Liquidity conditions and monetary policy operations in the period from 30 October 2019 to 28 January 2020

Published as part of the ECB Economic Bulletin, Issue 2/2020.

This box describes the monetary policy operations of the ECB during the seventh and eighth reserve maintenance periods of 2019, which ran from 30 October to 17 December 2019 and from 18 December 2019 to 28 January 2020, respectively. The review period encompasses the start of the two-tier system for remunerating excess liquidity holdings. Starting from the seventh reserve maintenance period, which began on 30 October 2019, this system exempts part of a credit institution’s excess liquidity holdings (i.e. reserve holdings in excess of minimum reserve requirements) from negative remuneration at the rate applicable to the deposit facility.[1] Instead, these excess liquidity holdings are currently remunerated at an annual rate of 0%. Other recent changes include the net repayments of liquidity provided through targeted longer-term refinancing operations (TLTROs) as well as the resumption of asset purchases.

Liquidity needs

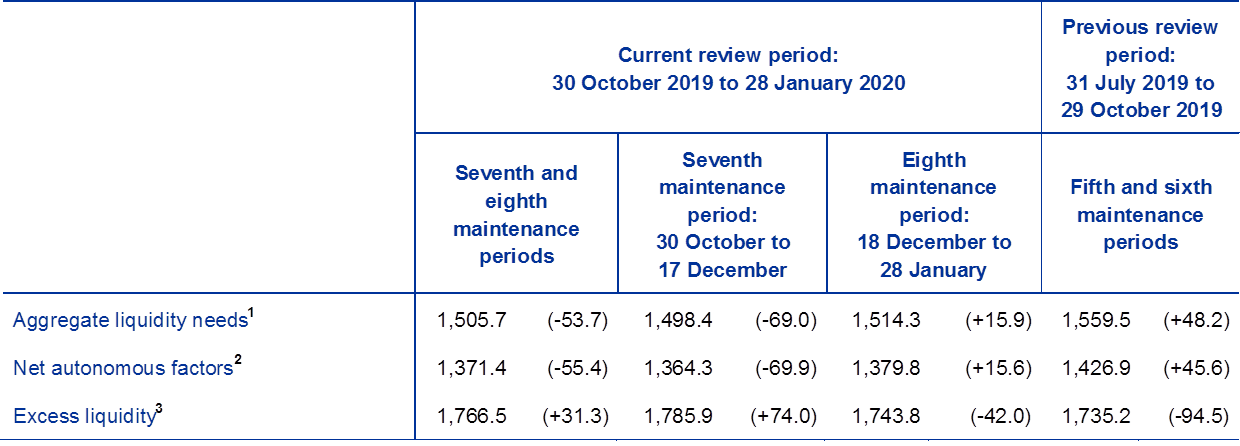

The average daily liquidity needs of the banking system, defined as the sum of net autonomous factors and reserve requirements, stood at €1,505.7 billion in the period under review. This was €53.7 billion lower than in the previous review period (i.e. the fifth and sixth reserve maintenance periods of 2019; see Table A). Net autonomous factors decreased by €55.4 billion, while minimum reserve requirements increased by €1.7 billion to €134.3 billion.

The decrease in net autonomous factors was driven primarily by an increase on the asset side of the Eurosystem balance sheet (net foreign assets and net assets denominated in euro). Autonomous factors on the asset side increased by €55.1 billion to €1,009.1 billion, reflecting both a €33.2 billion increase in net foreign assets, which was similar to the growth in the previous review period, and a €21.9 billion increase in net assets denominated in euro to €238.0 billion. Autonomous factors on the liability side remained almost unchanged on aggregate (down €0.4 billion). While other autonomous factors and banknotes in circulation rose by €42.3 billion and €20.0 billion, respectively, these increases were fully offset by lower government deposits, which averaged €219.8 billion in the period under review after reaching a historical high of €298.6 billion in the sixth reserve maintenance period. Overall, net autonomous factors – defined as liquidity-absorbing autonomous factors on the liability side less liquidity-providing autonomous factors on the asset side – fell to €1,371.4 billion.

Table A

Eurosystem liquidity conditions

Assets

(averages; EUR billions)

Source: ECB.Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

Other liquidity-based information

(averages; EUR billions)

Source: ECB.Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.1) Computed as the sum of net autonomous factors and minimum reserve requirements.2) Computed as the difference between autonomous liquidity factors on the liability side and autonomous liquidity factors on the asset side. For the purpose of this table, items in course of settlement are also added to net autonomous factors.3) Computed as the sum of current accounts above minimum reserve requirements and the recourse to the deposit facility minus the recourse to the marginal lending facility.

Interest rate developments

(averages; percentages)

Liquidity provided through monetary policy instruments

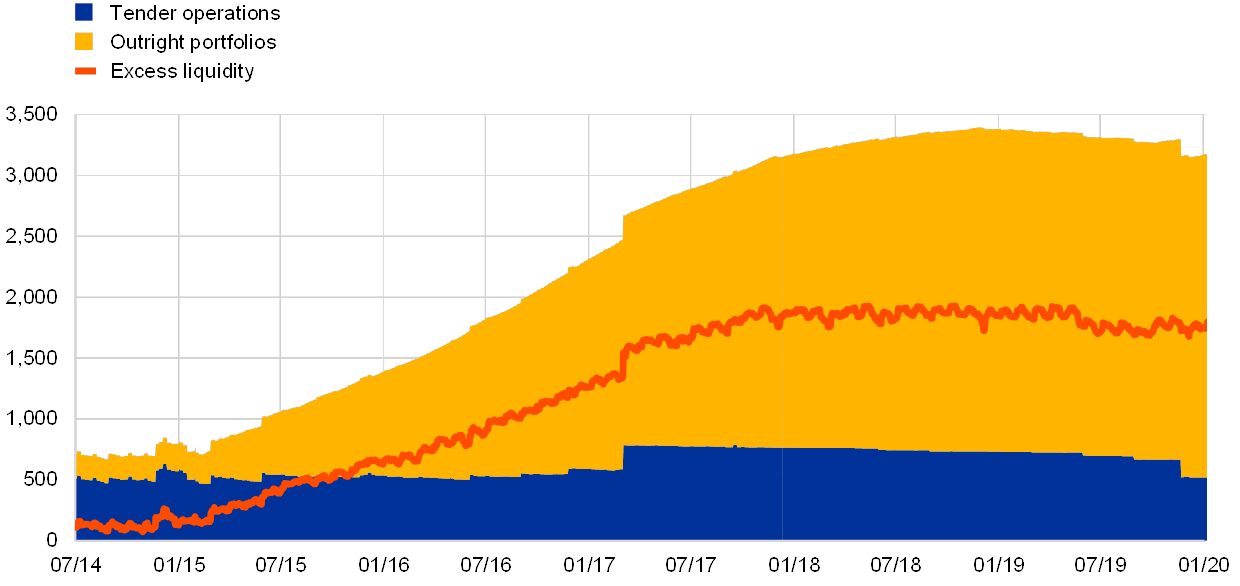

The average amount of liquidity provided through open market operations – including both tender operations and monetary policy portfolios – decreased by €22.4 billion to €3,272.2 billion (see Chart A). As during the previous two maintenance periods, this decrease was driven primarily by lower demand in tender operations. In contrast, and unlike in previous review periods in 2019, liquidity provided through monetary policy portfolios increased again as a result of the resumption of net purchases under the asset purchase programme (APP) in November 2019.

Chart A

Evolution of liquidity provided through open market operations and excess liquidity

(EUR billions)

Source: ECB.

Note: The latest observation is for 28 January 2020.

The average amount of liquidity provided through tender operations declined during the review period, as it did during the previous review period. The decrease of €39.9 billion to €644.0 billion was mainly due to lower liquidity provided through TLTROs. Financial institutions in the euro area voluntarily repaid €87.3 billion of TLTRO II funding on average during the two maintenance periods. This exceeded the uptake of new TLTRO III funding, which increased by €47.2 billion to €48.5 billion on average over the review period. In addition, liquidity provision via main refinancing operations (MROs) decreased slightly, from €2.5 billion to €2.3 billion. The observed average decrease would have been even larger without the year-end MRO operation, in which €7.9 billion was allotted. The outstanding amount of three-month longer-term refinancing operations (LTROs) increased slightly, by €0.5 billion.

Liquidity provided through the Eurosystem’s monetary policy portfolios increased by €17.5 billion to €2,628.2 billion, owing to the resumption of net asset purchases. Average holdings increased by €12.3 billion to €2,099.9 billion in the public sector purchase programme (PSPP) and by €6.2 billion to €183.5 billion in the corporate sector purchase programme (CSPP). In addition, holdings under the third covered bond purchase programme (CBPP3) and the asset-backed securities purchase programme (ABSPP) increased by €2.8 billion and €2.1 billion, respectively.[2] Redemptions of bonds held under the Securities Markets Programme (SMP) totalled €4.9 billion in the review period.

Excess liquidity

As aggregate liquidity needs decreased, average excess liquidity increased compared with the previous review period, by €31.3 billion to €1,766.5 billion (see Chart A). Despite lower provision of liquidity through tender operations, the decrease in net autonomous factors and the resumption of net asset purchases increased excess liquidity in the euro area.

In addition, the composition of excess liquidity was affected by the start of the two-tier system for remunerating excess liquidity holdings in the euro area as of the seventh maintenance period. This is due to the fact that only balances held in financial institutions’ current accounts up to their maximum allowance are exempt from negative remuneration at the rate applicable to the deposit facility. This led to a rebooking of funds held by financial institutions from the deposit facility, which decreased by €253.6 billion, to their current accounts, which increased by €284.9 billion.

Interest rate developments

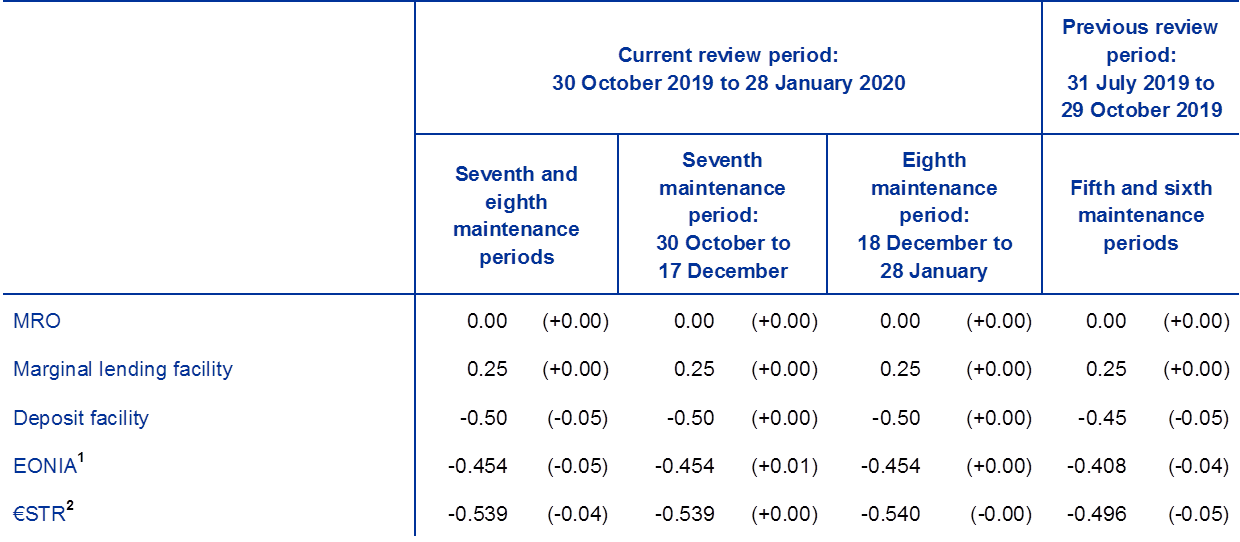

The €STR remained broadly stable during the seventh and eighth maintenance periods. The ECB’s deposit facility rate and the MRO and marginal lending facility rates remained unchanged during the period under review. Consequently, the €STR remained stable in the seventh and eighth maintenance periods at -53.9 and -54.0 basis points, respectively. The introduction of the two-tier remuneration system did not significantly affect the level of the €STR. The EONIA, which as of October 2019 is calculated as the €STR plus a fixed spread, moved in parallel with the €STR.

- Eligible reserve holdings of financial institutions are computed on the basis of average end-of-calendar-day balances held in the institution’s current account over the maintenance period. The exemption from negative interest rates applies to excess liquidity holdings in the current account up to a certain multiple of the institution’s minimum reserve requirement. The Governing Council set the initial multiplier at six.

- Even with full reinvestment, limited temporary deviations in the overall size and composition of the APP may occur for operational reasons. See the article entitled “Taking stock of the Eurosystem’s asset purchase programme after the end of net asset purchases”, Economic Bulletin, Issue 2, ECB, 2019.