The expanding functions and uses of stablecoins

Published as part of the Financial Stability Review, November 2021.

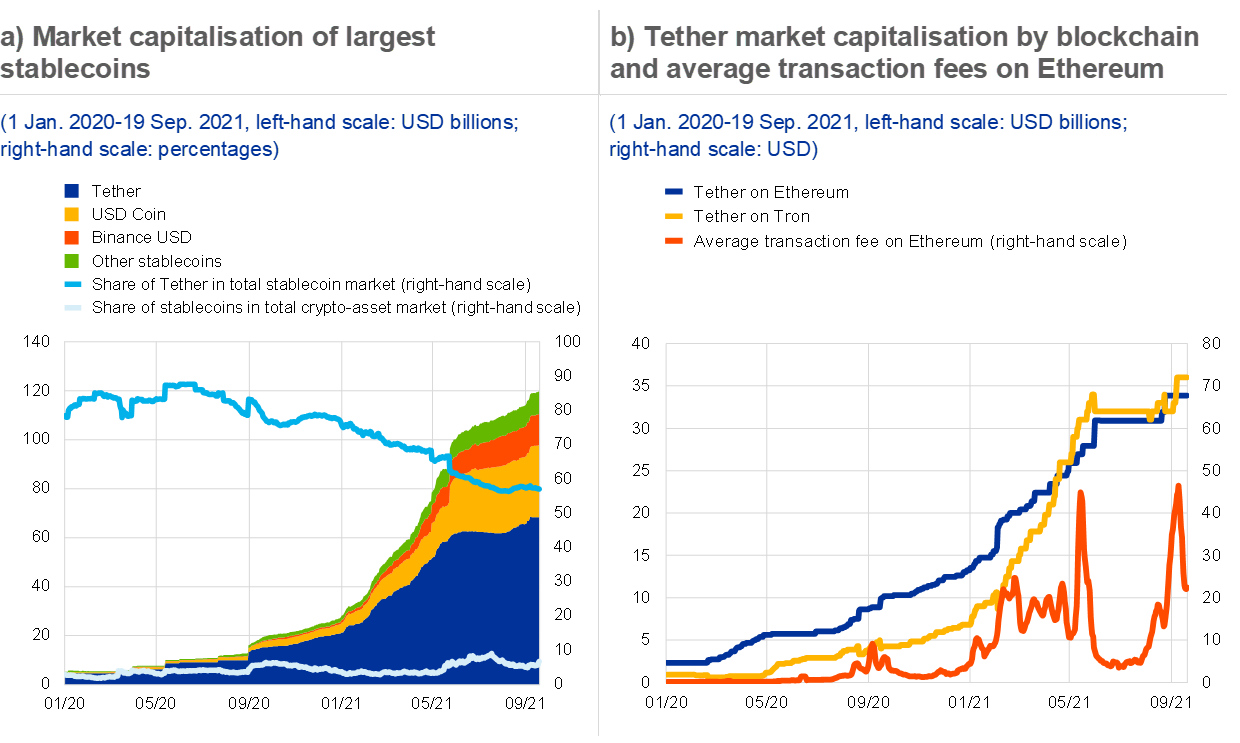

The market capitalisation of stablecoins has risen from USD 5 billion to USD 120 billion since 2020 and they are serving increasingly different functions in the crypto-asset ecosystem (see Chart A, panel a). Stablecoins are digital units of value that use blockchain cryptography. They rely on tools to maintain a stable value relative to one or several currencies or other assets (including crypto-assets), or make use of algorithms to maintain a stable value.[1] For those stablecoins referring to currencies or assets, these tools include holding reserve assets against which stablecoin holdings can be redeemed. Despite their recent growth, stablecoins still only account for around 6% of the estimated USD 2 trillion total market capitalisation of crypto-assets, though interlinkages between stablecoins and crypto-assets imply a correlation of risks between these market segments. At the same time, the functions served by stablecoins within the ecosystem have multiplied. In addition to acting as a relatively safe “parking space” for crypto volatility, stablecoins serve as a bridge between fiat currencies and crypto-assets. They are used for trading: in September 2021 around 75% of all trading on crypto trading platforms involved a stablecoin.[2] Due to their relatively low price volatility, they are also used as collateral in crypto-asset derivative transactions or in decentralised finance (“DeFi”). In the light of stablecoins’ direct links to the traditional financial system and their interlinkages with the wider crypto-asset market, this box analyses the risks associated with the evolving functions of stablecoins and the financial stability implications of such risks.

Chart A

The use of stablecoins has expanded rapidly over the past two years, despite high transaction fees on some blockchains such as Ethereum, which should in principle constrain their use as a form of payment

Sources: CryptoCompare, ECB calculations and Coinmetrics.io.

Note: Panel a: “Other stablecoins” includes Multi-Collateral DAI, Pax Dollar, TrueUSD and GeminiUSD.

The current high transaction fees on certain blockchains curb the use of stablecoins as a form of payment and may push the largest existing one towards a cheaper blockchain. Like other crypto-assets, stablecoins are issued on a blockchain which maintains a record of transactions made. For users to consider making payments with stablecoins, issuers need a blockchain with stable and low transaction fees. However, the fees on the Ethereum blockchain, where most stablecoins are currently issued, are considered too high and too volatile for payment use (see Chart A, panel b).[3] This situation may change if Ethereum’s transaction fees decrease or stablecoin usage moves to low or no-fee blockchains. In fact, the supply of Tether on Tron – which offers users a daily number of free transactions and generally low transaction fees – has now surpassed that on Ethereum (see Chart A, panel b).

Stablecoin holders can earn revenue from their holdings by providing liquidity, although they run the risk of incurring significant losses if they do so. The use of stablecoins in the DeFi ecosystem of financial applications that enable trading or lending is becoming increasingly popular. These DeFi activities are facilitated by liquidity pools consisting of crypto-assets and stablecoins governed by software protocols known as “smart contracts”. For example, trades between stablecoins and crypto-assets are enabled by liquidity pools, and liquidity providers earn income from the transaction fees paid for the trades they facilitate. Taking the example of an Ether/Tether pool, returns from providing liquidity in this way can reach around 18%.[4] However, stablecoin liquidity providers run the risk of incurring significant losses, even if the stablecoin itself remains stable.[5] The smart contract governing a liquidity pool requires the asset pair in that pool to maintain a constant total value. As a result, a price decrease for Ether creates arbitrage opportunities that increase the supply of Ether in the Ether/Tether pool but reduces the supply of Tether. In turn, the liquidity providers suffer a reduction in the total value of the liquidity pool in fiat currency, which could drop to zero if the Ether price falls to zero.

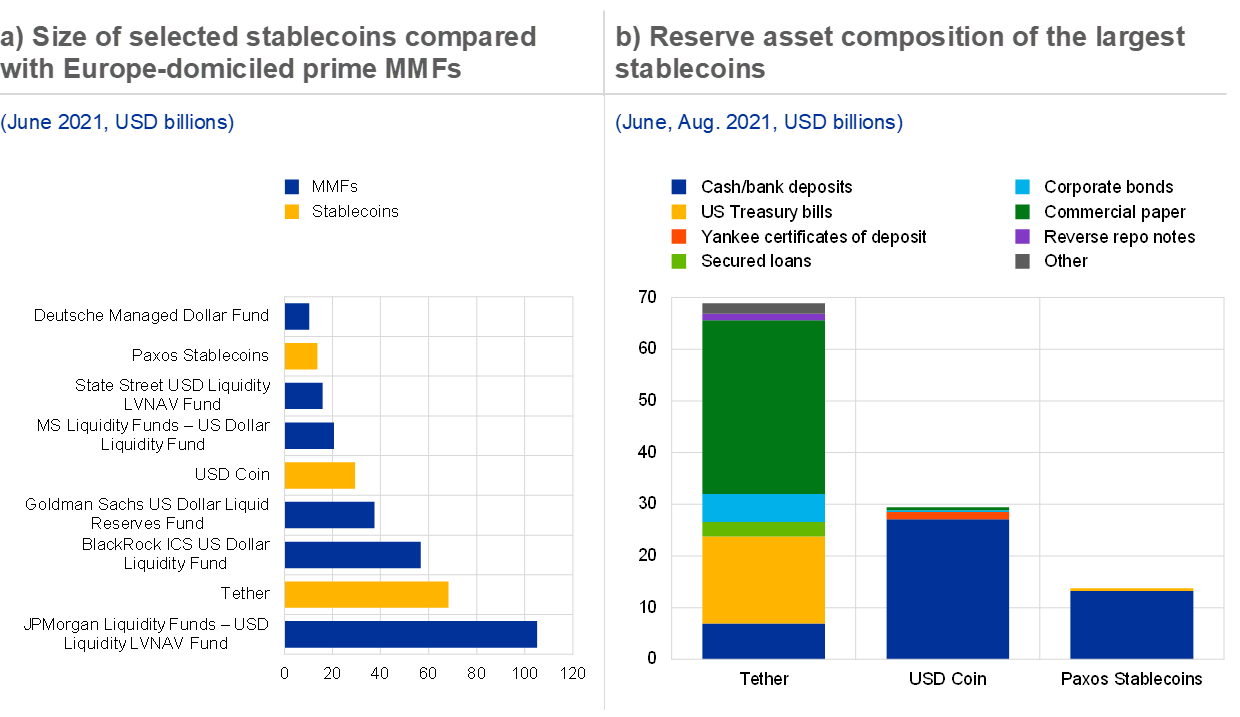

Stablecoins are exposed to similar vulnerabilities as money market funds (MMFs), and there is currently a lack of transparency regarding stablecoins’ reserve assets. Stablecoins, like MMFs, need to be backed by liquid reserve assets if users are to see the conversion back to a fiat currency as credible. Losses on reserves could trigger a loss of user confidence and prompt large-scale redemption requests, while the liquidation of underlying – usually traditional – assets to cover redemptions could have negative fire-sale contagion effects on the financial system. The market impact will depend on the size of the stablecoins, some of which have already reached asset values comparable to those of large prime MMFs domiciled in Europe (see Chart B, panel a). However, too few details on the reserve asset composition of major stablecoins have been disclosed for the risks within these reserves to be fully understood. For example, although Tether’s published reserve breakdown shows that half of the reserve assets were invested in commercial paper and 21% in cash and bank deposits, the lack of more granular information on its commercial paper investment makes it difficult to form a clear view of the liquidity of its holding (see Chart B, panel b).[6]

Chart B

The size of the reserve assets underlying stablecoin arrangements rivals that of large prime MMFs domiciled in Europe, but their composition raises concerns regarding their liquidity

Sources: Fitch European Money Market Fund Compare (June 2021) and company disclosures.

Notes: Panel a: Fitch’s Money Market Fund Compare covers all Europe-domiciled MMFs publicly rated by Fitch under its Global Money Market Fund Rating Criteria. All data are based on fund surveillance reports from the fund administrators and managers. The MMFs displayed are the largest prime dollar-denominated Europe-domiciled funds by asset size in June 2021. Panel b: reserve data are as at 30 June 2021 for Tether and Paxos Stablecoins (Binance USD, Pax Dollar) and 31 August 2021 for USD Coin. Total assets equal outstanding issuance as at 19 September 2021. Corporate bond holdings of Tether include funds and precious metals. Commercial paper holdings of Tether include certificates of deposit. Binance USD is issued along with Pax Dollar, so official reserve disclosures are consolidated under “Paxos Stablecoins”.

Stablecoins currently pose limited financial stability risks in the euro area, but their growing size, usage and interconnections call for urgent implementation of regulatory, supervisory and oversight frameworks. There are still few connections with the traditional financial system. However, the stablecoin landscape is evolving rapidly, with the growing participation of retail and institutional investors and a potentially larger role for banks. For example, it is currently planned that the Diem stablecoin (previously known as Libra) will be issued by a commercial bank which will also manage the underlying reserve assets.[7] In addition, the use of stablecoins may accelerate if large technology companies (big techs) start offering their own stablecoins or integrate existing stablecoins into their wallets. For example, Facebook recently launched a pilot of its Novi wallet in the United States and Guatemala using the stablecoin Pax Dollar.[8] Appropriate regulatory, supervisory and oversight frameworks must be put in place urgently before stablecoins pose greater risks to financial stability. The European Commission’s recent proposal for the Regulation on Markets in Crypto-assets (MiCA) is a significant step forward. The global reach of this market also underscores the need for global standard-setting bodies to further assess the extent to which existing standards are appropriate for, and applicable to, stablecoins, and close any gaps as necessary.

- See ECB Crypto-Assets Task Force, “Stablecoins: Implications for monetary policy, financial stability, market infrastructure and payments, and banking supervision in the euro area”, Occasional Paper Series, No 247, ECB, September 2020; and Bullmann, D., Klemm, J. and Pinna, A., “In search for stability in crypto-assets: are stablecoins the solution?”, Occasional Paper Series, No 230, ECB, August 2019.

- See “Share of Trade Volume by Pair Denomination”, The Block.

- See “The Ethereum Gas Report”, CoinMetrics, 22 March 2021 and Ethereum.org for an explanation of transaction fees on Ethereum and recent changes; Schär, F., “Decentralized Finance: On Blockchain and Smart Contract-Based Financial Markets”, Economic Research, Vol. 103, No 2, Federal Reserve Bank of St. Louis, 2021; and “Tether Use on Tron Passes Ethereum as Low Fees Attract Small Transactions”, CoinDesk.

- See “SushiSwap, Ethereum/USD Tether pair”, intotheblock. The return reflects the average Ether-Tether pool return on investment over a three-month period from 30 June to 30 September 2021 on the decentralised SushiSwap exchange.

- See “UniSwap: A Good Deal for Liquidity Providers?”, Pintail, 12 January 2019.

- In October 2021, the Commodity Futures Trading Commission issued a fine against Tether for misleading statements from at least June 2016 to February 2019 to the effect that Tether had sufficient dollar reserves to back each of its stablecoins in circulation; see “CFTC Orders Tether and Bitfinex to Pay Fines Totaling $42.5 Million”, Release Number 8450-21, 15 October 2021.

- See “Diem Announces Partnership with Silvergate and Strategic Shift to the United States”, Diem press release, 12 May 2021.

- See “Pilot Version of Novi Now Available”, Novi News, 19 October 2021.