Ladies and Gentlemen, [1]

The global economic and financial crisis confronted the world economy not only with financial turbulence, loss in output and social distress on a scale not seen since the Great Depression. It also created a series of challenges for policy- makers. Across the euro area, it exposed structural and institutional weaknesses that had remained hidden during the preceding era, the “Great Moderation”.

Times of crisis are times of hardship – but they are also times of change and opportunity. This seems particularly true for Europe, where progress has often come in this way.

The Second World War was the impetus for the European Coal and Steel Community, which was established to prevent another war between France and Germany. It formed the nucleus of today’s European Union. The demise of the Bretton Woods system in the 1970s was the catalyst for a European single currency, which was eventually introduced in 1999.

I’ll be talking today about the effects of the present crisis and the various challenges it has presented for the euro area. I’ll compare it with the East Asian crisis of 1997. In my view, there are similarities that yield useful policy lessons for the euro area. But there are also differences that need to be kept in mind.

What can we learn from the Asian crisis?

What are the parallels between the Asian crisis in 1997-1998 and the euro area crisis?

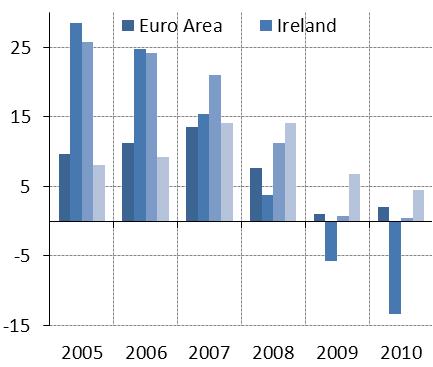

The economies of emerging Asia were characterised by buoyant growth and a brisk expansion of credit (see Chart 1). This rise in debt was facilitated by considerable inflows of foreign capital, which financed significant external deficits (see Chart 2). This led to growing financial imbalances, and in particular to currency and maturity mismatches on the balance sheets of local banks. In addition, the economic boom prevailing at that time was accompanied by a loss of competitiveness of the region’s export sector. Investors typically under-priced potential risks as they had overly optimistic expectations of the medium-term growth prospects. They did not identify systemic vulnerabilities such as the risk of sudden stops in capital flows or of twin crises of the banking system and the balance of payments, which eventually materialised. [2]

Except for currency mismatches, similar developments were evident in the euro area before 2009 – if not at the regional level, at least in those countries that later ran into financial difficulties. It was widely believed that sudden stops in capital flows, not to mention twin banking and balance of payments crises, could not happen in advanced economies. [3] And yet this is exactly what happened in Europe ten years after the Asian crisis (see Chart 2).

It seems therefore useful to look also at East Asia’s response to its crisis and see what lessons can be learned.

One lesson is that a deep and fundamental restructuring of the domestic financial sector is necessary.

Given the financial nature of the Asian crisis, this was a key element in resolving it. Non-viable financial institutions were closed, viable institutions recapitalised and strengthened, value-impaired assets dealt with and the corporate sector restructured, including through foreign investment. [4] These measures were implemented decisively. They were associated with a painful adjustment process in the crisis countries but, at the same time, they made a swift recovery possible.

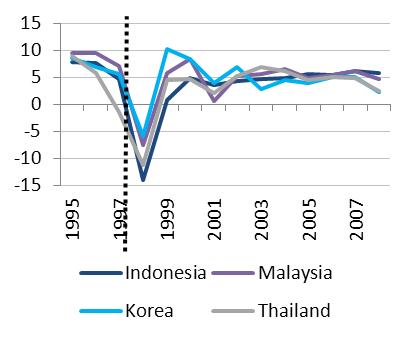

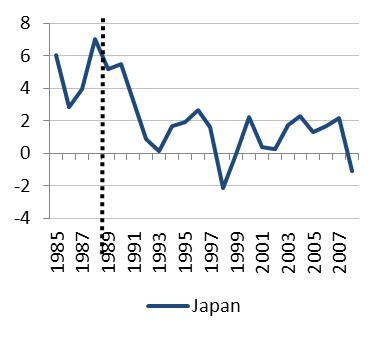

This experience contrasts with Japan’s experience in the late 1980s. Following the bursting of Japan’s asset bubble, there was by and large no rapid write-down of non-performing assets. Due to the low profitability of banks, it was believed that an immediate write-off of bad loans would prevent compliance with capital requirements. The recognition of losses was postponed and, as a consequence, capital continued to be allocated to investments with limited positive impact on Japan’s long-term growth potential, which some have called “zombie lending” [5]. Ultimately, this resulted in Japan’s “lost decade”, namely an extended period of anaemic growth (see Chart 3).

