19 June 2020

RESEARCH BULLETIN NO. 72

The Global Weakness Index – reading the economy’s vital signs during the COVID-19 crisis

The Global Weakness Index (GWI) is a real-time measure of how weak the global economy is. We use this index to assess on the spot how the repercussions of the coronavirus (COVID-19) crisis are playing out. After the release of certain soft indicators on 2 March 2020 the GWI increased sharply – much faster than in the 2008 crisis. And at the time of writing it remains at a record high.

Introduction

The COVID-19 crisis has once again shown how important it is to be able to assess economic conditions in real time. Although it has been clear since early March that some economies are sliding into recession, until very recently the standard measures – based on low-frequency indicators with publication delays – were silent about the increasing probability of recession in most advanced and emerging economies.

In order to solve this problem, various researchers have developed non-linear models based on several timely indicators. Unlike many other models, the Markov-switching dynamic factor (MSDF) models introduced by Chauvet (1998) have been successfully used to account for co-movements and non-linearities across several economic indicators. These models have widely shown their ability to identify turning points fast.

In MSDF models, the economy is assumed to switch between expansions and recessions with constant probabilities. Expansions and recessions are respectively characterised by high and low growth rates of the various activity indicators. Conditional on being in each state, the indicators, including GDP, move around these high/low growth rates[2]. Following Hamilton (1989), previous MSDF models have assumed that these two growth rates are the same for all the expansions and recessions in the sample.

This article explains how Leiva-Leon, Perez-Quiros and Rots (2020) estimate such a model using timely indicators but considering that recessions might differ in depth. To allow for this possibility has two advantages. First, allowing for the mean to vary across recessions is helpful because, once an economy has suffered a “severe” recession, such as the Global Financial Crisis, the model might not be able to identify an upcoming “mild” recession. This lack of sensitivity of the model comes from the fact that the estimated growth rate of recessions might be too low to capture “mild” recession periods. Second, as the growth rate of every recession is different, the model delivers real-time estimates of the depth of every recession, which provides valuable information to rapidly design and implement the necessary policy responses. This is especially important in the deep COVID-19 recession that we are currently experiencing.

Data, sample and technical features of the models

An MSDF with recessions of varying depth is estimated independently for twelve of the largest economic regions of the world, which together account for more than seventy percent of world GDP. Six are advanced and six are emerging economies:

Table A

Economies

We use supply-side variables (usually, industrial production), internal demand variables (imports or sales), external demand (exports) as well as one additional variable, specific to each economy, usually a soft indicator such as the PMI. All of these variables are monthly. In addition, the models contain GDP as a quarterly variable.[3]

The main advantage of relying exclusively on real variables is that we capture all types of recessions, whether they originate in the financial sector, energy prices, a pandemic or any other cause. Whatever is its origin, as long as there is an effect on the economy, the effect will be reflected in these variables.

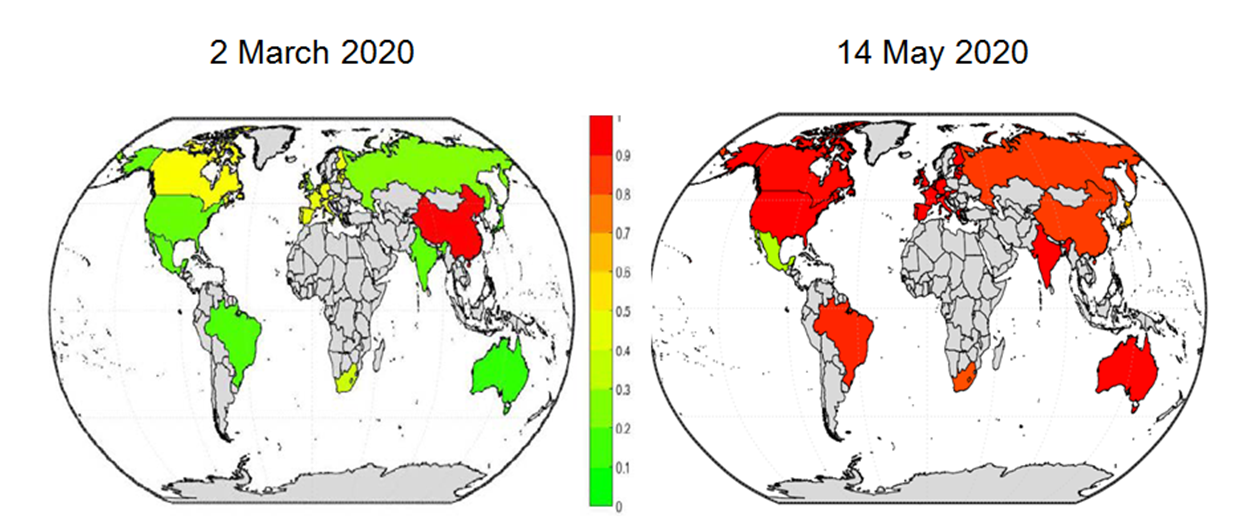

For every economy, both the probabilities of recessions and the depth of every recession are endogenously estimated. No external dating is used. Chart 1 plots recession probabilities for the different regions in 2 March 2020, the first day in which the model captured a serious increase in global weakness, and in 14 May 2020, the day of the writing of this article.

Chart 1

Recession probabilities across countries

Note: The heatmap of the world plots the overall pattern of the probabilities of the low economic activity regime for specific dates. The darker (lighter) the area, the higher (lower) the probability of recession. The animated sequence of world heatmaps, from April 2003 until February 2020 can be found at: https://sites.google.com/site/daniloleivaleon/global_weakness

Global Weakness Index

The information contained in Chart 1 can be summarised in an index – the Global Weakness Index (GWI). It is a weighted average of the probabilities of recession in different economies[4]. The weights depend on the GDP of each region in every quarter. Chart 2 plots the GWI computed on the same dates shown in Chart 1. As the chart shows, there is a sharp increase as early as March 2, which is confirmed by the latest numbers of May 14, where the GWI ends up close to 1. The index can be interpreted as the proportion of the world economy that is currently in recession.

Chart 2

Global Weakness Index

Note: The figure shows the Global Weakness Index, which is constructed as a weighted average of the probabilities of the low economic activity regime across economies. It is weighted by the size of the corresponding economies. The red area represents the credible set based on the 16th and 84th percentiles of the posterior distribution.

Given that the index is computed as a weighted average of the individual economies, it can be broken down by the individual contributors. Each economy’s contribution depends on the weight of that economy in world GDP and the probability of that economy being in a recession. The contribution of the different economic areas can be seen in Chart 3. It shows that, at the beginning of March, only China was clearly in a recession, but recently the United States and the euro area have also been large contributors to the high level of the index.

Chart 3

Contributors to the GWI

Note: The radar chart shows the relative contribution of each economy to the GWI. The contributions are normalised to sum up to one.

All in all, the GWI as an indicator has four key benefits. It is (i) updatable in real time; (ii) broken down by regional contributions; (iii) useful for quantifying risks; and (iv) simple to interpret.

Extensions

Our model includes GDP as one of its indicators, so it can be used to provide forecasts for GDP. As a matter of fact, computing the probability of negative growth or two quarters of negative growth, i.e. the probability of a recession according to its classical definition, is quite straightforward. In the case of the euro area, the latest figures suggest that the probability of a classical recession has reached 100%.

Conclusions

We present a new indicator of global economic weakness which uses real-time information available to estimate the proportion of the world economy that is in a recession. The indicator is based on the estimation of a dynamic non-linear factor model for individual economies which considers recessions of different depths. Leiva-Leon et al (2020) show the excellent real-time forecasting properties of this model for individual economies.

As this article illustrates, the indicator already pointed to clear signs of economic weakness as early as 2 March 2020. This weakness was confirmed by official statistics on 4 May 2020, when Q1 GDP data for most countries were released. Therefore this indicator helps provide early warnings of a downturn that can be crucial for a fast policy response.

References

Camacho, M., Perez-Quiros, G. and P. Poncela (2018). "Markov-switching dynamic factor models in real time", International Journal of Forecasting, Elsevier, vol. 34(4), pp. 598-611.

Chauvet, M. (1998). An econometric characterization of business cycle dynamics with factor structure and regime switches. International Economic Review 39 (4), 969-996.

Chauvet, M. and J. A. Piger (2008). “A comparison of the real-time performance of business cycle dating methods”, Journal of Business and Economic Statistics, vol. 26, pp. 42-49.

Hamilton, J. (1989). “A new approach to the economic analysis of nonstationary time series and the business cycles”, Econometrica, vol. 57, pp. 357-384.

Leiva-Leon, D., Perez-Quiros, G. and Rots, E. (2020). “Real-time weakness of the global economy: a first assessment of the coronavirus crisis” ECB Working Paper 2381 March 2020.

- The article was written by Danilo Leiva-Leon (Banco de España), Gabriel Perez-Quiros (Monetary Policy Research Division, European Central Bank) and Eyno Rots (Magyar Nemzeti Bank). It is based on their ECB Working Paper no. 2381 “Real-time weakness of the global economy: a first assessment of the coronavirus crisis”. The authors gratefully acknowledge the comments of Michael Ehrmann, Alberto Martin, Zoë Sprokel and the excellent research assistance of Romain Aumond. The views expressed here are those of the authors and do not necessarily represent the views of the Banco de España, the European Central Bank, the Magyar Nemzeti Bank or the Eurosystem.

- Indicators are transformed to be stationary. Depending on the indicators, they are used in growth rates, first differences or levels. GDP is included in growth rates but, given that the model is constructed in monthly frequencies, its relation to the factor is a weighted moving average of monthly activity.

- This choice follows the original approach of Stock and Watson (1991), Chauvet and Piger (2008) or Camacho et al. (2018). Those papers show that such a small set of variables reliably captures current conditions of the economy and comprises most of the information relevant for inferring recessions in real time.

- Technically, the researchers weight the individual draws obtained by Bayesian methods in each country. Therefore, they produce the density function of the distribution of GWI in every time period.