Carry-over effects and intra-quarter GDP growth – estimates based on monthly indicators[1]

Published as part of the ECB Economic Bulletin, Issue 7/2022.

The annual average growth rate of real GDP for a given year partly reflects developments in the previous year. The annual growth rate of real GDP for a given year is determined by the growth dynamics of real GDP not only in that particular year but also in the previous year, which results in a “carry-over effect”. The carry-over effect captures how much annual GDP would grow if all quarterly growth rates in that year were zero. The growth dynamics in the year in question can then simply be calculated as the difference between the annual growth rate and the carry-over effect. The carry-over effect is a useful metric as it gives some early indication of growth in the current year as a whole.[2]

Similarly, the quarterly growth rate of real GDP can in part be explained by developments in the previous quarter. This is particularly useful in the current environment, with sharp and sudden fluctuations in economic developments related in large part to the ongoing war in Ukraine and the consequences of the coronavirus (COVID-19) pandemic. This box presents estimates of carry-over effects and intra-quarter growth rates in recent quarters as well as the respective contributions from the main economic sectors. Specifically, a measure of monthly real GDP is estimated from January to September 2022 by interpolating actual quarterly real GDP into monthly observations using monthly indicator variables.[3] The monthly indicators are used up to their latest available observation and an unchanged level thereafter until the end of the third quarter. This approach allows an estimation of the carry-over effect on the third-quarter growth rate and an assessment of the growth dynamics within the quarter based on the latest available indicator values in the third quarter. Finally, a sectoral approach to measuring monthly GDP is adopted by using industrial production, construction production and an indicator for services production.[4]

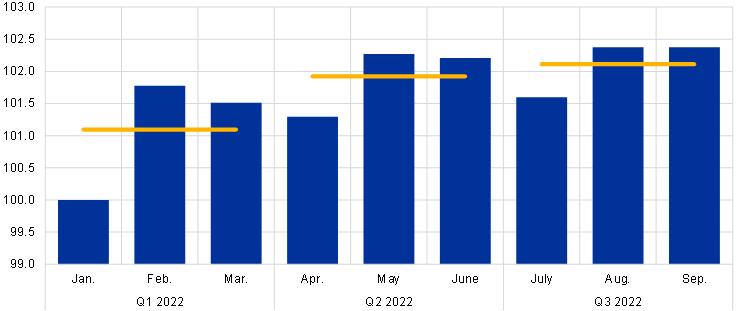

In the third quarter of 2022, monthly data point to a lower, but positive, carry-over effect on growth from the preceding quarter, while the dynamics within the quarter are likely to have turned negative. The bars in Chart A show the profile of estimated monthly real GDP from January to September 2022. The yellow horizontal lines represent the actual quarterly GDP levels in the three quarters shown in the chart. Thus, the difference between the second and the first line in the chart corresponds to the actual quarterly growth rate of real GDP in the second quarter of 2022 (0.8%). The difference between the estimated level of real GDP in March 2022 (the final month of the first quarter) and the first-quarter average is the estimated carry-over effect on growth in the second quarter (0.4%). This is what growth would have been in the second quarter if the level of GDP were unchanged from March throughout the second quarter. This implies that the difference between the second-quarter average and the level in March is equivalent to the estimated growth dynamics within the second quarter (0.4%). For the third quarter of 2022, when GDP increased by 0.2% according to the preliminary flash estimate, the same decomposition of growth can be applied. While the carry-over effect on third-quarter growth is still positive at 0.3%, the intra-quarter growth dynamics in the third quarter turned negative and are estimated at -0.1%.[5]

Chart A

Quarterly and estimated monthly real GDP levels for the euro area

(index: January 2022 = 100)

Sources: Eurostat and ECB calculations.

Notes: The chart shows the profile of estimated monthly real GDP from January to September 2022 based on an interpolation of actual quarterly GDP using monthly industrial, construction and services production as explanatory variables. The monthly indicators are used up to their latest available observations in the third quarter and an unchanged level thereafter up to September. The latest observations are for the third quarter of 2022 for quarterly GDP, August 2022 for industrial and construction production and June 2022 for services production (with estimates for July and August based on available country data).

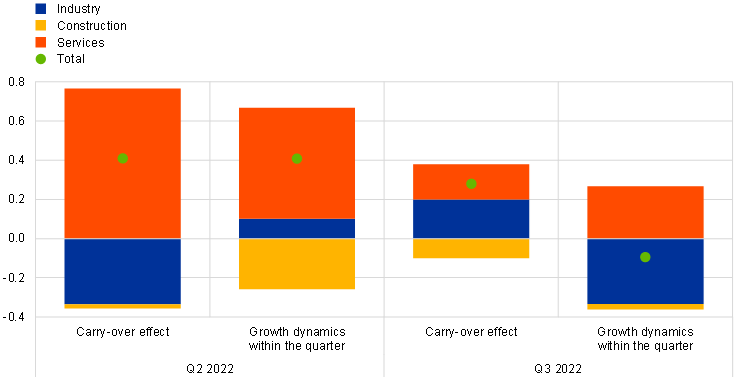

A sectoral breakdown of growth suggests that the slowdown in the third quarter reflects a smaller carry-over effect and heterogenous intra-quarter growth in services and industry. The method described above allows a sectoral analysis of growth dynamics in recent quarters. While industry was more affected by the impact of the war and input shortages, the services sector was boosted by the reopening of contact-intensive services following the pandemic. Indeed, the results show that both the carry-over effect on second-quarter growth and the growth dynamics within the second quarter were largely driven by the services sector (Chart B). In the third quarter, however, the growth impetus from the services sector is set to weaken. This is reflected not only in a weaker contribution of the services sector to the carry-over effect on growth in the third quarter but also in a smaller contribution to growth within the third quarter. In addition, industrial activity is likely to weigh on growth within the third quarter, reflecting a deterioration in industrial production on average in the first two months of the third quarter.

Chart B

Estimated sectoral contributions to carry-over effects and intra-quarter growth dynamics in the second and third quarters of 2022

(quarter-on-quarter percentage changes and percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: The chart shows model-implied sectoral contributions to carry-over effects and the growth dynamics within the quarter for quarterly real GDP growth. For details on the monthly GDP estimates, see the notes to Chart A.

To conclude, monthly indicators suggest that industrial output dynamics remained weak in the third quarter, while services sector growth declined. While output is estimated to have stagnated towards the end of the second quarter of 2022, it fell going into the third quarter. The deterioration in the short-term dynamics was broad-based across sectors, with both the industry and services sectors contributing to slower intra-quarter dynamics in the third quarter. This is in line with most forecasts, including the September 2022 ECB staff macroeconomic projections for the euro area, which indeed see a slowdown in economic activity in the second half of the year.

This box includes data released after the cut-off date for data for the main text (26 October 2022).

For a more detailed explanation of the carry-over effect on annual growth from quarterly developments, see, for example, the box entitled “The carry-over effect on annual average real GDP growth”, Monthly Bulletin, ECB, March 2010.

The interpolation method used is a variant of the method described in Chow, G.C. and Lin, A., “Best Linear Unbiased Interpolation, Distribution, and Extrapolation of Time Series by Related Series”, The Review of Economics and Statistics, Vol. 53, No 4, November 1971, pp. 372-375. Specifically, the model treats monthly GDP as an unobserved component in a state-space model and uses the observation equation to ensure that quarterly GDP is the sum of monthly GDP within a given quarter. The regression equation that links monthly GDP to monthly indicator variables is expressed in logarithms, and the regression residual is assumed to follow a random walk. For a related model for the euro area, see “The monthly development of aggregate output in the euro area”, Monthly Report, Deutsche Bundesbank, May 2020.

The indicator for services production refers to the production of services of the business economy. This indicator includes service activities that were most affected by the pandemic, such as accommodation and food services, but excludes trade and financial and insurance services and is only available as of January 2015. For the purposes of this analysis, it is estimated back to 2006 using available historical data for services production.

It should be noted that the monthly input variables are inherently volatile and prone to revisions, which means that the results presented in this box may change in later releases.