Oil prices, the terms of trade and private consumption

Published as part of the ECB Economic Bulletin, Issue 6/2018.

Oil prices affect private consumption through direct and indirect channels. An increase in oil prices affects households’ purchasing power directly through higher prices for oil-based energy products (e.g. petrol, heating oil). In the euro area about one-third of the economy’s total oil use is in the form of final consumption, i.e. the use by consumers of such products (Chart A). The other two-thirds comes from oil being used in the production of non-energy goods. A rise in oil prices implies an increase in the production costs of these sectors. If these costs cannot be passed on to the final prices of these goods, there will be an indirect impact on households’ purchasing power, since either wages or profits received from these sectors will be lower.[1] Moreover, for advanced economies that produce oil (e.g. Canada, Norway, the United Kingdom and the United States) the indirect effects through wages and profits from the oil-producing sector are even more important.

Chart A

Oil use in the euro area

(EUR billions)

Sources: Eurostat and ECB calculations.

Note: Data refer to coke and refined petroleum products and are at current and basic prices.

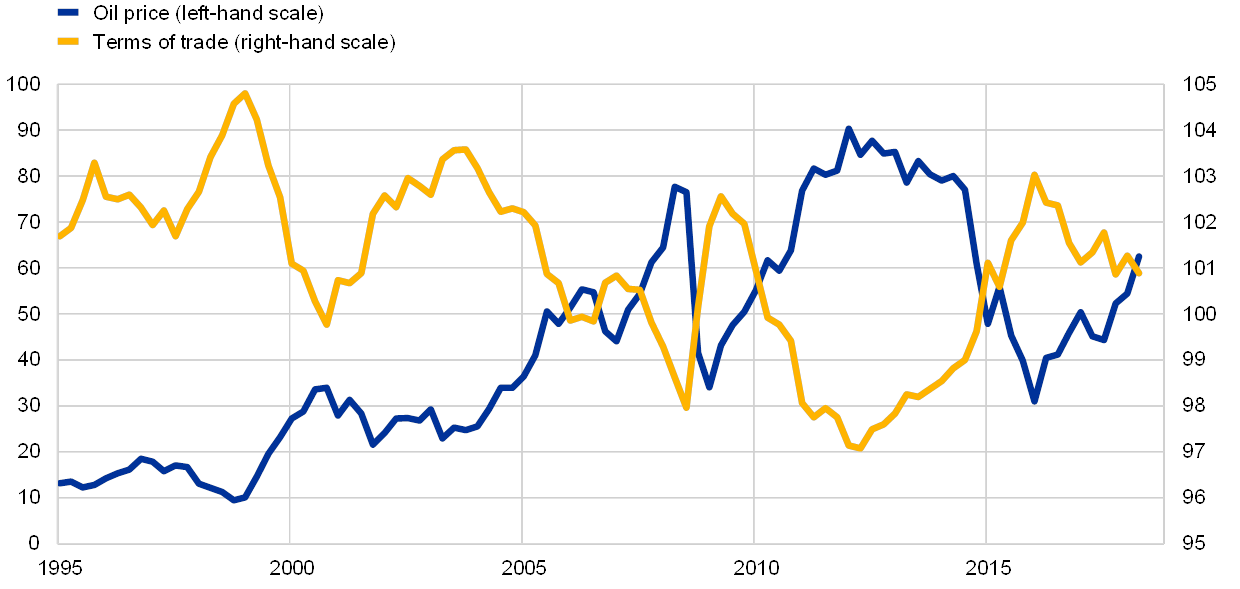

The terms of trade are highly correlated with oil price fluctuations. Changes in the relative prices of exports and imports, or the terms of trade, typically affect private consumption. The terms of trade can be interpreted as the amount of imported goods an economy can purchase per unit of exported goods. Chart B shows that the euro area’s terms of trade are highly correlated with oil prices.[2] When oil prices rise, the terms of trade deteriorate and household purchasing power falls. The strong correlation between oil prices and the terms of trade is widespread globally.[3] The correlation is typically negative for net oil importers and positive for net oil exporters. This relationship can change over time, as a result of either changes in the oil-intensity of consumption and the production of non-energy goods, or changes in oil production. The relationship between oil prices and consumption is thus inherently unstable.

Chart B

Oil prices and the terms of trade

(EUR per barrel; 2010 = 100)

Sources: Eurostat and ECB calculations.

Note: The terms of trade are calculated as the ratio of the export deflator over the import deflator.

The impact of oil price changes on real disposable income can be proxied by the differential between the deflators of GDP and consumption. Chart C presents a decomposition of household real disposable income, i.e. the income of households after tax and benefits, adjusted for price changes. It uses the differential between the deflators of GDP and consumption to capture the impact of oil-related changes in the terms of trade; for the euro area, the correlation between oil prices and this differential is negative. The measure is theoretically well-founded and captures both the direct and indirect channels through which oil prices affect household real disposable income.[4] Even if the channels through which oil prices affect the economy change, this approach still shows stability in the relationship between oil-induced changes in purchasing power and private consumption. This is relevant in the face of changes in the oil-intensity of consumption and innovations in the production of oil and non-energy goods; for example due to higher energy efficiency or new technologies to produce shale oil.[5]

Chart C

Household disposable income and consumption

(annual percentage changes; percentage points)

Sources: Eurostat and ECB calculations.

Notes: All income components are deflated with the GDP deflator. The contribution from the terms of trade is proxied by the differential between the GDP and consumption deflators. Consumption and total disposable income are deflated with the consumption deflator.

Recent oil price increases are not expected to derail the expansion of private consumption. While the drop in oil prices in 2014 and 2015 certainly supported the expansion of private consumption, the overall growth of real disposable income since 2013 has been largely driven by labour income (Chart C). From mid‑2017 to mid‑2018 oil prices increased from about USD 50 to about USD 75 per barrel. If they remain at their present level, the increase is unlikely to significantly dent the growth of real disposable income and private consumption. Moreover, oil prices are still far below the levels observed from 2011 to 2014. As labour markets continue to improve, private consumption growth is expected to remain robust.[6]

- To the extent that producers of non-energy goods do adjust their prices to changes in oil prices, the purchasing power of households will be affected directly, as through the consumption of oil-based energy products.

- In principle the terms of trade can also be affected by other factors (e.g. the nominal exchange rate, the prices of goods and services other than oil). Empirically, however, most of the variation in the euro area terms of trade is explained by oil prices.

- See Backus, D. and Crucini, M., “Oil prices and the terms of trade”, Journal of International Economics, Vol. 50, No 1, pp. 185‑213.

- See Blanchard, O. and Galí, J., “The Macroeconomic Effects of Oil Price Shocks: Why Are the 2000s so Different from the 1970s?”, in Galí, J. and Gertler, M. (eds.), International Dimensions of Monetary Policy, University of Chicago Press, 2010, pp. 373‑421.

- See Fosco, M. and Klitgaard, T., “Recycling Oil Revenue”, Liberty Street Economics, Federal Reserve Bank of New York, 14 May 2018.

- See the article entitled “Private consumption and its drivers in the current economic expansion”, Economic Bulletin, Issue 5, ECB, 2018.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts