Liquidity conditions and monetary policy operations in the period from 31 October 2018 to 29 January 2019

Published as part of the ECB Economic Bulletin, Issue 2/2019.

This box describes the ECB’s monetary policy operations during the seventh and eighth reserve maintenance periods of 2018, which ran from 31 October 2018 to 18 December 2018 and from 19 December 2018 to 29 January 2019 respectively. Throughout this period the interest rates on the main refinancing operations (MROs), the marginal lending facility and the deposit facility remained unchanged at 0.00%, 0.25% and −0.40% respectively. In parallel, the Eurosystem continued to purchase public sector securities, covered bonds, asset-backed securities and corporate sector securities as part of its asset purchase programme (APP), with a target of €15 billion of net purchases on average per month until the end of December 2018. It then entered the reinvestment phase on 1 January 2019.

Liquidity needs

In the period under review, the average daily liquidity needs of the banking system, defined as the sum of net autonomous factors and reserve requirements, stood at €1,511.5 billion, an increase of €51.8 billion compared with the previous review period (i.e. the fifth and sixth maintenance periods of 2018). This rise in liquidity needs was largely the result of an increase in net autonomous factors, which grew on average by €51.4 billion to €1,384.5 billion during the review period, while minimum reserve requirements increased on average by €0.4 billion to €127.1 billion.

The growth in net autonomous factors was due to an increase in liquidity-absorbing factors and a decrease in liquidity-providing factors. Among liquidity-absorbing factors, banknotes in circulation and other autonomous factors rose on average by €16.8 billion to €1,210 billion and by €18.5 billion to €730.7 billion respectively, partly offset by a decline in government deposits of €23.3 billion to €236.1 billion. The most significant contribution to the growth in net autonomous factors came from a decrease in net assets denominated in euro, which declined on average by €46.7 billion to €153.5 billion. Eurosystem liabilities to non‑euro area residents in euro increased on average by €50.5 billion, reflecting a more pronounced seasonal pattern at the year-end than at the quarter-end during the previous review period[1] and thus contributing negatively to the (liquidity-providing) average net assets denominated in euro.

Table A

Eurosystem liquidity conditions

Liabilities – liquidity needs (averages; EUR billions) Source: ECB. 1) “Minimum reserve requirements” is a memo item that does not appear on the Eurosystem balance sheet and therefore should not be included in the calculation of total liabilities.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

2) The overall value of autonomous factors also includes “items in course of settlement”.

Assets – liquidity supply

(averages; EUR billions)

Other liquidity-based information

(averages; EUR billions)

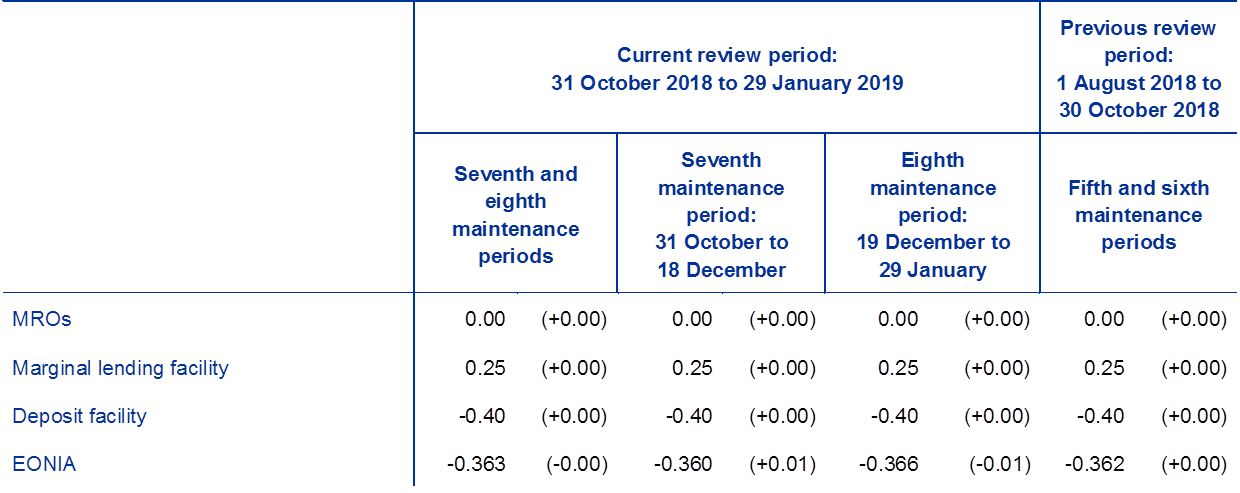

Interest rate developments

(averages; percentages)

Liquidity provided through monetary policy instruments

The average amount of liquidity provided through open market operations – including both tender operations and APP purchases – increased by €35.7 billion to €3,379.8 billion (see Chart A). This increase was fully attributable to net APP purchases, while demand for tender operations decreased slightly.

Chart A

Evolution of open market operations and excess liquidity

(EUR billions)

Source: ECB.

The average amount of liquidity provided through tender operations declined slightly over the review period, by €6.6 billion to €732.5 billion. This decrease was entirely due to a lower average outstanding amount of targeted longer-term refinancing operations (TLTROs), which decreased by €9.2 billion. The average liquidity provided through MROs increased by €2.5 billion to €7.3 billion, which partially offset the decline in TLTROs.

Liquidity provided through the Eurosystem’s monetary policy portfolios increased by €42.2 billion to €2,647.2 billion on average, owing to net APP purchases, which continued into December 2018. However, the size of the increase shrank by €24.8 billion compared to the previous review period. Liquidity provided by the public sector purchase programme, the third covered bond purchase programme, the corporate sector purchase programme and the asset-backed securities purchase programme rose on average by €30.9 billion, €3.9 billion, €8.4 billion and €0.3 billion respectively. Redemptions of bonds held under the Securities Markets Programme and the previous two covered bond purchase programmes totalled €1.3 billion.

Excess liquidity

As a consequence of the developments detailed above, average excess liquidity decreased slightly compared with the previous review period, by €16.1 billion to €1,868.2 billion (see Chart A). This decrease reflects higher net autonomous factors, mainly in the eighth maintenance period, driven partly by year-end developments in liabilities to non-euro area residents in euro, which were only partially offset by the liquidity provided through the APP purchases, which slowed down towards the end of December, prior to entering the reinvestment phase on 1 January. Regarding the allocation of excess liquidity holdings between current accounts and the deposit facility, average current account holdings marginally declined by €0.5 billion to €1,357.6 billion, and average recourse to the deposit facility declined by €15.2 billion to €637.8 billion.

Interest rate developments

Overnight unsecured and secured money market rates remained close to the ECB deposit facility rate. In the unsecured market, the euro overnight index average (EONIA) averaged −0.363%, almost unchanged from the previous review period. The EONIA fluctuated between a low of −0.374% observed on 21 December and a high of −0.335% observed on 27 December. Regarding the secured market, the spread between the average overnight repo rates for the standard and the extended collateral baskets in the general collateral (GC) pooling market[2] narrowed. Compared to the previous period, the average overnight repo rate for the standard collateral basket increased by 2 basis points to −0.417%, while for the extended collateral basket it declined by 2 basis points to −0.406%. The 2018 year-end decline in core repo rates was less pronounced than the 2017 year-end decline. This suggests that market participants have adopted more efficient collateral management practices. In addition, the Eurosystem public sector purchase programme securities lending facility continued to support the smooth functioning of the repo market.

- Eurosystem liabilities to non-euro area residents in euro mainly consist of euro-denominated deposits in accounts held by non-euro area central banks with the Eurosystem. Quarter-ends, and to a lesser extent month-ends, are typically affected by increases in these deposits, as commercial banks are more reluctant to accept cash, either in the unsecured or secured market, ahead of balance sheet reporting dates. On 31 December 2018 liabilities to non-euro area residents denominated in euro increased to €459.3 billion, compared to an average of €315.3 billion during the seventh and eighth maintenance periods. This implied a more pronounced effect than that observed on 30 September 2018, when these liabilities increased to €301.7 billion, compared to an average of €264.7 billion in the fifth and sixth maintenance periods.

- The GC Pooling market allows repurchase agreements to be traded on the Eurex platform against standardised baskets of collateral.