Contingent liabilities: past materialisations and present risks

Published as part of the Financial Stability Review, May 2021.

Fiscal policy support has mitigated financial stability risks during the pandemic, but the vulnerabilities arising from contingent liabilities have increased for euro area sovereigns. National policy responses to support households and firms during the pandemic directly increased the aggregate euro area general government debt-to-GDP level by around 14 percentage points to around 100% of GDP in 2020. Additionally, public guarantee schemes that were introduced in 2020 constitute sizeable contingent liabilities for governments in most euro area countries, adding to the stock of both existing government guarantees and other implicit contingent liabilities, which reinforces concerns about the emergence of an adverse sovereign-bank-corporate nexus. Against this backdrop, this box presents historical evidence from contingent liability materialisations, investigates their commonalities and differences with the situation under the current pandemic-induced shock and assesses the ensuing risk for sovereigns.

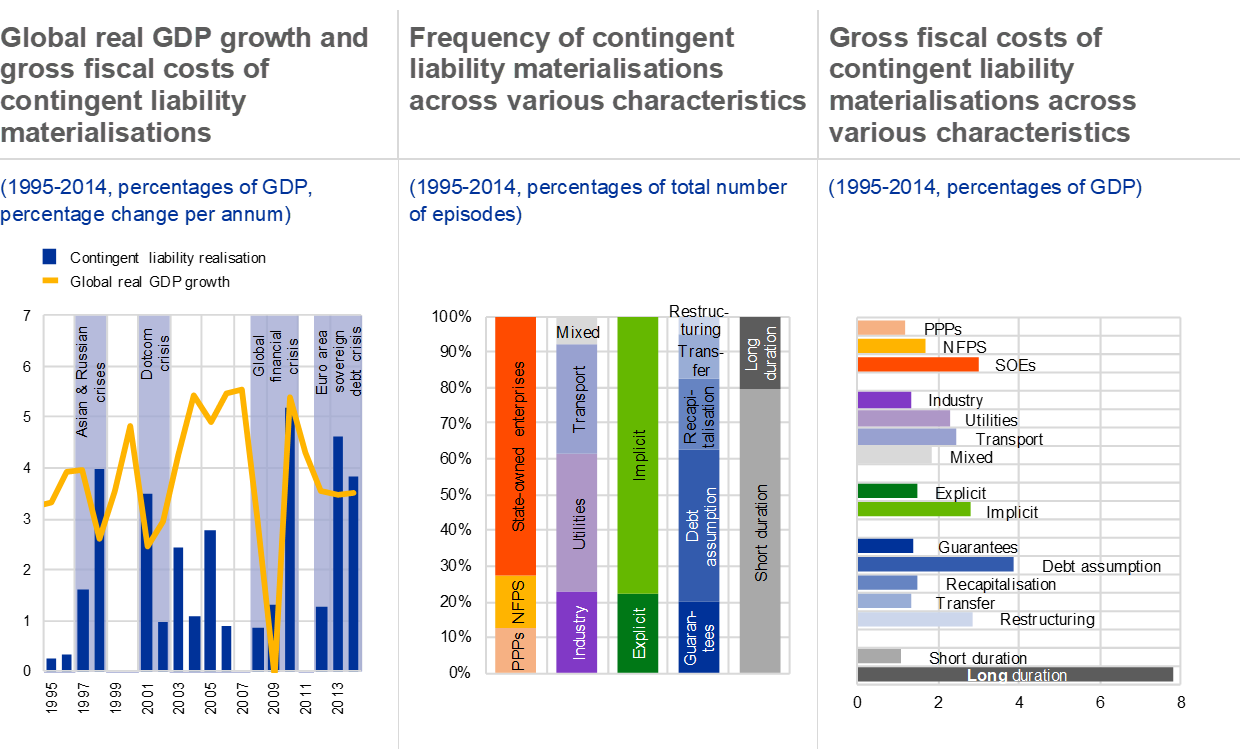

Chart A

Historical evidence on contingent liability materialisations suggests that they can be a significant source of risk for sovereigns

Sources: Bova, Ruiz-Arranz, Toscani and Ture (2019), ECB and ECB calculations.

Notes: The global sample covers 33 advanced and emerging market economies across the globe. Following Bova et al., gross fiscal costs are defined as gross government payouts associated with contingent liability materialisations, expressed as a share of GDP. Middle and right panels: NFPS: non-financial private sector; PPP: public-private partnerships. Right panel: average gross fiscal costs per category as a share of GDP. SOEs: state-owned enterprises.

Historically, contingent liabilities have materialised in waves and can be a significant source of risk for sovereigns.[1] Data on global historical materialisation of government contingent liabilities for non-financial firms reveal that the fiscal costs incurred by sovereigns can be sizeable.[2] In particular, the global financial crisis and the euro area sovereign debt crisis have demonstrated that associated fiscal costs may average around 5% of GDP, and have even exceeded 10% of GDP in some European countries. The costs have been exacerbated by the marked drops in GDP growth coinciding with the materialisation of contingent liabilities (see Chart A, left panel).[3]

In the past, the largest fiscal costs related to public bailouts of state-owned enterprises stemming from implicit commitments. In general, implicit contingent liabilities – not linked to an explicit legal commitment of the state – have materialised more frequently and have also incurred higher costs in the past (see Chart A, middle and right panels). Resolution measures, mainly in the form of debt assumption and restructuring, were generally associated with higher costs. By contrast guarantees coincided with the lowest costs. Also, it appears that support measures with a short duration entail lower fiscal costs (see Chart A, right panel), meaning that the speed with which policy actions are implemented can be an important consideration when designing policy responses.[4]

In contrast to past crises, the recent pandemic-induced large-scale loan guarantee programmes constitute a novel source of contingent liabilities. State-guaranteed bank lending schemes have been a key pillar of the pandemic fiscal support measures. Public guarantee envelopes amount to around 14% of GDP, with take-up of around 4% of GDP for the euro area on aggregate so far. The euro area aggregate masks considerable heterogeneity between countries in terms of both envelopes and take-up levels. One explanation could be that, instead of adhering to direct support measures, fiscally more constrained governments opted for more generous guarantee schemes which do not affect fiscal balances immediately (see Chart B, left panel).

While pandemic-related loan guarantees have the benefit of sharing some risks with banks and spreading the exposure across many firms, they are concentrated in the most vulnerable sectors. In most euro area countries, government guarantees cover less than 100% of the underlying loan. Accordingly, banks not only share some of the risk ex post but also have direct incentives to help prevent losses arising ex ante. In addition, the vast majority of these schemes have been utilised by SMEs, which account for up to 80% of total guarantee take-up (see Chart B, middle panel). The average loan size is therefore relatively small, ranging from €80,000 in Italy to €380,000 in Germany. In contrast to past contingent liability materialisations which were characterised primarily by the resolution of large firms, the guarantees expose governments now to a more dispersed risk which depends on the overall health of the corporate sector rather than individual exposures. While this is inherently related to the pace and strength of the economic recovery, SMEs in the most affected sectors were more likely to take up guarantees as they were facing more severe liquidity needs and a more abrupt tightening of credit conditions.[5] As a consequence, the risk exposure of governments may be larger than the aggregate health of the corporate sector suggests.

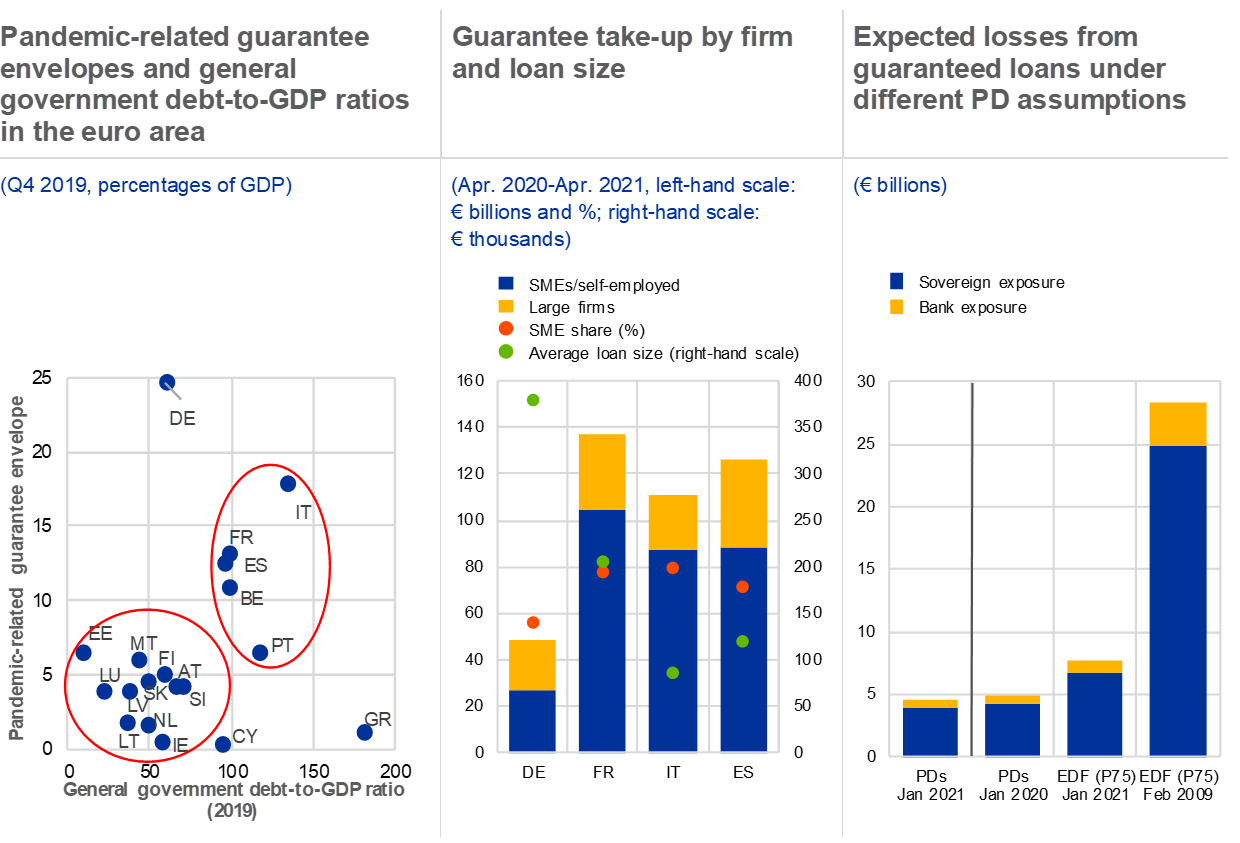

Chart B

SMEs benefit most from guarantee schemes despite the differences in take-up levels and envelopes of contingent liabilities across countries, while the risk for governments appears to be contained

Sources: Eurostat, ECB and ECB calculations based on AnaCredit, national sources and Moody’s Analytics.

Notes: Right panel: expected losses are computed based on aggregate government guarantee take-up (from national sources) and different measures of one-year ahead probabilities of default. PDs are weighted average PDs of a fixed sample of debtors in AnaCredit who used government guarantees at least once since January 2020. Expected default frequencies (EDF) are obtained from Moody’s and reflected the 75th percentile of the cross-firm distribution in January 2021 and its historical maximum in February 2009.

The probability of default (PD) on guaranteed loans has fallen during the pandemic, which mitigates sovereigns’ risk exposure but could conceal tail risks if PDs are too optimistic. According to banks’ internal models, corporates which took up government-guaranteed loans were less likely to default, despite the challenging economic situation. On the one hand, this could reflect the benign effect of guarantees on corporate financing conditions, which allows firms to stay afloat for longer, despite the drop in revenues and profits. On the other hand, falling PDs could be driven by adjustments to banks’ internal models, which might result in an overly optimistic assessments of firms’ likelihood of defaulting.[6] Based on the bank-reported credit risk, lower PDs imply that the expected losses for governments on these guarantees are smaller than they would have been based on pre-pandemic PDs (see Chart B, right panel). At the same time, the actual exposure of sovereigns could be higher than internal bank models suggest. This would be the case if the current assessment turns out to be too optimistic and PDs are closer to the market-based expected default frequencies during historical stress episodes and among vulnerable corporates.

The risks arising from government guarantees appear manageable, while possible bailouts for state-owned enterprises pose a tail risk. Although estimated PDs may be too optimistic, the overall size of the sovereign risk exposure from guarantees appears to be contained Even if PDs on guaranteed loans were to rise to levels last seen among the 25% most vulnerable firms during the global financial crisis, the expected losses for sovereigns would rise to only €25 billion or 0.2% of euro area GDP (see Chart B, right panel). At the same time, more conventional materialisations of contingent liabilities related to implicit commitments towards large corporates or state-owned enterprises may still occur going forward. Based on historical evidence, the fiscal impact of these contingent liabilities can be sizeable and therefore pose a larger tail risk for sovereigns than their direct exposure from guarantees.

- For an analysis of government involvement in non-financial corporate restructuring involving fiscal costs, see Grigorian, D. and Raei, F., “Government Involvement in Corporate Debt Restructuring: Case Studies from the Great Recession”, IMF Working Paper, No 10/260, International Monetary Fund, 2010, while for fiscal costs associated with the financial sector bailouts, see Amaglobeli, D., End, N., Jarmuzek, M. and Palomba, G., “The Fiscal Costs of Systemic Banking Crises”, International Finance, Vol. 20, Issue 1, 2017, pp. 2-25.

- Bova et al., “The Impact of Contingent Liability Realizations on Public Finances”, International Tax and Public Finance, Vol. 26, Issue 2, 2019, pp. 381-417, provide a comprehensive database with contingent liability materialisations since 1990, encompassing information for 80 advanced and emerging market economies across Europe, North and South America, Asia and Australia. One important aspect that is not covered by this database for non-financial corporates is the net fiscal cost, which would take into account asset recoveries, and typically reduce the cost for sovereigns over time.

- This is in line with the findings of Bova et al. for the measure of contingent liability materialisations incorporating both non-financial and financial corporates using the multivariate regression framework. The results based on a similar framework but employing the measure of contingent liability materialisation covering only non-financial corporates, corroborate this finding.

- This finding is broadly consistent with the evidence from Frydl, E., “The Length and Cost of Banking Crises”, IMF Working Paper, No 99/30, International Monetary Fund, 1999, and Baldacci, E., Gupta, S. and Mulas-Granados, C., “How Effective is Fiscal Policy Response in Systemic Banking Crises?”, IMF Working Paper, No 09/160, International Monetary Fund, 2009, for banking stress episodes.

- For more details on the drivers of cross-country differences in the take-up of government guarantees, see the box entitled “Public loan guarantees and bank lending in the COVID-19 period”, Economic Bulletin, Issue 6, ECB, 2020.

- For further details, see the introductory statement by Andrea Enria at the press conference on the results of the 2020 SREP cycle, 28 January 2021.