- SPEECH

Disinflation in the euro area

Speech by Philip R. Lane, member of the Executive Board of the ECB, Hutchins Center on Fiscal & Monetary Policy at the Brookings Institution

Washington, D.C., 8 February 2024

Today, I wish to report on the progress in disinflation in the euro area.

Chart 1 shows the dynamics of headline and core inflation, extended forward through 2026 on the basis of the December 2023 Eurosystem staff projections.[1] Relative to its pandemic low point in late 2020, inflation started to increase in early 2021, rising above the two percent medium-term target in July 2021. Inflation continued to climb through the rest of 2021 and most of 2022, peaking at 10.6 percent in October 2022. Since late 2022, inflation has declined and stood at 2.8 per cent in January 2024. According to the December 2023 Eurosystem staff projections, inflation is expected to stabilise around the two per cent target from about the middle of 2025 onwards.

Chart 1

Headline inflation, core inflation and Eurosystem staff macroeconomic projections

(annual percentage changes)

Sources: Eurostat and Eurosystem staff macroeconomic projections.

Notes: HICP refers to headline inflation and HICPX to HICP excluding food and energy. Realised HICP and HICPX are at a monthly frequency, and HICP and HICPX projections are at a quarterly frequency. The latest observations for realised HICP and HICPX are for January 2024 (flash).

The main factors in the 2021-2022 inflation surge were the direct and indirect effects of the energy shock, together with a set of pandemic-related factors including supply chain bottlenecks and, during 2022, the Russian invasion of Ukraine and demand-supply mismatches associated with the reopening of the contact-intensive service sectors (Chart 2).

By the time headline inflation peaked at 10.6 per cent in October 2022, energy inflation had reached 41.5 per cent. Since then, energy inflation has not only stabilised but turned negative: in January 2024, it stood at -6.3 per cent. The energy shock also contributed to very high food inflation: at 5.7 per cent in January, food inflation has come down substantially from its peak of 15.5 per cent in March 2023 but remains elevated. Core inflation was 3.3 per cent in January, down from the 5.7 per cent peak also in March 2023. The decline in goods inflation has been the main driver in core disinflation, with goods inflation standing at 2.0 per cent in January, down from 6.8 per cent in February 2023. Inflation in the services sector stands at 4.0 per cent, having eased less so far than the other components; its peak was 5.6 per cent in July 2023.

Chart 2

Inflation developments and December 2023 Eurosystem staff macroeconomic projections

(annual percentage changes, percentage point contributions) | |

|---|---|

|  |

Sources: Eurostat, December 2023 Eurosystem staff projections and ECB calculations.

Note: The latest observations are for January 2024 (flash).

Overall, the strong disinflation over the past year largely reflects the unwinding in energy inflation (which, in turn, partly reflects large base effects), which explains about half of the disinflation (Chart 3). In addition, the ongoing easing of pipeline pressures and the relaxation of supply bottlenecks have supported the disinflation in the other HICP components. Monetary policy tightening has contributed to the disinflation process by dampening demand and anchoring medium-term inflation expectations at our two per cent target.

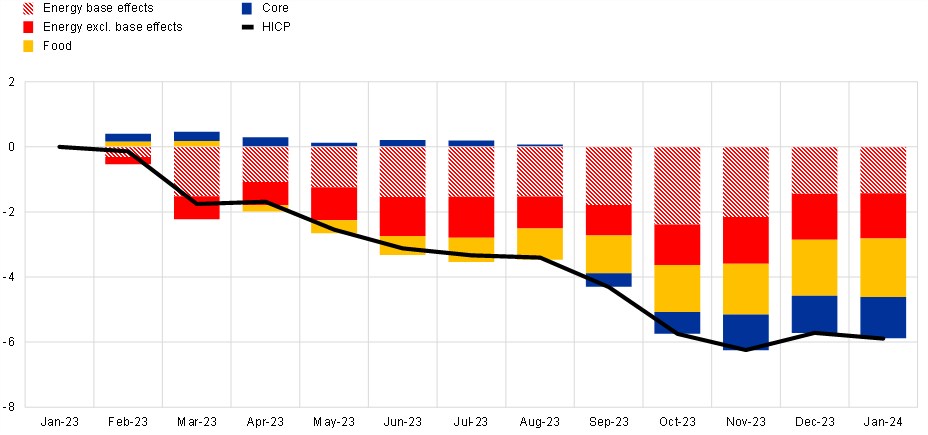

Chart 3

Headline inflation vis-à-vis January 2023

(percentage points)

Sources: Eurostat and ECB calculations.

