The 2018 Ageing Report: population ageing poses tough fiscal challenges

Published as part of the ECB Economic Bulletin, Issue 4/2018.

This box presents the main projection results of the 2018 Ageing Report for euro area countries. The 2018 Ageing Report, published on 25 May 2018, is the latest of the reports prepared every three years by the Ageing Working Group of the Economic Policy Committee.[1] The report provides long-term projections of total public age-related costs and their components, which comprise pensions, health care, long-term care, education expenditure and unemployment benefits, for all EU countries over the period 2016‑70. These projections are, of course, dependent on the underlying assumptions.[2]

The euro area population is ageing. The old-age dependency ratio in the euro area, i.e. the number of people aged 65 or older relative to the working age population, is projected by Eurostat to rise by 20 percentage points between 2016 and 2070, reaching 52% in 2070. If not addressed through decisive policy action, population ageing could have adverse implications for the public debt trajectory and potential growth.[3]

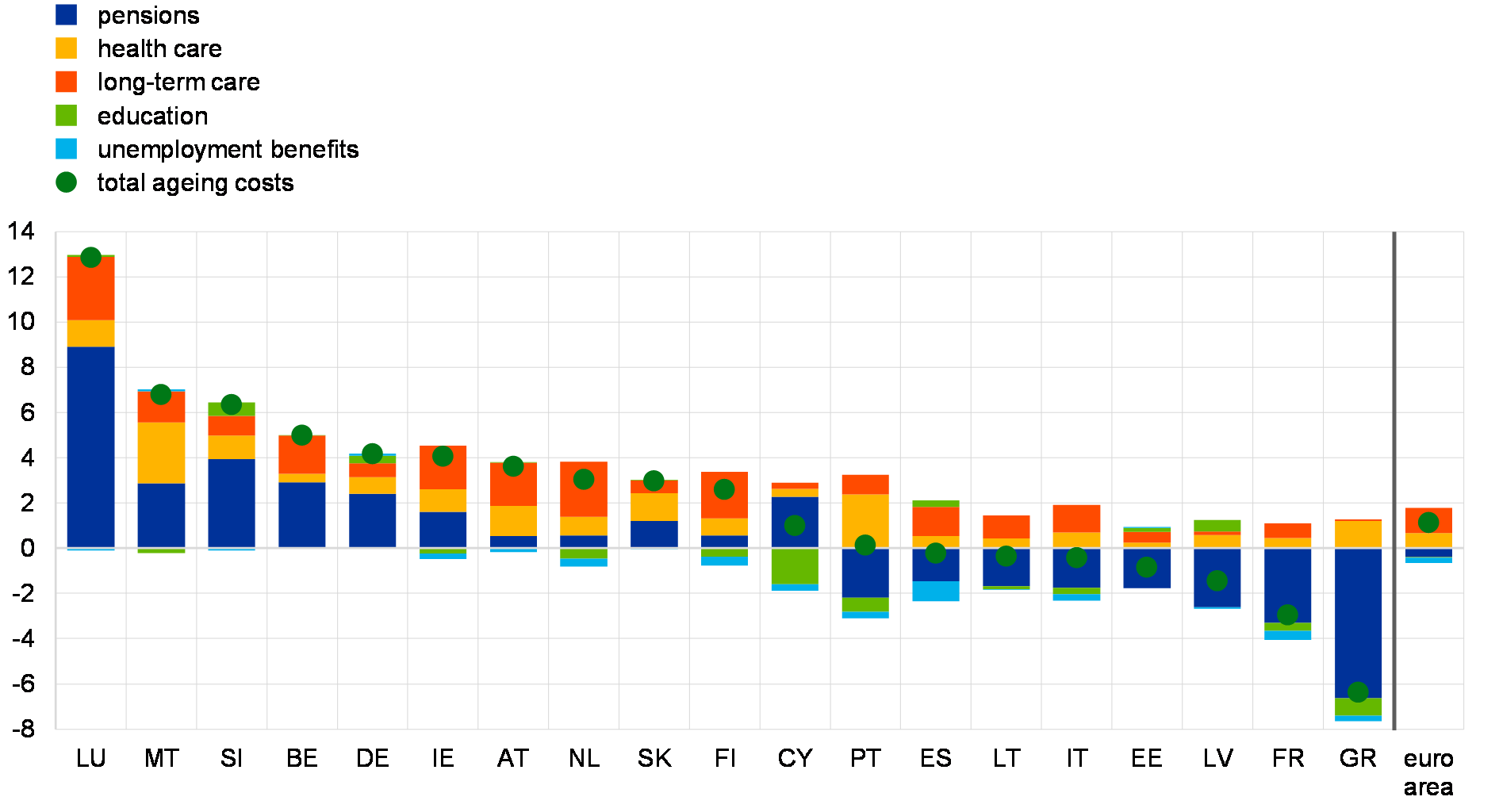

According to the 2018 Ageing Report, total public ageing costs in the euro area are projected to increase by 1.1 percentage points of GDP over the projection horizon (2016-70), rising from 26% of GDP in 2016 to 28.2% of GDP in 2040, before declining again to 27.1% of GDP in 2070. The report shows that ageing costs in the euro area will peak in the early 2040s with the baby boomer generation in retirement, and partly decline from 2050 onwards.[4] Ageing cost estimates differ substantially across countries, and this variance is expected to increase towards the end of the projection horizon. By 2070, ageing costs are projected to be highest in Belgium, Luxembourg, Austria and Finland, reaching levels above 30% of GDP, compared to around 15% of GDP in Latvia and Lithuania (Chart A). Over the projection horizon, ageing costs are expected to increase in 11 countries, remain broadly unchanged in four countries and decline in four countries. The most notable increases are projected for Luxembourg, followed by Malta, Slovenia and Belgium, while the most significant declines are projected for Greece and France (Chart B).

Chart A

Total public ageing costs

(percentages of GDP; 2016, 2040 and 2070)

Sources: 2018 Ageing Report and ECB calculations.

Note: Weighted average for the euro area.

Chart B

Changes in total public ageing costs and their components

(percentage points of GDP; 2016‑70)

Sources: 2018 Ageing Report and ECB calculations.

Note: Weighted average for the euro area.

The total ageing cost projections are largely influenced by public pension costs, followed by health care and long-term care costs.[5] On average, public pension costs in the euro area are expected to increase by 1.3 percentage points of GDP by 2040, but to decline by 0.4 percentage point of GDP over the whole projection horizon to 11.9% of GDP in 2070. There is, however, significant heterogeneity across countries. Public pension costs are the most important driver of increasing ageing costs in Belgium, Luxembourg, Slovenia, Germany, Malta and Cyprus, while they contribute significantly to the decline in ageing costs in Greece and France. By contrast, in all countries, health care and long-term care costs contribute positively to the change in total ageing costs, despite large cross-country heterogeneity (Chart B).

Public pension cost dynamics are driven by opposing factors. On the one hand, the rise in the old-age dependency ratio due to population ageing is expected to increase pension cost pressures in all countries. On the other hand, this impact is expected to be compensated by projected declines in other factors, namely (i) the benefit ratio, (ii) the coverage ratio, and (iii) the labour market effect (Chart C). The decline in the benefit ratio (i.e. pension benefits relative to wages) reflects past reforms that reduce the accumulation of pension benefits, but also relatively favourable assumptions regarding labour and total factor productivity via their impact on wages. The coverage ratio (i.e. the number of pensioners relative to the number of people aged 65 or older) is projected to decline in almost all countries, mainly due to measures restricting access to early retirement and raising the statutory retirement age. Finally, the labour market effect (i.e. the impact on pension costs of labour market changes affecting employment, working time and the old-age participation rate) is projected to decline owing to the impact of reforms (e.g. encouraging longer working careers) and the assumption that the unemployment rate converges to a lower structural rate in the long run. Overall, the projected pension cost developments are the result not only of past reform efforts but also of partly favourable underlying assumptions.

Chart C

Drivers of pension cost projections

(percentage points of GDP; 2016-70)

Sources: 2018 Ageing Report and ECB calculations.

Note: Weighted average for the euro area.

The Ageing Report projections are exposed to substantial adverse risks arising from the favourable underlying assumptions. If the underlying demographic and macroeconomic assumptions do not materialise as expected, this would result in substantially higher ageing costs. Total factor productivity is assumed to converge to a growth rate of 1% per year in the long run in all countries, which implies a strong improvement for the majority of countries relative to current values (Chart D). In addition, structural unemployment is projected to decline to an average rate of 6.8% in the long run, from 10.2% in 2016. While the projections are made under the “no policy change” assumption, it is, however, very unlikely that it would be possible to achieve significantly higher productivity and lower structural unemployment rates without major structural reforms. Moreover, for several countries, Eurostat’s population projections seem optimistic when compared to projections by national authorities or the United Nations.

Chart D

Total factor productivity: past, current and projected growth rates

(percentages per annum)

Sources: 2018 Ageing Report, European Commission and ECB calculations.

Further risks relate to the reversal of enacted reforms. The report assumes that all pension reforms legislated in recent years will be fully implemented. However, in some countries (e.g. Italy and Spain), there seems to be a high risk that previously adopted pension reforms will be reversed. Moreover, the risk of reform reversals could rise for countries currently projecting major declines in pension benefit ratios. Alternatively, in such cases, the risk of continuously rising social assistance transfers could increase if private pension arrangements fail to fill the gaps.

Overall, further reform efforts are needed in a number of countries to curb the expected increase in public ageing costs in an environment of already high public debt levels. Against this background, it will be important that countries take additional decisive policy action and increase their structural reform efforts in the area of pensions, health care and long-term care.

- See “The 2018 Ageing Report: Economic & Budgetary Projections for the 28 EU Member States (2016‑2070)”, European Commission, May 2018.

- The Ageing Report projections are based on a set of demographic and macroeconomic assumptions and a commonly agreed methodology. These were published in a separate report entitled “2018 Ageing Report: Underlying Assumptions & Projection Methodologies”, European Commission, November 2017. As discussed later, for a number of countries, these underlying assumptions are rather favourable.

- For an analysis of ageing cost-related challenges and the role of pension reform, see the article entitled “The economic impact of population ageing and pension reforms”, Economic Bulletin, Issue 2, ECB, 2018.

- Compared with the previous Ageing Report from 2015, total public ageing costs in the euro area are projected to increase by 0.6 percentage point more between 2016 and 2060, which was the end-date of the previous projections. However, the projected ageing-cost level in 2060 remains almost unchanged at 27.6% of GDP, owing to the downward revision of the 2016 level.

- In 2016 almost half of the total ageing costs consisted of pension expenditure (45%), with lower shares for health care (27%), education (18%), long-term care (6%) and unemployment benefits (3%).

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts