- PRESS RELEASE

- 29 April 2019

Euro area economic and financial developments by institutional sector: fourth quarter of 2018

- Euro area net saving increased to €797 billion in the four quarters to the fourth quarter of 2018, compared with €788 billion in the four quarters to the previous quarter. Euro area net non-financial investment increased to €478 billion (from €433 billion previously), owing to increased investments by households and non-financial corporations. Euro area net lending to the rest of the world decreased to €329 billion (from €363 billion previously).

- Household debt was lower at the end of the fourth quarter of 2018 compared with a year earlier, in relation to both GDP and gross disposable income (the corresponding ratios decreased to 57.9% and to 93.5%, from 58.2% and to 94.0% respectively). Non-financial corporation debt decreased to 136.2% of GDP, from 136.9% one year earlier.

- This release presents financial transactions (flows) and assets and liabilities (stocks) for deposits, loans, debt securities, listed shares and investment fund shares, with a counterpart sector breakdown. The corresponding charts (see Charts 2 and 3) show that most financial assets of households are liabilities of financial intermediaries, which in turn provide most of the financing to non-financial corporations. The developments of the financial links between the resident sectors, and with the rest of the world can be analysed using the underlying time series.

Total euro area economy

Euro area net saving increased to €797 billion (8.5% of euro area net disposable income) in the four quarters to the fourth quarter of 2018, compared with €788 billion in the four quarters to the previous quarter. Euro area net non-financial investment increased to €478 billion (5.1% of net disposable income), owing to increased investments by households and non-financial corporations.

Euro area net lending to the rest of the world decreased to €329 billion (from €363 billion previously) reflecting the increased net non-financial investment. Net lending by non-financial corporations decreased from €133 billion to €87 billion (0.9% of net disposable income) while net lending by financial corporations increased from €71 billion to €95 billion (1.0% of net disposable income). Net lending by households was broadly stable at €212 billion (2.2% of net disposable income). The decrease in net lending by the private sector as a whole was amplified by an increase in net borrowing by the government sector (-0.7% of net disposable income, compared with -0.5% in the four quarters to the previous quarter).

Chart 1. Euro area saving, investment and net lending to the rest of the world

(EUR billions, four-quarter sums) * Net saving minus net capital transfers to the rest of the world (equals the change in net worth due to transactions).

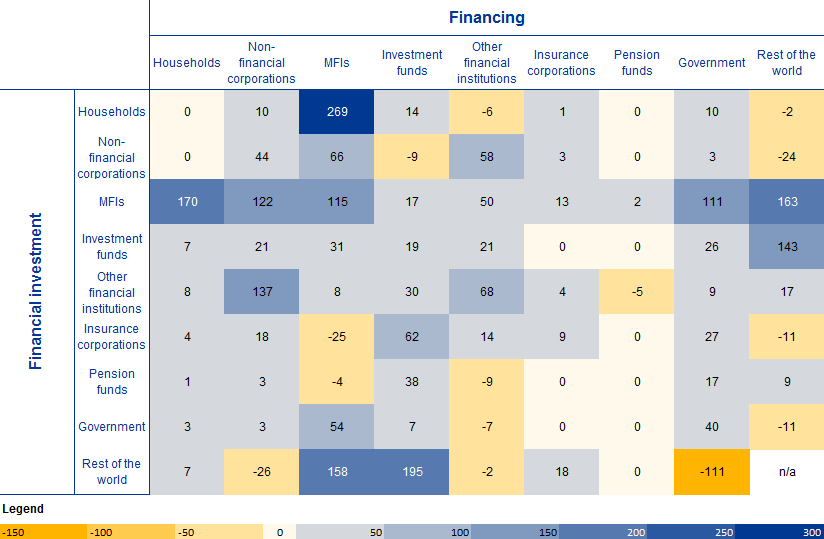

Financial transactions can be presented with a counterpart sector breakdown for deposits, loans, debt securities, listed shares and investment fund shares (see Table 1). In 2018 the largest transactions in these financial instruments within the euro area were financial investments by households with MFIs[1] (€269 billion), mostly in the form of deposits, and financing received from MFIs by households (€170 billion) in the form of loans. Financial transactions with the rest of the world were largest for financial investments of the rest of the world with euro area investment funds (€195 billion), and financial investments by MFIs with the rest of the world (€163 billion).

Table 1. Selected financial transactions* between sectors and with the rest of the world

(EUR billions, four-quarter sums, 2018) * Financial instruments for which the counterpart sector breakdown is available: deposits, loans, debt securities, listed shares and investment fund shares/units.

