- THE ECB BLOG

One market, one supervision: the case for integrated EU capital markets oversight

30 March 2026

The current supervisory framework for EU capital markets is complex and fragmented. Key market players would need integrated supervision, which would increase supervisory consistency, improve cross-border risk detection and support market integration, providing stronger foundations for the savings and investments union.

The savings and investments union agenda has given fresh momentum to Europe’s ambition to deepen its capital markets and channel its vast pool of savings into productive investments. One central initiative is the “market integration and supervision package”[1] presented by the European Commission in December 2025. This package is aimed at deepening and integrating EU capital markets. Effective supervision is essential to make this work.

A new ECB Occasional Paper[2] lays out in detail why and how we need more integrated supervision of capital market players. It describes which entities could be supervised at the EU level, presenting the relevant criteria. It also shows how reforming the European Securities and Markets Authority (ESMA) could make EU-level capital market supervision work in practice. This ECB blog post provides a comprehensive summary of the paper.

A fragmented supervisory architecture

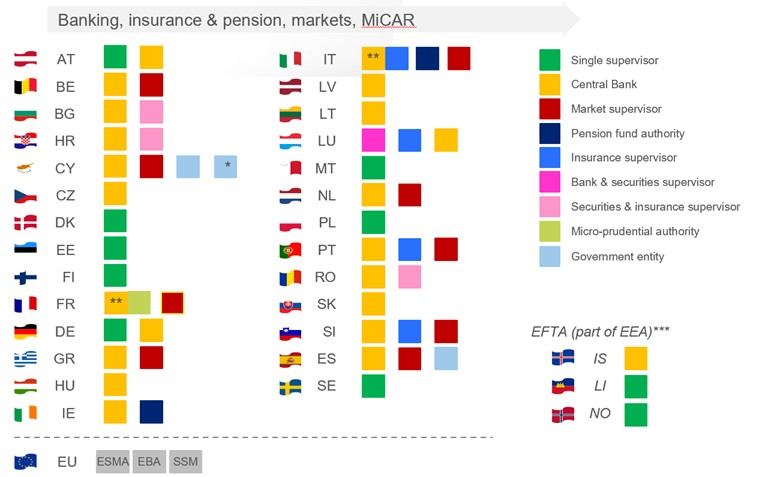

Capital market players increasingly operate across the borders of EU Member States. However, this involves navigating a patchwork of 52 national supervisory authorities (Chart 1). Individual authorities have strong domestic expertise, but no full overview of cross-border risks and activities. National authorities often apply diverging rules and supervisory practices despite the Single Rulebook. This situation is different than European banking supervision, which since 2014 has been significantly centralised through the Single Supervisory Mechanism (SSM).

Chart 1

Supervisory authorities for capital markets in Europe

Notes: The count of supervisory authorities includes banking, insurance and pension fund, central securities depositories (CSDs), central counterparties (CCPs), asset managers, funds, investment firms and trading venues, as well as activities regulated by MiCAR (electronic money tokens, asset-referenced tokens, other crypto-assets and crypto-asset service providers). Supervision of auditors is not covered (see Véron, 2025 for auditor supervision). *In Cyprus there are two government agencies with supervisory responsibilities: one in charge of insurance supervision, another in charge of pension supervision. ** In France and Italy, the microprudential supervisor for banks and insurance, and insurance respectively, comes under the central bank. *** The three non-EU countries of the European Economic Area – Iceland, Lichtenstein and Norway – may be also considered, as their capital market entities fall under ESMA.

Source: ECB.

The fragmentation no longer reflects either market realities or the ambition to have a truly integrated European capital market. For example, a few large central counterparties (CCPs) clear transactions from across the whole EU and beyond. Pan-European central securities depository (CSD) groups are supervised by a range of authorities across multiple jurisdictions. And crypto-asset service providers (CASPs) operate across borders by design. In all these cases, no single national authority has a complete overview – or capacity to act on the system-wide risks involved.

Why EU-level supervision matters

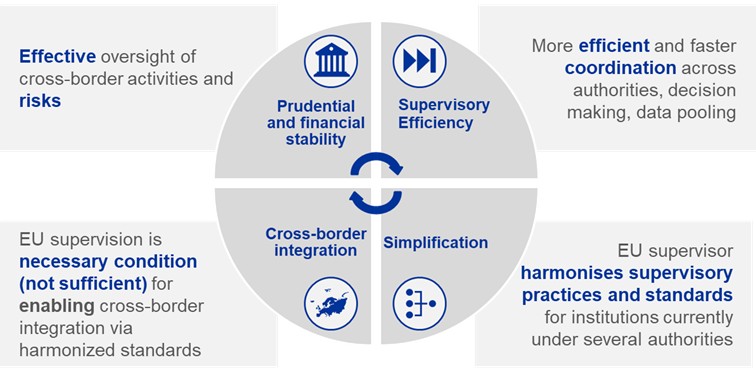

A more integrated supervisory approach would bring four major benefits (Chart 2):

- greater supervisory effectiveness – only EU-level supervision can align supervisory powers with cross-border risks;

- greater efficiency – having one EU supervisor for the largest cross-border players would reduce duplication, streamline data collection and enable proper benchmarking across institutions;

- simpler processes for firms – a single EU interlocutor would dramatically reduce both complexity and compliance costs for large cross-border groups;

- deeper capital market integration – only an EU-level supervisory system can ensure consistent application of the Single Rulebook across the EU and foster a level playing field.

Further harmonisation of insolvency regimes, taxation and company law would compound these benefits, but reforms in those areas are complex, politically difficult and slow. By contrast, integrating the supervisory architecture can deliver tangible progress now.

Chart 2

Four reasons for EU-level supervision

Source: ECB.

How would a new supervisory framework look?

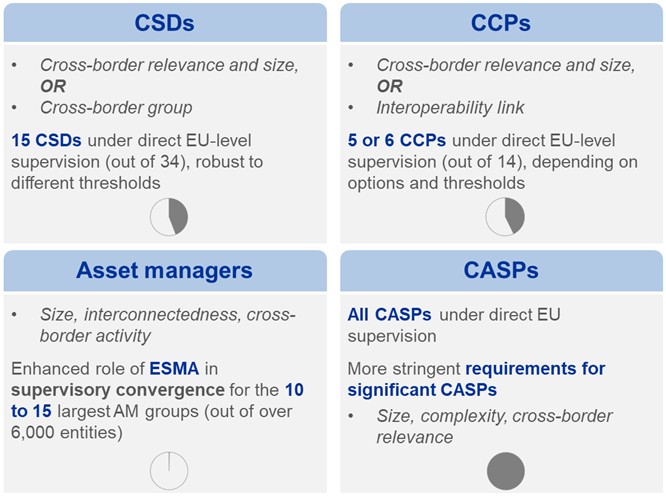

The occasional paper identifies which entities may warrant direct supervision by ESMA, based on size and cross-border relevance, while keeping in mind sectoral specificities. The result is a proportionate two-tier framework. ESMA would directly supervise certain large cross-border players while national authorities would continue to oversee the majority of firms.

Turning to market infrastructures first, five or six CCPs and 15 CSDs – roughly 40% of each sector – would qualify for direct EU supervision. These entities are systemically important beyond any single jurisdiction. However, most CCPs and CSDs mainly serve domestic markets and are not integrated in cross-border groups, so these would remain under national oversight (Chart 3).

Chart 3

Sensitivity analysis on the scope of entities potentially under direct EU supervision*

Note: The grey areas in the circles indicate the share of players that would fall under direct EU supervision based on the proposed analysis.

Source: ECB.

The asset management sector is highly concentrated among a few countries and firms. It is also highly fragmented across the EU.[3] Further harmonisation of the Single Rulebook and effective supervision are essential to supporting integration while adequately capturing the risks of a sector with increasing cross-border activity. Although it is unlikely to achieve direct supervision of asset managers in the short term, a stronger ESMA role in fostering supervisory convergence for the 10 to 15 largest cross-border groups would provide a meaningful European dimension to their oversight.

By contrast there is a compelling case for all CASPs to be under EU supervision, as they are inherently cross-border operators. Some 94 providers were authorised under MiCAR as of November 2025, of which 62 already intend to operate in seven or more Member States and 47 are planning EU-wide activities. Direct EU-level supervision of these providers, with additional prudential requirements for the largest and most complex ones, would create a level playing field from the start. There is also an important simplification argument unique to this sector. As crypto-asset supervision is new, centralising it from the start means the necessary expertise can be built up once and to the highest possible standard. This would also avoid duplicating it imperfectly across 27 jurisdictions.

Expanded supervisory responsibilities require a suitable governance structure. An independent Executive Board (as per the Commission’s proposal) – insulated from national interests and with full enforcement powers – is essential for ESMA to carry out its new responsibilities. Critically, national authorities would still play a significant role. They would cooperate closely with ESMA and act as primary supervisors for their domestic firms, leveraging their local expertise and proximity.

Why act now

EU supervision of capital markets would deliver tangible benefits and is a necessary step to remove existing barriers to capital market integration. It is not a silver bullet – progress on the broader issues holding back the savings and investments union, from innovation financing to legal harmonisation challenges, will be key to channelling capital into productive investment in Europe. But waiting for full legal convergence before reforming supervision would be wasting a major opportunity – and precious time. Already now there is a need for a more consistent and predictable application of the Single Rulebook for significant capital market players. Reforming supervision and promoting legal convergence should go hand in hand.

In line with EU leaders’ call[4] to foster Europe’s competitiveness, the Commission’s proposal to strengthen direct supervision by ESMA provides a real and timely opportunity. The analysis in the occasional paper supports this objective and highlights the need to sustain ambition across the wider savings and investments union agenda.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

See European Commission (2025a), “Further development of capital market integration and supervision within the Union”, COM(2025) 940 final, December, and European Commission (2025b), “Market integration and supervision package”, December.

See Carmassi, J., Dumora Lemaire, O., Evrard, J., Gati, Z., Milea, C., Parisi, L., Rouveyrol, C. and Spolaore, A. (2026), “One market, one supervision”, Occasional Paper Series, No 383, ECB.

See also Ceh, A.M., Daly, P., Evrard, J., Grill, M., Martino, A., Wedow, M., and Weistroffer, C. (2026), “Why we need an EU perspective in the supervision of large asset managers”, The ECB Blog, 13 February 2026.

Conclusions of the European Council meeting of 19 March 2026, see Part III. “Competitiveness and single market”.