The euro area bank lending survey – Second quarter of 2020

Introduction

The results reported in the July 2020 bank lending survey (BLS) relate to changes observed during the second quarter of 2020 and expectations for the third quarter of 2020. The survey was conducted between 5 and 23 June 2020. A total of 144 banks were surveyed in this round, with a response rate of 100%. In addition to results for the euro area as a whole, this report also contains results for the four largest euro area countries.[1]

A number of ad hoc questions were included in the July 2020 survey. They look at the impact that the situation in financial markets has had on banks’ access to retail and wholesale funding, the impact of banks’ non-performing loan (NPL) ratios on lending policies as well as the change in bank lending conditions and loan demand across all main sectors of economic activities.

1 Overview of results

The results of the July BLS show a continued upward impact of the coronavirus

(COVID-19) pandemic on firms’ loan demand, largely driven by emergency liquidity needs. At the same time, banks also reported broadly unchanged credit standards on loans or credit lines to firms in the second quarter of 2020. According to banks, fiscal and monetary policy measures played a significant role for maintaining favourable credit standards for loans to firms. Banks expect credit standards for enterprises to tighten considerably in the third quarter, which is reported to be related to the expected end of state guarantee schemes for loans in some large euro area countries.

Firms’ demand for loans or drawing of credit lines surged further in the second quarter of 2020, reaching the highest net balance since the survey was launched in 2003. The increased demand for working capital connected to emergency liquidity needs and possibly precautionary build-up of liquidity buffers more than offset the negative contribution of demand for fixed investment. Banks expect the net increase in firms’ demand for loans to be lower in the third quarter.

Credit standards for housing loans and consumer credit tightened considerably in the second quarter, related mostly to the deterioration of the economic outlook and worsened borrowers’ creditworthiness. Net demand for housing loans and consumer credit decreased considerably in the second quarter, on account of precautionary savings and low spending possibilities during the strict lockdown period, coupled with uncertainties in the employment situation. Banks expect a continued net tightening of credit standards and a rebound in household loan demand in the third quarter of 2020.

Regarding the impact of non-performing loan (NPL) ratios, banks reported a net tightening impact of NPL ratios on their credit standards and on terms and conditions for loans across all loan categories in the first half of 2020. Over the next six months, they expect an increased net tightening impact for loans to enterprises, housing loans and consumer credit. Risk perceptions and risk aversion were the main drivers of the tightening impact of NPL ratios.

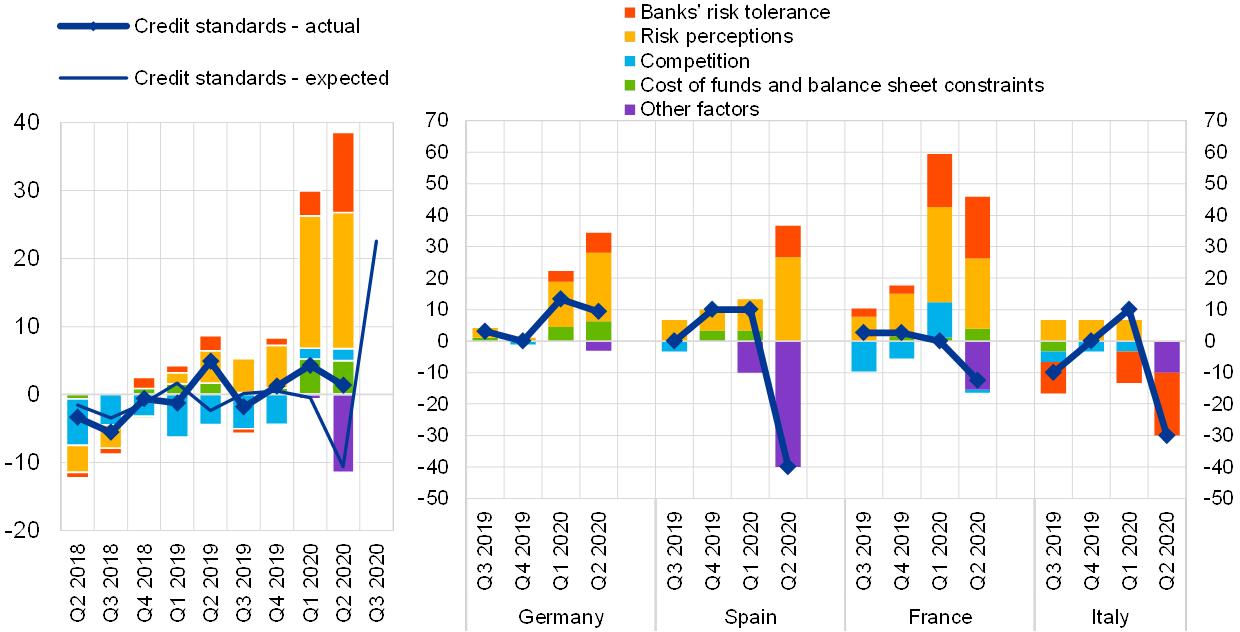

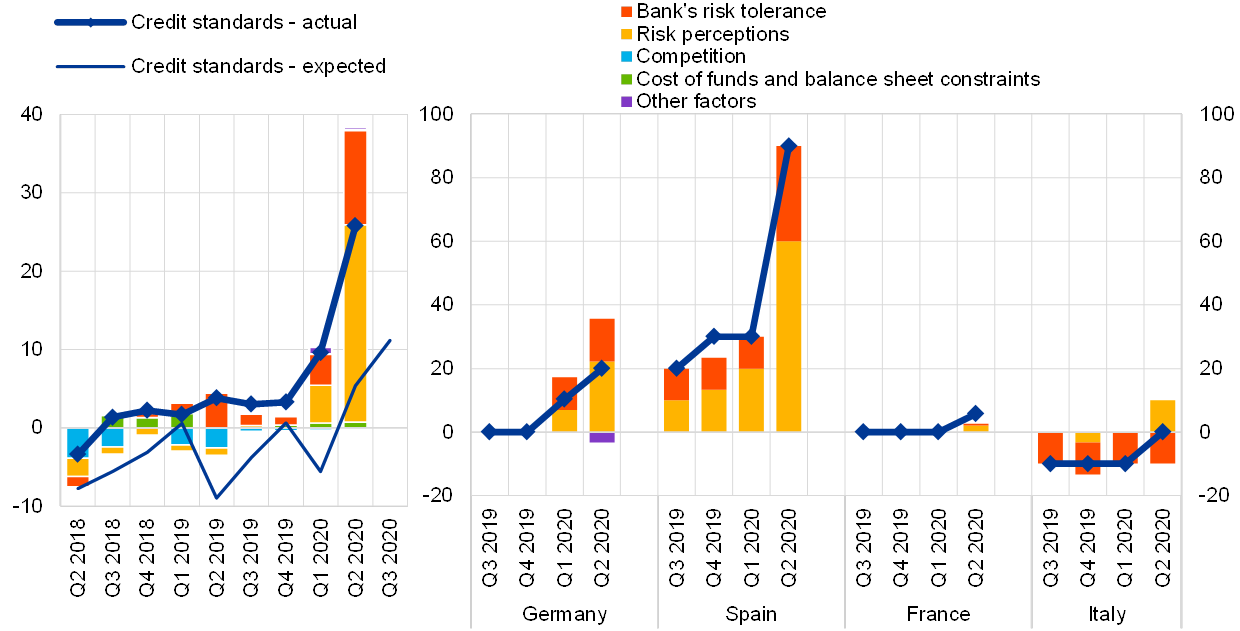

In more detail, credit standards (i.e. banks’ internal guidelines or loan approval criteria) for loans to enterprises remained broadly unchanged in the second quarter of 2020 (net percentage of 1%, after 4% in the first quarter of 2020; see Overview table), compared with expectations of a net easing of credit standards in the previous survey round. In contrast with the previous financial and sovereign debt crises, when credit standards for loans to enterprises tightened significantly, the limited impact of the current crisis could be explained by the sizeable monetary policy measures, fiscal measures, especially loan guarantees provided by governments, and the strengthened capital position of euro area banks. Banks reported a net tightening of credit standards for loans to SMEs (net percentage of 3%), while for large enterprises credit standards remained broadly unchanged (1%). Banks also indicated that their credit standards tightened for long-term loans (11%), while they easing for short-term loans (-6%). Euro area banks expect a considerable net tightening of credit standards on loans to enterprises (net percentage of 23%) in the third quarter of 2020, which is reported to be related to the expected end of state loan guarantee schemes in some large euro area countries.

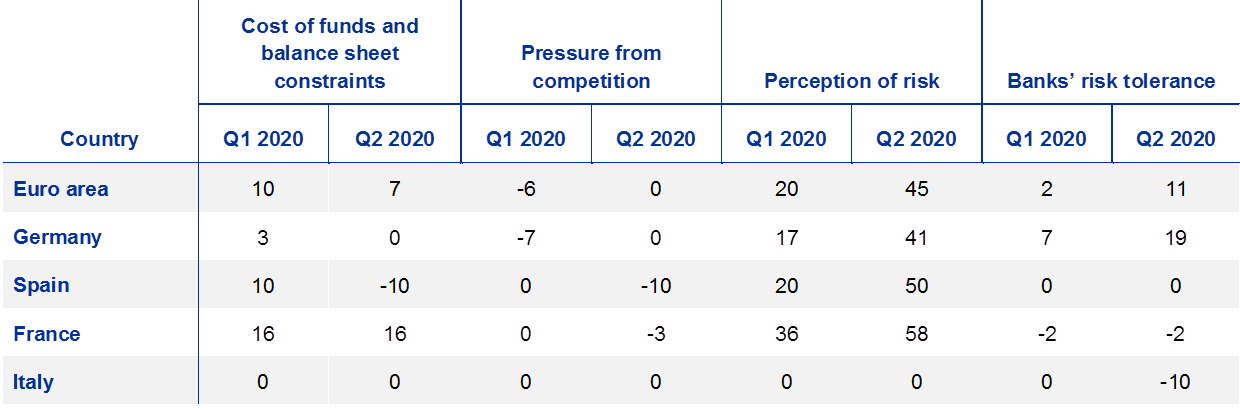

Banks continued to indicate risk perceptions (related to the deterioration in the general economic and firm-specific situation) as the main factor contributing to the tightening of credit standards. Banks also reported lower risk tolerance than in the previous survey round. In addition, costs related to banks’ capital positions and deteriorated market financing conditions had a tightening impact on banks’ credit standards for loans to enterprises. These factors, however, remained moderate overall compared with the values observed during the financial and sovereign debt crises. At the same time, banks reported that government loan guarantees (included in “other factors”) played a significant role in maintaining favourable credit standards. In line with this, risks related to required collateral contributed to an easing of credit standards.

Credit standards for loans to households for house purchase (net percentage of 22%, after 9% in the previous quarter) and for consumer credit and other lending to households (26%, after 10%) tightened considerably in the second quarter of 2020. Banks referred to the deterioration of the economic outlook, worsened creditworthiness of households and housing market prospects, and a lower risk tolerance as the main factors contributing to the tightening. In addition, banks indicated the coronavirus pandemic as a relevant factor contributing to the tightening of credit standards for housing loans. For the third quarter, banks expect a continued net tightening of credit standards for housing loans (21%) and for consumer credit (11%).

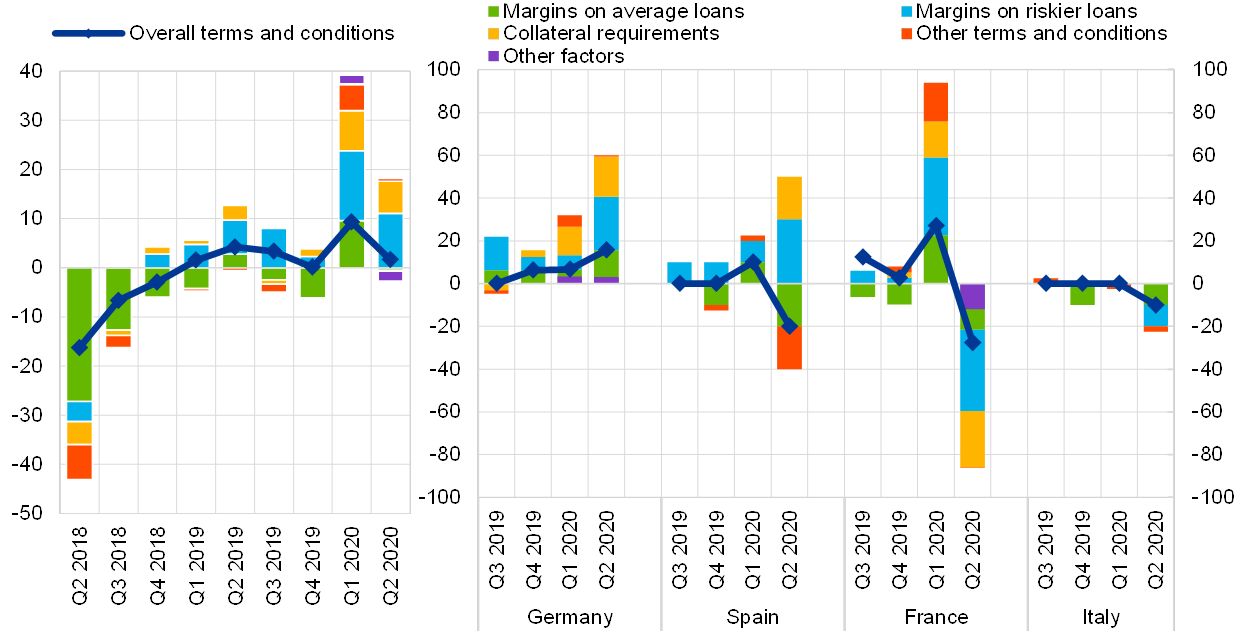

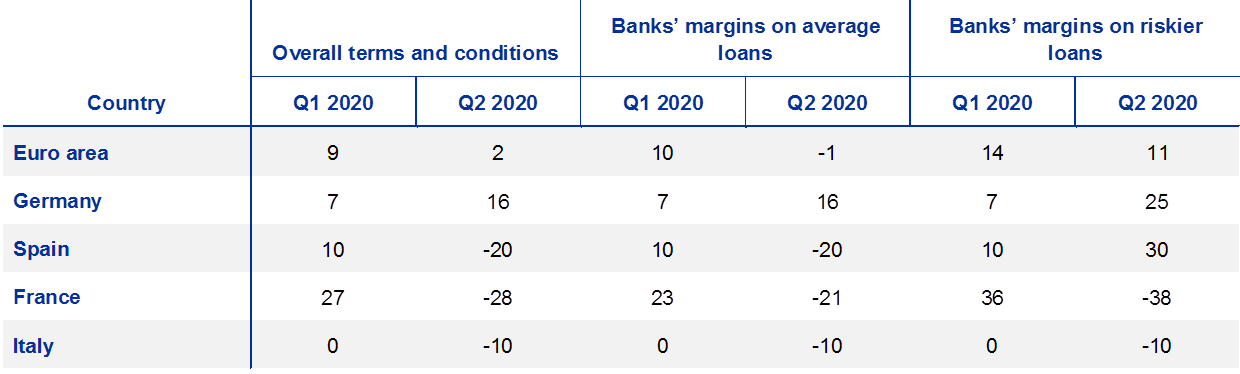

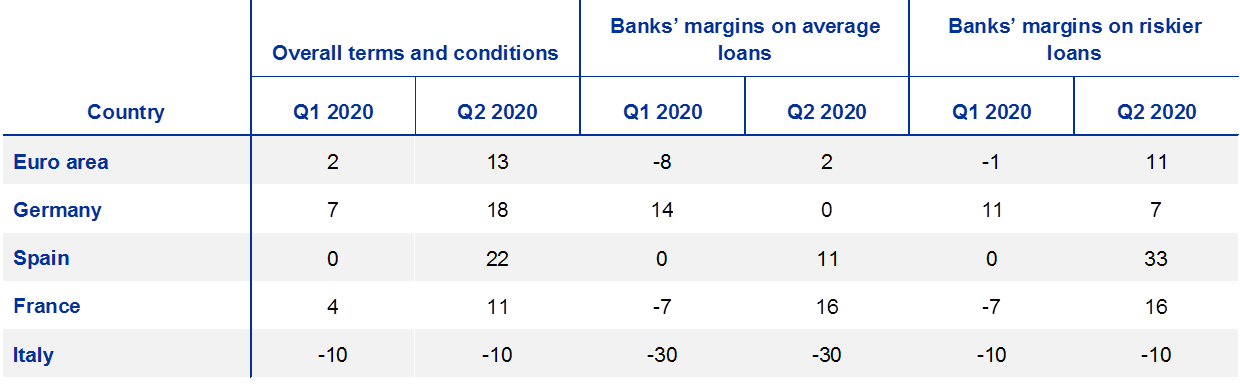

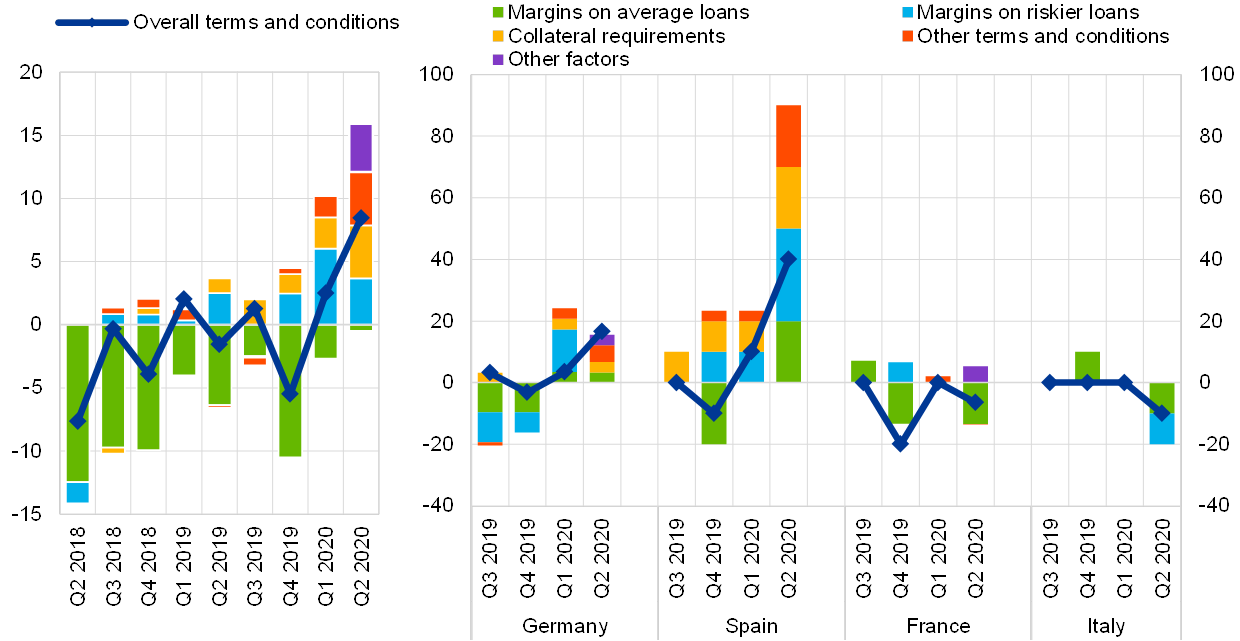

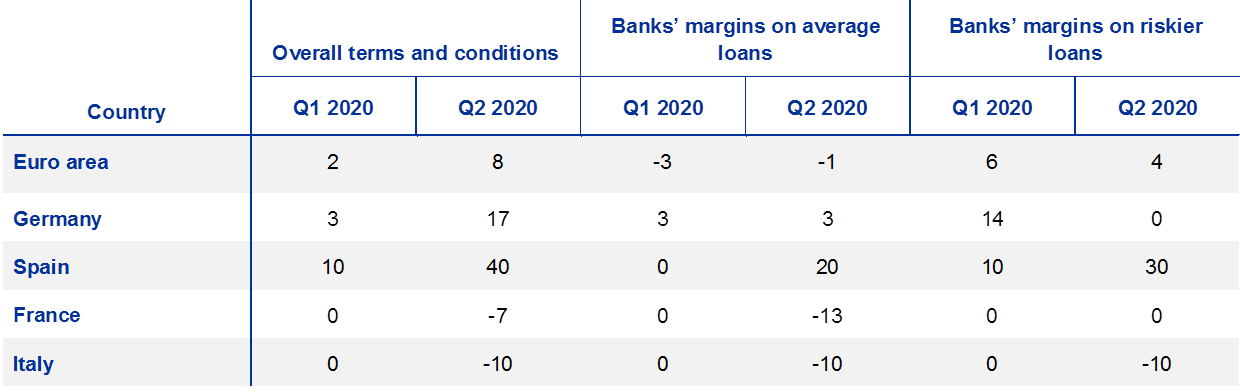

Banks’ overall terms and conditions (i.e. banks’ actual terms and conditions agreed in the loan contract) for new loans to enterprises tightened slightly in the second quarter of 2020 (net percentage of 2%, after 9%). Margins on average loans to firms (defined as the spread over relevant market reference rates) remained broadly unchanged, while margins on riskier loans continued to tighten. Most other terms and conditions, such as collateral requirements, loan covenants and non-interest rate charges tightened, while loan size contributed to an easing in the second quarter. Banks’ overall terms and conditions tightened for housing loans (net percentage of 13%, after 2%) and for consumer credit and other lending to households (8%, after 2%). The net tightening for loans to households was related to wider margins on riskier loans, while for housing loans banks also reported a tightening impact of loan-to-value ratios and other loan size limits.

The rejection rate for loan applications from enterprises decreased, while increasing for housing and consumer credit. Euro area banks reported that the net share of rejected applications for loans to firms decreased (-12%, after 9%), while increasing for housing loans (4%, after 6%) and for consumer credit and other lending to households (15%, after 12%).

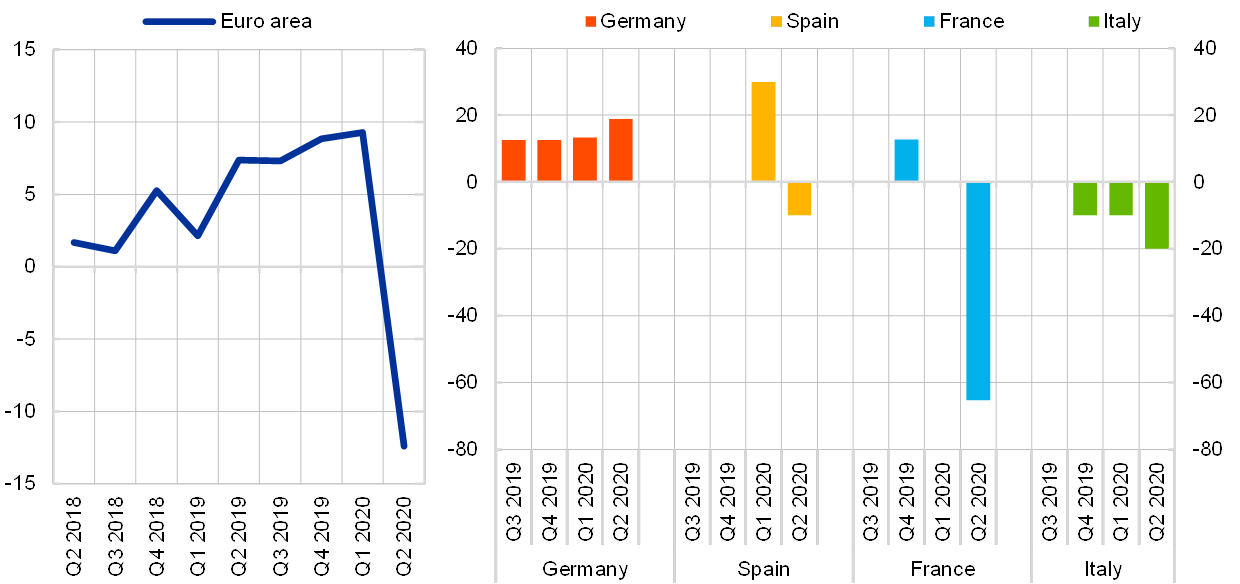

Firms’ demand for loans or drawing of credit lines surged further in the second quarter of 2020, reaching the highest net balance since the start of the survey in 2003 (net percentage of banks reporting an increase in loan demand at 62%, after 26% in the previous quarter; see Overview table). Banks expect that net demand for NFC loans will increase less in the third quarter (net percentage of 11%). Loan demand was higher for SMEs (net percentage of 61%) than for large firms (47%) and significantly higher for short-term loans (net percentage of 60%) than for long-term loans (11%). This shows particularly strong emergency liquidity needs of firms and possibly a precautionary build-up of liquidity buffers in the second quarter of 2020, when the lockdown measures were widespread across euro area countries. In line with this, banks reported that financing needs for inventories and working capital was the main factor underlying firms’ loan demand, which more than offset the negative contribution from fixed investment for loan demand. In addition, other financing needs, such as debt refinancing/restructuring, supported firms’ loan demand. At the same time, financing needs for mergers and acquisitions and the general level of interest rates dampened firms’ loan demand.

By contrast, net demand for housing loans declined strongly in the second quarter (net percentage of banks of -61%, after 12% in the previous quarter); however, the net percentage of banks reporting a decline in loan demand was somewhat smaller than in the second half of 2008, when Lehman Brothers collapsed. The net demand for consumer credit and other lending to households reached a record low (net percentage of -76%, after -4%) in the second quarter of 2020. Banks expect an increase in net demand for housing loans (6%) and in particular for consumer credit (30%) in the third quarter of 2020. A strong decline in housing loan demand was driven mainly by lower consumer confidence in the context of the coronavirus pandemic and, to a lesser extent, worsened housing market prospects. For consumer credit, all factors contributed to the decline in demand, especially lower consumer confidence and decreased spending on durable goods, in line with precautionary savings and low spending possibilities during the strict lockdown period as well as uncertainties on the employment situation.

Across the largest euro area countries, credit standards on loans to enterprises tightened in Germany in the second quarter of 2020, while easing in Spain, Italy and France (see Overview table). Banks in Spain, Italy and France reported that government loan guarantees (included in “other factors”) played a significant role in maintaining favourable credit standards for loans to firms, while banks in Germany mentioned that firms’ demand for loans guaranteed by governments was lower overall than expected. For housing loans and consumer credit, credit standards tightened in Germany, France and Spain, but remained unchanged in Italy.

Net demand for loans to enterprises increased considerably in all the largest euro area countries in the second quarter of 2020. The opposite development was observed for housing loans and consumer credit, for which net demand decreased strongly in almost all euro area countries.

Overview table

Latest BLS results for the largest euro area countries

(net percentages of banks reporting a tightening of credit standards or an increase in loan demand)

Notes: The “Avg.” columns contain historical averages, which are calculated over the period since the beginning of the survey, excluding the most recent round. For France, net percentages are weighted on the basis of outstanding loan amounts for individual banks in the respective national samples. Owing to different sample sizes across countries, which broadly reflect the differences in the national shares in lending to the euro area non-financial private sector, the size and volatility of the net percentages cannot be directly compared across countries.

The July 2020 BLS also included a number of ad hoc questions. Regarding euro area banks’ access to retail and wholesale funding, banks reported in net terms that access to retail funding improved in the second quarter of 2020, while access continued to deteriorate for debt securities, securitisation and money markets.

Euro area banks reported a net tightening impact of NPL ratios on their credit standards and on terms and conditions for loans across all loan categories in the first half of 2020. They expect an increased net tightening impact for loans to enterprises, housing loans and consumer credit over the next six months. Risk perceptions and risk aversion related to the general economic outlook and borrowers’ creditworthiness were the main drivers of the tightening impact of NPL ratios.

Firms’ net demand for loans or credit lines increased strongly in manufacturing, trade and services sectors in the first half of 2020, while the increase in demand was negligible in the real estate sector. Euro area banks reported a net tightening of credit standards and somewhat stronger net tightening of terms and conditions for new loans to enterprises across all main sectors of economic activities over the past six months. Banks expect that credit standards and terms and conditions will continue to tighten further for new loans to firms in all main economic sectors in the second half of 2020.

Box 1

General notes

The bank lending survey (BLS) is addressed to senior loan officers at a representative sample of euro area banks. In the current round, 144 banks were surveyed, representing all euro area countries and reflecting the characteristics of their respective national banking structures. The main purpose of the BLS is to enhance the Eurosystem’s knowledge of bank lending conditions in the euro area.[2]

BLS questionnaire

The BLS questionnaire contains 22 standard questions on past and expected future developments: 18 backward-looking questions and four forward-looking questions. In addition, it contains one open-ended question. Those questions focus on developments in loans to euro area residents (i.e. domestic and euro area cross-border loans) and distinguish between three loan categories: loans or credit lines to enterprises; loans to households for house purchase; and consumer credit and other lending to households. For all three categories, questions are asked about the credit standards applied to the approval of loans, the terms and conditions of new loans, loan demand, the factors affecting loan supply and demand conditions, and the percentage of loan applications that are rejected. Survey questions are generally phrased in terms of changes over the past three months or expected changes over the next three months. Survey participants are asked to indicate in a qualitative way the strength of any tightening or easing or the strength of any decrease or increase, reporting changes using the following five-point scale: (1) tightened/decreased considerably, (2) tightened/decreased somewhat, (3) basically no change, (4) eased/increased somewhat or (5) eased/increased considerably.

In addition to the standard questions, the BLS questionnaire may contain ad hoc questions on specific topics of interest. Whereas the standard questions cover a three-month time period, the ad hoc questions tend to refer to changes over a longer time period (e.g. over the past and next six months).

Aggregation of banks’ replies to national and euro area BLS results

The responses of the individual banks participating in the BLS are aggregated in two steps. In the first step, the responses of individual banks are aggregated to form national results for euro area countries. And in the second step, those national BLS results are aggregated to form euro area BLS results.

In the first step, banks’ replies can be aggregated to form national BLS results by applying equal weights to all banks in the sample[3] or, alternatively, by applying a weighting scheme based on outstanding loans to non-financial corporations and households for the individual banks in the respective national samples. Specifically, for France, Malta, the Netherlands and Slovakia, an explicit weighting scheme is applied.

In the second step, since the numbers of banks in the national samples differ considerably and do not always reflect those countries’ respective shares of lending to euro area non-financial corporations and households, the national survey results are aggregated to form euro area BLS results by applying a weighting scheme based on national shares of outstanding loans to euro area non-financial corporations and households.

BLS indicators

Responses to questions relating to credit standards are analysed in this report by looking at the difference (the “net percentage”) between the percentage of banks reporting that credit standards applied in the approval of loans have been tightened and the percentage of banks reporting that they have been eased. For all questions, the net percentage is determined on the basis of all participating banks that have business in or exposure to the respective loan categories (i.e. they are all included in the denominator when calculating the net percentage). This means that banks that specialise in certain loan categories (e.g. banks that only grant loans to enterprises) are only included in the aggregation for those categories. All other participating banks are included in the aggregation of all questions, even if a bank replies that a question is “not applicable” (“NA”). This harmonised aggregation method was introduced by the Eurosystem in the April 2018 BLS. It has been applied to all euro area and national BLS results in the current BLS questionnaire, including backdata.[4] The resulting revisions for the standard BLS questions have generally been small, but revisions for some ad hoc questions have been larger owing to a higher number of “not applicable” replies by banks.

A positive net percentage indicates that a larger proportion of banks have tightened credit standards (“net tightening”), whereas a negative net percentage indicates that a larger proportion of banks have eased credit standards (“net easing”).

Likewise, the term “net demand” refers to the difference between the percentage of banks reporting an increase in loan demand (i.e. an increase in bank loan financing needs) and the percentage of banks reporting a decline. Net demand will therefore be positive if a larger proportion of banks have reported an increase in loan demand, whereas negative net demand indicates that a larger proportion of banks have reported a decline in loan demand.

In the assessment of survey balances for the euro area, net percentages between -1 and +1 are generally referred to as “broadly unchanged”. For country results, net percentage changes are reported in a factual manner, as differing sample sizes across countries mean that the answers of individual banks have differing impacts on the magnitude of net percentage changes.

In addition to the “net percentage” indicator, the ECB also publishes an alternative measure of banks’ responses to questions relating to changes in credit standards and net demand. This measure is the weighted difference (“diffusion index”) between the percentage of banks reporting that credit standards have been tightened and the percentage of banks reporting that they have been eased. Likewise, as regards demand for loans, the diffusion index refers to the weighted difference between the percentage of banks reporting an increase in loan demand and the percentage of banks reporting a decline. The diffusion index is constructed in the following way: lenders who have answered “considerably” are given a weight (score of 1) which is twice as large as that given to lenders who have answered “somewhat” (score of 0.5). The interpretation of the diffusion indices follows the same logic as the interpretation of net percentages.

Detailed tables and charts based on the responses provided can be found in Annex 1 for the standard questions and Annex 2 for the ad hoc questions. In addition, BLS time series data are available on the ECB’s website via the Statistical Data Warehouse.

A copy of the questionnaire, a glossary of BLS terms and a BLS user guide with information on the BLS series keys can all be found at: https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html

2 Developments in credit standards, terms and conditions, and net demand for loans in the euro area

2.1 Loans to enterprises

2.1.1 Credit standards for loans to enterprises remained broadly unchanged

Credit standards (i.e. banks’ internal guidelines or loan approval criteria) for loans to enterprises remained broadly unchanged in the second quarter of 2020 (net percentage of 1%, after 4% in the first quarter of 2020; see Chart 1 and Overview table). At the same time, the dispersion of banks’ answers reached the highest value on record. The net percentage remained below the historical average since 2003 (8%). In contrast with the previous financial and sovereign debt crises, when credit standards for loans to firms tightened significantly, the limited impact of the current crisis could be explained by the sizeable monetary policy measures, fiscal measures, especially loan guarantees provided by governments, as well as by the strengthened capital position of euro area banks.

Chart 1

Changes in credit standards applied to the approval of loans or credit lines to enterprises, and contributing factors

(net percentages of banks reporting a tightening of credit standards and contributing factors)

Notes: “Actual” values are changes that have occurred, while “expected” values are changes anticipated by banks. Net percentages are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. The net percentages for responses to questions related to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to a tightening and the percentage reporting that it contributed to an easing. “Cost of funds and balance sheet constraints” is the unweighted average of “costs related to capital position”, “access to market financing” and “liquidity position”; “risk perceptions” is the unweighted average of “general economic situation and outlook”, “industry or firm-specific situation and outlook/borrower’s creditworthiness” and “risk related to the collateral demanded”; “competition” is the unweighted average of “competition from other banks”, “competition from non-banks” and “competition from market financing”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards, currently mainly related to the policy interventions in response to the COVID-19 pandemic.

Banks reported a net tightening of credit standards for loans to SMEs (net percentage of 3%), while for large enterprises credit standards remained broadly unchanged (1%). Banks also indicated that their credit standards tightened for long-term loans (11%), while easing for short-term loans (-6%).

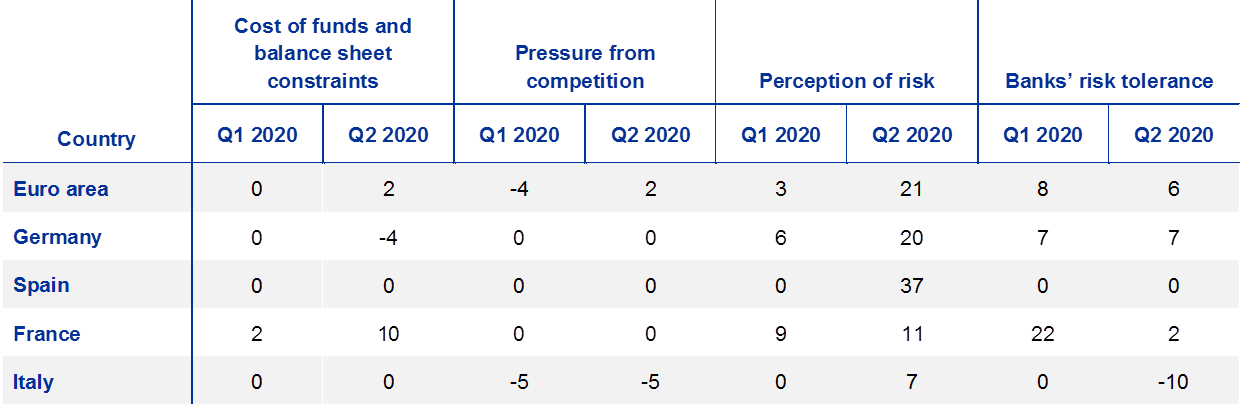

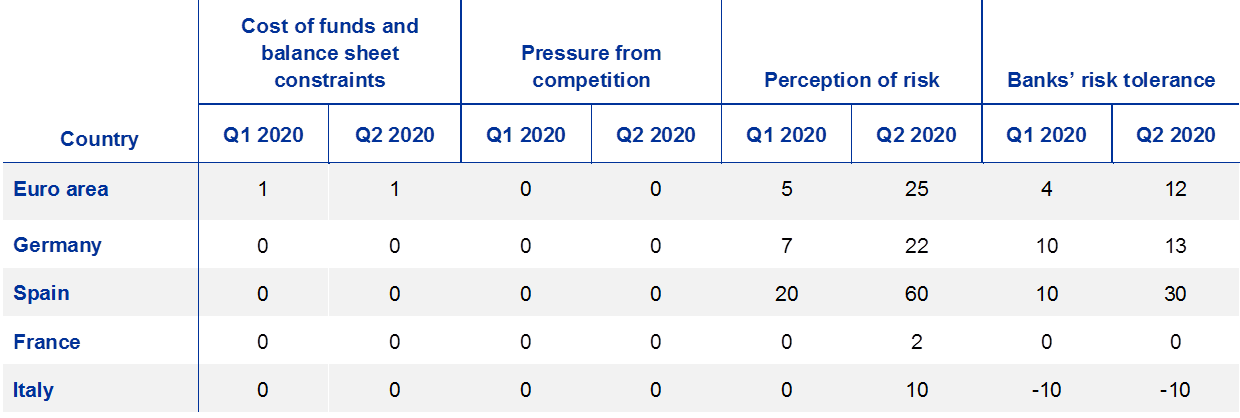

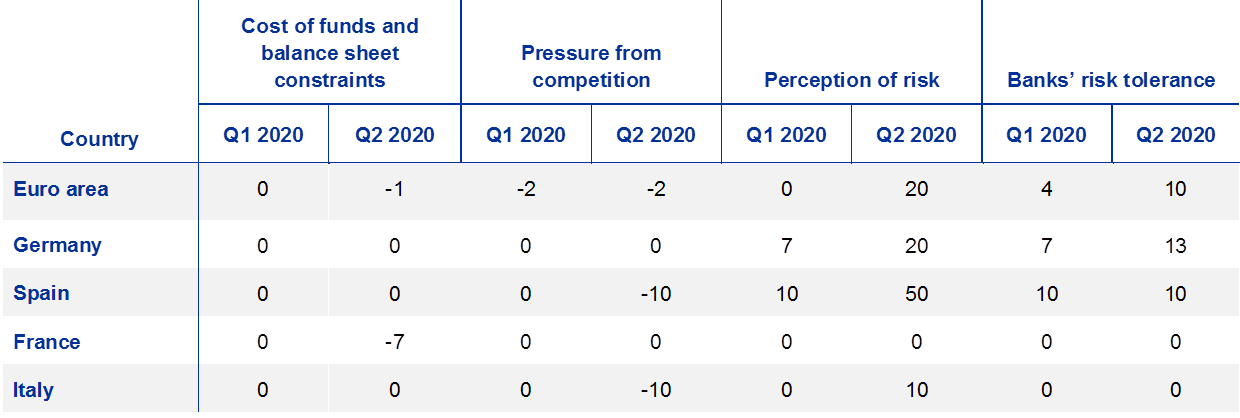

Banks continued to indicate risk perceptions (related to the deterioration in the general economic and firm-specific situation) as the main factor contributing to the tightening of credit standards (see Chart 1 and Table 1). Banks also reported lower risk tolerance than in the previous survey round. In addition, costs related to banks’ capital position and deteriorated market financing conditions had a tightening impact on banks’ credit standards for loans to enterprises. At the same time, banks reported that government loan guarantees (the main driver of the “other factors”) played a significant role in maintaining favourable credit standards. In line with this, risks related to required collateral contributed to an easing of credit standards.

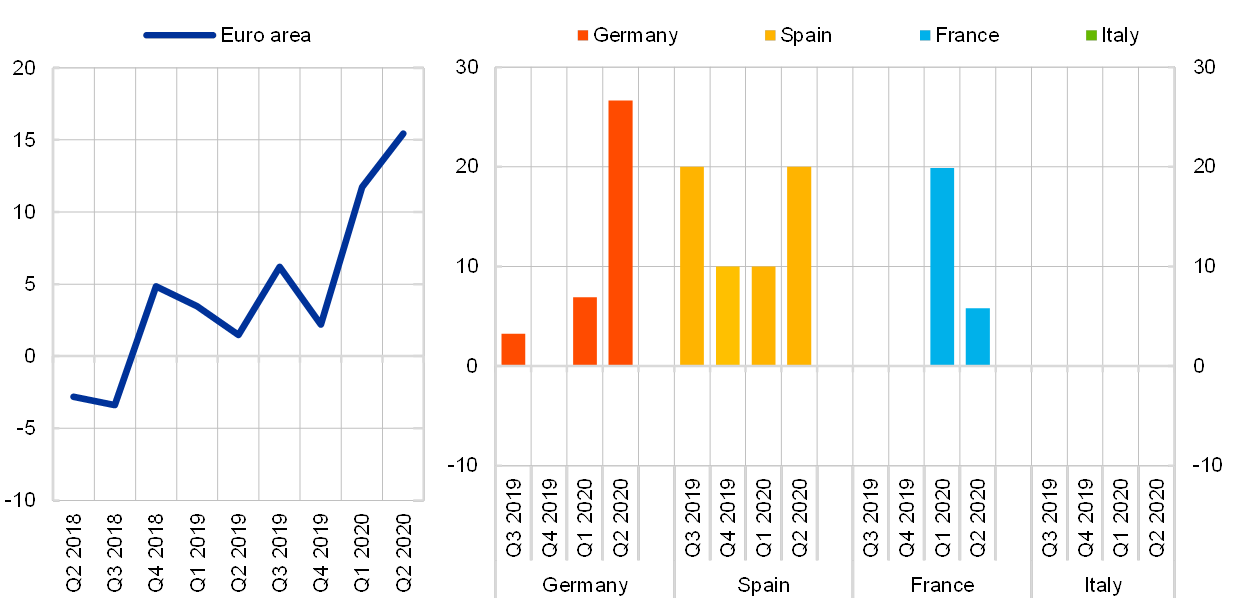

Across the largest euro area countries, credit standards on loans to enterprises tightened in Germany in the second quarter of 2020, while easing in France and especially in Italy and Spain. Banks in Germany referred to higher risk perceptions and, to a lesser extent, lower risk tolerance and cost of funds and balance sheet constraints as relevant factors for the tightening of their credit standards. Banks in Germany also mentioned that firms’ demand for loans guaranteed by governments was overall lower than expected. By contrast, banks in France and Spain reported that the positive impact of government loan guarantee schemes (included in “other factors”) outweighed, in net terms, the negative impact of higher risk perceptions and lower banks’ risk tolerance. A net easing of credit standards in Italy was supported by banks’ higher risk tolerance and government support measures for loans to SMEs.

Euro area banks expect a considerable net tightening of credit standards for loans to firms (net percentage of 23%) in the third quarter of 2020, which is reported to be related to the expected end of state guarantee schemes in some large euro area countries. At the same time, banks’ expectations should be interpreted with some caution as the uncertainty of the impact of the coronavirus pandemic still remains high. It is reflected in the dispersion of banks’ responses, which remained at the levels last seen during the global financial crisis.

Table 1

Factors contributing to changes in credit standards for loans or credit lines to enterprises

(net percentages of banks)

Note: See the notes to Chart 1.

2.1.2 Terms and conditions on loans to enterprises slightly tightened

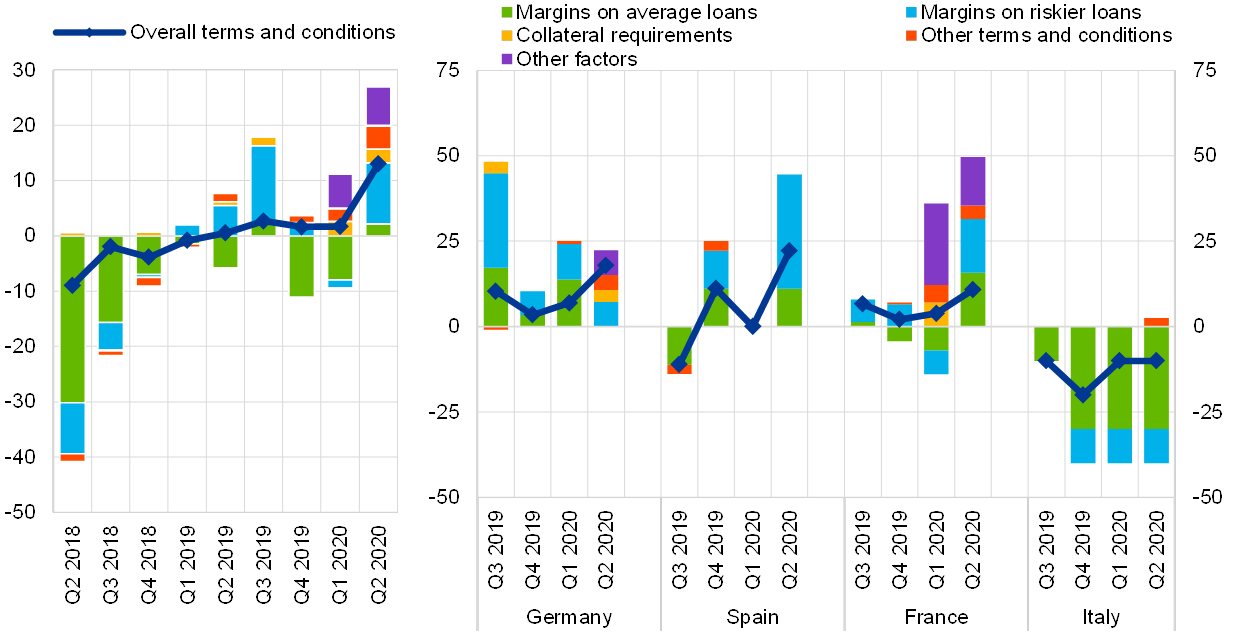

Banks’ overall terms and conditions (i.e. banks’ actual terms and conditions agreed in the loan contract) for new loans to enterprises slightly tightened in the second quarter of 2020 (net percentage of 2%, after 9% in the previous quarter). Margins on average loans to firms (defined as the spread over relevant market reference rates) remained broadly unchanged, while margins on riskier loans continued to tighten. Most of other terms and conditions, such as collateral requirements, loan covenants and non-interest rate charges, tightened, while loan size contributed to an easing in the second quarter (see Chart 2 and Table 2).

Chart 2

Changes in terms and conditions on loans or credit lines to enterprises

(net percentages of banks reporting a tightening of terms and conditions)

Notes: “Margins” are defined as the spread over a relevant market reference rate. “Other terms and conditions” is the unweighted average of “non-interest rate charges”, “size of the loan or credit line”, “loan covenants” and “maturity”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards, currently mainly related to the policy interventions in response to the COVID-19 pandemic.

Risk perceptions continued to be the main contributor to the net tightening of overall terms and conditions (see Table 3). To a smaller extent, banks’ lower risk tolerance and banks’ cost of funds and balance sheet constraints also contributed to the tightening.

Across the largest euro area countries, overall terms and conditions on new loans or credit lines to enterprises tightened in Germany, while easing in France, Spain and Italy. This was in line with the developments of banks’ credit standards for loans to firms. The tightening in Germany was related to wider loan margins and higher collateral requirements, while the opposite was reported by banks in France. Banks in Spain reported that narrower margins on average loans and other terms and conditions such as loan size and maturity outweighed wider margins on riskier loans and stricter collateral requirements. A net easing of terms and conditions in Italy was driven by narrower loan margins.

Table 2

Changes in terms and conditions on loans or credit lines to enterprises

(net percentages of banks)

Note: See the notes to Chart 2.

Table 3

Factors contributing to changes in overall terms and conditions on loans or credit lines to enterprises

(net percentages of banks)

Note: The net percentages for these questions relating to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to a tightening and the percentage reporting that it contributed to an easing.

2.1.3 Rejection rate for loans to enterprises decreased

The rejection rate for loans to euro area enterprises decreased considerably in the second quarter of 2020 (-12%, after 9% in the previous survey round; see Chart 3).

Chart 3

Changes in the rejection rate for loans to enterprises

(net percentages of banks reporting an increase in the share of rejections)

Notes: The net percentages of rejected loan applications are defined as the difference between the percentages of banks reporting an increase in the share of loan rejections and the percentages of banks reporting a decline. Banks’ responses refer to the share of rejected loan applications relative to the total volume of applications in that loan category.

The pronounced decline in the share of rejected loan applications for loans to enterprises could also be explained by the sizeable state loan guarantees provided by the euro area governments.

Across the largest euro area countries, the net rejection rate decreased in Italy, Spain and especially in France, while increasing in Germany.

2.1.4 Net demand for loans to enterprises surged further

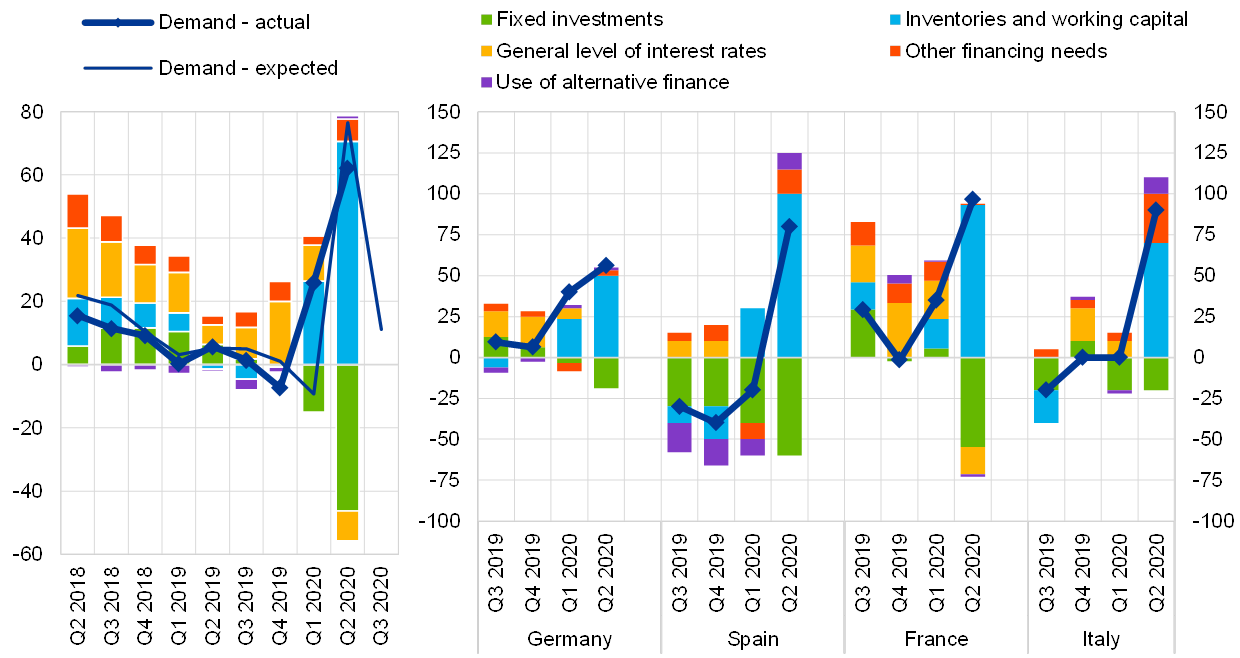

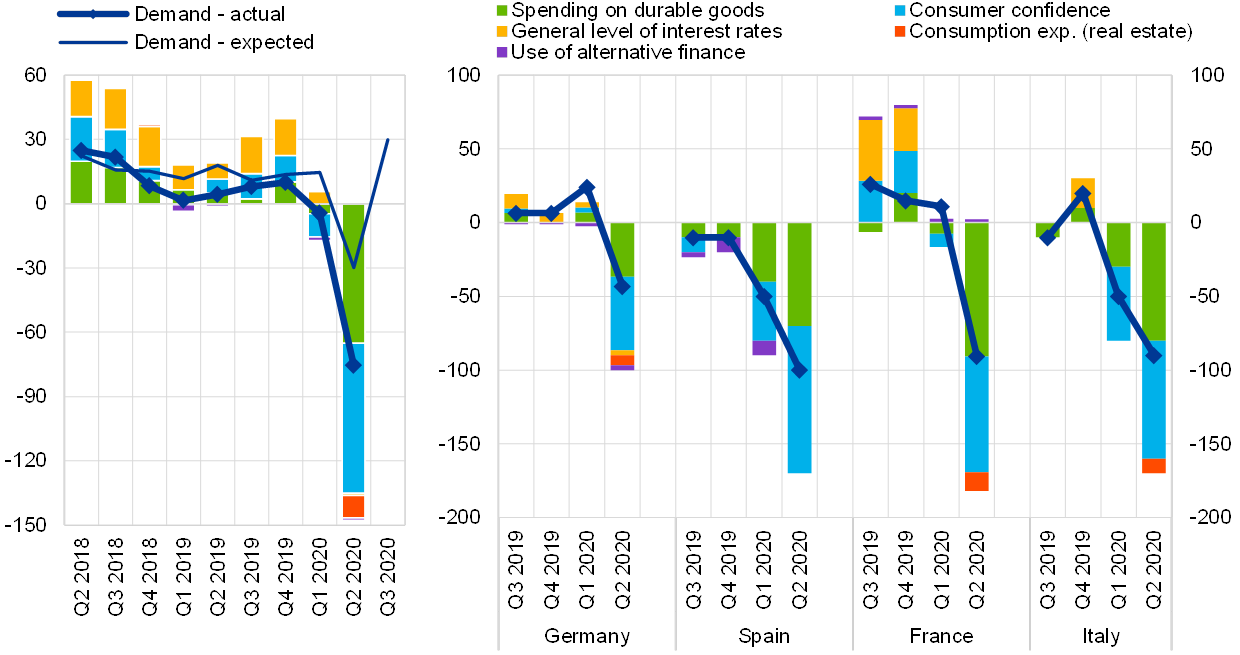

Firms’ demand for loans or drawing of credit lines surged further in the second quarter of 2020, reaching the highest net balance since the survey was launched in 2003 (a net percentage of banks reporting an increase in loan demand of 62%, after 26% in the first quarter of 2020; see Chart 4 and Overview table). This shows particularly strong emergency liquidity needs of firms and possibly precautionary build-up of liquidity buffers in the second quarter of 2020, when the lockdown measures were widespread across the euro area countries. Firms have also continued to draw previously and newly committed credit lines. In addition, the dispersion in banks’ responses increased further to the highest level since the survey was launched, which is reflected in the opposing developments in loan demand for short-term emergency liquidity and long-term investment.

Chart 4

Changes in demand for loans or credit lines to enterprises and contributing factors

(net percentages of banks reporting an increase in demand and contributing factors)

Notes: “Actual” values are changes that have occurred, while “expected” values are changes anticipated by banks. Net percentages for the questions on demand for loans are defined as the difference between the sum of the percentages of banks responding “increased considerably” and “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” and “decreased considerably”. The net percentages for responses to questions relating to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to increasing demand and the percentage reporting that it contributed to decreasing demand. “Other financing needs” is the unweighted average of “mergers/acquisitions and corporate restructuring” and “debt refinancing/restructuring and renegotiation”; “use of alternative finance” is the unweighted average of “internal financing”, “loans from other banks”, “loans from non-banks”, “issuance/redemption of debt securities” and “issuance/redemption of equity”.

Loan demand was higher for SMEs (net percentage of 61%), which tend to be highly bank-dependent, than for large firms (47%) and significantly higher for short-term loans (net percentage of 60%) than for long-term loans (11%). In line with this, banks reported that financing needs for inventories and working capital was the main factor underlying firms’ loan demand, which more than offset the negative contribution from fixed investment for loan demand. In addition, other financing needs, such as debt refinancing/restructuring, supported firms’ loan demand. By contrast, financing needs for M&As and general level of interest rates dampened firms’ loan demand (see Chart 4 and Table 4).[5]

Table 4

Factors contributing to changes in demand for loans or credit lines to enterprises

(net percentages of banks)

Note: See the notes to Chart 4.

A strong increase in net demand for loans to enterprises was reported by banks in all largest euro area countries. The increase was driven by acute liquidity needs for inventories and working capital, while banks in Germany and in particular Spain and Italy indicated that debt refinancing/restructuring (included in other financing needs) also supported firms’ loan demand. A pronounced decline in financing needs for fixed investment was reported by all the largest euro area countries.

Banks expect that net demand for loans to firms will increase less in the third quarter of 2020 (net percentage of 11%).

2.2 Loans to households for house purchase

2.2.1 Credit standards for loans to households for house purchase tightened further

Credit standards for loans to households for house purchase tightened further in the second quarter of 2020 (22%, after 9%; see Chart 5 and Overview table). The net percentage has been well above the historical average since 2003 (5%), and the second quarter saw the strongest net tightening since the fourth quarter of 2011.

Banks referred to risk perceptions related to the general economic outlook, borrowers’ creditworthiness and housing market prospects as the most important factor for the tightening. Banks also indicated lower risk tolerance and the coronavirus pandemic (included in “other factors”) as relevant factors contributing to the tightening. In addition, competition from non-banks and banks’ cost of funds and balance sheet situation had a small tightening impact on banks’ credit standards for housing loans (see Chart 5 and Table 5).

Chart 5

Changes in credit standards applied to the approval of loans to households for house purchase, and contributing factors

(net percentages of banks reporting a tightening of credit standards and contributing factors)

Notes: See the notes to Chart 1. “Risk perceptions” is the unweighted average of “general economic situation and outlook”, “housing market prospects, including expected house price developments” and “borrower’s creditworthiness”; “competition” is the unweighted average of “competition from other banks” and “competition from non-banks”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards. For France, this mainly relates to macroprudential policy recommendations.

Across the largest euro area countries, credit standards tightened in Germany, France and Spain, but remained unchanged in Italy. Banks in Germany and Spain referred to higher risk perceptions related to the general economic outlook, borrowers’ creditworthiness and housing market prospects as the main factor contributing to the tightening of credit standards. Banks in France indicated higher risk perceptions and cost of funds and balance sheet situation as having a tightening impact. They have also continued to refer to the macroprudential recommendations by the French High Council for Financial Stability in December 2019, according to which banks were asked to tighten their lending conditions for mortgage credit, as a relevant tightening factor. By contrast, banks in Italy indicated no changes in credit standards on housing loans in the second quarter of 2020.

Table 5

Factors contributing to changes in credit standards for loans to households for house purchase

(net percentages of banks)

Note: See the notes to Chart 5.

Looking ahead, euro area banks expect a continued strong net tightening of credit standards for housing loans (net percentage of 21%) in the third quarter of 2020.

2.2.2 Terms and conditions on loans to households for house purchase tightened

Banks’ overall terms and conditions tightened for housing loans (net percentage of 13%, after 2% in the previous quarter). The net tightening was mainly related to a widening of margins on riskier loans and a tightening impact of loan-to-value ratios and other loan size limits. Banks also mentioned other factors, mainly related to the coronavirus pandemic, as relevant for the tightening. In addition, margins on average loans and collateral requirements tightened slightly (see Chart 6 and Table 6).

Chart 6

Changes in terms and conditions on loans to households for house purchase

(net percentages of banks reporting a tightening of terms and conditions)

Notes: “Margins” are defined as the spread over a relevant market reference rate. “Other terms and conditions” is the unweighted average of “loan-to-value ratio”, “other loan size limits”, “non-interest rate charges” and “maturity”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards. For France, this mainly relates to macroprudential policy recommendations.

Higher risk perceptions and lower risk tolerance had a main tightening impact on overall terms and conditions on housing loans at the euro area level. In addition, banks reported a small tightening impact from banks’ cost of funds and balance sheet situation. At the same time, competitive pressures had an easing impact (see Table 7).

Across the largest euro area countries, banks in Germany, France and Spain reported a net tightening of overall terms and conditions on housing loans, while banks in Italy reported an easing. Banks in Germany indicated wider margins on riskier loans, loan-to-value ratios, other loan size limits and collateral requirements as the main factors contributing to the tightening, while banks in Spain and France referred mainly to wider loan margins on both average and riskier loans. In addition, the macroprudential recommendations of the French High Council for Financial Stability continued to have a tightening impact in France, but less than in the previous quarter.

Table 6

Changes in terms and conditions on loans to households for house purchase

(net percentages of banks)

Note: See the notes to Chart 6.

Table 7

Factors contributing to changes in overall terms and conditions on loans to households for house purchase

(net percentages of banks)

Note: The net percentages for these questions relating to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to a tightening and the percentage reporting that it contributed to an easing.

2.2.3 Rejection rate for housing loans increased

A net percentage of 4% of banks reported an increase in the share of rejected loan applications for housing loans in the second quarter of 2020 (after 6% in the previous survey round; see Chart 7).

Across the largest euro area countries, the rejection rate for housing loans increased in Germany and slightly in France, while declining in Italy and Spain.

Chart 7

Changes in the rejection rate for loans to households for house purchase

(net percentages of banks reporting an increase in the share of rejections)

Notes: Net percentages of rejected loan applications are defined as the difference between the percentages of banks reporting an increase in the share of loan rejections and the percentages of banks reporting a decline. Banks’ answers refer to the share of rejected loan applications relative to the total volume of applications in that loan category.

2.2.4 Net demand for housing loans declined strongly

Net demand for housing loans declined strongly in the second quarter of 2020

(-61%, after 12% in the previous quarter; see Chart 8 and Overview table), i.e. the share of banks indicating a decline in loan demand compared with the share of banks reporting an increase in loan demand was much higher. The decline in net loan demand was smaller than expected by banks in the previous survey round and somewhat smaller than in the second half of 2008, when Lehman Brothers collapsed.

Chart 8

Changes in demand for loans to households for house purchase, and contributing factors

(net percentages of banks reporting an increase in demand and contributing factors)

Notes: See the notes to Chart 4. “Other financing needs” is the unweighted average of “debt refinancing/restructuring and renegotiation” and “regulatory and fiscal regime of housing markets”; “use of alternative finance” is the unweighted average of “internal finance of house purchase out of savings/down payment”, “loans from other banks” and “other sources of external finance”.

The strong decline in housing loan demand was driven mainly by lower consumer confidence in the context of the coronavirus pandemic and, to a lesser extent, worsened housing market prospects. By contrast, low general level of interest rates and other financing needs, such as debt refinancing/restructuring, supported housing loan demand. The use of alternative sources of finance continued to have a slightly negative effect on demand, on account of loans from other banks and internal financing from household savings (see Chart 8 and Table 8).

Banks in all the largest euro area countries reported a strong decrease in demand for housing loans. This was largely driven by lower consumer confidence, with banks referring explicitly to the negative impact of the coronavirus pandemic on households. The impact of housing market prospects continued to be negative in most of the largest euro area countries, except Germany, where it remained positive. Also, banks in Italy and Spain indicated that other financing needs, such as debt refinancing/restructuring, supported housing loan demand.

Banks expect an increase in net demand for housing loans to increase in the third quarter (net percentage of 6%). The dispersion in banks’ responses remains at levels last seen in 2009, which indicates high uncertainty.

Table 8

Factors contributing to changes in demand for loans to households for house purchase

(net percentages of banks)

Note: See the notes to Chart 8.

2.3 Consumer credit and other lending to households

2.3.1 Credit standards for consumer credit and other lending to households tightened considerably

Credit standards for consumer credit and other lending to households tightened considerably in the second quarter of 2020 (26%, after 10% in the previous quarter; see Chart 9 and Overview table). This was the strongest net tightening since the first quarter of 2009 and well above the historical average since 2003 (4%).

Chart 9

Changes in credit standards applied to the approval of consumer credit and other lending to households, and contributing factors

(net percentages of banks reporting a tightening of credit standards and contributing factors)

Notes: See the notes to Chart 1. “Risk perceptions” is the unweighted average of “general economic situation and outlook”, “creditworthiness of consumers” and “risk on the collateral demanded”; “competition” is the unweighted average of “competition from other banks” and “competition from non-banks”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards.

Strongly increased risk perceptions related to the deterioration of the economic outlook and worsened creditworthiness of households, coupled with lower risk tolerance of banks, were the main factors contributing to the tightening of credit standards on consumer credit in the second quarter of 2020 (see Chart 9 and Table 9).

Across the largest euro area countries, credit standards for consumer credit and other lending to households tightened in Germany, France and especially Spain, while remaining unchanged in Italy. The reported tightening in Spain and Germany was mainly related to higher risk perceptions and lower risk tolerance of banks, while tightening in France was driven by higher risk perceptions.

Looking ahead to the third quarter of 2020, euro area banks expect a continued, albeit smaller, net tightening of credit standards for consumer credit and other lending to households (11%).

Table 9

Factors contributing to changes in credit standards for consumer credit and other lending to households

(net percentages of banks)

Note: See the notes to Chart 9.

2.3.2 Terms and conditions on consumer credit and other lending to households tightened

Banks’ overall terms and conditions applied when granting new consumer credit and other lending to households tightened further in the second quarter of 2020 (net percentage of 8%, after 2% in the previous quarter). The net tightening was driven by wider margins on riskier loans and other terms and conditions, such as loan size, maturity and collateral requirements. Banks also mentioned other factors, mainly related to the coronavirus pandemic, as relevant for the tightening. At the same time, margins on average loans remained broadly unchanged (see Chart 10 and Table 10).

Chart 10

Changes in terms and conditions on consumer credit and other lending to households

(net percentages of banks reporting a tightening of terms and conditions)

Notes: “Margins” are defined as the spread over a relevant market reference rate. “Other terms and conditions” is the unweighted average of “size of the loan”, “non-interest rate charges” and “maturity”. The net percentages for the “other factors” refer to further factors which were mentioned by banks as having contributed to changes in credit standards.

Table 10

Changes in terms and conditions on consumer credit and other lending to households

(net percentages of banks)

Note: See the notes to Chart 10.

Increased risk perceptions and lower risk tolerance were the main factors underlying the net tightening of overall terms and conditions, while pressure from competition had a small easing impact (see Table 11).

Across the largest euro area countries, overall terms and conditions on consumer credit and other lending to households tightened in Germany and especially Spain, while easing in France and Italy. Wider loan margins, higher collateral requirements and other terms and conditions such as loan size and maturity had a negative impact in Spain, while tightening in Germany was mainly driven by loan size and, to a lesser extent, wider margins on average loans, loan maturity and higher collateral requirements.

Table 11

Factors contributing to changes in overall terms and conditions on consumer credit and other lending to households

(net percentages of banks)

Note: The net percentages for these questions relating to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to a tightening and the percentage reporting that it contributed to an easing.

2.3.3 Rejection rate for consumer credit and other lending to households increased further

Banks indicated a further increase in the share of rejected loan applications for consumer credit and other lending to households in the second quarter of 2020 (15%, after 12% in the previous survey round; see Chart 11). This may indicate increased risk of borrowers in the context of the coronavirus pandemic, due mainly to the deteriorating income and employment situation.

Across the largest euro area countries, the rejection rate increased for banks in Germany, Spain and France, while remaining unchanged in Italy.

Chart 11

Changes in the rejection rate for consumer credit and other lending to households

(net percentages of banks reporting an increase in the share of rejections)

Notes: Net percentages of rejected loan applications are defined as the difference between the percentage of banks reporting an increase in the share of loan rejections and the percentage of banks reporting a decline. Banks’ responses refer to the share of rejected loan applications relative to the total volume of applications in that loan category.

2.3.4 Net demand for consumer credit and other lending to households reached a record low

In the second quarter of 2020, net demand for consumer credit and other lending to households reached a record low since the survey was launched in 2003 (net percentage of -76%, after -4% in the previous quarter; see Chart 12 and Overview table). The decline in net loan demand was much higher than expected by banks in the previous survey round, and the percentage has been well below its historical average since 2003 (2%).

All factors contributed to the decline in loan demand, especially lower consumer confidence and decreased spending on durable goods (see Chart 12 and Table 12). This could be explained by precautionary savings and low spending possibilities for households during the strict lockdown period, as well as uncertainties on employment.

Net demand for consumer credit and other lending to households declined in all the largest euro area countries. This was driven mainly by weaker consumer confidence and lower spending on durable goods. Banks in Germany, France and Italy also reported lower consumption expenditure financed through real-estate guaranteed loans.

Banks expect that net demand for consumer credit and other lending to households will increase in the third quarter of 2020 (net percentage of 30%), likely related to the loosening of the lockdown measures and regained spending opportunities. In line with the other loan categories, the dispersion of banks’ demand expectations remains at high levels.

Chart 12

Changes in demand for consumer credit and other lending to households, and contributing factors

(net percentages of banks reporting an increase in demand and contributing factors)

Notes: See the notes to Chart 4. “Use of alternative finance” is the unweighted average of “internal financing out of savings”, “loans from other banks” and “other sources of external finance”. “Consumption exp. (real estate)” denotes “consumption expenditure financed through real estate-guaranteed loans”.

Table 12

Factors contributing to changes in demand for consumer credit and other lending to households

(net percentages of banks)

Note: See the notes to Chart 12.

3 Ad hoc questions

3.1 Banks’ access to retail and wholesale funding

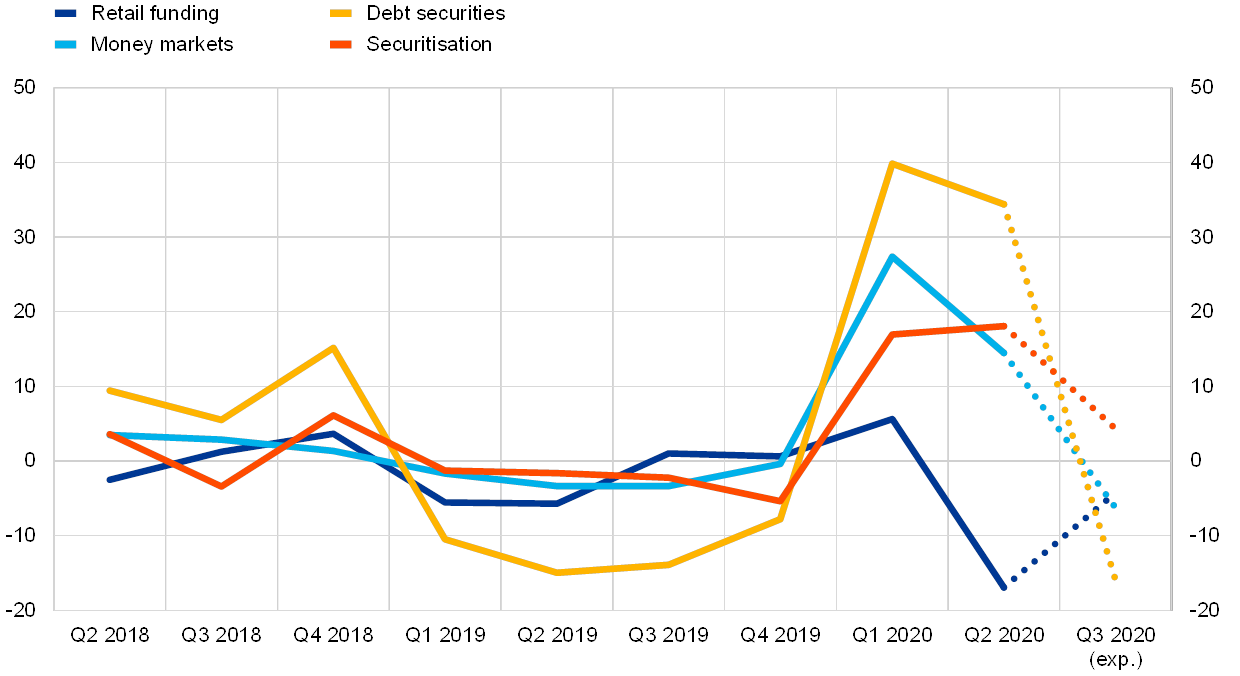

The July 2020 survey included a question assessing the extent to which the situation in financial markets had affected banks’ access to retail and wholesale funding. Banks were asked whether their access to funding had deteriorated or eased over the past three months, as well as about their expectations for the next three months. Here, negative net percentages indicate an improvement, while positive figures indicate a deterioration in net terms.

Euro area banks reported in net terms that their access to wholesale funding continued to deteriorate in the second quarter of 2020, while access to retail funding improved (see Chart 13 and Table 13). In particular, banks continued to report a strong, albeit somewhat smaller, deterioration in access to funding via short-term and long-term debt securities, and to money markets. This reflected a continued stress in bank bond and money markets in the second quarter of 2020, albeit mitigated by accommodative monetary policy. Access to securitisation also continued to deteriorate.[6] As regards retail funding, although access to long-term funding improved, this was largely driven by short-term deposit funding, which likely reflects the increase in overnight deposits by firms and households for precautionary reasons in the context of the coronavirus pandemic.

Chart 13

Banks’ assessment of funding conditions and the ability to transfer credit risk off the balance sheet

(net percentages of banks reporting a deterioration in market access)

Note: The net percentages are defined as the difference between the sum of the percentages for “deteriorated considerably” and “deteriorated somewhat” and the sum of the percentages for “eased somewhat” and “eased considerably”.

Looking ahead to the third quarter of 2020, euro area banks expect that, except for securitisation, their access to retail and wholesale funding will improve. This may reflect improving risk sentiment on account of the broad reopening of economic activities and a favourable impact of monetary policy measures on banks’ funding costs.

Table 13

Banks’ assessment of funding conditions and the ability to transfer credit risk off the balance sheet

(net percentages of banks reporting a deterioration in market access)

Note: See the notes to Chart 13.

3.2 The impact of banks’ NPL ratios on their lending policies

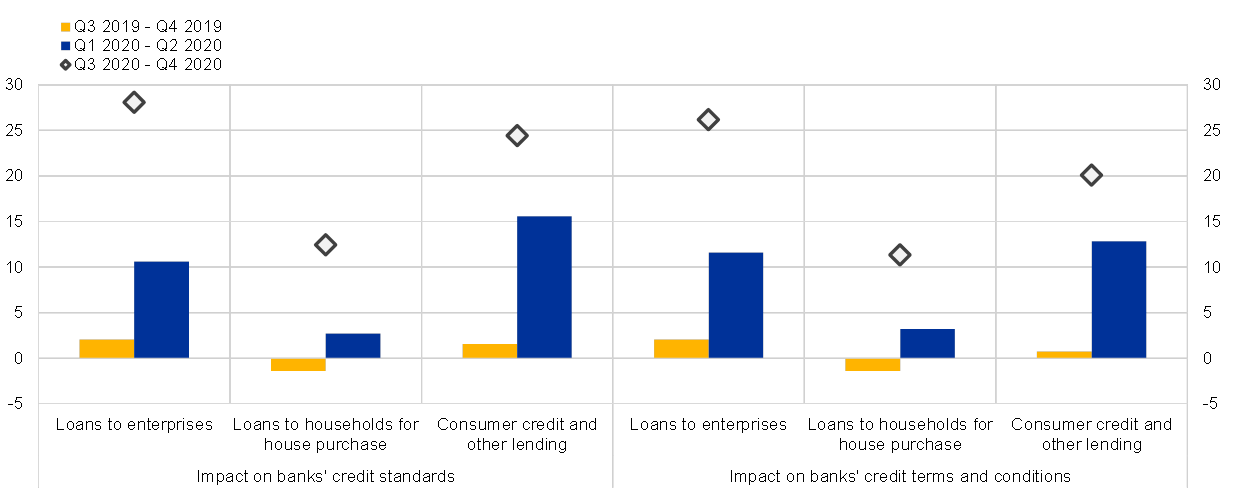

The July 2020 survey included a biannual ad hoc question about the impact that banks’ NPL ratios have on their lending policies and the factors through which NPL ratios contribute to changes in lending policies. Banks were asked about the impact on loans to enterprises, loans to households for house purchase, and consumer credit and other lending to households over the past six months and over the next six months.

Euro area banks indicated a net tightening impact of NPL ratios on credit standards and on terms and conditions for loans across all loan categories in the first half of 2020 (see Chart 14). The net tightening impact of NPL ratios on credit standards was more pronounced for loans to enterprises and consumer credit (net percentages of 11% and 16% respectively), while it was more restrained for housing loans (3%), following a small net tightening impact for loans to enterprises and consumer credit and broadly neutral impact on housing loans in the second half of 2019. The NPL ratios also influenced banks’ credit terms and conditions, as banks reported a stronger net tightening impact for loans to enterprises and consumer credit (net percentages of 12% and 13% respectively), and a smaller net tightening impact for housing loans (3%) over the past six months.

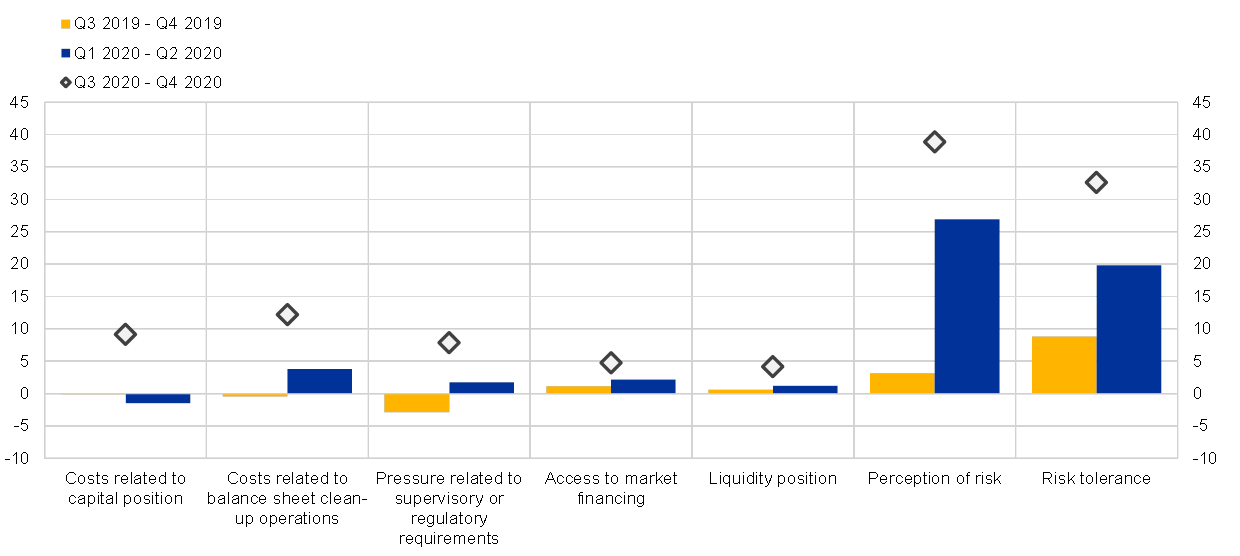

Euro area banks referred mainly to a tightening impact of their NPL ratios on bank lending conditions via higher risk perceptions (net percentage of 27%) related to the general economic outlook and borrowers’ creditworthiness and via a lower risk tolerance (20%), in the first half of 2020 (see Chart 15). Other factors, such as costs related to balance sheet clean-up operations, deteriorated access to market financing and pressure related to supervisory and regulatory requirements, also contributed to the tightening of bank lending conditions via NPL ratios. By contrast, costs related to capital position exerted slightly less pressure via NPL ratios on lending conditions (-2%).

Chart 14

Impact of banks’ NPL ratios on credit standards and terms and conditions

(net percentages of banks)

Notes: The NPL ratio is defined as the stock of gross NPLs on a bank’s balance sheet as a percentage of the gross carrying amount of loans. Changes in credit standards and/or terms and conditions can be caused by changes to the NPL ratio or by changes to regulations or the bank’s assessment of the level of the NPL ratio. The net percentages are defined as the difference between the sum of the percentages for “contributed considerably to tightening” and “contributed somewhat to tightening” and the sum of the percentages for “contributed somewhat to easing” and “contributed considerably to easing”.

Over the next six months, euro area banks expect an increased net tightening impact of their NPL ratios on credit standards and on terms and conditions for loans across all loan categories. This expectation may be related to the end of some fiscal support measures and the longer-lasting nature of the pandemic, with potential negative consequences for borrowers’ creditworthiness. As a result, banks’ increased risk perceptions related to the economic outlook and borrowers’ creditworthiness, as well as lower risk tolerance, are expected by banks to continue to be the most relevant factors for the tightening impact of NPL ratios. Banks also expect all other factors to contribute to the tightening on lending conditions via NPL ratios over the next six months.

Chart 15

Contributions of factors through which NPL ratios affect banks’ policies on lending to enterprises and households

(net percentages of banks)

Note: See the notes to Chart 14.

3.3 Bank lending conditions and loan demand across main sectors of economic activities

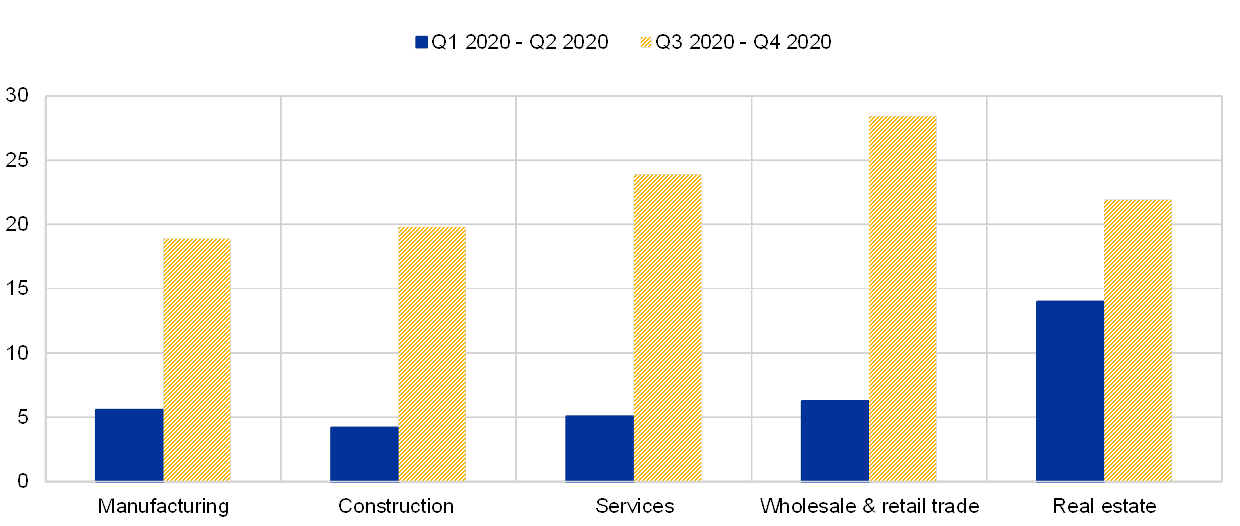

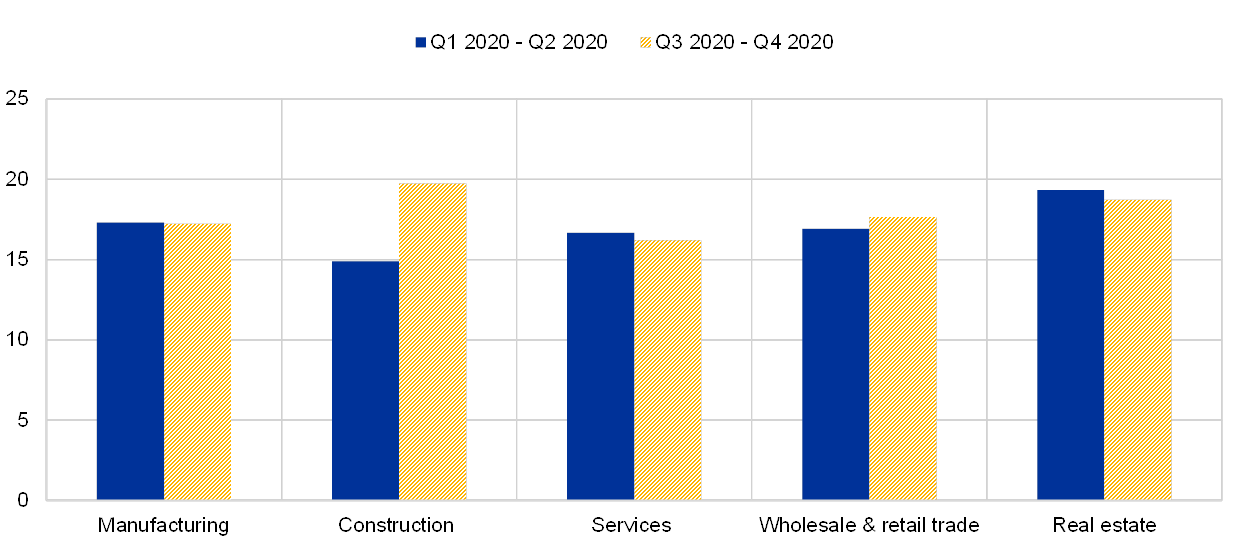

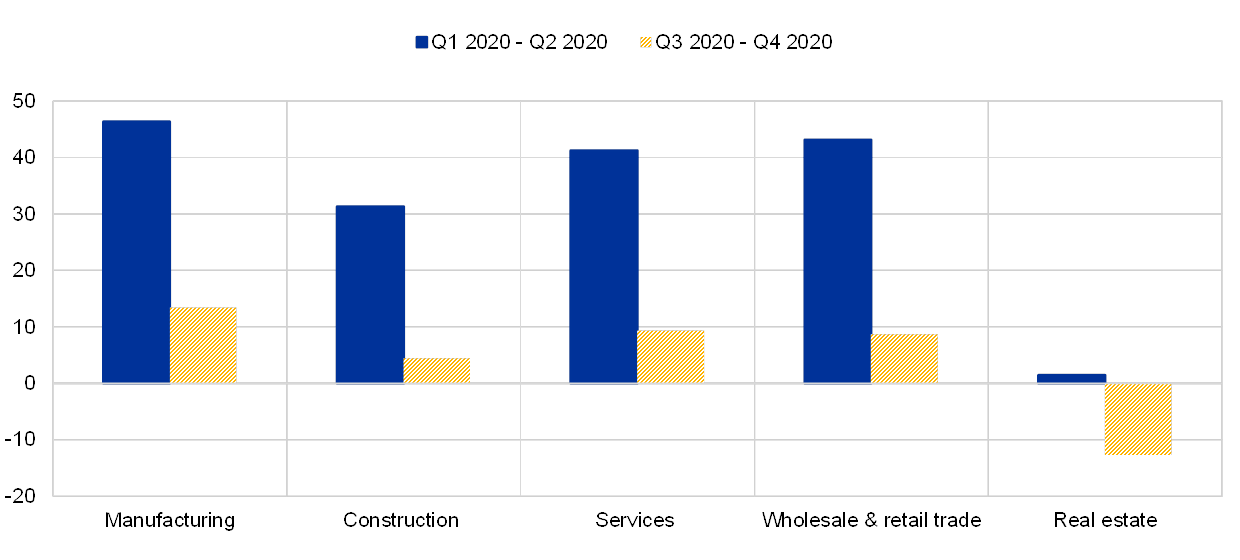

The July 2020 survey included a new biannual ad hoc question aimed to collect information on changes in banks’ credit standards, overall terms and conditions and loan demand across main economic sectors over the past and next six months. Banks were asked to collect information covering five sectors: manufacturing, construction (excluding real estate), services (excluding financial services and real estate), wholesale and retail trade, and real estate (including both real estate construction and real estate services).

Euro area banks indicated a net tightening of credit standards and somewhat stronger net tightening of terms and conditions for new loans to enterprises across main sectors of economic activities over the past six months (see Chart 16 and Chart 17). The net tightening of credit standards was more pronounced for loans to firms in the real estate sector (net percentage of 14%, consistent with the deterioration of banks’ credit standards for housing loans), while in other sectors tightening was smaller (a net percentage range between 4% and 6%). Banks’ tightening of overall terms and conditions for new loans to enterprises was stronger than for credit standards and was similar across different economic sectors (a range of a net percentage between 15% and 19%).

Over the next six months, euro area banks expect that credit standards will continue to tighten further for loans to enterprises across all main sectors of economic activities, especially in wholesale and retail trade (net percentage of 28%). Banks also expect a continued net tightening of their overall terms and conditions for loans to enterprises in all main economic sectors in the second half of 2020.

Chart 16

Changes in credit standards for new loans to enterprises across main economic sectors

(net percentages of banks; over the past and next six months)

Note: The net percentages are defined as the difference between the sum of the percentages for “deteriorated considerably” and “deteriorated somewhat” and the sum of the percentages for “eased somewhat” and “eased considerably".

Chart 17

Changes in terms and conditions for new loans to enterprises across main economic sectors

(net percentages of banks; over the past and next six months)

Note: See the notes to Chart 16.

Firms’ net demand for loans or credit lines increased strongly in the manufacturing, wholesale and retail trade, and services sectors in the first half of 2020 (see Chart 18). The increase in demand was negligible in the real estate sector. Smaller demand from firms in this sector partly reflects a more pronounced tightening of credit standards by banks over the past six months.

Over the next six months, banks expect that firms’ loan demand will increase less in almost all economic sectors, except the real estate sector, where banks expect net demand to decline.

Chart 18

Changes in demand for loans or credit lines to enterprises across main economic sectors

(net percentages of banks; over the past and next six months)

Note: The net percentages are defined as the difference between the sum of the percentages for “increased considerably” and “increased somewhat” and the sum of the percentages for “decreased somewhat” and “decreased considerably".

Annexes

See more.

© European Central Bank, 2020

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted, provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary.

PDF ISSN 1830-5989, QB-BA-20-003-EN-N

HTML ISSN 1830-5989, QB-BA-20-003-EN-Q

- The four largest euro area countries in terms of GDP are Germany, France, Italy and Spain.

- For more detailed information on the bank lending survey, see the article entitled “A bank lending survey for the euro area”, Monthly Bulletin, ECB, April 2003; Köhler-Ulbrich, P., Hempell, H. and Scopel, S., “The euro area bank lending survey”, Occasional Paper Series, No 179, ECB, 2016; and Burlon, L., Dimou, M., Drahonsky, A. and Köhler-Ulbrich, P., “What does the bank lending survey tell us about credit conditions for euro area firms?”, Economic Bulletin, Issue 8, ECB, December 2019.

- In this case, the selected sample banks are generally of similar size or their lending behaviour is typical of a larger group of banks.

- The non-harmonised historical data differ from the harmonised data mainly as a result of heterogeneous treatment of “NA” replies and specialised banks across questions and countries. Non-harmonised historical BLS data are published for discontinued BLS questions and ad hoc questions.

- The calculation of a simple average when combining factors in broader categories assumes that all factors have the same importance for banks. This helps to explain some inconsistencies between developments in demand for loans and developments in the main underlying factor categories.

- Considerable percentages of banks indicated that questions on securitisation were “not applicable”, as that source of funding was not relevant to them (between 48% and 55% of banks in the second quarter of 2020, depending on the type of securitisation).

-

14 July 2020