Households

The annual growth rate of household financial investment was unchanged in the fourth quarter of 2018 at 2.0%. Accelerating investment in currency and deposits, and decelerating investment in investment fund shares were the main factors (see Table 2).

Households were net buyers of listed shares. By issuing sector, they were net buyers of listed shares of non-financial corporations, insurance corporations and the rest of the world (shares issued by non-residents), while they were marginally net sellers of listed shares of MFIs and other financial institutions (except insurance corporations). Households continued to sell debt securities (in net terms) issued by MFIs and other financial institutions, while they were net buyers of debt securities issued by government and the rest of the world (see Table 2.2. in the Annex).

Table 2. Financial investments and financing of households, main items

(annual growth rates)

Financial transactions |

|||||

Q4 2017 |

Q1 2018 |

Q2 2018 |

Q3 2018 |

Q4 2018 |

|

Financial investment* |

2.1 |

2.0 |

2.0 |

2.0 |

2.0 |

Currency and deposits |

3.3 |

3.3 |

3.8 |

3.8 |

4.1 |

Debt securities |

-12.6 |

-13.3 |

-9.3 |

-5.3 |

-3.8 |

Shares and other equity |

1.9 |

2.1 |

1.1 |

0.5 |

0.4 |

Investment fund shares |

7.3 |

6.1 |

3.5 |

2.4 |

0.3 |

Life insurance and pension schemes |

2.2 |

2.2 |

2.2 |

2.2 |

2.0 |

Financing** |

3.3 |

2.9 |

3.1 |

2.9 |

3.2 |

Loans |

2.9 |

3.0 |

3.0 |

3.1 |

3.1 |

* Items not shown include: loans granted, prepayments of insurance premiums and reserves for outstanding claims and other accounts receivable.** Items not shown include: financial derivative's net liabilities, pension schemes and other accounts payable.

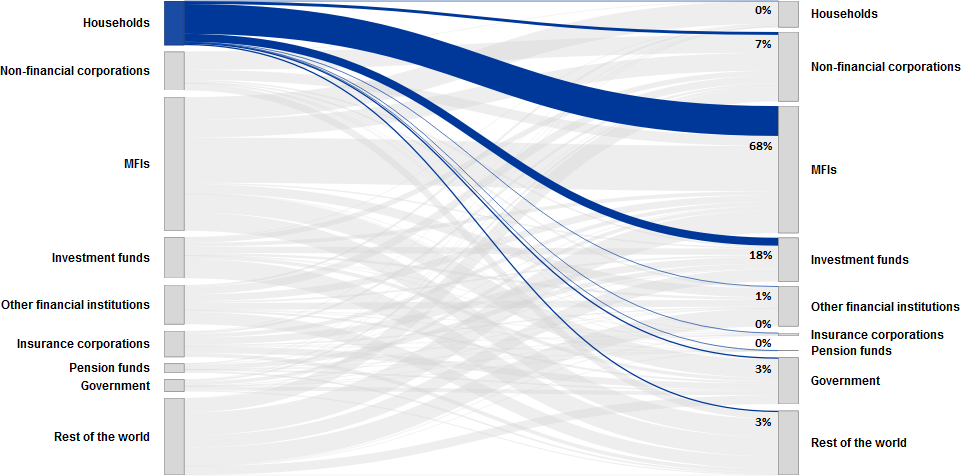

Chart 2 below shows the stock of selected households’ financial assets (in dark blue) vis-à-vis counterpart sectors. At the end of 2018, households’ financial assets in the financial instruments with a counterpart sector breakdown were mostly liabilities of financial intermediaries such as MFIs (68% of outstanding amounts) and investment funds (18%).[2] Direct holdings of financial assets issued by non-financial corporations (7%), government (3%) and the rest of the world (3%), e.g. in the form of listed shares and debt securities, represented much lower shares of households’ financial assets.

Chart 2. Households’ financial assets by counterpart sector; selected financial instruments*

(EUR billions, 2018 end of period stocks) * Financial instruments for which the counterpart sector breakdown is available: deposits, loans, debt securities, listed shares and investment fund shares/units.

The household debt-to-income ratio[3] continued to decrease in the fourth quarter of 2018, to 93.5% from 94.0% in the fourth quarter of 2017, as disposable income grew faster than the outstanding amount of loans to households. Similarly, the household debt-to-GDP ratio decreased to 57.9% in the fourth quarter of 2018, from 58.2% in the fourth quarter of 2017.