Notes: The notion of base effects is explained, inter alia, in the ECB Economic Bulletin box entitled “Recent dynamics in energy inflation: the role of base effects and taxes”. The latest observation is for January 2024 (flash).

While the December 2022 projections had foreseen considerable disinflation during the course of 2023, the realised pace of disinflation has exceeded these estimates (Chart1). Energy prices not only stabilised but fell considerably in the course of 2023 (Chart 4), including due to the impact of global monetary tightening on world activity levels and commodity prices.

Chart 4

Oil and gas prices

Sources: LSEG, ECB staff calculations and Eurosystem/ECB staff projections.

Note: The latest observations are for 6 February 2024.

The downward revisions to 2023-2024 growth reflected unexpectedly-weak global demand for European exports and the under-estimation of the adverse impact of the 2021-2022 decline in real incomes and the terms of trade on consumption and investment dynamics. In addition, the scale of deceleration in credit dynamics was underestimated.

During the disinflation process, forecast errors have been small, and even turned negative in recent times (Chart 5 and Chart 6). This stands in contrast to the inflation surge period, which triggered substantial one-quarter ahead forecast errors in September 2021 ECB staff macroeconomic projections and the following rounds.[2]

Chart 5

One-quarter ahead HICP forecast errors – comparison with other forecasters

(percentage points)

|

Sources: Eurosystem/ECB staff projections, Consensus Economics, Survey of Monetary Analysts (SMA), European Commission, OECD and Eurostat.

Notes: See also Chahad, M., Hofmann-Drahonsky, A.-C., Page, A. and Tirpák, M. (2023), “An updated assessment of short-term inflation projections by Eurosystem and ECB staff”, Economic Bulletin, Issue 1/2023, ECB. For other forecasters, the errors are shown for publications where the corresponding cut-off date is closest to that of the Eurosystem/ECB staff projections. For the SMA, the median of survey respondents is shown. The arrows indicate differences in the months of available HICP data at the cut-off point for each publication relative to the Eurosystem/ECB staff projections. An upward arrow indicates one additional month of data, a downward arrow indicates one month less data, and two downward arrows indicate two months less data. Quarterly projections from the OECD are only available twice per year and therefore no error is shown in the first and third quarters. Notes on errors for third and fourth quarters of 2023: The European Commission did not publish quarterly forecasts in its Summer 2023 forecast, so no errors are depicted in the chart. The cut-off date for the Eurosystem/ECB staff projections was 30 August 2023. Although this was one day before the publication of the euro area HICP flash estimate for August 2023, flash releases for five euro area countries (covering 45% of the euro area HICP) were included implying no deviation from the Eurostat release for headline HICP.

Chart 6

Decomposition of recent one-quarter-ahead HICP inflation errors in the Eurosystem/ECB staff projections

(percentage points)

|

Source: ECB calculations.

Notes: See also Chahad, M., Hofmann-Drahonsky, A.-C., Page, A. and Tirpák, M. (2023), “An updated assessment of short-term inflation projections by Eurosystem and ECB staff”, Economic Bulletin, Issue 1/2023, ECB. “Total error” is the outturn minus the projection. “Indirect impact of energy prices on non-energy inflation” is the sum of the indirect effects of oil, gas and electricity prices. (For oil, these are based on the elasticities derived from the Eurosystem staff macroeconomic models, and for gas and electricity these are computed assuming an elasticity proportional to the oil price shock.) “Impact of non-energy related assumptions” represents the assumptions for short and long-term interest rates, stock market prices, foreign demand, competitors’ export prices, food prices and the exchange rate.

Charts 7 and 8 compare the current inflation episode in the euro area to a sample of past episodes.[3] The scale of the inflation shock to headline exceeds previous episodes, which reflects not only the energy shock but also the preceding rebound from the very low inflation during the initial months of the pandemic. The disinflation of headline inflation so far is proceeding in a fairly symmetrical fashion. However, core inflation measures have peaked later and remain at relatively high levels from a historical perspective. This is driven primarily by the dynamics of services inflation, whereas goods inflation has already come down more decisively. Amongst other factors, the adjustment of the services sector to rising energy costs and the impact of the price level shock on subsequent nominal wage dynamics is necessarily a gradual process, especially in view of the staggered nature of the wage setting process in European labour markets. In addition, the pandemic reopening effect was still supporting unusually high pricing power in contact-intensive services sectors through the summer of 2023.

Chart 7

Historical inflation and the recent inflation episode in the euro area – headline and core inflation rates

Headline inflation | Core inflation |

|---|---|

(percentage points) | (percentage points) |

|  |

Sources: BIS, Eurostat, and ECB calculations.

Notes: The shaded areas and the orange and yellow lines represent respectively the interquartile range and the median of national headline and core inflation series relative to their peaks during disinflation episodes before 2022 across a panel of 30 advanced economies and 28 emerging market economies. Month = 0 when the headline inflation rate is at its highest during that particular episode. The dark blue line represents the latest developments in headline and core inflation for the euro area, relative to the October 2022 peak. The latest observations are for January 2024.

Chart 8

Historical inflation and the recent inflation episode in the euro area – goods and services inflation rates

Non-energy industrial goods inflation | Services inflation |

|---|---|

(percentage points) | (percentage points) |

|  |

Sources: BIS, Eurostat, and ECB calculations.

Notes: The shaded areas and the blue and green lines represent respectively the interquartile range and the median of national NEIG and services inflation series relative to their peaks during disinflation episodes before 2022. Non-energy industrial goods inflation refers to a panel of all euro area countries, while services inflation refers to a panel of 30 advanced economies and 28 emerging market economies. Month = 0 when the headline inflation rate is at its highest during that particular episode. The dark blue line represents the latest developments in non-energy industrial goods and services inflation for the euro area, relative to the October 2022 peak. The latest observations are for January 2024.

In the December 2023 Eurosystem staff macroeconomic projections, HICP inflation is projected to decrease from an average of 5.4 per cent in 2023 to 2.7 per cent in 2024 and 2.1 per cent in 2025, and then to stand at 1.9 per cent in 2026 (Chart 1). In 2024, energy inflation should increase as base effects turn positive and some fiscal support measures are scheduled to be discontinued. This is expected to partly offset further declines in food inflation and HICP inflation excluding energy and food (HICPX), implying that headline inflation will fall only gradually in the course of 2024. From the end of 2024, all the main inflation components are expected to continue to ease, supporting headline HICP inflation in reaching the ECB’s target in the second half of 2025.

Inflation could decline more quickly in the near term if energy prices evolve in line with the recent downward shift in market expectations for the future path for oil and gas prices (Chart 4). This is recognised in the risk assessment of the January ECB monetary policy statement. It is also reflected in the Consensus expectations of external experts, which are below the December 2023 Eurosystem staff projections in the near term (Chart 9). Work by ECB staff (Lenza et al. (2023) – using a machine‑learning approach with about 60 variables, weighted according to their track record – also points to the possibility of outturns below the December projections.[4] That said, it is worth emphasising that the confidence bands associated with the analysis are very wide, which cautions against putting too much weight on the centre of the distribution.

Chart 9

Short-term forecasts

(annual percentage changes) | |

|---|---|

|  |

Sources: Eurostat, December 2023 Eurosystem staff projections, Consensus Economics and ECB calculations.

Notes: Cut-off date for the random forest is 1 February 2024. Consensus Economics data were collected on 8 January 2024. Random forest estimates are from Lenza, M., Moutachaker, I. and Paredes, J. (2023), “Forecasting euro area inflation with machine learning models”, Research Bulletin, No 112, ECB and Lenza, M., Moutachaker, I. and Paredes, J. (2023), “Density forecasts of inflation: a quantile regression forest approach”, Working Paper Series, No 2830, ECB. The shadowed area shows the 5-95th confidence interval of the regression forest forecast. The latest observations are for January 2024 (flash).

The broad range of underlying inflation measures have come down substantially from their peaks and also fell in December, reflecting the fading impact of past shocks and weaker demand, including due to the ongoing strong transmission of tighter monetary policy (Chart 10).[5] However, while at a general level, measures of underlying inflation are meant to capture the persistent component of inflation and therefore send signals about medium-term inflation, the relative price shocks that have been triggered by the scale and breadth of the energy shock and the pandemic- and war-related shocks mean that standard measures of contemporaneous underlying inflation may, in fact, not send reliable signals about medium-term inflation dynamics.

Making an adjustment for the impact of energy costs and supply bottlenecks on core inflation deliver measures that peaked at lower levels.[6] The difference between the adjusted and standards measures of underlying inflation suggests that the temporary factors amounted to at least two and a half percentage points at the peak. There is still around one per cent of temporary factors in the unadjusted measures as of now, but the difference is fading out gradually. In addition, this adjustment technique does not correct for the additional pricing power of firms in contact-intensive services during the pandemic reopening phase. To the extent that this effect is also fading out, further deceleration in underlying inflation can be expected.

Chart 10

Measures of underlying inflation

(annual percentage changes)

Sources: Eurostat and ECB staff calculations. Notes: “PCCI” stands for “persistent and common component of inflation”. The ‘adjusted’ measures abstract from energy and supply-bottleneck shocks using a large SVAR, see Bańbura, Bobeica and Martínez-Hernández, (2023), “What drives core inflation? The role of supply shocks”, ”, Working Paper Series, No 2875, ECB), deducted mechanically from each measure. The latest observations are for January 2024 (flash) for HICP excluding energy, HICP excluding energy and food, and HICP excluding energy and unprocessed food in the left panel, December 2023 for the rest.

Chart 11

Momentum of inflation and its components

(annualised three-month-on-three-month percentage changes) | |

|---|---|

|  |

Sources: Eurostat and ECB calculations.

Notes: Calculated using seasonally adjusted data. The dashed line corresponds to services adjusted for the effects of the €9 and €49 tickets introduced in Germany in June 2022 and May 2023 respectively.

The latest observations are for January 2024 (flash) for food, energy and goods, December 2023 for the rest. Missing data points for January 2024 will become available with the HICP release on 22 February 2024.

Momentum indicators have eased further for headline inflation and all of its components (Chart 11). The annualised three-month-on-three-month growth rate of seasonally-adjusted HICPX stand at 1.4 per cent, with momentum in goods inflation at zero and momentum in services inflation close to 2 per cent, while the momentum of food inflation is around 3 per cent.

Taken at face value, these readings might be interpreted as challenging the medium-term forecast. However, according to the staff projections, several factors are expected to raise momentum in the coming months, for both headline and core inflation. First, the windfall of plunging input costs through lower energy costs and lower intermediate prices, which may have temporarily muted the need for firms to raise prices is expected to level out. This, in turn, means that rising wage costs (even at the decelerating rate foreseen in the projections) will exert stronger upward pressure on overall costs. Second, the projections foresee a recovery in domestic and external demand this year. All else equal, this will increase pricing power compared to last year. Third, many of the fiscal measures that leaned against strong price pressures in 2022 are scheduled to expire, which will act to push up prices in the near term. This combination of factors explains why the overall trajectory of inflation in the December 2023 projections only converges to the target in the second half of 2025.

In assessing the wage data, compensation per employee from the national accounts provides the most comprehensive measure (Chart 12). However, these data become available only with a lag of over two months. According to the December 2023 Eurosystem staff macroeconomic projections, euro area wage growth is expected to have peaked in 2023 but to remain above the medium-term steady state level during 2024 and 2025, reflecting the ongoing gradual correction of the real wage gap that was generated by the 2021-2022 inflation surge, together with robust labour markets.[7]

Growth in compensation per employee edged downward to 5.3 per cent in 2023Q3 from 5.5 per cent in the previous two quarters. Forward-looking wage trackers provide timely and higher-frequency complements to the official wage data releases and may act as leading indicators for the subsequent releases of the official compensation per employee data.[8] One important indicator from the wage tracker is average wage growth for twelve months ahead, as embedded in agreements reached in the latest quarter (Chart 13).[9] This indicator also gradually edged down in the second half of 2023. Many wage agreements will be renewed in the early months of 2024, and updates to the wage trackers will provide essential information in projecting wage dynamics.

Chart 12

Indicators of euro area wage growth

(annual percentage growth and percentage point contribution)

Sources: Eurostat, ECB and ECB calculations.

Notes: “Wage drift” measures deviations between developments in actual wages as measured by wages and salaries and developments in negotiated wages. The latest observations are for the third quarter of 2023.

Chart 13

Euro area wage tracker

(percentage points contributions)

Sources: Calculated based on micro data on wage agreements provided by Deutsche Bundesbank, Banco de España, the Dutch employer association (AWVN), Oesterreichische Nationalbank, Bank of Greece, Banca d’Italia and Banque de France.

Notes: Euro area aggregate based on DE, FR, IT, ES, NL, AT, GR, as of December 2023.The indicator of latest agreements reflects wage growth in the agreements reached in a certain quarter for the 12 months after an agreement. One-offs payments are spread over 12 months from the agreed disbursement date - smoothing the impact of one-off payments on wage growth. Data of latest agreements for Q4 2023 preliminary as not all collective agreements reached in Q4 2023 are available yet. For the methodology, see also Górnicka, L. and G. Koester (eds.) 2024: "A forward-looking tracker of negotiated wages in the euro area". Eurosystem wage tracker experts. ECB Occasional Paper No. 338. European Central Bank (forthcoming).

Latest observation is for the fourth quarter of 2023.

The available survey indicators are broadly consistent with the decreasing wage profile foreseen in the latest Eurosystem staff projections (Chart 14). According to our most recent discussions with large European non-financial corporations, the wage growth expectations of this set of companies for 2024 are 4.4 percent on average, which is a marked easing compared to the average 2023 wage growth of 5.3 per cent.[10] Similarly, in the ECB’s latest Survey of Professional Forecasters (SPF), expectations for annual growth in compensation per employee point to a gradual decline in wage growth looking ahead and were revised down over the longer horizon. While expectations are only slightly below that forecasted for 2024 in the December 2023 BMPE round (by 0.15 percentage points), SPF respondents expect a much faster decline in wage pressures in 2025 and 2026.

Chart 14

Survey-based wage expectations and the December 2023 Eurosystem staff macroeconomic projections

(annual percentage changes)

Sources: January 2024 Corporate Telephone Survey (CTS), Survey of Professional Forecasters (SPF) and December 2023 Eurosystem staff projections.

Finally, progress along the disinflationary path will also depend on firms buffering rising labour costs with a slowdown in profit growth. Since the aggregate level of profits surged in 2021-2022, there is some room for profit compression without driving profitability to below-average levels (Chart 15). The contribution of unit profits to domestic price pressures continued to fall in the third quarter of 2023, suggesting that unit profits are absorbing some of the price pressures coming from rising unit labour costs. The profit margin proxies derived from the responses to recent corporate telephone surveys also suggest that this buffering process is at work (Chart 16).

Chart 15

SAFE-ORBIS profit margins

(percentages)

Source: ECB, European Commission survey on the access to finance of enterprises (SAFE) and Moody’s ORBIS.

Notess: The SAFE-ORBIS aggregate profit margin is calculated by summing the profits before taxes and revenues of firms in each ORBIS balance sheet year before calculating the profit margin ratio.

Chart 16

Corporate Telephone Survey (CTS)- implied profit margin

(average of Corporate Telephone Survey scores)

Source: Corporate Telephone Survey (CTS).

Notes: The score is calculated as the "selling price score - 0.5 x input cost score - 0.5 x wage score. Past and future selling and input price scores refer to developments in the previous and next quarters. The dashed lines represent the 2009-2019 average for “past” and “future”. Latest observations are from the 2024 January CTS.

Finally, a successful disinflation process requires inflation expectations to be anchored at the two-per cent target over the long term. Taking a longer view, following the protracted period of below-target inflation, between the middle of 2021 and early 2022, there was a remarkable shift in long-term inflation expectations, with survey respondents moving away from long-held views that inflation would indefinitely remain below the two per cent target (Chart 17). While there certainly was a marked increase in the fraction of survey respondents that expected inflation to remain above target in the long term, the majority of respondents assessed that the inflation shock served to re-anchor long-term inflation expectations at the target by demonstrating that inflation risks were two-sided. In turn, reinforced by the target-consistent monetary policy decisions during this period, the stabilisation of inflation expectations has provided an important anchor in the disinflation process.

In this respect, it is encouraging that measures of shorter-term inflation expectations have come down markedly more recently, while measures of longer-term inflation expectations mostly stand around 2 per cent. In particular, the inflation expectations of professional forecasters have moved down over the entire horizon, with longer-term expectations now standing at 2.0 per cent (Chart 18). Similarly, while the expectations component contained in market-based measures of inflation compensation, such as the five-year-in-five-years inflation-linked swaps, has remained anchored at two per cent throughout the inflation episode, it is notable that risk premia have receded over recent months (Chart 19).[11]

Chart 17

Evolution of long-run inflation expectations over survey rounds

(percentage of respondents)

|

Source: Survey of Monetary Analysts (SMA).

Notes: The three groups are based on the HICP long-run forecasts provided by respondents on the macroeconomic projections question of the SMA.

Chart 18

Professional forecasters’ inflation expectations

(annual percentage changes)

Sources: Consensus Economics, Survey of Professional Forecasters (SPF), ECB’s Survey of Monetary Analysts (SMA). Note: The weighted average of surveys is computed using the number of respondents in each survey as a weight.

Latest observations: January 2024 for Consensus Economics and SMA, 2024 Q1 for SPF.

Chart 19

Decomposition of 5-year-in-5-years inflation-linked swap rate

(annual percentage changes)

Sources: Bloomberg and ECB staff calculations

Notes: The 5y5y ILS rates (monthly data) refer to the average inflation rate over a five year period starting in five years’ time, as implied by ILS rates. The expectations component is based on average estimates from two affine term structure models following Joslin, Singleton and Zhu (2011) applied to ILS rates (adjusted for the indexation lag); see Burban et al. (2021), ECB Economic Bulletin Issue 8, 2021, Box 4. The latest observations are for 29 January 2024.

Conclusion

Let me conclude. The declining trend in underlying inflation has continued, and our past interest rate increases keep being transmitted forcefully into financing conditions. By tightening financing conditions, the restrictive monetary policy stance is dampening demand, and this is helping to push down inflation and stabilise inflation expectations.

The December 2023 Eurosystem staff projections see inflation stabilising around the two per cent target from about the middle of 2025 onwards. The incoming data suggest that the process of disinflation in the near term in fact may run faster than previously expected, although the implications for medium-term inflation are less clear. At the same time, the strength of the recovery of the economy, the path of fiscal policies, wage developments, and the degree to which firms absorb higher input costs, all in a context of continued heightened geopolitical uncertainty, will have an important bearing on the inflation trajectory. The March 2024 ECB staff macroeconomic projections will provide the opportunity for a comprehensive update of our medium-term inflation outlook.

We will continue to follow a firmly data-dependent approach to determining the appropriate level and duration of restriction. In particular, our interest rate decisions will be based on our assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.[12] In this process, monetary policy needs to carefully balance the risk of overtightening by keeping rates too high for too long against the risk of prematurely moving away from the hold-steady position that we have been in since September. In terms of an overall evaluation of our policy trajectory, we need to be further along in the disinflation process before we can be sufficiently confident that inflation will hit the target in a timely manner and settle at target sustainably.

I am grateful to Katalin Bodnár, Malin Andersson, Colm Bates, Anna Beschin, Cristina Checherita-Westphal, Andrea Fabbri, Anna-Camilla Hofmann-Drahonsky, Eliza Lis, Aurora Monza, Flavie Rousseau and Fabian Schupp for their contributions to this speech.

See Chahad, M., Hofmann-Drahonsky, A.-C., Page, A. and Tirpák, M. (2023), “An updated assessment of short-term inflation projections by Eurosystem and ECB staff”, Economic Bulletin, Issue 1/2023, ECB and Chadad, M., Hofmann-Drahonsky, A.-C., Meunier, B., Page, A. and Tirpák, M. (2022): What explains recent errors in the inflation projections of Eurosystem and ECB staff?, Economic Bulletin, Issue 3/2022.

I thank the BIS for generous sharing of data. These charts build on the original analysis in the 2023 BIS Annual Economic Report.

Lenza, M., Moutachaker, I. and Paredes, J. (2023): Forecasting euro area inflation with machine learning models, ECB Research Bulletin No. 112.

Headline inflation is noisy since it is affected by the short-term volatility induced by temporary idiosyncratic shocks, thereby blurring the signal about medium-term inflationary pressure that is relevant for monetary policy. Thus, central banks monitor measures of underlying inflation in order to distinguish signal from noise in the data. See Lane, P. R. (2022): Inflation Diagnostics, ECB Blog, 25 November 2022. and Bánbura, M., Bobeica, E., Bodnár, K., Fagandini, B, Healy, P. and Paredes, J. (2023): Underlying inflation measures: an analytical guide for the euro area, ECB Economic Bulletin, Issue 5/2023.

See Bánbura, M., Bobeica, E., Bodnár, K., Fagandini, B, Healy, P. and Paredes, J. (2023): Underlying inflation measures: an analytical guide for the euro area, ECB Economic Bulletin, Issue 5/2023; Lane, P. R. (2022): Inflation Diagnostics, ECB Blog, 25 November 2022. and Lane, P. R. (2023): Underlying inflation, Lecture at Trinity College Dublin, 6 March 2023.

Legislated increases in minimum wages are an important part of the adjustment process.

Wage trackers focus on negotiated wages. While compensation per employee also reflects other factors, the differential between the two (primarily the “wage drift” term) has weakened in recent months.

The wages offered in job vacancy notices provide an additional leading indicator, since the outside option of looking for a new job is relevant in the wage bargaining process. The associated wage tracker produced by the collaboration between Indeed and the Central Bank of Ireland provides an important perspective on this dimension. See Adrjan, P. and Lydon, R. (2022): Wage Growth in Europe: Evidence From Job Ads. Central Bank of Ireland Economic Letter Vol. 2022, No. 7.

These figures are based on the mid-points of the reported ranges.

Consumer inflation expectations and perceptions have overall declined in recent months, even if expectations three years ahead edged up in the most recent release. In general, some volatility in the distribution of household inflation expectations can be interpreted as inescapable, although persistent and material shifts away from the neighbourhood of the target warrant careful monitoring.

Monetary policy ultimately has to be calibrated vis-à-vis the underlying equilibrium rate of interest. For a recent update of estimates of the natural rate of interest in the euro area, see C. Brand, N. Lisack and F. Mazelis, “Estimates of the natural interest rate for the euro area - an update”, Economic Bulletin, Box 7, Issue 1, ECB, 2024.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts