Breaking the “chain effect” of tariffs – foreign trade zones in the time of protectionism

Published as part of the ECB Economic Bulletin, Issue 1/2020.

In foreign trade zones (FTZs) imported goods can be handled, manufactured and re-exported without the intervention of customs authorities. This box reviews the benefits of FTZs, how they are used in the United States,[1] China[2] and the European Union (EU)[3] and whether they can cushion the rise in tariffs resulting from new trade restrictions.[4]

FTZs were originally designed to promote economic development and employment by favouring international trade. In FTZs, processing trade and re-exported goods are exempt from import duties – other advantages include lower processing fees and deferred import duties. There are also some disadvantages to FTZs. For example, existing businesses may simply relocate to a FTZ from elsewhere in the same country so as to benefit from lower duties or lower taxes. This can lead to a fall in government tax revenue without sizeable net positive effects on employment and economic activity.[5] With these advantages and disadvantages in mind, the extent to which countries benefit from FTZs is highly context-dependent. In several countries, the number of FTZs has grown over the past two decades as governments have tried to encourage global production on their territories.

FTZs can break the “chain effect” of tariffs to the extent that parts and components (otherwise known as intermediate goods) are either exempted from duties when they are re-exported or can enter the market at favourable rates. In the United States, tariff rates are higher on intermediate goods than on final products (in what is known as tariff inversion), but inputs imported through FTZs can be exempted from duties or levied the lower final product tariff rate. Furthermore, the value created within FTZs is domestic and therefore shielded from US taxation on foreign imports. Instead of paying a tariff on each imported intermediate good entering production of final goods, firms can take advantage of FTZs to break this “chain” of tariffs by only paying the applicable tariff on the foreign value added of the finished item. Alternatively, they can transform and manufacture the goods in FTZs and then re-export them elsewhere without paying US import tariffs. Products manufactured within global value chains (GVCs) obtain the greatest cost-saving benefits from FTZs, as they typically cross borders repeatedly and would otherwise be subject to duties at each border. In the absence of FTZs, tariffs would pile up on GVC products because they are levied on the gross value of the item and not on the value added at each stage. According to the US National Association of Foreign-Trade Zones, roughly half of the costs firms save by locating in FTZs are due to tariff inversion avoidance.[6]

In the United States, FTZs handle a substantial share of total imports (around 38% in 2018). However, those imports that are considered to have “foreign status” and receive favourable treatment account for only 14% of total imports.[7] Around half of the foreign-status imports eventually enter US domestic borders for final consumption, while the rest are processed and re-exported. In 2018, 440,000 workers were employed in US FTZs. Besides oil, which transits through US FTZs for historical reasons, the bulk of imports entering the United States via FTZs are made up of electronic items, machinery and transportation goods with global production networks.[8] Foreign car makers take advantage of tariff inversion by locating inside FTZs.[9]

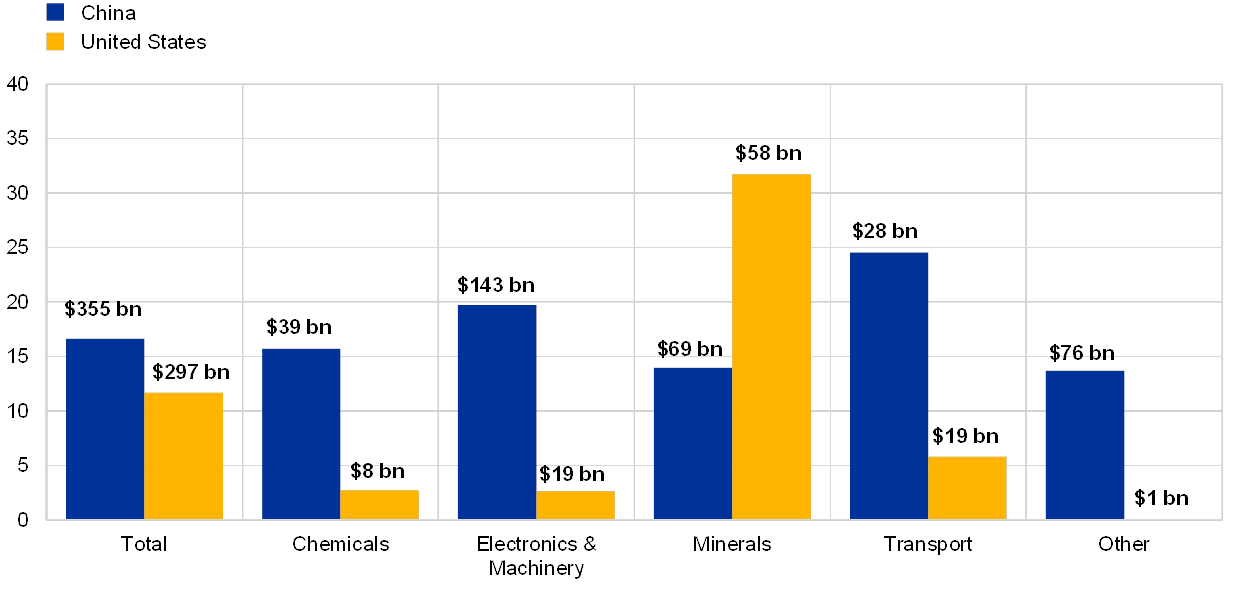

FTZs in China also account for a significant and growing share of overall trade. While relief from import duties is not currently a feature of FTZs in China, this has been under consideration and may change as part of the continued expansion of FTZs. In China, there are currently 12 large FTZs. These zones employ 4% of the workforce and handle goods representing around 17% of total Chinese imports. As in the United States, around half of these goods are for domestic consumption and half are for re-export. Electronics and machinery imported through FTZs account for 20% of imports in their respective sectors (see Chart A), while transport goods make up 25% of imports in that sector. Firms located in FTZs (as well as in other special economic zones) can also take advantage of looser capital controls and tax advantages.

Chart A

Chinese and US imports via FTZs in 2018

(foreign status imports as a share of total imports in each sector)

Sources: US Census, Trade Data Monitor and ECB staff calculations.

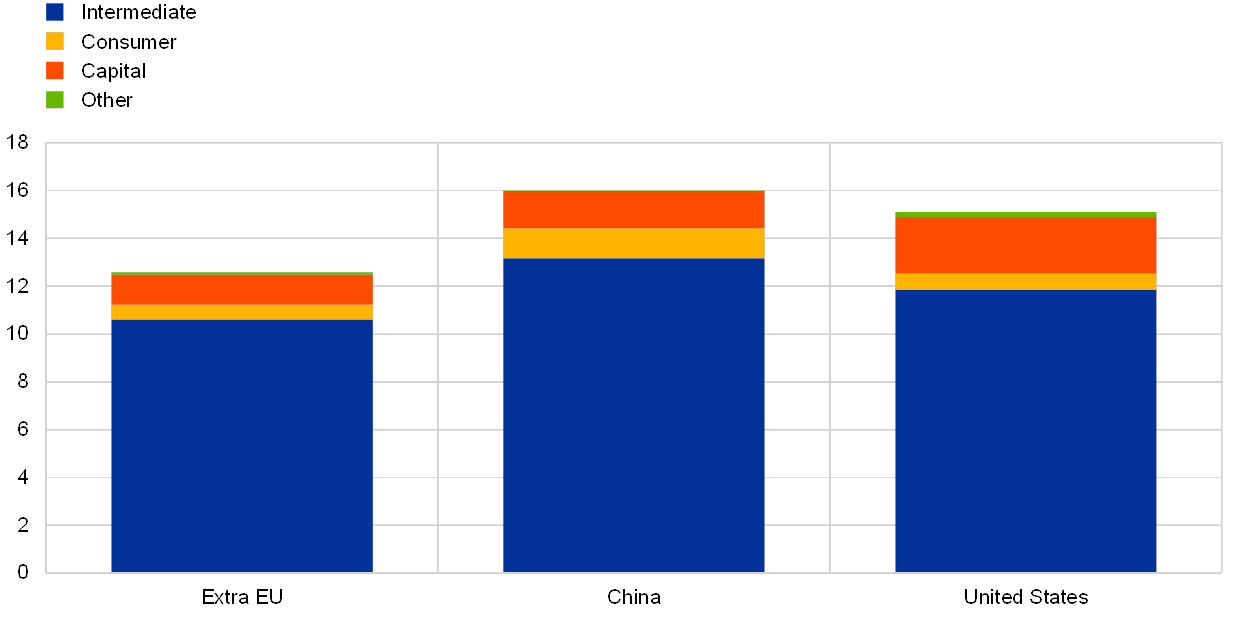

In the EU, no duty waiver is granted to imports passing through FTZs because FTZs are mainly used to smooth out customs processes – instead a similar effect is achieved via an import duty suspension scheme.[10] This scheme, introduced in 2013, guarantees a level playing field to companies operating in the EU irrespective of their geographical location. The share of euro area imports under suspension arrangements is comparable to imports through FTZs in other regions (12% of euro area imports are under suspension arrangements, while 17% of imports into China and 14% of imports into the United States take place through FTZs). In line with the original aim of FTZs, the duty suspension scheme primarily concerns intermediates. Capital goods benefit to a lesser extent, whereas consumer goods account for a negligible fraction of all euro area imports under suspension arrangements (see Chart B). However, since the ultimate scope is to support domestic production and the development of regional value chains, only items that are not produced within the EU can be granted duty suspensions; in particular neither cars nor car parts have ever been included on the suspension list.

Chart B

Euro area imports under import duty suspension arrangements in 2018

(share of total imports by product type)

Sources: European Commission, Eurostat and ECB staff calculations.

Note: The list of suspensions is revised twice a year, and suspensions from customs duties can be granted for up to five years.

FTZs can cushion the impact of the US-China trade war, depending on the relative size of the tariffs on intermediates compared with those on final goods.[11] Increasing tariffs on intermediates relative to final goods generates a greater incentive to import through FTZs in the United States in order to take advantage of import duty exemptions. In the ongoing trade war between China and the United States, around 90% of Chinese intermediate goods were affected by a rise in US tariffs.[12] Protectionist measures increased the bilateral tariff rate by 14.2 percentage points and the increase in the average US tariff rate on intermediate goods from China is twice as high as the tariff rise on consumer goods (6 percentage points compared with 3 percentage points). The trade war has therefore made tariff inversion more pronounced and further increased the incentive to import through FTZs. Recourse to FTZs may have lowered the bilateral effective US-China tariff rate by up to 0.7 percentage points. Assuming all imported Chinese intermediates are rerouted through US FTZs, the bilateral effective US-China tariff rate may be up to 4.5 percentage points lower.[13]

- For a complete list of FTZs in the United States, see the “List of Foreign-Trade Zones by State”.

- For a list of FTZs in China, see the article “China: China Introduces New Free Trade Zones and Improved Practices”, International Tax Review, 15 October 2019.

- For a complete list of FTZs in the EU, see the document “Free zones which are in operation in the customs territory of the Union, as communicated by the Member States to the Commission”, 20 December 2019.

- Matt Gold, former US trade negotiator, affirmed that “in a world where trade barriers increase, FTZs become more valuable”, see the article “Trump Erects Trade Barriers, and ‘Foreign Trade Zones’ Take Them Down”, Governing: The Future of States and Localities, 6 March 2018.

- For a brief overview of the advantages and disadvantages of FTZs, see “Special economic zones – Not so special”, The Economist, 4 April 2015.

- NAFTZ, “The US Foreign-Trade Zones Program: Economic Benefits to American Communities”, 2019.

- For more information on the definitions of “domestic status/duty paid” and “foreign status” goods, see the “Glossary of FTZ terms” produced by the US Foreign-Trade Zones Board.

- Oil imports represent two-thirds of all FTZ imports in the United States. Refineries are located in FTZs to bypass the historical ban on crude importing dating back to the 1930s, when the United States was still a net exporter of oil.

- Tiefenbrun, S., “U.S. Foreign Trade Zones of the United States, Free-Trade Zones of the World, and their Impact on the Economy”, Journal of International Business and Law, Vol. 12(2), 2013.

- The rationale for this approach is that exemption from import duties using FTZs would constitute an unfair competitive advantage for companies located in FTZs compared with those located elsewhere in the EU.

- Siroën, J.M. and Yücer, A., “Trade Performance of Free Trade Zones”, Document de travail /Working paper, No DT/2014-09, Université Paris-Dauphine, 2014.

- Protectionist measures against Chinese imports raised the bilateral effective tariff rates by 16.3 percentage points. However, following the announcement in December 2019 of a partial deal (entering into force in February 2020) and the subsequent easing of tensions, effective tariff rates rose by 14.2 percentage points.

- Inputs imported via FTZs for production in the United States were worth USD 130 billion in 2018. Assuming that the share of Chinese intermediates entering production in US FTZs is the same as the share of imported Chinese intermediates in total US intermediate imports, the cushioning effect of FTZs may be up to 0.7 percentage points. Furthermore, if we assume that all imported Chinese intermediates (USD 149 billion in 2017) are rerouted through FTZs, this could lead to a one-third reduction in the impact on the bilateral effective tariff. For example, this would result in a rise of 9.8 percentage points instead of 14.2 percentage points. Since the data on US FTZ trade composition are limited, we make assumptions about the share of imports of Chinese intermediates entering production in US FTZs. We also assume that all foreign inputs that enter FTZs for production are channelled towards the US domestic market for final consumption (i.e. not re-exported). In addition, we assume that all Chinese intermediate imports have been affected by a 25 percentage point increase in tariffs, while tariffs on consumer goods have only increased by 7.5 percentage points. These are reasonable assumptions, as 83% of Chinese intermediates in total US intermediate imports from China have been affected by a 25 percentage point increase in the tariff rate. At the same time, almost 70% of Chinese consumer goods in total US consumer goods imports from China have been targeted by an increase in tariffs equal to or lower than 7.5 percentage points.