Non-financial corporations

In the fourth quarter of 2018 the annual growth rate of financing of non-financial corporations declined to 1.4%, from 1.7% in the previous quarter, mainly owing to the deceleration in the growth of financing by debt securities, loans and trade credits (see Table 3 below). The annual growth rate of loan financing decreased to 2.2% from 2.7% previously, as the growth of loans granted by MFIs and between non-financial corporations decelerated, which was partially offset by an increase in loans from non-MFI financial institutions and the rest of the world (see Table 3.2. in the Annex).[4]

Table 3. Financial investments and financing of non-financial corporations, main items

(annual growth rates)

Financial transactions |

|||||

Q4 2017 |

Q1 2018 |

Q2 2018 |

Q3 2018 |

Q4 2018 |

|

Financing* |

2.3 |

1.8 |

1.9 |

1.7 |

1.4 |

Debt securities |

5.5 |

5.5 |

5.4 |

5.7 |

4.3 |

Loans |

2.6 |

2.3 |

2.5 |

2.7 |

2.2 |

Shares and other equity |

1.2 |

1.2 |

1.0 |

0.8 |

0.9 |

Trade credits and advances |

8.1 |

5.5 |

6.2 |

4.9 |

3.1 |

Financial investment** |

3.8 |

3.1 |

3.2 |

2.9 |

2.2 |

Currency and deposits |

7.4 |

4.6 |

5.6 |

4.9 |

3.7 |

Debt securities |

-4.1 |

-12.1 |

-6.3 |

-7.8 |

-1.0 |

Loans |

4.1 |

3.7 |

2.4 |

2.2 |

-0.1 |

Shares and other equity |

1.3 |

1.7 |

1.8 |

2.0 |

2.1 |

* Items not shown include: pension schemes, other accounts payable, financial derivative's net liabilities and deposits.** Items not shown include: other accounts receivable and prepayments of insurance premiums and reserves for outstanding claims.

Non-financial corporations' debt-to-GDP ratio decreased to 136.2% in the fourth quarter of 2018, from 136.9% in the fourth quarter of 2017.

Chart 3 below shows non-financial corporations’ debt (in dark blue) vis-à-vis counterpart sectors. At the end of 2018, non-financial corporations’ debt in the form of loans and debt securities was held primarily by MFIs (37%), other non-financial corporations (27%), the rest of the world (15%) and other financial institutions (13%).

Chart 3. The main components of NFC debt (loans and debt securities) by counterpart sector

(EUR billions, 2018 end of period stocks)

Annexes

For media queries, please contact Stefan Ruhkamp, tel.: +49 69 1344 5057.

Notes

- These data come from a second release of quarterly euro area sector accounts from the European Central Bank (ECB) and Eurostat, the statistical office of the European Union. This release incorporates revisions compared with the first quarterly release and provides data for all sectors, thus completing the data on euro area households and non-financial corporations released on 4 April 2019. The financial transactions, assets and debt data by counterpart sector (also referred to as who-to-whom data) presented in this release are available for deposits, loans, debt securities, listed shares and investment fund shares/units and are shown in the press release published at the end of April each year.

- The debt-to-GDP (or debt-to-income) ratios are calculated as the outstanding amount of debt in the reference quarter divided by the sum of GDP (or income) in the four quarters to the reference quarter. The ratio of non-financial transactions (e.g. savings) as a percentage of income or GDP is calculated as the sum of the four quarters to the reference quarter for both numerator and denominator.

- The annual growth rate of non-financial transactions and of outstanding assets and liabilities (stocks) is calculated as the percentage change between the value for a given quarter and that value recorded four quarters earlier. The annual growth rates used for financial transactions refer to the total value of transactions during the year in relation to the outstanding stock a year before.

- The next release of the ECB’s Household sector report containing results for the euro area and all EU countries is scheduled for 13 May 2019.

- Hyperlinks in the main body of the press release lead to data that may change with subsequent releases as a result of revisions. Figures shown in tables and charts contained within annexes are a snapshot of the data as at the time of the current release.

- [1]In addition to banks and money market funds, the MFI sector also covers the Eurosystem.

- [2]This excludes relevant financial instruments such as unlisted shares, other equity, life insurance and annuity entitlements, pension schemes and other accounts payable for which the counterpart sector breakdown is not available.

- [3]This is calculated as loans divided by gross disposable income.

- [4]Loan financing comprises loans granted by all euro area sectors (in particular MFIs, non-monetary financial institutions and other non-financial corporations) and by creditors that are not resident in the euro area.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts