The role of demand and supply factors in HICP inflation during the COVID-19 pandemic – a disaggregated perspective

The role of demand and supply factors in HICP inflation during the COVID-19 pandemic – a disaggregated perspective

1 Published as part of the ECB Economic Bulletin, Issue 1/2021.

Introduction

The economic impact of the coronavirus (COVID-19) pandemic is not a standard textbook shock. Instead the shock is multidimensional, with sources on both the external and the domestic side, on both the demand and the supply side, and at both the aggregate and the sector-specific level. This poses challenges for the assessment of inflation. Established relationships between inflation and its determinants may not hold up or may not be scalable, given the magnitude of disturbances in product and labour markets. Moreover, the increasing emphasis of the inflation literature on distributions rather than point outcomes for future inflation is relevant for analysing the impact that the COVID-19 shock has had on inflation risks.

Understanding the drivers of inflation during the pandemic is helped by adopting a more granular perspective than usual. A disaggregated approach is often used by central banks to complement assessments based on headline inflation. Typically, such an approach is used to distil underlying (common) trends in inflation or to improve forecast accuracy.[1] To understand the drivers of inflation, the ECB’s analysis regularly looks at the main components of inflation, such as energy, food, non-energy industrial goods (NEIG) and services. By moving to a higher level of granularity than usual (i.e. the 12 sub-components of the Harmonised Index of Consumer Prices, HICP), the analysis in this article helps to better understand the diverse impact of the pandemic across components and ultimately to enhance our understanding of the current drivers of headline inflation.[2]

The role of supply-side effects in particular is likely to be larger than usual for a number of inflation components. The nature of the lockdowns and containment measures imposed after the outbreak of the pandemic implied a shutdown of business and/or an increase in costs for some sectors.[3] Price changes associated with such supply-side effects may, in the first instance, change relative price developments and not necessarily aggregate inflation. It is common in regular inflation analysis to assess short-term supply disturbances in energy and food prices due to the often large magnitude of these types of shocks. What is distinctive about the pandemic, however, is the larger than usual role of supply effects on core inflation that stem from the lockdowns. A disaggregated approach extended to core components can also shed light on the consequences of the demand shock associated with COVID-19-related income losses or uncertainty. Given the magnitude of the shock, there can be implications for both aggregate price levels and, depending on income and substitution elasticities, relative prices.

This article illustrates how a more disaggregated perspective can help to gauge the implications of COVID-19, augmenting the regular inflation analysis. Section 2 first describes the evolution of aggregate inflation during the COVID-19 period and explains the motivation for the level of granularity adopted in the analysis. Section 3 then examines the drivers of the inflation response, component by component, mainly focusing on the role of domestic factors that are unique to the pandemic. The section also examines the role of demand and supply effects and includes a component-level decomposition of inflation into the structural shock contributions of such effects. Section 4 provides some concluding messages.

2 How has HICP inflation adjusted so far?

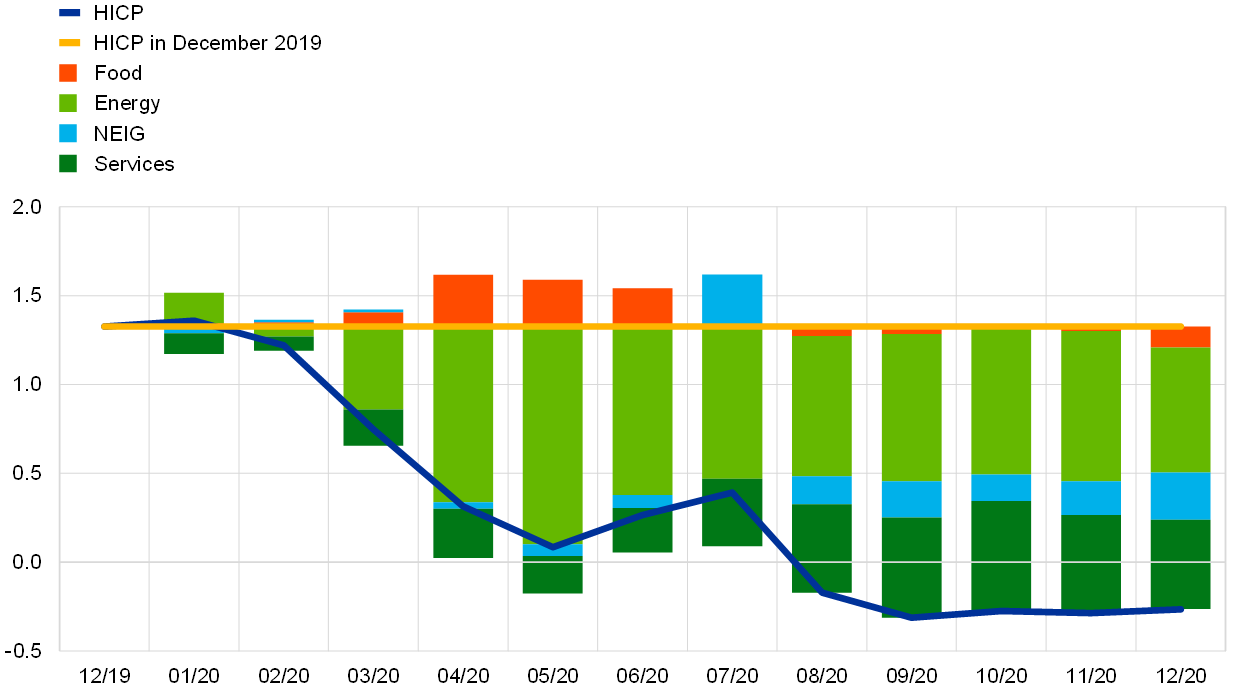

The main components of HICP inflation responded heterogeneously to the pandemic shock. Headline inflation declined from 1.2% in February to 0.1% in May, before dropping into negative territory in August (Chart 1). However, at the level of main components, the response was uneven in terms of both speed and magnitude. The initial steep decline in headline inflation was mainly due to a fall in the contribution of energy inflation from 0.0 to -1.2 percentage points between February and May. The declining contribution of energy can be clearly ascribed to a commodity (oil) related external supply price shock. During the same period, however, the contribution of food inflation increased, mainly owing to the unprocessed food component.[4] The rising contribution of food inflation cannot easily be ascribed to a particular type of shock, as it is likely that there were upward effects from food commodity prices owing to the H1N1 swine flu and higher costs in international and domestic supply chains, but also higher demand as households were forced to shift expenditure from restaurants and canteens to food for home consumption during lockdown. From the middle of the year onwards, headline inflation fell further as HICP inflation excluding energy and food (HICPX) also increasingly contributed to the disinflationary tendencies, mainly owing to a decline in services inflation and, to a lesser extent, a decline in NEIG inflation.

Chart 1

Decomposition of HICP inflation

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: The bars show contributions of components to the change in annual HICP since December 2019.

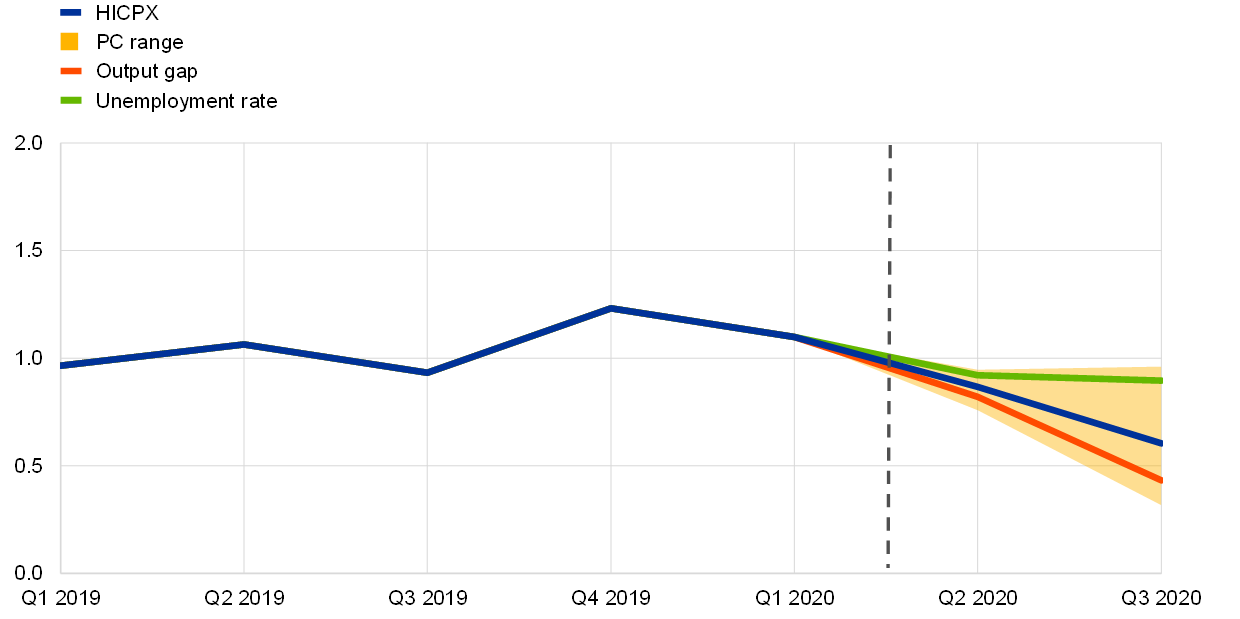

Until the third quarter of 2020 the response of HICPX inflation was broadly in line with historical regularities, pointing to a clear role for downward demand effects. The response of HICPX inflation during the pandemic was modest relative to the decline in activity. Such short-term persistence can reflect a range of factors, including menu costs, pre-existing supply contracts or a higher priority assigned to maintaining good relationships with business clients.[5] In this respect, HICPX evolved broadly in line with a Phillips curve-based forecast conditioned on developments in standard activity and slack indicators.[6] Assuming that the recessionary impact of the pandemic became fully pervasive in the second quarter, the response of HICPX was broadly in line with expectations (Chart 2). This response in line with slack indicators suggests that weaker (net) demand is likely to have played an important role, but does not preclude the possibility that the multidimensional COVID-19 shock was also characterised by larger than usual supply effects. Indeed, a more structural analysis of the drivers of aggregate headline inflation points to a role for domestic supply effects in the recent dynamics of headline inflation (see Box 1).

The remainder of this article examines the adjustment in HICPX inflation during the pandemic in terms of its short-term persistence and its main drivers. A component-by-component approach based on a higher level of disaggregation for HICPX inflation is used, which can also be related more easily to other sector-specific effects, including measurement issues relating to price imputations.

Chart 2

HICPX inflation response during the pandemic relative to Phillips curve forecasts

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The estimation period ends in the first quarter of 2020. “PC range” refers to the Phillips curve-based forecasts conditioned on GDP growth, the output gap, the unemployment rate and the unemployment gap.

Box 1

Decomposing inflation dynamics during the pandemic: an aggregate perspective

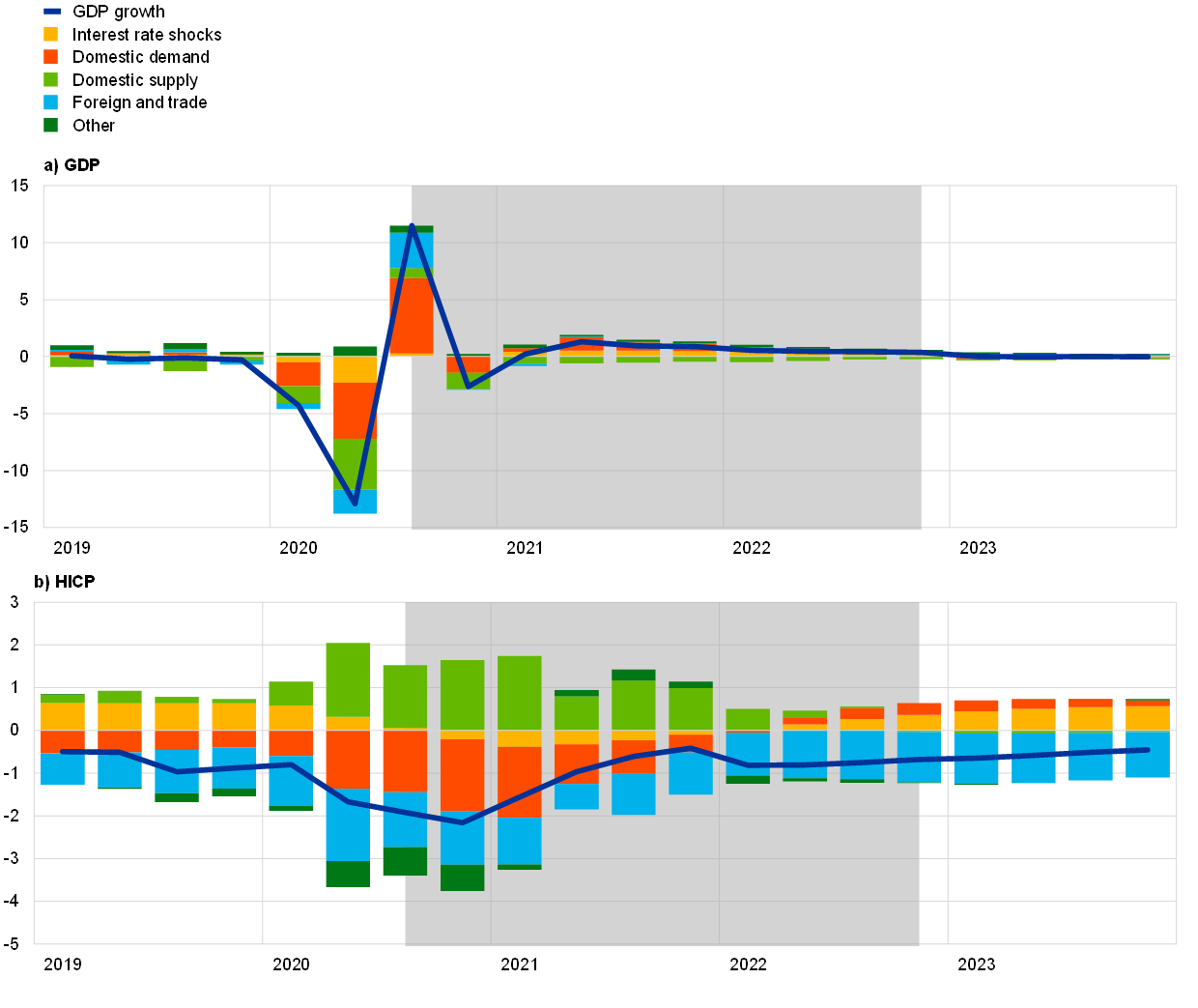

Interpreting price dynamics in terms of structural drivers is a regular exercise in inflation assessment and forecasting. This box does so through the lens of a structural macroeconomic model, the New Area-Wide Model II (NAWM II), which is the ECB’s main dynamic stochastic general equilibrium (DSGE) model.[7] The model is able to disentangle drivers of real GDP growth and inflation in a coherent framework and thereby inform the analysis of the price adjustment.[8]

Based on the historical shock decomposition from the NAWM II, Chart A visualises the drivers of quarterly GDP growth (panel a) and HICP inflation (panel b).[9] The model interprets the weakening in real economic activity as being driven by adverse domestic supply-side and demand-side effects as well as foreign/trade effects, reflecting the global nature of the pandemic shock. The domestic demand-side shocks mainly reflect a fall in domestic consumption following the introduction of confinement measures across almost all countries in the euro area to stop the spread of the virus. Furthermore, a steep fall in foreign demand, owing to the global dimension of the crisis, contributed to the contraction in euro area GDP. GDP recovered in the third quarter of 2020, mainly driven by domestic demand-side factors as consumption rose and, to a lesser extent, by a positive impact from the external sector. Based on the projections for GDP growth in 2021, 2022 and 2023, supply-side factors remain slightly contractionary.

Domestic and foreign demand-side effects and pressures from shocks to interest rates, which drove GDP growth down in 2020, were the main factors behind the fall in euro area HICP inflation in the first half of 2020. This reflects the fact that firms tend to lower prices in response to lower demand. Supply-side effects, however, prevented inflation from falling even further. On the supply side, the drivers of the fall in GDP growth were a combination of adverse effects on factor productivity and direct pricing decisions of firms. Shocks related to the former have, however, only minor consequences for inflation dynamics. Through the lens of the model, firms tried to stabilise profits by leaving prices largely unchanged, whereas the weaker demand would have indicated an even stronger fall in inflation.[10] On balance, these domestic supply-side factors largely offset the downward pressure from weaker domestic demand and mitigate the pass-through from the real side to the nominal side of the economy. The downward pressure on inflation from demand-side factors is more persistent, which is a reflection of price stickiness. Inflation is expected to return to its pre-crisis level in the course of 2021, at which time the model sees both supply-side and demand-side factors vanish.

Chart A

Historical shock decomposition based on NAWM II

(panel a: quarterly percentage changes, deviations from steady state of 1.5%; panel b: annual percentage changes, deviations from steady state of 1.9%)

Source: ECB calculations using NAWM II.

Notes: Panel a: historical shock decomposition – historical data combined with the December 2020 Eurosystem staff macroeconomic projections (grey area) for GDP growth; panel b: historical shock decomposition – historical data combined with the December 2020 Eurosystem staff macroeconomic projections (grey area) for HICP inflation. Shock decompositions are conducted using NAWM II. See Coenen, G., Karadi, P., Schmidt, S. and Warne, A., “The New Area-Wide Model II: an extended version of the ECB’s micro-founded model for forecasting and policy analysis with a financial sector”, Working Paper Series, No 2200, ECB, November 2018. The category “Interest rate shocks” comprises shocks which mainly explain the short-term interest rate (monetary policy shocks), the long-term interest rate (shocks to banks’ survival rate) and the lending rate (shocks to retail banks’ markdown). The category “Foreign and trade” captures shocks to foreign demand, foreign prices, US 3-month and 10-year interest rates, competitors’ export prices, oil prices, import demand and export preferences, mark-up shocks to export prices and import prices, and foreign risk-premium shocks. The category “Domestic demand” includes domestic risk-premium shocks and shocks to government spending, while “Domestic supply” includes transitory and permanent technology shocks as well as wage and price mark-ups. The category “Other” includes measurement errors and residuals from bridge equations.

3 What explains the adjustment of HICP inflation so far?

3.1 Overview of factors unique to the pandemic

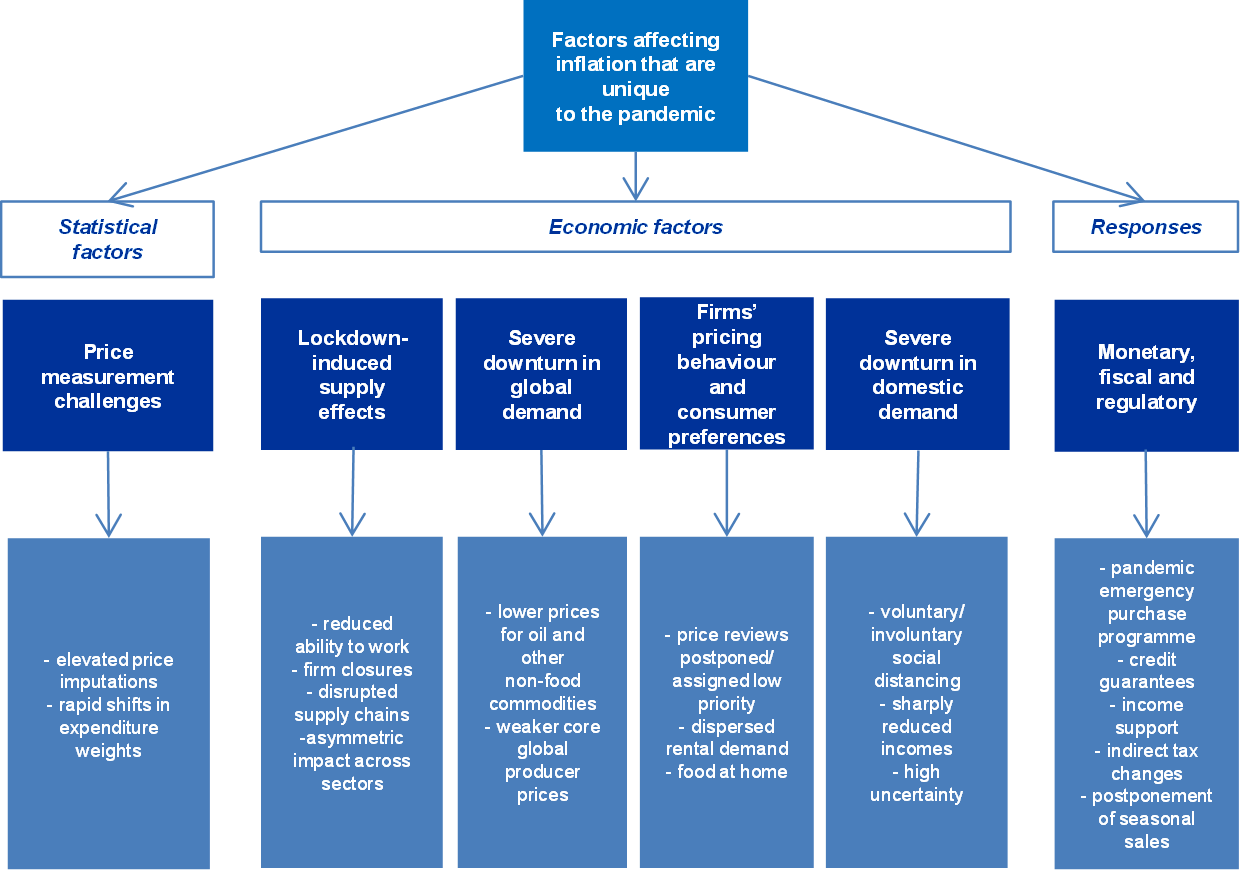

A diverse mix of domestic and global pandemic-related factors have influenced recent inflation dynamics (Figure 1). These factors are of both direct and indirect relevance for inflation, but have in common that they are unparalleled in scale. This holds for the sharp decline in domestic demand, especially in the consumer-facing sectors most exposed to the impact of social distancing. It also holds for the large-scale responses from both monetary and fiscal authorities to the consequences of the pandemic. Given the global nature of the pandemic, the confluence of domestic and external factors has also been unusually strong, including, on the external side, the impact of much weaker global demand, lower prices for oil and other non-food commodities, and, from the third quarter of 2020, the appreciation of the euro effective exchange rate.

Figure 1

Factors that affected the response of inflation to the pandemic shock

Sources: ECB.

Note: For a more detailed exposition on the channels for demand and supply shocks, see, for example, Bobeica, E. and Hartwig, B., “The COVID-19 shock and challenges for time series models”, Working Paper Series, ECB, forthcoming, 2021.

Fiscal and regulatory factors have directly influenced inflation dynamics. The pandemic has triggered fiscal and regulatory responses with a direct, albeit temporary, impact on inflation. In response to the pandemic, several euro area countries have reduced indirect tax rates on a scale not seen before.[11] Taking into account their net effect on a mechanical basis, the impact on HICPX inflation is estimated to be around -0.7 percentage points in the second half of 2020.[12] This compares with an average contribution of 0.2 percentage points since 2004. Regulatory changes have also influenced recent inflation dynamics. For example, the sales season for clothing and footwear in some euro area countries, including Italy and France, was postponed from July to August and extended into September. This added to the volatility of annual inflation rates, making it more challenging to gauge underlying price trends. In assessing the impact of such developments, and pricing behaviour more generally, the availability of timely micro price data has proved helpful (see Box 2).

Pandemic-related factors with an impact on prices beyond the near term have also emerged. The pandemic has had a profound impact on consumer behaviour. Demand for travel and tourism is depressed and seems likely to remain so until there has been a widespread roll-out of effective vaccines. This not only dampened inflation at the aggregate euro area level, but also led to increased heterogeneity in inflation developments across euro area countries, given the important role of tourism in some of them. Moreover, some prices that are typically resilient in crises have also weakened. One example is rents, for which the annual growth rate declined from 1.4% in February 2020 to 1.2% in October 2020. The downward pressure on rents could stem from the indexation of rents to past inflation. However, it could also reflect the introduction of rent freezes in certain cities in response to the pandemic.[13] The pandemic may have also provided some support to price developments in other areas. For example, the prevalence of remote working arrangements has seen an increase in the share of expenditure on personal IT equipment.[14] Other goods for which demand has been boosted include gardening equipment and bicycles.

The lockdowns are unique to the pandemic, especially in terms of the magnitude of the supply effects they have generated. The lockdowns triggered by the pandemic led to severe disruptions to labour supply and production supply chains, particularly during April and May and, to a somewhat lesser extent, in November and December. As noted above, recent evidence on the impact of the initial lockdowns suggests that the associated supply effects have exerted upward pressure on inflation to some extent. Lockdowns also presented price collection difficulties for statisticians. The remainder of this article contains an empirical analysis of the impact of the lockdowns.

Box 2

The role of microdata in inflation analysis

Microdata on prices complement inflation analysis based on official price indices by providing additional information on the behaviour of individual prices. While official price indices allow price levels and inflation rates of narrowly defined product groups to be tracked, these do not allow the tracking of individual prices. Microdata on prices allow additional aspects of price movements to be analysed, e.g. whether price changes become less or more common over time. Microdata on prices are available from three different sources: web-scraped information collected from online stores, shop scanner data and household scanner data. The latter two are collected by, for example, market research companies.[15],[16] This box provides an example of the use of web-scraped information.

Web-scraped data provide highly granular price information in a timely fashion. The data are collected directly from websites of online retailers, making it possible to monitor price movements in quasi-real time. In addition to tracking individual prices over time, these data provide additional information on prices and products offered. For example, online retailers often include information on whether a product price is currently discounted, thereby allowing, for example, the behaviour of discounts during the COVID-19 pandemic to be analysed.

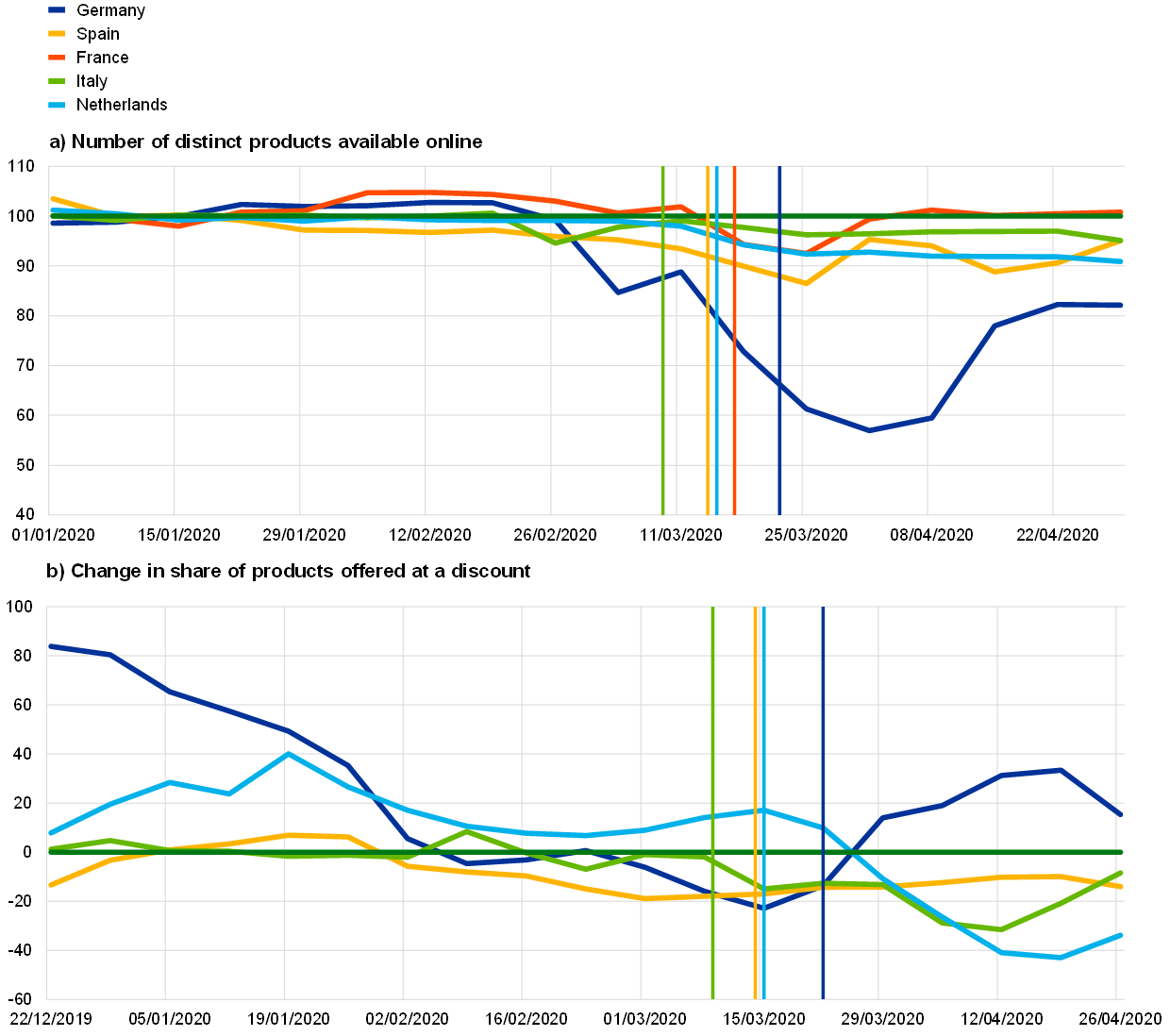

An analysis of web-scraped supermarket data provided by PriceStats shows that during the first wave of the virus both the number of distinct products available online and the share of products offered at a discount decreased. Panel a of Chart A shows that the number of products available online started to decrease at the beginning of March 2020 and, for most online supermarkets in the sample, had not recovered by the end of April. While the number of products available online decreased in all supermarkets in the sample, it did so to different extents, with the largest drop being observed in Germany, where the number of products available in early April was less than 60% of the number available in January 2020. Panel b of Chart A shows that temporary price discounts also became less common during the first wave of the virus, compared to the same period in the previous year. For example, in the Italian supermarket in our sample, the share of products at temporarily reduced prices was nearly 40% lower in mid-April 2020 than a year earlier. This decrease in discounts could be one factor that contributed to the temporary surge in food prices observed in the spring of 2020.

Chart A

Number of distinct products available online by country and annual percentage change in the share of products offered at a discount

(panel a: index, January 2020 = 100; panel b: year-on-year percentage changes)

Source: PriceStats, web-scraped price data.

Notes: Microdata on online prices provided by PriceStats for one online supermarket per country. Panel a shows a weekly index of the number of products available online by country, computed as the ratio of the weekly median of the number of distinct products to the median number of products in January 2020. Panel b shows the 5-week moving average of the year-on-year percentage change in the weekly median of the share of products offered at a discount. France is excluded from the analysis of temporary discounts, as no information on temporary discounts was available from the French online supermarket. The vertical lines indicate the start of the country-specific lockdowns. Latest observations: 30 April 2020.

Microdata on prices will be further analysed within the Price-setting Microdata Analysis Network (PRISMA), which was set up by the European System of Central Banks to deepen the understanding of price-setting behaviour and inflation dynamics in the EU.

3.2 Lockdown-induced inflation persistence

While there is some evidence of postponements of price reviews, it is likely that the impact on inflation persistence was at most modest and temporary. During the initial phase of lockdowns, many firms were closed. Subsequently, during the containment phases, social distancing meant that some firms (e.g. in the tourism and travel sectors) continued to face difficulties in enticing customers. Indeed, reducing prices appears to have generated little or no rebound in demand. Such extraordinary conditions could have resulted in an unanticipated change in pricing behaviour, i.e. the response of the profit margins of firms was fundamentally different to before. Partly to avoid incurring additional menu costs, firms may have also preferred to delay changing prices until the degree of uncertainty surrounding their business outlook eased. The ECB’s Corporate Telephone Survey, for example, indicates that price reviews were pushed down the list of priorities, with postponements not uncommon among firms (see also Box 3). However, other studies based on different data sources point to a quicker reaction in the pricing behaviour of firms, suggesting that the overall impact on frequency of price changes is not clear cut.[17]

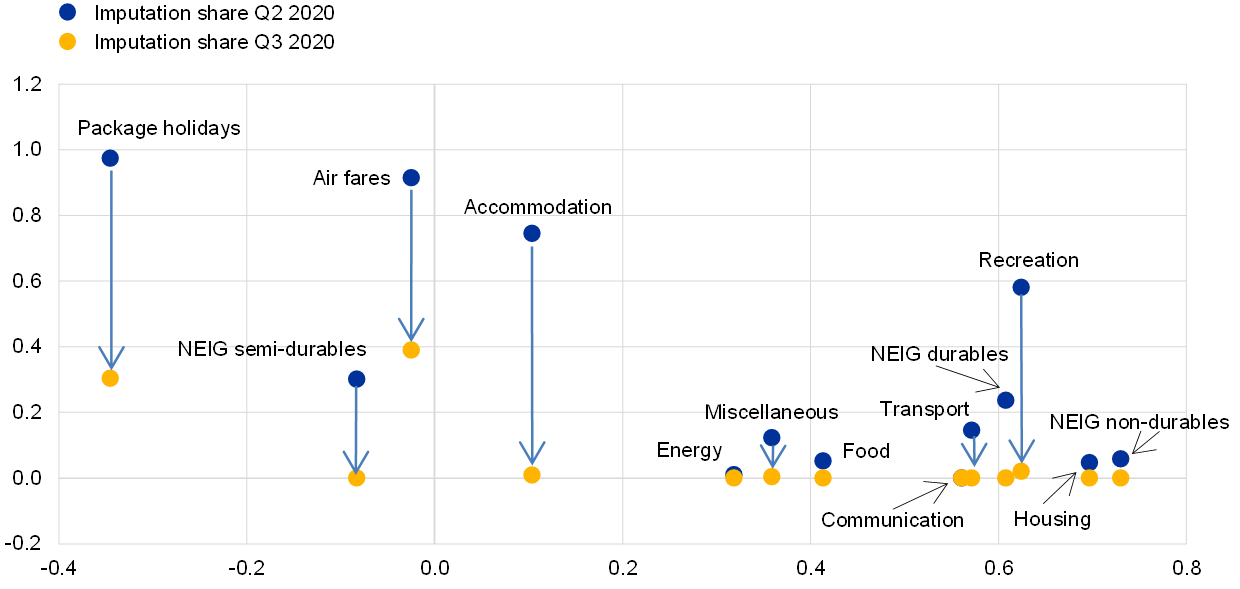

Price imputations are also likely to have imparted some short-lived increase in inflation persistence. Price collection by statisticians faced severe challenges during the lockdown.[18] For example, price collection could not take place in stores that were closed. In addition, sampling in supermarkets and drugstores was largely discontinued in order to protect price collectors. The recreation sector was heavily affected by price imputations, owing to the non-availability of package holidays and the cancellation of entertainment events. Thus, several prices needed to be imputed, sometimes based on the patterns of previous years. This was especially the case for items that typically exhibit relatively low persistence (Chart 3). For example, the share of imputation for air fares jumped in April and remained elevated for some euro area countries until the autumn. The high level of imputations is likely to mean that these published price indices did not fully capture the impact of the severe downturn, but instead generally reflected developments in past data from more normal times. As a result, the overall persistence of inflation during the pandemic may have appeared higher than it actually was for certain components of core inflation, particularly for the second quarter of 2020.[19]

Chart 3

Inflation persistence and price imputations

(x-axis: inflation persistence, sum of autoregressive coefficients; y-axis: imputation share, percentages)

Sources: Eurostat and ECB calculations.

Note: “Transport” excludes air fares and “Recreation” excludes accommodation services and package holidays. The dependent variable is annualised quarter-on-quarter seasonally adjusted inflation, and the number of autoregressive lags is chosen according to the Schwarz Information Criterion. The estimation sample period is from the first quarter of 1999 to the fourth quarter of 2019. The negative inflation persistence estimates for package holidays and air fares may be partly due to the impact of calendar effects. The shares of price imputations were close to zero for all components prior to the second quarter of 2020.

Box 3

Insights from PMI data on pricing by firms during the pandemic[20]

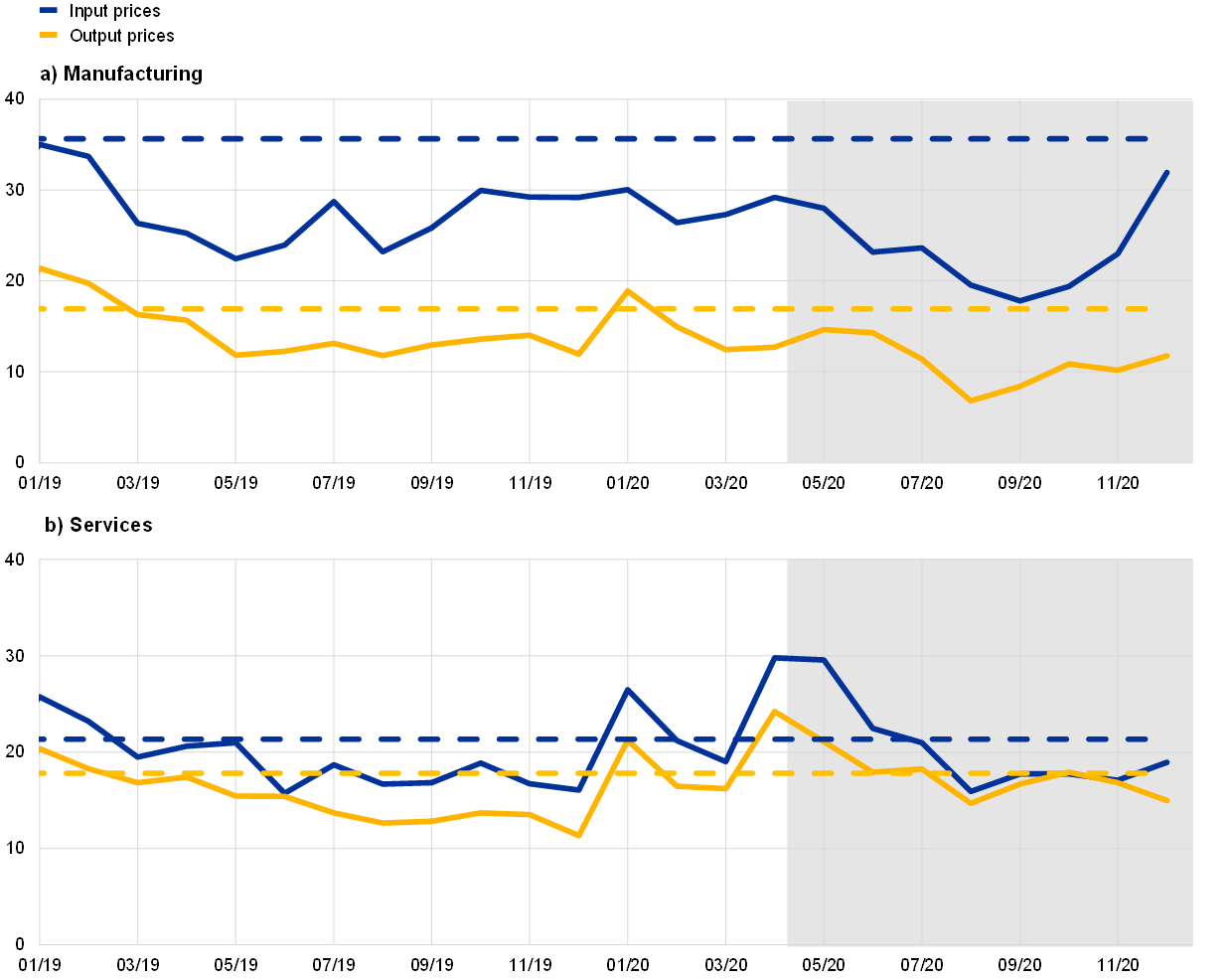

How quickly prices adjust in the face of sharp economic downturns is naturally related to the frequency of price changes. For instance, the avoidance of menu costs implies very infrequent price updates and thus, as a minimum, a delay in price and inflation adjustment to changes in activity developments.[21] In the case of short-lived changes in activity, prices may even remain unchanged throughout. This box uses monthly PMI data for manufacturing and services to gauge the frequency of price changes during the COVID-19 pandemic. For this purpose, the frequency of price changes is defined as the sum of the percentages of PMI survey respondents indicating that prices were “higher” or “lower” than the previous month.[22]

The frequency of output price changes has generally remained unchanged during the pandemic, with the exception of a temporary increase in the services sector during the severe lockdown months of April and May 2020. In the manufacturing sector, the frequency of changes in output prices declined sharply in 2012 and thereafter remained subdued until 2016. This may have been in part due to a lower frequency of changes in input prices, which in turn probably reflected lower volatility in commodity prices, such as oil prices. This also broadly corresponds to a prolonged period of subdued wage growth.[23] Subsequently, the frequency of price changes gradually picked up, before stabilising during 2018. More recently, looking through seasonal variations, the frequency of price changes during the first half of 2020 was broadly comparable to pre-COVID-19 levels (Chart A, upper panel). In the services sector, the frequency of price changes was on a slight downward trend during 2012-2016 and picked up thereafter. Again, this largely reflected trends in the frequency of changes for input prices, where weak developments in wage costs are directly taken into account. The frequency of price changes was somewhat higher during April and May 2020 than their pre-pandemic levels in 2019, and also higher than in the manufacturing sector (Chart A, lower panel).[24]

Overall, the sharp economic downturn does not appear to have been mirrored in a more pronounced frequency of price adjustment. Firms generally did not respond with greater urgency than usual in changing output prices. This may partly reflect the fact that firms update output prices if this is justified by input price changes. It is also worth noting that there is no guarantee that the frequency of changes in factory output prices can be mapped to a corresponding frequency at the level of retail prices.

Chart A

Frequency of price changes for manufacturing and services

(percentages)

Sources: PMI Markit and ECB calculations.

Notes: The latest observation is for December 2020. Dashed lines correspond to historical averages. The shaded regions correspond to the pandemic. The frequency of price changes is defined as the sum of the percentages of PMI survey respondents indicating that prices were “higher” or “lower” than the previous month.

3.3 Lockdown-induced supply effects

Different approaches can be used to assess whether adverse supply effects may have played a role in the response of some components of inflation to the pandemic. All such approaches are subject to caveats and, in the context of the complex nature of the COVID-19 crisis, should be seen as contributing to an approximation of what is going on rather than as conclusive pieces of evidence. One approach used to shed light on the role of demand and supply effects is based on unconditional out-of-sample forecasting exercises.[25] The forecasting errors for the prices and quantities of components for the second and third quarters of 2020 are compared with their respective average historical forecasting errors.[26] A larger than usual positive forecasting error for prices accompanied by a larger than usual negative forecasting error for quantities or vice versa would tentatively point to a more dominant than usual role of supply shocks. This assumes the broad characterisation of a supply shock in the economic literature as a movement of prices and quantities in opposite directions.[27] On that basis, there is some evidence of supply effects in the second quarter of 2020, mainly for food and non-durable goods (Chart 4). At the same time, for some other components where demand fell more than expected (e.g. semi-durables), supply effects cannot be ruled out, as high imputation shares could mask underlying upward movements in inflation. In the third quarter of 2020, any supply effects that existed tended to ease.

Chart 4

Relative forecasting errors for inflation components

(x-axis: quantities, y-axis: prices; forecasting error divided by the average of absolute historical forecasting errors)

Sources: Eurostat and ECB calculations.

Notes: A value greater than one or less than minus one for either prices or quantities implies a larger than usual forecasting error. The forecasting model is a VAR model containing a price and a quantity series (estimated nominal household spending) in log levels at quarterly frequency with four lags and is estimated using Bayesian techniques (the prior is a Normal-Wishart prior with grid search for hyperparameter optimisation, lambda1=0.05, lambda2=1, lambda3=1, lambda4=100, lambda5=0.001 and lambda6 and lambda7=0.01; 2,000 iterations and burn-in of 1,000). “HICPXX” refers to HICPX excluding clothing and footwear and travel-related items. The ECB’s BEAR toolbox Version 4.2 is used (see Dieppe, A., Legrand, R. and van Roye, B., “The BEAR toolbox”, Working Paper Series, No 1934, ECB, July 2016).

A more clear-cut distinction between demand and supply effects ideally relies on a structural identification. Hence, another approach to disentangling demand and supply effects uses conventional VAR models, each containing seven variables: volumes and prices per HICPX component, real GDP, real GDP relative to world real GDP, oil prices, HICP and the short-term interest rate. Five structural drivers are identified: global demand, domestic demand, domestic supply, oil supply and monetary policy. The identification relies on a mix of zero and sign restrictions as informed by theory.[28] The model is estimated using Bayesian techniques.[29] The historical decompositions of the first three quarters of 2020 point to a pervasive and dominant downward impact of both domestic and global demand effects (Chart 5). Furthermore, the decompositions point to a more limited role for adverse supply shocks having an upward impact on inflation even if these were unusually large compared with the typical size of previous supply shocks. These upward supply effects mainly related to certain non-energy industrial goods and miscellaneous services in the second quarter of 2020.[30] Overall, although the two approaches individually come with important caveats and are intended to provide a first-pass assessment, both tend to point to some role for supply effects in explaining the behaviour of inflation during the pandemic, but indicate that demand effects were the dominant factor.

Chart 5

Historical decompositions based on a structural VAR for inflation components for the first to the third quarters of 2020

(percentage point contributions from structural factors to the quarter-on-quarter growth rate of inflation excluding trend, percentage changes)

Sources: Eurostat and ECB calculations.

Notes: “NEIG semi-durables” excludes clothing and footwear, “Transport” excludes air fares and “Recreation” excludes accommodation services and package holidays. The VAR model contains a component price and quantity series in log levels as well as GDP, HICP and oil prices in log levels, euro area GDP relative to rest-of-world GDP, and the short-term interest rate (the euro overnight index average, EONIA). The model is estimated using Bayesian techniques (for more details, see the notes to Chart 4). Zero and sign restrictions are used to identify five structural shocks (domestic demand, domestic supply, global demand, oil supply and monetary policy) based on theory. The ECB’s BEAR toolbox Version 4.2 is used (see Dieppe, Legrand and van Roye, op. cit.).

4 Conclusions

Summing up, a disaggregated perspective can help to better comprehend the response of inflation to the multi-dimensional COVID-19 shock. A disaggregated approach, which goes beyond just analysing the main components of inflation, is particularly suited to current circumstances where past empirical regularities in the interpretation of recent aggregate and core inflation may not apply. By taking a disaggregated approach, the analysis in this article points to a dominant role for downward domestic and global demand effects. This was only partly offset by upward supply effects, which were strongest in the second quarter of 2020 and were more prevalent in goods than in services. Increased use of price imputations, such as for travel-related services, may also help to explain the response of inflation, although these effects appear to have eased, which may partly explain why the decline in inflation gained further momentum during the second half of 2020.

It is likely that a more granular than usual perspective will continue to be needed to assess the evolution of the pandemic and its implications for the drivers of inflation. For monetary policy it is important to identify and look beyond any supply-side effects in order to gain a clearer picture of the disinflationary demand effects that inevitably come with income losses and uncertainty. Moreover, recent research also raised the possibility that supply effects could morph into larger negative demand effects.[31] Given the clear policy relevance of such a scenario, further consideration of this mechanism in the context of the euro area, which partly depends on the degree of its inter-sectoral linkages, would be useful. Finally, although generally weaker, pre-pandemic, non-commodity-related supply effects (e.g. technology shocks) are an ever-present factor in price dynamics. In this regard, the more granular analysis of inflation drivers presented here can also continue to be useful after the pandemic.

- See the article entitled “Measures of underlying inflation for the euro area”, Economic Bulletin, Issue 4, ECB, 2018; Benalal, N., Diaz del Hoyo, J.L., Landau, B., Roma, M. and Skudelny, F., “To aggregate or not to aggregate? Euro area inflation forecasting”, Working Paper Series, No 374, ECB, July 2004; and Chalmovianský, J., Porqueddu, M. and Sokol, A., “Weigh(t)ing the basket: aggregate and component-based inflation forecasts for the euro area”, Working Paper Series, No 2501, ECB, December 2020.

- This complements existing literature that analyses sectoral inflation – see, for example, Imbs, J., Jondeau, E. and Pelgrin, F., “Sectoral Phillips curves and the aggregate Phillips curve”, Journal of Monetary Economics, Vol. 58(4), May 2011, pp. 328-344; Reis, R. and Watson, M.W., “Relative Goods’ Prices, Pure Inflation, and the Phillips Correlation”, American Economic Journal: Macroeconomics, Vol. 2(3), July 2010, pp. 128-157; and Stock, J.H. and Watson, M.W., “Trend, Seasonal, and Sectoral Inflation in the Euro Area”, in Castex, G., Galí, J. and Saravia, D. (eds.), Changing Inflation Dynamics, Evolving Monetary Policy, Central Bank of Chile, 2020, pp. 317-344.

- Indeed, recent evidence on the impact of the initial lockdowns suggests that the associated supply effects may have exerted significant upward pressure on inflation. For the Netherlands and the euro area, see Bonam, D. and Smadu, A., “Supply and demand shocks due to the coronavirus pandemic contribute equally to contraction in production”, DNBulletin, De Nederlandsche Bank, 5 November 2020; for Germany, see Balleer, A., Link., S., Menkhoff, M. and Zorn, P., “Demand or Supply? Price Adjustment during the Covid-19 Pandemic”, Covid Economics, Vetted and Real-Time Papers, Issue 31, Centre for Economic Policy Research, June 2020, pp. 59-102; for the United Kingdom, see Macaulay, A. and Surico, P., “Is the Covid-19 recession caused by supply or demand factors?”, Questions and answers about coronavirus and the UK economy, Economics Observatory, 2020; and for the United States, see Shapiro, A., “A Simple Framework to Monitor Inflation”, Working Papers, No 2020-29, Federal Reserve Bank of San Francisco, August 2020; and Baqaee, D. and Farhi, E., “Supply and Demand in Disaggregated Keynesian Economies with an Application to the Covid-19 Crisis”, NBER Working Papers, No 27152, May 2020.

- See the box entitled “Recent developments in euro area food prices”, Economic Bulletin, Issue 5, ECB, 2020.

- The notion of muted price adjustment relative to activity is confirmed by Purchasing Managers Index (PMI) data for the manufacturing and services sectors. PMI data have the advantage that the price and activity data are from the same source. Moreover, European Commission survey data on 3-month ahead selling price expectations suggest that the PMI survey data do not reflect unexpected developments, but are instead broadly expected at each point in time going forward, i.e. they are part of firms’ price-setting plans.

- As such Phillips curve specifications also include lagged inflation, the forecasts depend to some extent on the starting point. See the article entitled “Drivers of underlying inflation in the euro area over time: a Phillips curve perspective”, Economic Bulletin, Issue 4, ECB, 2019.

- See Coenen, G., Karadi, P., Schmidt, S. and Warne, A., “The New Area-Wide Model II: an extended version of the ECB’s micro-founded model for forecasting and policy analysis with a financial sector”, Working Paper Series, No 2200, ECB, November 2018. The DSGE model is based on the optimisation problems of agents faced with constraints. NAWM II features an elaborated financial sector in which borrowing-constrained banks intermediate funds between the household sector and the goods-producing non-financial sector. Furthermore, the effect on the domestic economy of developments in the global economy is modelled using a stylised external sector. The model is estimated with euro area data. Exogenous shocks drive the business cycle through the imposed structure of the economy, and the drivers behind euro area business cycle and inflation developments can be visualised by looking at the historical shock decomposition.

- Since the estimation of the model covers a long period, including the financial crisis, it may also be well suited to analyse the recent crisis.

- The model features 24 structural shocks. For the sake of simplicity and to facilitate an interpretation of the drivers, the contributions of shocks are bundled in groups. The group “interest rate shocks” comprises shocks which mainly affect short-term and long-term domestic interest rates and domestic lending rates. Shocks to the external sector or to variables directly related to the external sector are collected in “foreign and trade”. Domestic shocks entailing a negative correlation between GDP and inflation are grouped together in “domestic supply”, while remaining shocks with a positive correlation are included in “domestic demand”. The group “other” captures observation errors and errors in bridge equations.

- Technically, the upside pressure on inflation comes mainly from domestic price mark-up shocks which capture the notion of changes in the pricing behaviour of firms.

- See the box entitled “The role of indirect taxes in euro area inflation and its outlook”, Economic Bulletin, Issue 6, ECB, 2020.

- This mechanical estimate assumes a full and immediate pass-through.

- See Kholodilin, K., “Housing Policies Worldwide during Coronavirus Crisis: Challenges and Solutions”, DIW focus, No 2, DIW Berlin, April 2020.

- A higher expenditure share on IT equipment may, however, exert downward pressure on overall inflation, given that inflation for such items tends by nature to be relatively low.

- Shop scanner data are transaction data collected in shops directly at the point of sale (e.g. from supermarket checkouts). Household scanner data are data collected directly from households which record the prices and quantities of goods they purchase.

- In addition to these data sources, microdata collected by national statistical offices for the compilation of the HICP are also available to researchers in several countries but are not published in most countries.

- See Balleer et al., op. cit.

- See the box entitled “Consumption patterns and inflation measurement issues during the COVID-19 pandemic”, Economic Bulletin, Issue 7, ECB, 2020.

- It is worth noting that the pandemic also disproportionately affected the sectors of the economy that tend to show higher persistence (i.e. services rather than goods). This was more marked than, for example, during the global financial crisis.

- Data on the breakdown of responses were provided by PMI Markit. Other data sources point to a quicker reaction of firms’ pricing behaviour.

- As well as menu costs, other factors, including pre-existing supply contracts or a higher priority assigned to maintaining good relationships with business clients, can also play an important role.

- PMI respondents are asked the following: “Is the level of output at your unit (in volume terms) higher, the same or lower than one month ago?”. The focus of the analysis in this box is solely on whether a larger share of firms than usual adjusted their prices. The frequency of price changes is generally not helpful in explaining inflation because the change in the share of firms reporting price increases is normally partly offset by the change in the share of firms reporting price decreases. To determine inflation in a low-inflation environment, the relative shares of upward and downward price adjustments (see Cornille, D. and Dossche, M., “Some Evidence on the Adjustment of Producer Prices”, The Scandinavian Journal of Economics, Vol. 110, No 3, September 2008, pp. 489-518) or information on the average magnitude of price changes (see Gagnon, E., “Price Setting during Low and High Inflation: Evidence from Mexico”, The Quarterly Journal of Economics, Vol. 124, No 3, August 2009, pp. 1221-1263) can be used.

- Wage costs are not taken into account in PMI manufacturing input prices.

- The results are broadly similar across the four largest euro area economies. See also Vermeulen, P., Dias, D.A., Dossche, M., Gautier, E., Hernando, I., Sabbatini, R. and Stahl, H., “Price Setting in the Euro Area: Some Stylized Facts from Individual Producer Price Data”, Journal of Money, Credit and Banking, Vol. 44(8), December 2012, pp. 1631-1650.

- A vector autoregressive (VAR) model is used to produce forecasts for the first, second and third quarters of 2020, taking into account the joint dynamics of the prices and quantities of components prior to the pandemic.

- For more details on the quantity series, see Table A in the box entitled “Consumption patterns and inflation measurement issues during the COVID-19 pandemic”, Economic Bulletin, Issue 7, ECB, 2020.

- See also Shapiro, A., “A Simple Framework to Monitor Inflation”, Working Papers, No 2020-29, Federal Reserve Bank of San Francisco, August 2020.

- The identification scheme used is based on elements of Corsetti, G., Dedola, L. and Leduc, S., “The international dimension of productivity and demand shocks in the US economy”, Journal of the European Economic Association, Vol. 12(1), February 2014, pp. 153-176; and Bobeica, E. and Jarociński, M., “Missing disinflation and missing inflation: the puzzles that aren't”, Working Paper Series, No 2000, ECB, January 2017.

- See Lenza, M. and Primiceri, G., “How to estimate a VAR after March 2020”, Working Paper Series, No 2461, ECB, August 2020. In order to allay concerns about the unprecedented variation in parameter estimates, a pre-pandemic sample from the second quarter of 2002 to the fourth quarter of 2019 is used to provide historical decompositions for the first to the third quarters of 2020.

- It is worth noting that the positive contributions from “Other” in the second quarter for several components, including travel-related and recreational services, may partly reflect the distortionary impact of the increased use of price imputations.

- For example, for the United States, see Guerrieri, V., Lorenzoni, G., Straub, L. and Werning, I., “Macroeconomic Implications of COVID-19: Can Negative Supply Shocks Cause Demand Shortages?”, NBER Working Papers, No 26918, April 2020; and Cesa-Bianchi, A. and Ferrero, A., “The Transmission of Keynesian Supply Shocks”, 20 October 2020.