A second lesson is that institutional and structural reforms are essential.

Early in the crisis, emerging Asian economies strengthened prudential regulation and supervision, together with bank governance and market transparency and discipline, in order to prevent further instability and bring domestic standards closer to the international norms. [6]

Furthermore, they generally acknowledged that their economic “miracle” before the crisis was not sustainable. It was driven by over-investment encouraged by Colbertist policies, implicit government guarantees, and too often, opaqueness and political interference in market mechanisms [7]. As a result, at the macro level, growth was led by capital accumulation in the wrong sectors and not by a rise in total factor productivity. In Paul Krugman’s words, the Asian miracle was “the fruit of perspiration, not of inspiration” [8].

To address the root causes of the crisis, structural reforms aimed at improving governance and challenging vested interests, both in public policy-making and in the corporate sector, were essential. [9] The lesson to be learnt was that sustainable growth can only be achieved by fostering an environment that encourages open markets, innovation and entrepreneurship.

A third lesson is that re-nationalisation and protectionism are not the solution to a crisis.

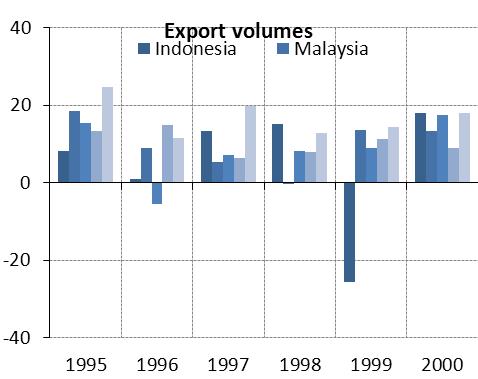

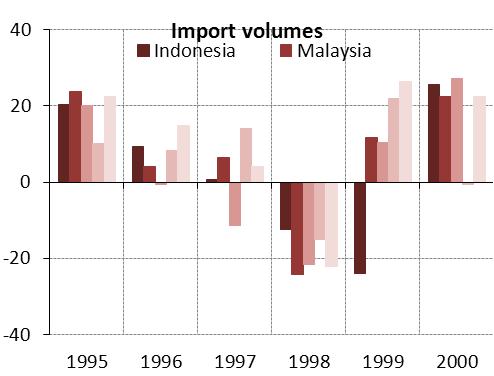

Indeed, there is empirical evidence that more open economies recover faster from the output contraction that usually accompanies a sudden stop of capital. [10] As such, the most open Asian economies, such as Hong Kong and Singapore, were among the least severely affected and fastest to recover from the Asian crisis. [11] In other words, despite the attendant risks, globalisation in trade is still the best way to achieve progress and economic development, and open financial markets can support it provided they are backed by strong prudential supervision. Open trade policies in the crisis helped Asian economies to benefit from the upswing in global trade and growth towards the turn of the millennium (see Chart 4), which in turn supported the post-crisis recovery.

However, while there may be lessons to learn, what are the important differences between emerging Asia of the 1990s and the euro area today?

Emerging Asian economies had greater policy leeway than euro area countries in dealing with their crises, in that they had flexible exchange rate regimes. Some might argue that this makes it hard to say which part of the Asian experience is relevant for Europe. But I would have a different interpretation: a lack of nominal exchange rate flexibility does not preclude real exchange rate adjustment. Sharing a currency entails a fundamental trade-off. It brings considerable microeconomic benefits but it creates responsibilities for participating countries. They should run prudent policies to make asymmetric shocks less frequent, ensure that relative prices can adjust if such a shock nevertheless occurs, and be prepared to insure each other against extreme outcomes when the former mechanisms are not enough.

The conditions were unfortunately not met in the euro area. National policies were run on the misguided assumption that countries, companies and households could borrow forever. In spite of needing more flexible markets with its single currency, Europe faced stronger nominal rigidities than East Asia in labour and product markets. [12] This limited the ability of euro area countries to adjust to asymmetric shocks, especially as cross-border labour mobility was low and public debt levels were already high. And finally, no mutual insurance mechanism was in place.

But, and here comes the good news, unlike emerging Asia in the late 1990s, Europe had a well-established regional political framework to address its crisis. The framework of integration and cooperation among EU members is old and dense, building on the experience gained with the European Monetary System [13]. This made it possible to create the necessary instruments (the EFSF and ESM) for financial support for domestic adjustment programmes to come mainly from within the Union, with the IMF focusing on monitoring conditionality.

Some will remember the IMF Annual Meetings in 1997 in Hong Kong, when calls to create an “Asian Monetary Fund” were judged incompatible with the IMF’s universal mandate. [14] Contrary to Asia in the late 1990s, Europe had the political infrastructure in place to sustain the sharing of sovereignty that makes mutual insurance mechanisms possible. This is not to say that all the discussions were easy, far from it, as might be expected in times of crisis. Europe’s sense of commonality was, and still is, under severe strain. But the political framework was there to produce decisions, and most importantly, a legal framework was also there to implement them.

The lesson from this is that regional integration, regional rule of law, and the sense of a common project are sources of stability. [15] In East Asia, things have moved on since the late 1990s, with the Chiang Mai Initiative multilateralisation. The G20 has taken stock of the Asian and European experiences and acknowledged the relevance of regional financial arrangements.

The road ahead for the euro area

Based on the lessons learnt from the Asian crisis, what are the main challenges we face in the euro area? Let me consider them one by one.

Restructuring Europe’s financial sector

To begin with, we need to reform Europe’s financial sector.

We have, so to speak, come to a crossroads in Europe. In one direction lies the Japanese experience, and in the other direction that of emerging East Asia. The authorities can either choose between swiftly auditing and repairing the banking sector, which will help to restore credit flows, or they can allow forbearance, which will harm the long-term prospects for our economy.

I do not mean to downplay the significant restructuring and recapitalisation that has already taken place in Europe. Since the onset of the global financial crisis, euro area banks have raised around €225 billion of fresh capital and a further €275 billion has been injected by governments, equivalent in total to more than 5% of euro area GDP. Today, the median Core Tier 1 capital ratio of the largest euro area banks stands close to 12%. But there is some way to go. To ensure that we take the right road, I see three responses as key.

The first is to carry out a comprehensive clean-up of the banking system so that the price mechanism is no longer obscured by uncertainty about asset valuation and bank funding models, and banks can free up balance sheet capacity to extend new loans.

The ECB will take up its supervisory responsibilities in about a year from now, and as part of this we will conduct a comprehensive assessment of 128 significant credit institutions covering 85% of euro area bank assets. We announced the details of this exercise on Wednesday last week. [16] It aims to increase transparency, to identify the necessary corrective actions and to build confidence in the banking system.

With such steps, and provided that sources of capital are clearly identified, including public backstops when private sources have been exhausted, I firmly believe we can put the banking system on a sounder footing and enable it to support the economy’s recovery.

The second response is to reduce financial fragmentation. Despite having a single market for capital in Europe, liquidity is not fully fungible between and even within cross-border banks. This means that liquidity usage is not optimised – surpluses in some countries are not used to fund deficits in others. The result is a greater divergence in bank funding costs and lending rates than would be warranted by the underlying economic fundamentals, and euro area companies being unable to tap a single pool of savings to fund their development.

The third response is to explore avenues for non-bank financing – that is, to develop debt and equity capital markets in Europe. Around 75% of firms’ external financing in the euro area comes from banks, which makes the economy particularly vulnerable to crises that spread through the banking system. Measures are being introduced in Europe to develop capital markets for long-term financing and deepen markets for the securitisation of loans to small and medium-sized enterprises [17].

However, having a well-functioning financial sector is only one part of the story. To leave the crisis behind us, we also have to ask: what in fact does that sector finance? Again, we can learn from the Asian crisis: we need to foster growth and total factor productivity with new business models.

Fostering growth: new business models

Due to its length and severity, the economic downturn has already caused a permanent loss in output and a rise in structural unemployment, and we cannot rule out that the growth rate of potential output has been affected too. To repair this damage, investment in both physical and human capital has to be a key component of the recovery. Clearly, there is spare capacity in the euro area economy. Total investment in the euro area is currently 17% lower than it was in 2007. But some of this capacity is in sectors which will not be future engines of growth – such as commercial real estate in some of the stressed countries. What we need is investment in new business models that will raise total factor productivity and provide the sources of future growth.

Politicians are not the best placed to decide what these business models will be. The market economy will take care of that. The important thing is that we create an environment that encourages innovation and entrepreneurship so that new models can emerge, and capital and labour can be reallocated to a more efficient use. This is in the best interests of the people of Europe, both as workers and as savers, beginning with those who have been hit hardest by the crisis. It nevertheless implies changes at both national and European levels.

At national level, we need to prioritise public spending towards productivity-enhancing investment, ensure that labour and goods market are flexible, cultivate a supportive regulatory, judicial and educational environment, and open our economies to spur competition and encourage the emergence of new actors.

Opaqueness and vested interests [18] are not only defining features of developing economies. Successful reform in European economies hinges on efforts to curb rent-seeking behaviours. For example, doesn’t the Single Supervisory Mechanism have the objective of freeing bank supervision from national politics?

At European level, we need to provide a framework that supports and incentivises the introduction of such national policies. This is the role of economic union in the euro area, the “E” of EMU. I would stress, however, that economic union does not mean defining a single economic model across all countries. On the contrary, its purpose is to create the conditions for each country to identify and develop its comparative advantage. Paradoxically, it is only by encouraging difference – comparative advantage – that the euro area can achieve convergence – that is, a more even distribution of economic outcomes.

Avoiding re-nationalisation and protectionism

Let me finally address the third lesson learnt from East Asia. Europe needs to avoid protectionist temptations and calls for re-nationalisation. Protectionism and beggar-thy-neighbour policies would lead to further losses of welfare at both European and global level.

Fortunately, there has been no significant surge in barriers to global trade in recent years – unlike during the Great Depression – thanks to global and regional policy coordination. These efforts remain important. Barriers to trade in goods and services cannot be raised within Europe thanks to our Single Market and competition rules which are enshrined in European laws, but the Single Market can be further enhanced.

Savings have been partly re-nationalised as a consequence of financial fragmentation. This is a trend that, if left unchecked, can be fatal to the Single Market. Completing the Banking Union is key to halt it, and I welcome EU leaders’ resolve to swiftly agree on a Single Resolution Mechanism.

Finally, Europe should remain open to the world. Further progress on bilateral or regional free trade agreements, and cooperation in implementing the new financial regulatory standards, are the best signal in this respect.

Conclusion

Let me draw to a close by re-emphasising that crises, despite their negative consequences, can have positive effects. They can galvanise efforts and focus minds. They can drive change and bring about progress. They can pave the way for innovative solutions. But to secure these gains, cooperation across national borders is crucial, in other words, there must be a willingness to work towards common goals and to learn from each other and resist protectionism. This spirit will be essential to tackle the challenges still ahead of us, not only in the euro area but also at a global level.

It is often claimed that the Chinese and Japanese word for crisis, wēijī or kiki (危机 or 危機), is made of the two characters meaning “danger” and “opportunity”. While there can be no doubt that wēi means “danger”, I would rather understand jī as meaning the critical moment when things have to change – the ancient Greeks’ kairos. This critical moment has now arrived for Europe. Europe has emerged from the danger zone. It’s time for us to get our act together, to reform, and to grow.

Thank you very much for your attention.

Chart 1: Credit growth to the private sector in East Asia and the euro area (in percentage changes, year to year)

Sources: IMF WEO and Haver Analytics

Chart 2: Current account balances in East Asia and the euro area (in % of GDP, East Asia in 1996, euro area in 2008)

Sources: IMF WEO and Haver Analytics

Chart 3: Real GDP growth in East Asia and Japan before, during and after their crises ( in percentage, year to year).

Source: Haver Analytics

Chart 4: Export and Import volumes of goods and services in East Asia (in percentage changes, year to year)

Sources: IMF WEO and Haver Analytics

-

[1]I would like to thank Ine Van Robays for her contribution. I remain solely responsible for the opinions contained herein.

-

[2]See Calvo, G. (1998). “Capital Flows and Capital-Market Crises: The Simple Economics of Sudden Stops”, Journal of Applied Economics 1(1), pp. 35-54, and Kaminsky, G. and C. Reinhart (1999). “The Twin Crises: Causes of Banking and Balance-of-Payments Problems”, American Economic Review, 89, pp. 473-500. A well known example of complacency about East Asian growth is the 1993 World Bank report on “The East Asian Miracle”.

-

[3]See FRBSF Economic Letter (2011). “Could We Have Learned from the Asian Financial Crisis of 1997-98?”, February 2011.

-

[4]See Lindgren, C.-J. et al. (1999). “Financial Sector Crisis and Restructuring. Lessons from Asia”, IMF Occasional Paper, 188.

-

[5]See Fukao, M. (2003). “Japan’s Lost Decade and its Financial System”, The World Economy, 26, pp. 365-384, and Caballero, R., T. Hoshi and A. Kashyap (2008). “Zombie Lending and Depressed Restructuring in Japan”, American Economic Review, 98:5, pp. 1943-1977.

-

[6]See footnote 4.

-

[7]See Krugman, P. (1999). “What happened to Asia?”, in Sato R. et al., Global Competition and Integration, Kluwer Academic Publishers, pp. 315-327. Already in 1590 Hong Zicheng’s Càigēntán claimed that “water that is clear has no fish.”

-

[8]See Krugman, P. (1994). “The Myth of Asia’s Miracle”, Foreign Affairs, 73:6 (1994: November/December).

-

[9]See Kochpar, K., P. Loungani and M. Stone (1998): “The East Asian Crisis: Macroeconomic Developments and Policy Lessons”, IMF Working Paper 98/128.

-

[10]See Cavallo E.A. and J. A. Frankel (2008). “Does Openness to Trade Make Countries More Vulnerable to Sudden Stops, Or Less? Using Gravity to Establish Causality”, Journal of International Money and Finance, Volume 27, Issue 8, pp. 1430–1452.

-

[11]See Loong, L.S. (2000). “Post crisis Asia – The way forward”, BIS William Taylor Memorial Lecture, 21 September 2000.

-

[12]See Heinz, F.F. and D. Rusinova (2011): “How flexible are real wages in EU countries? A Panel Investigation”, ECB Working Paper No 1360.

-

[13]See James, H. (2012):”Making European Monetary Union”, The Belknap Press of Harvard University Press.

-

[14]See Sakakibara, E., 2000, Nihon to Sekai ga Furueta Hi, Chuo Koron Shinsha.

-

[15]“G20 Principles for Cooperation between the IMF and Regional Financing Arrangements as endorsed by G20 Finance Ministers and Central Bank Governors”, 15 October 2011.

-

[16]The comprehensive assessment entails three broad elements. First, a supervisory risk assessment to review key risks including liquidity and funding. Second, a balance sheet assessment to enhance transparency in banks’ balance sheets and their asset quality, collateral valuation and provisions, and so on. And third, a stress test to examine banks’ resilience to adverse scenarios. See European Central Bank (2013). “ECB starts comprehensive assessment in advance of supervisory role”, 23 October.

-

[17]See European Commission (2013). Long term financing of the European economy, Green Paper, March.

-

[18]I refer here to the concept of “limited access social orders”, see North, D., J. Wallis and B. Weingast (2009). Violence and Social Orders: A Conceptual Framework for Interpreting Recorded Human History, Cambridge University Press.