Published as part of the Financial Integration and Structure in the Euro Area 2024

This box reassesses the patterns of euro area financial integration, adjusting for the role of financial centres in the euro area. Since the introduction of the euro, Luxembourg, Ireland and the Netherlands have accumulated large volumes of cross-border assets and liabilities, vis-à-vis both intra- and extra-euro area counterparts. In fact, as shown in Chart A, the exceptional growth in euro area cross-border financial positions since 1990 has been driven largely by positions vis-à-vis Luxembourg, Ireland and the Netherlands which are referred to as “euro area financial centres” (EAFCs).[1] Their special role involves acting as one of the euro area’s major hubs for (i) the investment fund industry, and (ii) securities issuance by affiliates of foreign companies. For example, investment funds domiciled in Luxembourg and Ireland hold around 40% of the euro area’s cross-border equity and debt securities, while 33% of all intra-euro area cross-border holdings of corporate bonds are in securities issued in EAFC jurisdictions.

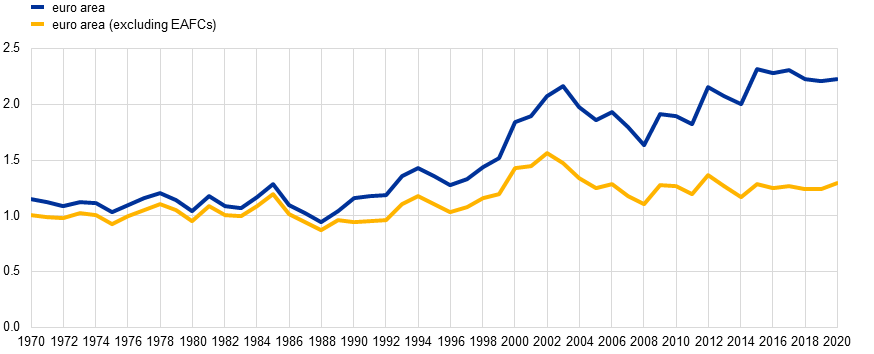

Chart A

Gross external position

(relative to GDP and average for a set of advanced countries)

Source: Reproduction from BCLMSS (2024).

Notes: The gross external position is defined as the ratio of the gross assets and gross liabilities of all euro area countries relative to the sum of their GDPs. The chart plots a time series for this gross positions index scaled by the average value of the gross external position for a set of other advanced economies (blue line), which includes the United States, Japan, the United Kingdom, Switzerland, Australia, New Zealand, South Korea, Norway and Canada. The yellow line shows the equivalent series when Luxembourg, Ireland and the Netherlands are excluded from the set of euro area countries.

Looking through the dual role of EAFCs as hubs for investment funds and securities issuance provides a nuanced picture of euro area financial integration and portfolio exposures.[2] The results presented in this box are based on the methodology developed in BCLMSS (2024), which combines various security-level, commercial and macro-financial data sources. The restatements of the euro area’s external positions by BCLMSS (2024) involve two steps. First, the ECB’s Securities Holdings Statistics provide information about euro area investment in individual securities, including fund shares, at the euro area country-sector level. When combing this information with estimates of fund-level investment for funds domiciled in Luxembourg and Ireland (based on commercial data sources), a granular look-through approach enables the fund investments to be traced to investors based in other euro area countries and in the rest of the world (RoW).[3] Second, the resulting data are combined with a mapping algorithm that reassigns each globally-issued security from its immediate issuer entity to the ultimate parent entity, and thereby determines its nationality.[4] Finally, the aggregates built-up from the micro-level data are benchmarked to the euro area and the Member States’ data on international investment positions.

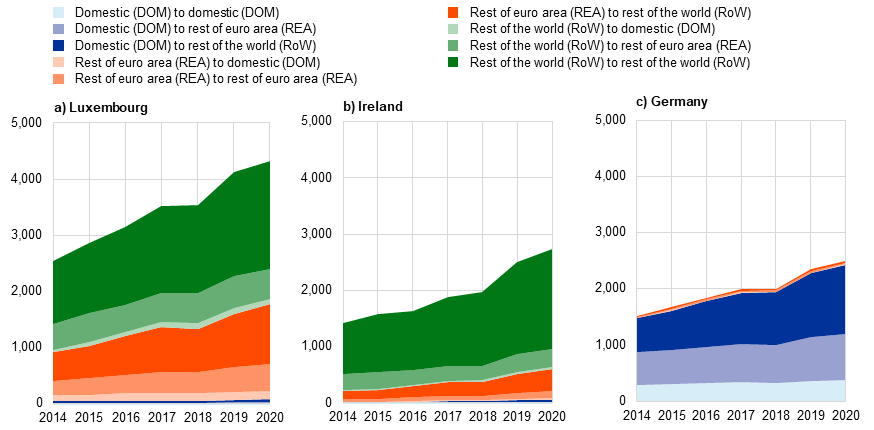

The restatements methodology reveals that the euro area as a whole is less financially integrated with the rest of the world, i.e. it has a smaller external portfolio investment position, than implied by the official data. Quantitatively, this is largely because a sizeable fraction of the fund share holdings in Luxembourg and Ireland are identified as not being held by euro area residents (Chart B, green areas). Such investments do not constitute an economically meaningful exposure for the euro area since they are held on behalf of RoW investors. To the extent that RoW investors mainly invest in non-euro area countries via funds in Luxembourg and Ireland, these positions constitute a form of pass-through via EAFCs (Chart B, dark green areas).

The restatements also reveal that Luxembourg and Ireland act as a source of portfolio diversification for the other euro area countries, since the methodology factors in their indirect fund holdings via EAFCs.[5] These holdings are sizeable, in particular those that are invested in RoW countries (Chart B, panels a) and b), dark red areas). For instance, the exposure of euro area investors to securities issued by Chinese companies is found to be much larger than in the official data. This is mainly due to the fact that offshore issuance by affiliates of Chinese companies is assigned to the Chinese parent entities in the restated data. The patterns observed for Ireland and Luxembourg contrast with those for other euro area countries such as Germany, where fund shares are largely held by domestic investors (Chart B, panel c). Moreover, the restatements show that the underlying portfolio of securities held by euro area investors differs considerably from that of RoW investors via these funds. Funds held by euro area investors are more likely to invest in securities issued by euro area entities and in euro-denominated bonds, as compared with funds held by RoW investors.

Chart B

Heterogeneity in holdings through investment funds in Luxembourg, Ireland and Germany

(EUR billions)

Source: Reproduction from BCLMSS (2024).

Notes: This chart uses the methodology to decompose the assets of investments funds domiciled in Luxembourg, Ireland and Germany in the ECB’s Securities Holdings Statistics into who the ultimate investors are and which countries’ securities (by nationality) the investments are in. Blue areas correspond to domestic investors, red areas to investors in the rest of the euro area (REA) and green areas to unaccounted-for investors, potentially in the rest of the world (RoW). Light shades correspond to investment in domestic securities, medium shades to investment in REA securities and dark shades to investment in RoW securities.

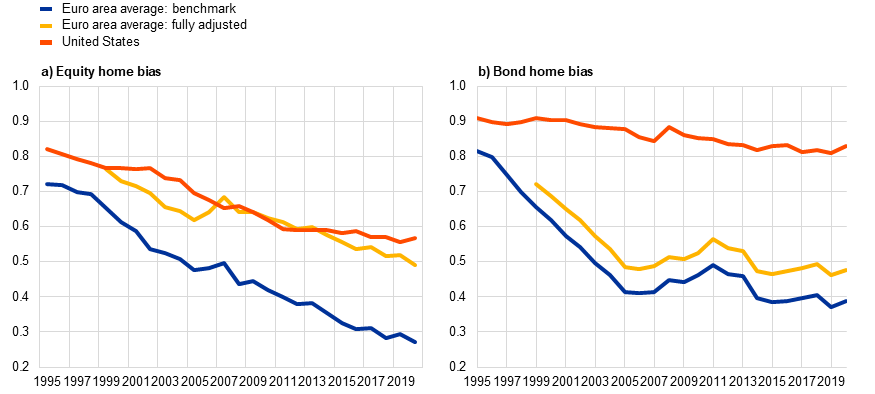

The adjusted dataset provides new evidence on the extent of euro area financial integration with the rest of the world, as measured by home bias.[6] Chart C shows the estimated time series of equity and bond home bias for the euro area for the period 1995-2020 compared with the same measure for the United States. According to standard benchmarks used in the literature, there was a sharp decline in home bias in the euro area for both bonds and equities relative to the United States around the time of the introduction of the euro (Chart C, red solid line). Yet, owing to the unavailability of granular data, these benchmarks were based on a number of assumptions which tended to significantly overstate the fall in equity home bias for the euro area relative to the United States. The distortion in the measurement of home bias occurs largely because euro area holdings of fund shares in Luxembourg and Ireland were treated as claims on foreign common equities in standard estimation methodologies, while they in fact also reflect claims on domestic assets, as well as on debt securities and other non-equity assets.[7] Moreover, EAFC fund positions are partly held on behalf of RoW investors, who tend to invest in more diversified funds.

Following the adjustments, the evolution of equity home bias in the euro area looks very similar to that of the United States since 1995, while euro area bond home bias declined significantly (Chart C). The introduction of the common currency thus had an impact on bond home bias, also when using the restated data, which is in line with economic theory.

Chart C

Home bias in equities and bonds in the United States and the euro area

(index)

Source: Reproduction from BCLMSS (2024).

Notes: The blue lines show the baseline average home bias estimate for the euro area countries without corrections, while the yellow lines adjust for the presence of RoW investors’ holdings in funds in Luxembourg and Ireland and for the indirect portfolios held by euro area investor countries. For comparison, the red lines show the home bias for the United States.

Bonds issued in EAFCs are more widely held by other euro area investors than those issued in domestic capital markets (Chart D, panel a). Firms which raise capital through EAFCs therefore better approximate the policy goal of a capital markets union, with their bonds held more widely by investors within the euro area. The analysis in BCLMSS (2024) demonstrates that, within a given firm’s bond issuance, investors based in other euro area countries are more likely to hold bonds issued in EAFCs than those issued domestically. As shown in panel b) of Chart D, this allocative effect is stronger for southern European Member States, such as Italy, than for Germany.

The analysis suggests that the use of financing structures in EAFCs helps European firms to overcome some of the frictions in cross-border financial integration. Such frictions may arise from differences in information on the functioning of the legal systems across the EU, which may be particularly true for firms in the southern EU Member States.[8] At the same time, to the extent that setting up EAFC financing affiliates involves fixed costs, the effects presented might skew financial integration towards those firms that are largest, most productive and most sophisticated.

At the same time, the outsized role of EAFCs overstates the extent of euro area financial integration – both within the euro area and vis-à-vis the rest of the world –particularly in the case of equity investment. This may have implications for macro-financial stability and surveillance in the euro area, in addition to other implications for economic governance. For instance, tracing portfolio investments from ultimate issuers to the underlying investors has become increasingly difficult, owing to the complex chains of financial intermediation in the euro area.

Chart D

Impact of EAFC issuance on the investor base

a) Distribution of domestically held shares for bonds | b) Within-firm effects: Italy versus Germany |

|---|---|

|  |

Notes: Reproduction from BCLMSS (2024). Panel a): For each bond issued by a European ultimate parent entity, the chart computes the share held by domestic investors, after accounting for indirect holdings through the fund unwind step. The blue density shows kernel estimates of the distribution of domestically held shares for bonds issued via domestic entities, while the red density shows the same, but for bonds issued through EAFC affiliates. The data are shown as of 2020, and ultimate parent entities with nationality in Luxembourg, Ireland or the Netherlands are excluded. Panel b): The chart plots the estimated marginal within-firm effects of an EAFC indicator on the domestically held share of euro-denominated bonds, inclusive of firm fixed effects, for the two subsamples of Italian (blue estimates) and German (red estimates) ultimate parent entities. The estimates are calculated separately for each year in the sample. The chart also shows point estimates and the corresponding 95% confidence band. Standard errors for the estimated PPML coefficient are clustered at the firm level, and they are converted to standard errors on marginal effects using the delta method.

See also Beck, R., Coppola, A., Lewis, A.J., Maggiori, M., Schmitz, M. and Schreger, J., “The Geography of Capital Allocation in the Euro Area”, Working Paper, No 32275, National Bureau of Economic Research, March 2024. Hereinafter, this working paper is referred to as “BCLMSS (2024)”.

When investment funds domiciled in the EAFC countries hold securities on behalf of other euro area or global investors, these holdings are recorded in the official statistics as belonging to these EAFCs rather than to the countries of the underlying owners. Similarly, when firms issue bonds or equities through subsidiaries in these jurisdictions, these securities are recorded in the official statistics as liabilities of the EAFC rather than of the country of their ultimate parent entity.

RoW investments are derived as a residual, i.e. securities that are not reported to be held by euro area investors are assumed to be owned by RoW investors. BCLMSS (2024) provides evidence that this is very likely the case for the largest part of the residual, e.g. using a “revealed micro-level preference” approach.

For further details on the mapping of issuers by nationality, see Coppola, A., Maggiori, M., Neiman, B. and Schreger, J., “Redrawing the Map of Global Capital Flows: The Role of Cross-Border Financing and Tax Havens”, The Quarterly Journal of Economics, Vol. 136, No 3, August 2021, pp. 1499-1556.

This finding is consistent with previous studies that have performed a fund unwind. See, for example, Carvalho, D. and Schmitz, M., “Shifts in the portfolio holdings of euro area investors in the midst of COVID-19: looking-through investment funds”, Working Paper Series, No 2526, ECB, Frankfurt am Main, February 2021, in which the fund share holdings by euro area members are unwound by assuming that investors own a representative portfolio of fund holdings. See also Lambert C., Vivar, L. M. and Wedow, M., “Is home bias biased? New evidence from the investment fund sector”, ECB Working Paper No. 2924, April 2024, in which the authors perform an unwind at the fund-security level and find that the home bias within the mutual fund sector is lower for euro area member countries when the unwound positions are included.

See, for example, Coeurdacier, N. and Rey, H., “Home Bias in Open Economy Financial Macroeconomics”, Journal of Economic Literature, Vol. 51, No 1, March 2013, pp. 63-115, and the references provided therein.

For example, see Coeurdacier, N. and Rey, H. (2013), in which the authors consider intra-euro area cross-border equity holdings as foreign holdings of common equity.

This effect could be similar to that of premia for bonds issued in foreign jurisdictions, which can offer more legal protection than domestic bonds. See, for example, Chamon, M., Schumacher, J. and Trebesch, C., “Foreign-law bonds: can they reduce sovereign borrowing costs?”, Working Paper Series, No 2162, ECB, Frankfurt am Main, June 2018.