- STATISTICAL RELEASE

Euro area economic and financial developments by institutional sector: fourth quarter of 2022

27 April 2023

- Euro area net saving decreased to €626 billion in 2022, compared with €668 billion in the four quarter period ending on the third quarter of 2022

- Household debt-to-income ratio declined to 93.1% in fourth quarter of 2022 from 95.8% one year earlier

- Non-financial corporations' debt-to-GDP ratio (consolidated measure) decreased to 74.7% in fourth quarter of 2022 from 79.0% one year earlier

Total euro area economy[1]

Euro area net saving decreased to €626 billion (5.9% of euro area net disposable income) in 2022 compared with €668 billion in the four quarter period ending on the third quarter of 2022. Euro area net non-financial investment was broadly unchanged at €661 billion (6.3% of net disposable income), reflecting stable net investment by all euro area sectors (see Chart 1).

Euro area net lending to the rest of the world decreased to €2 billion (from €39 billion previously), reflecting the lower net saving and the broadly unchanged net non-financial investment. Net lending of non-financial corporations increased to €75 billion (0.7% of euro area net disposable income) from €57 billion, while that of financial corporations grew to €76 billion (0.7% of euro area net disposable income) from €61 billion. Net lending by households decreased to €335 billion (3.2% of euro area net disposable income) from €347 billion. The increase in net lending by the total private sector was more than offset by an increase in net borrowing by the general government to €484 billion (-4.6% of euro area net disposable income), after €426 billion previously.

Chart 1

Euro area saving, investment and net lending to the rest of the world

(EUR billions, four-quarter sums)

* Net saving minus net capital transfers to the rest of the world (equals change in net worth due to transactions).

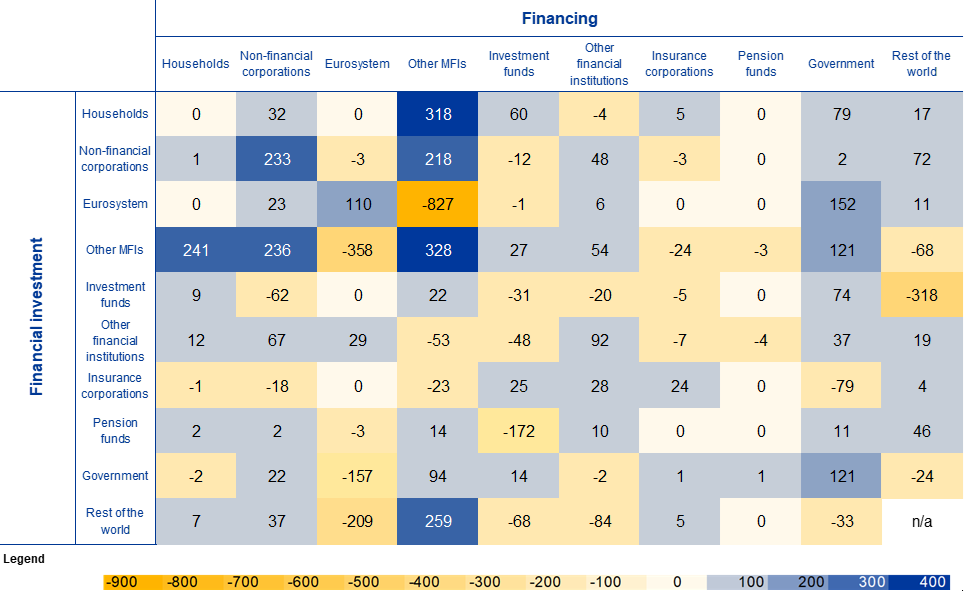

Financial transactions can be presented with a counterpart sector breakdown for deposits, loans, debt securities, listed shares and investment fund shares (see Table 1). In 2022 the largest aggregated transactions in these financial instruments were interbank operations as other MFIs[2] redeemed liabilities with the Eurosystem (-€827 billion), decreased deposits with the Eurosystem (-€358 billion) and increased deposits and other assets with other MFIs (€328). Financial investment of households involved to a large extent transactions vis-à-vis other MFIs (€318 billion), mostly in the form of deposits, as well as the financing of government through purchases of debt securities (€79 billion). In parallel, the financing received by households from other MFIs in the form of loans amounted to €241 billion. The largest financial transactions vis-à-vis the rest of the world involved euro area investment funds, which sold (in net terms) instruments issued by the rest of the world (-€318 billion). In addition, the financing of other MFIs received from the rest of the world reached €259 billion.

Table 1

Selected financial transactions* between sectors and with the rest of the world

(EUR billions, four-quarter sums, 2022)

Source: ECB.

* Financial instruments for which the counterpart sector breakdown is available: deposits, loans, debt securities, listed shares and investment fund shares/units.

Households

Household financial investment increased at an annual rate of 2.5% in the fourth quarter of 2022, down from 2.7% in the previous quarter. Investment in currency and deposits as well as shares and other equity were the main contributors to this deceleration, while net purchases of debt securities accelerated (see Table 2 below).

Households were net buyers of debt securities issued by all sectors except other financial institutions. Households were overall net buyers of listed shares, primarily those issued by non-financial corporations and the rest of the world (i.e. shares issued by non-residents), while selling listed shares issued by MFIs (see Table 2.2. in the Annex).

Table 2

Financial investment and financing of households, main items

(annual growth rates)

Financial transactions | |||||

2021 Q4 | 2022 Q1 | 2022 Q2 | 2022 Q3 | 2022 Q4 | |

Financial investment* | 3.7 | 3.0 | 2.7 | 2.7 | 2.5 |

Currency and deposits | 4.9 | 4.2 | 3.7 | 4.0 | 3.7 |

Debt securities | -7.5 | -5.8 | 0.9 | 8.5 | 22.5 |

Shares and other equity | 3.7 | 2.6 | 2.2 | 1.3 | 0.8 |

Life insurance | 2.2 | 1.9 | 1.5 | 1.3 | 1.0 |

Pension schemes | 2.0 | 2.2 | 2.4 | 2.4 | 2.5 |

Financing** | 4.1 | 3.7 | 4.7 | 5.2 | 4.6 |

Loans | 4.1 | 4.2 | 4.3 | 4.2 | 3.7 |

Source: ECB.

* Items not shown include: loans granted, prepayments of insurance premiums and reserves for outstanding claims and other accounts receivable.

** Items not shown include: financial derivatives' net liabilities, pension schemes and other accounts payable.

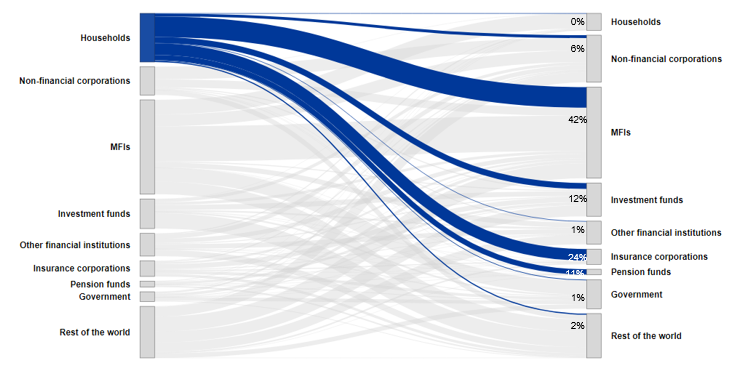

Chart 2 below shows the stock of selected financial assets held by households (in dark blue) vis-à-vis counterpart sectors, at the end of 2022.[3] Households’ financial assets were mostly issued by financial intermediaries such as MFIs (42% of households’ allocated financial assets), insurance corporations (24%), investment funds (12%) and pension funds (11%). Holdings of financial assets vis-à-vis non-financial corporations (6%), government (1%) and the rest of the world (2%), mainly in the form of listed shares and debt securities, represented much lower proportions of households’ financial assets.

Chart 2

Households’ financial assets by counterpart sector; selected financial instruments*

(2022 end of period stocks)

Source: ECB.

Discrepancies between totals and their components may arise from rounding.

* Financial instruments for which the counterpart sector breakdown is available: deposits, loans, debt securities, listed shares and investment fund shares/units. In addition, in this chart the counterpart sector breakdown for insurance, pension and standardised guarantee schemes (F.6) is estimated. (See methodological note: Extension of the who-to-whom presentation to insurance and pension assets).

The household debt-to-income ratio[4] decreased, to 93.1% in the fourth quarter of 2022 from 95.8% in the fourth quarter of 2021. The household debt-to-GDP ratio declined, to 57.3% in the fourth quarter of 2022 from 59.8% in the fourth quarter of 2021 (see Chart 3).

Chart 3

Debt ratios of households and non-financial corporations

(percentages of GDP)

Source: ECB and Eurostat.

* Outstanding amount of loans, debt securities, trade credits and pension scheme liabilities.

** Outstanding amount of loans and debt securities, excluding debt positions between non-financial corporations.

*** Outstanding amount of loan liabilities.

Non-financial corporations

In the fourth quarter of 2022, the annual growth of financing of non-financial corporations declined to 2.1%, after 3.2% in the previous quarter. This resulted from a deceleration in financing by loans, in particular from MFIs, other financial institutions and the rest of the world, as well as financing in the form of debt securities, shares and other equity, and trade credits (see Table 3 below and Table 3.2 in the Annex).

Table 3

Financing and financial investment of non-financial corporations, main items

(annual growth rates)

Financial transactions | |||||

2021 Q4 | 2022 Q1 | 2022 Q2 | 2022 Q3 | 2022 Q4 | |

Financing* | 3.1 | 3.0 | 3.1 | 3.2 | 2.1 |

Debt securities | 5.3 | 5.5 | 4.8 | 3.1 | 0.7 |

Loans | 4.6 | 4.6 | 5.1 | 6.0 | 4.5 |

Shares and other equity | 1.1 | 1.2 | 1.3 | 1.5 | 1.0 |

Trade credits and advances | 10.6 | 9.6 | 9.7 | 7.5 | 4.4 |

Financial investment** | 4.9 | 4.6 | 4.5 | 4.4 | 3.1 |

Currency and deposits | 9.6 | 9.0 | 8.5 | 8.0 | 5.8 |

Debt securities | -5.5 | -1.5 | 3.9 | 10.5 | 12.9 |

Loans | 6.4 | 6.4 | 5.7 | 5.2 | 3.9 |

Shares and other equity | 1.4 | 1.7 | 2.1 | 2.5 | 1.8 |

Source: ECB.

* Items not shown include: pension schemes, other accounts payable, financial derivative's net liabilities and deposits.

** Items not shown include: other accounts receivable and prepayments of insurance premiums and reserves for outstanding claims.

Non-financial corporations' debt-to-GDP ratio (consolidated measure) decreased to 74.7% in the fourth quarter of 2022, from 79.0% in the fourth quarter of 2021; the non-consolidated, wider debt measure declined to 135.7% from 142.1% (see Chart 3).

Chart 4 below shows the main components of the non-financial corporations’ debt (in dark blue) vis-à-vis counterpart sectors. At the end of 2022, the non-financial corporations’ debt in the form of loans and debt securities was held primarily by MFIs (37%), other non-financial corporations (29%), the rest of the world (15%) and other financial institutions (10%).

Chart 4

The main components of NFC debt (loans and debt securities) by counterpart sector

(2022 end of period stocks)

Source: ECB.

Discrepancies between totals and their components may arise from rounding.

For queries, please use the Statistical information request form.

Notes

- These data come from a second release of quarterly euro area sector accounts from the European Central Bank (ECB) and Eurostat, the statistical office of the European Union. This release incorporates revisions and completed data for all sectors compared with the first quarterly release on "Euro area households and non-financial corporations" of 5 April 2023.

- The euro area and national financial accounts data of non-financial corporations and households are available in an interactive dashboard.

- The debt-to-GDP (or debt-to-income) ratios are calculated as the outstanding amount of debt in the reference quarter divided by the sum of GDP (or income) in the four quarters to the reference quarter. The ratio of non-financial transactions (e.g. savings) as a percentage of income or GDP is calculated as sum of the four quarters to the reference quarter for both numerator and denominator.

- The annual growth rate of non-financial transactions and of outstanding assets and liabilities (stocks) is calculated as the percentage change between the value for a given quarter and that value recorded four quarters earlier. The annual growth rates used for financial transactions refer to the total value of transactions during the year in relation to the outstanding stock a year before.

- Hyperlinks in the main body of the statistical release lead to data that may change with subsequent releases as a result of revisions. Figures shown in annex tables are a snapshot of the data as at the time of the current release.

Euro area data exclude Croatia.

Other MFIs include banks and money market funds but exclude the Eurosystem.

This excludes financial instruments for which the counterpart sector breakdown is not available such as unlisted shares, other equity, and other accounts payable.

Calculated as loans divided by gross disposable income adjusted for the change in pension entitlements.