central bank.

For pension funds, in particular, the shortening of the time horizon associated with the progressive aging of society might create incentives for asset managers to be myopic.

Overall, while noting that the growing importance of pension funds is beneficial to the functioning of the financial system, it also provides new challenges for central bank analysis and operations.

Finally, in particular in view of the current juncture of financial market turmoil, I would like to stress the significance of a strong and stable pension fund sector for the stability of financial markets and the wider economy.

Summary

Let me now briefly conclude by summarising the main points of my intervention:

Several difficult challenges are faced by the euro area economy in general and the private pension funds sector more specifically:

1. the ageing population, where I see an greater need on the side of public authorities and private pension funds to foster conditions that encourage and are conducive to saving, particularly in countries with a strong ageing of the population.

2. the preservation of the purchasing power of money, where pension funds as long-run investors have a great interest that the ECB fulfils its mandate of price stability.

This is important not only for preserving the confidence of investors in private pension funds, but also to ensure the sustainability of pension funds as an important source of funding for the rest of the financial sector. Let me, therefore, assure you, that the ECB remains focussed on delivering price stability for the euro area.

3. the shift in the preference for managed savings on behalf of households, where I encourage all actions that improve the corporate governance framework for pension funds and provide more information and transparency to pension fund customers, supporting the long term accountability of private pension funds. At the same time, for such measures to be fruitful, I see a need to enhance the financial education of our fellow citizen.

It is in the most fundamental interest of Europe to have a strong and vibrant pension fund sector. This need is currently compounded in the context of the financial market turbulences as private pension funds owing to their property as long-term investors can importantly contribute to the stability of financial markets, and thus the macro-economy.

Thank you for your attention!

Annex

Chart I: Old age dependency ratio

(65+ in % 20-64)

Source OECD.

Chart II. Structure of assets of pension funds in selected OECD countries 2001-2006

(in per cent of total investment)

Source: OECD, Global pension statistics.

Note: Investment funds include “mutual funds” and private investment funds” (including private equity and hedge funds).

Chart III. Structure of assets of pension funds in selected OECD countries 2006

(in per cent of total investment)

Source: OECD, Global pension statistics.

Note: Investment funds include “mutual funds” and private investment funds” (including private equity and hedge funds).

-

[1] See e.g. OECD (2008), Survey of Investment Regulations of Pension Funds, July.

-

[2] See OECD (2007), Pension Markets in Focus, Issue 4, November.

-

[3] See, for example, the article on “The role of banks in the monetary policy transmission” in the August 2008 ECB Monthly Bulletin.

-

[4] See e.g. Box 3 entitled “The recent repricing of credit risk” in the October 2007 ECB Monthly Bulletin.

-

[5] See Rajan, R. (2005), “Has financial development made the world riskier?”, NBER Working Paper No. 11728.

-

[6] Recent examples of monetary and financial analyses conducted at the ECB include Box 1 entitled “New estimates on holdings by sector for euro area M3” in the December 2007 Monthly Bulletin; Box 1 entitled “Recent developments in MFI longer-term financial liabilities” in the July 2006 Monthly Bulletin; and Box 3 entitled “Demand for bonds by institutional investors and bond yield developments in the euro area” in the May 2007 Monthly Bulletin.

Banco Central Europeo

Dirección General de Comunicación

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Alemania

- +49 69 1344 7455

- media@ecb.europa.eu

Se permite la reproducción, siempre que se cite la fuente.

Contactos de prensa