Private consumption and its drivers in the current economic expansion

Private consumption and its drivers in the current economic expansion

Published as part of the ECB Economic Bulletin, Issue 5/2018.

This article documents the key role that private consumption has played in recent output growth (2013‑18), and asks how long the current growth in consumption can continue and whether it is self-sustaining. To that end, this article tries to identify the relative importance of different factors driving consumption, such as the recovery in the labour market, accommodative monetary policy, the 2014‑15 drop in oil prices, the increase in asset prices, the easing of credit conditions and deleveraging. As the fall in consumption from 2008 to 2013 was very heterogeneous across countries, this article also sheds light on the extent to which the current expansion has actually led to a net increase in consumption over the past decade. This is relevant because private consumption is also a prime indicator of the economic well-being of households.

While the growth of consumption has been low compared with previous expansions, since 2013 it has exceeded initial expectations. It has been driven mainly by the recovery in the labour market, even though unemployment in some countries and for some groups of workers remains higher than before 2008. Looking forward, as labour markets continue to improve, private consumption should expand further in all countries and for all groups of workers. Through its impact on the labour market, the ECB’s accommodative monetary policy is not only contributing to the expansion of private consumption, but also to a decrease in inequality. At the same time, there is little evidence that low interest rates have led to generalised increases in household indebtedness, supporting the sustainability of the overall economic expansion.

1 Introduction

Euro area private consumption has played a significant role in the current economic expansion since its start in 2013. In some euro area countries the initial increase in private consumption was even stronger than the increase in investment, although that is typically the fastest-growing demand component during an economic expansion. Five years into the current expansion, the question is how long the current pace of consumption growth can continue. For an assessment of the current euro area economic outlook it is therefore essential to uncover the drivers of the recent expansion in private consumption.

The analytical approach in this article has been influenced by the lessons from the financial crisis. It has long been recognised that certain aspects of the data are at odds with the standard life-cycle/permanent income hypothesis, which suggests that private consumption should not react to transitory income changes.[1] This has led to several extensions of the theory of consumption (including income uncertainty and liquidity constraints) stressing the importance of individual household characteristics.[2] The importance of this was further demonstrated by economic developments during and after the Great Recession. This article therefore presents evidence on the drivers of private consumption both from an aggregate and a disaggregate perspective, including the interaction with income and wealth inequality. In addition, the country-specific macroeconomic environment, in particular through conditions in labour and housing markets, has greatly affected private consumption dynamics across countries in the euro area. The country dimension is therefore explored in more depth where relevant.

This article is structured as follows. Section 2 assesses the strength of consumption growth in the ongoing expansion, both from a historical perspective and across different countries and consumption categories. Section 3 reviews the drivers of real household income. Section 4 reviews developments in household wealth and indebtedness. Section 5 concludes and assesses the outlook for consumption growth. Box 1 provides more detailed evidence on the importance of income and wealth effects for euro area private consumption. Box 2 analyses the interaction between monetary policy, household inequality and private consumption.

2 Consumption in the ongoing economic expansion

2.1 A consumption-led economic expansion?

Since the beginning of the current economic expansion in 2013, growth has been driven mainly by private consumption. As private consumption is the biggest expenditure component, this may be considered normal; in 2017 private consumption accounted for about 55% of gross domestic product (GDP). However, it stands in stark contrast to the 2009‑11 recovery, where on average only about 10% of euro area GDP growth was driven by private consumption (see Chart 1).[3] This observation is not confined to the euro area only. In the recent economic expansion many industrialised countries have witnessed strong consumption dynamics, often with consumption growth exceeding that of investment.[4]

Chart 1

Average contributions to GDP growth

(quarterly percentage points)

Sources: Eurostat and ECB calculations.

Private consumption growth has systematically exceeded professional forecasters’ initial expectations. Chart 2 shows how, for every year since the start of the current economic expansion, actual annual consumption growth has exceeded the initial forecasts for private consumption. This is particularly evident in 2014‑15, when the initial consumption growth forecasts considerably underestimated the final momentum of this expenditure component. This period coincided with an unexpected drop in oil prices, which gave a considerable boost to euro area households’ purchasing power. Since then, consumption growth has hovered around 1.7% per annum.

Chart 2

Monthly forecast vintages of euro area private consumption

(annual percentage changes)

Sources: Consensus Economics, Eurostat and ECB calculations.

Note: Dots refer to Eurostat’s most recent release of actual annual consumption growth data.

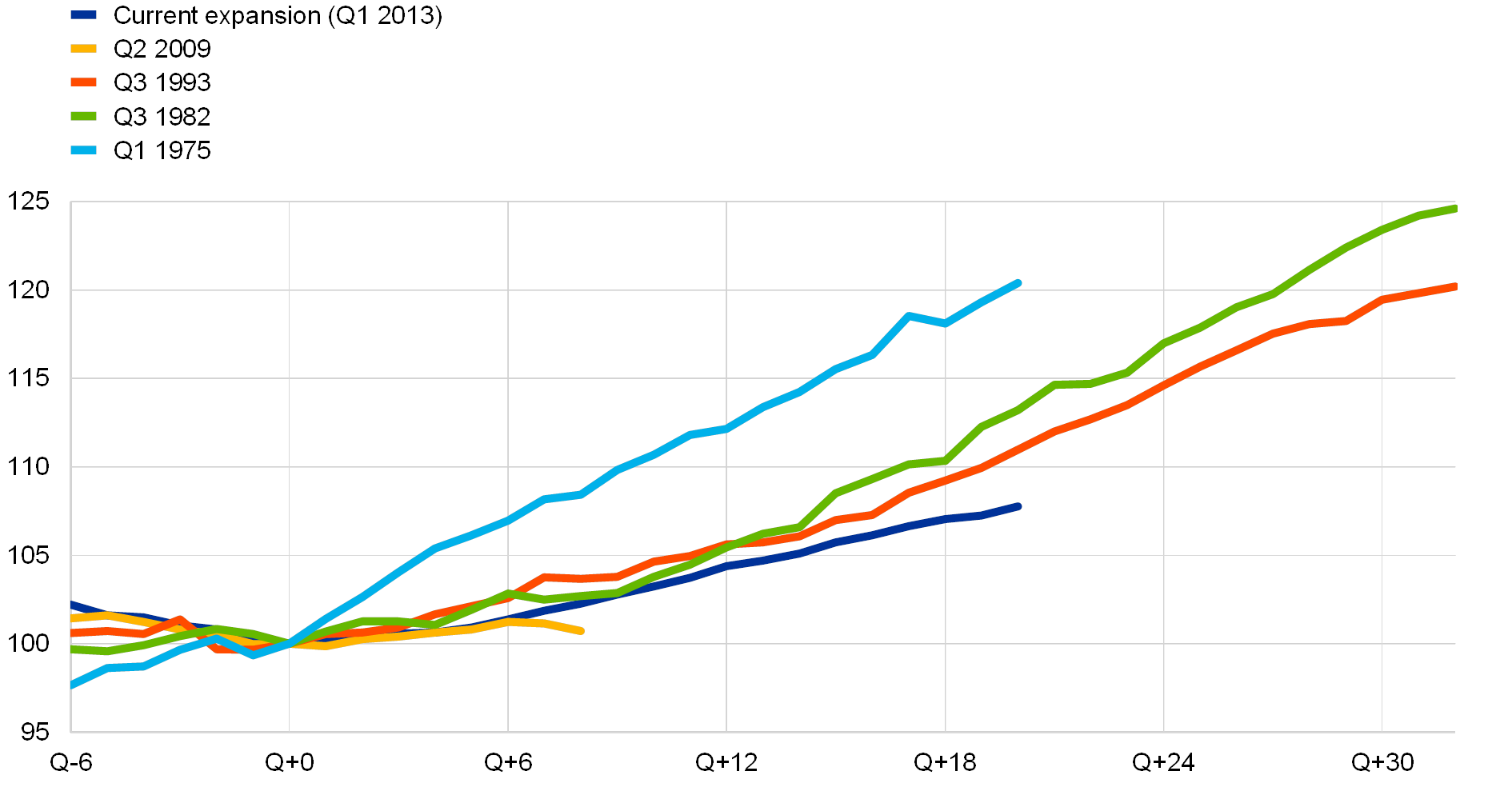

From a historical perspective, the expansion in private consumption has nevertheless remained weak. In fact, the current expansion in private consumption is among the weakest since the 1970s (see Chart 3).[5] However, the recent expansion in GDP has also been among the slowest on record. This observation is again not confined to the euro area only. Most industrialised countries have witnessed GDP growth below that of previous expansions.[6] This raises the question as to how much factors specific to the household sector (e.g. income and wealth developments, or borrowing constraints) have dampened the expansion in private consumption. In other words, has consumer spending that is conditional on household income and wealth been exceptionally weak during the past five years?

Chart 3

Historical expansions of euro area private consumption

(accumulated quarterly changes, Q+0 = 100)

Sources: Eurostat and ECB calculations.

Note: Q+0 represents the trough of the euro area business cycle as identified by the Euro Area Business Cycle Dating Committee.

Since 2013 private consumption has been closely aligned with developments in household income and wealth. Chart 4 presents a counterfactual consumption path, similar to that developed in Pistaferri, based on an estimated relationship between pre-crisis private consumption and household income and wealth developments.[7] The two textbook determinants of private consumption, household income and wealth, seem to explain the largest part of consumption growth since 2013. Only during the period of the Great Recession and the sovereign debt crisis was private consumption lower than this simple relationship with income and wealth would suggest. Since 2013 private consumption has recovered strongly; since mid-2016 it stands even higher than the estimated pre-crisis relationship with income and wealth suggests. This is also in line with a gradual decrease in the household saving ratio over the same period (see Section 4.2).

Chart 4

Consumption dynamics conditional on household income and wealth

(EUR trillions, constant 2010 prices)

Sources: ECB, Eurostat and ECB calculations.

Notes: The historical relationship between private consumption and household income and wealth is estimated using quarterly data from 1999 to 2007. The counterfactual consumption path from 2008 onwards is constructed using that estimated relationship and actual household income and wealth.

2.2 Consumption across countries

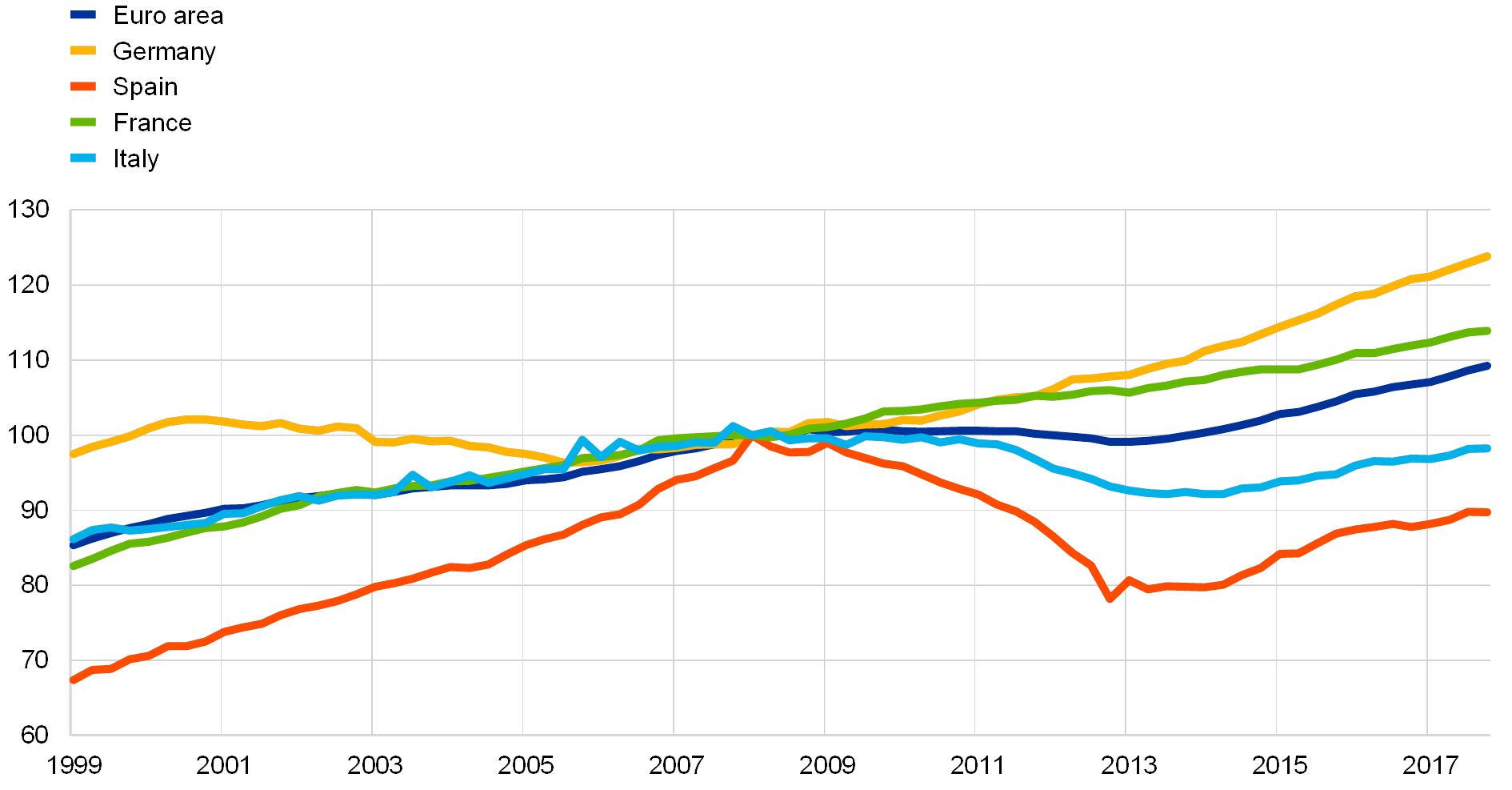

Consumption growth has been broad-based across countries since 2013, but the losses from the financial crisis have not been recouped everywhere. While some large euro area countries experienced strong declines in consumption as a result of the Great Recession and the sovereign debt crisis (e.g. Italy and Spain), other countries (e.g. Germany and France) have been much less affected (see Chart 5). Ten years after the start of the Great Recession private consumption in Germany and France stands about 10% higher than before it began. By contrast, consumption in Italy and Spain has not yet recovered completely. Since 2013, however, all countries have been on a clearly expansionary path. Spain, which experienced the deepest downturn, has shown the strongest expansion since 2013.

Chart 5

Consumption in the four largest euro area countries

(quarterly, EUR thousands per capita, constant 2010 prices)

Sources: Eurostat and ECB calculations.

2.3 Consumption across product categories

Household spending on durable goods is the part of private consumption that is most sensitive to the business cycle. Durable goods typically have an expected lifetime of more than three years, whereas semi-durables and non-durables have a much shorter lifetime. Households do not derive utility directly from spending on durable goods in the current period, but rather from the flow of services they provide over their lifetime. Households may decrease these purchases when their income is low, with a relatively small reduction in their utility, postponing them until periods when their income recovers. As a result, the consumption of durable goods varies more over the business cycle.[8]

Consumption of durables has recovered to “normal” levels. An important factor supporting recent durable goods consumption has been pent-up demand. The sharp drop in durable goods consumption during the crisis resulted in a decline in the effective stock of durables and a commensurate increase in its average age.[9] In the countries that were more affected by the financial crisis the average age of the stock of durable goods also increased more, which gave rise to pent-up demand as soon as economic conditions improved.[10] As the economic recovery progressed, households were able to increase spending on durable goods and offset earlier declines in their stock of durables. Since 2015, however, the positive impact of pent‑up demand for durables has been declining. Following a long catch-up phase for private consumption, this can be regarded as a normalisation (see Chart 6).

Chart 6

Consumption of durable and non-durable goods

(index: 2008 = 100)

Sources: Eurostat and ECB calculations.

Note: The data point for 2017 has been computed using available data on real disposable income and consumption together with the historical income elasticity of durable goods.

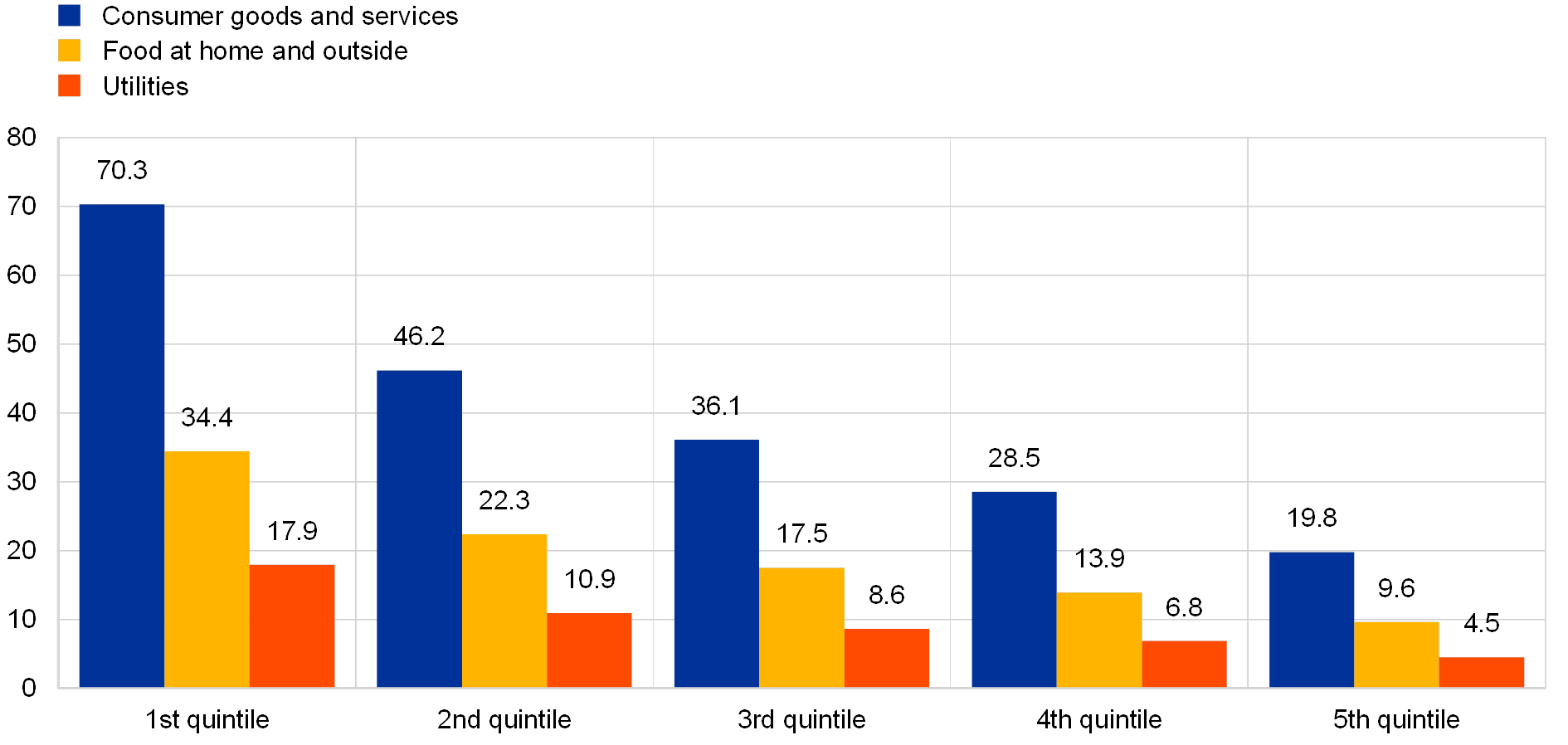

The consumption of necessities, which provide for basic human needs, suggests that there is more room for consumer spending to recover. Private consumption can also be split into necessities (e.g. food, health care and rent) and non-necessities (e.g. electrical appliances, holidays and restaurant visits), which each make up roughly 50% of total euro area private consumption. When households absorb a negative income shock, they mainly adjust their consumption of non‑necessities. As a result, non-necessities have a higher income elasticity than necessities. However, in the long run both components of consumption can be expected to grow at a similar pace.[11] Chart 7 therefore suggests that as household income keeps rising, the consumption of non-necessities should further support total consumption. Put differently, the breakdown between necessities and non‑necessities suggests that the cyclical recovery in euro area consumption can still be expected to last for some time.[12]

Chart 7

Consumption of necessities and non-necessities

(index: 2008 = 100)

Sources: Eurostat and ECB calculations.

Box 1 Income and wealth effects on euro area private consumption

This box reports empirical estimates of income and wealth effects on private consumption in the euro area since 1999. It follows a so-called thick modelling approach that considers a multiplicity of model specifications rather than a single “best” one. Thick modelling considers the uncertainty stemming from both model specifications and unstable parameters.[13] It is particularly useful for empirical applications using a short sample of “true” euro area data that starts in 1999, where model and parameter uncertainty are expected to matter. The thick modelling keeps those model specifications that reliably explain (in-sample) and forecast (out-of-sample) quarter-on-quarter growth of private consumption and have a solid theoretical basis.[14] It uses standard determinants from the consumption literature, distinguishing between long-run and short-run drivers of consumption. In the long run disposable income and wealth determine private consumption, assuming unit elasticity of total income and wealth combined. This assumption implies that consumer spending moves one-to-one with income and wealth in the long term. In the short run, besides income and wealth a rich set of other potential determinants is considered, such as interest rates, indebtedness, uncertainty and demographics.

In the long run, income has been the key driver of private consumption in the euro area since 1999. The estimated long-run elasticities of labour income are greater than those of non‑labour income (alternatively, property and transfer income): typically they are about twice as big. The differences are smaller in terms of the proportion of additional income that an individual consumes, referred to as the marginal propensity to consume (MPC). The MPC out of labour income has been somewhat higher than the MPC out of non-labour income (see Table A). For wealth components, the average long-run elasticity of financial wealth is found to be four to five times larger than that of non-financial wealth. The average MPC out of financial wealth is found to be around 1 cent and out of non-financial wealth 0.1 cent. The estimated wealth effects are similar to those reported in the literature for the euro area.[15]

In the short run, labour income plays a bigger role in consumption growth than the other types of income. In the short run the estimated elasticity ranges are lower than those for the long run and vary between 0.1 and 0.3 for both labour and non-labour income. A similar range results for the second definition of labour income, whereas property and transfer income play a smaller role in consumption growth in the short run. For short-run wealth effects, the estimated elasticity range of financial wealth is smaller than that of non-financial wealth. This is in contrast to the long-run estimates, which show a larger impact for financial wealth than for non-financial wealth. This finding may be explained by the fact that financial asset prices are more volatile in the short run than house prices. Households may perceive financial wealth fluctuations as being less persistent with the result that they do not necessarily have an impact on short-run dynamics in consumption.

Table A

Income and wealth elasticities and marginal propensities to consume

(estimates for Q3 2001‑Q3 2017, marginal propensity to consume (MPC) in euro cents)

Source: Author calculations – see de Bondt, Gieseck and Zekaite.

Notes: Ranges and averages are based on selected equations from a thick modelling approach assuming long-run unit elasticity of income and wealth: 43 for the first income decomposition and 13 for the second. Labour income is defined in two different ways: (i) total compensation of employees minus direct taxes or total compensation of employees minus direct taxes and net social security contributions plus net social benefits and other current transfers; (ii) total compensation of employees plus mixed income (i.e. income of the self-employed) minus both net social security contributions and the labour income share of direct taxes. Property income is the sum of gross operating surplus excluding mixed income, net interest income, net other property income and net other current transfers. Non-labour/transfer income is the remaining part of disposable income.

3 Developments in household income

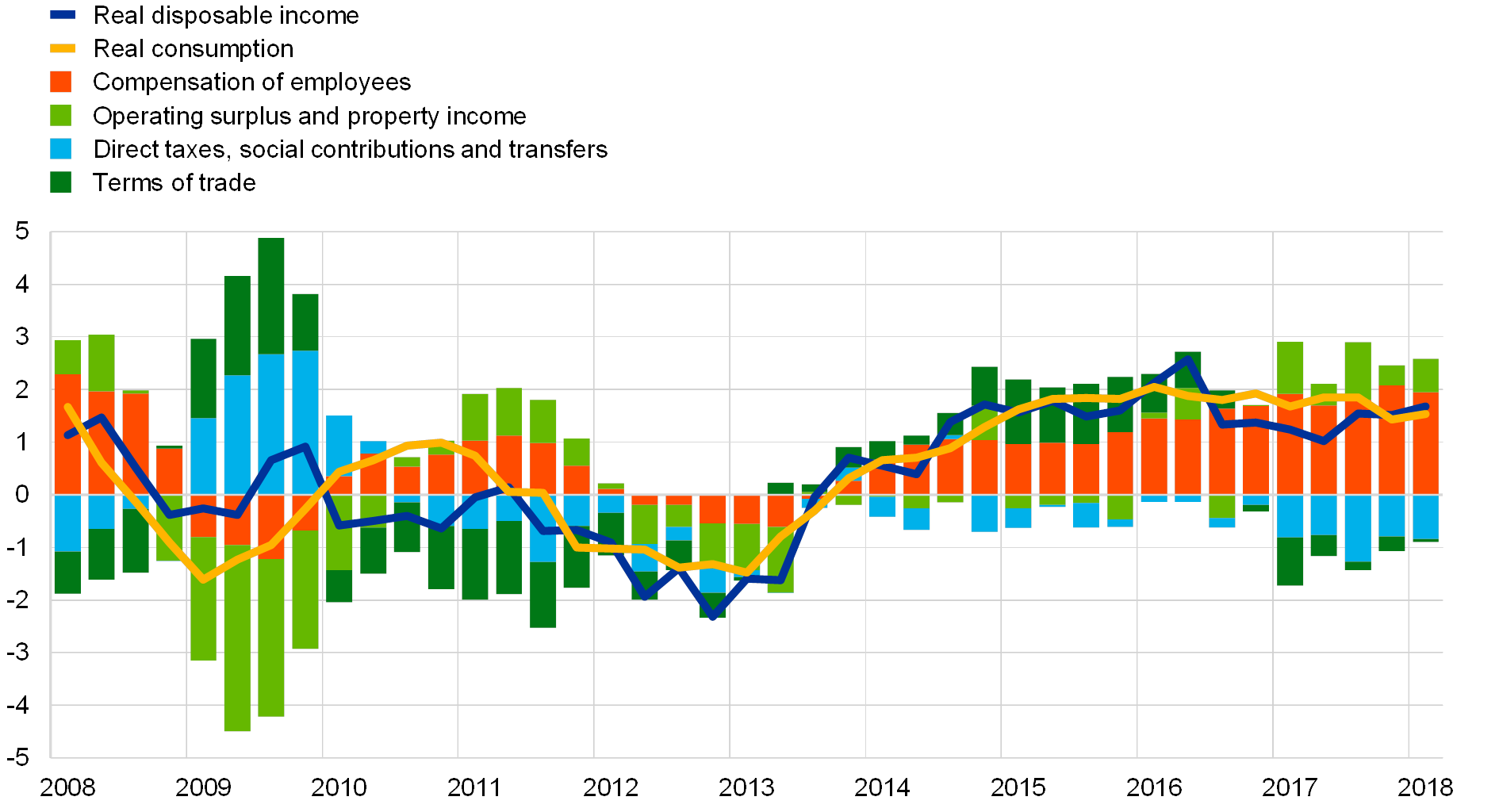

Private consumption growth has closely followed growth in household income. This section sheds more light on the drivers of household income and their implications for overall spending on consumer goods. Chart 8 shows that in the early years of the expansion (2014‑15), real disposable income was strongly supported by improvement in the terms of trade as a result of the fall in oil prices. At the same time, the compensation of employees gradually became the main driver of households’ real disposable income. This stands in stark contrast to the contribution of property and mixed income, or the income households receive from holding assets, which has remained almost unchanged since 2010. As the economic expansion progressed, the contribution of taxes and transfers became somewhat more negative in 2017. In good times automatic fiscal stabilisers tend to have a dampening effect on the growth of real disposable income.

Chart 8

Household real disposable income

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: All income components are deflated with the GDP deflator. The contribution from the terms of trade is proxied by the differential between the GDP and consumption deflators. Consumption and total disposable income are deflated with the consumption deflator.

3.1 Labour income

Despite broad-based increases, labour income in some countries remains significantly below its pre-2008 level. With an increase in the number of employed persons of around eight million since 2013, the current recovery in the euro area labour market has been remarkable.[16] However, these aggregate numbers conceal large differences. For example, in Italy and Spain real compensation of employees remains significantly lower than before the crisis (see Chart 9), on account of both crisis-induced wage moderation and unemployment remaining elevated. Moreover, strong employment growth also reflects increased labour market participation among older as well as female workers. As the unemployment rate in some countries has not yet returned to pre-crisis levels, unemployment risk is still dampening consumption growth to some extent. Despite the strong consumption growth since 2013, this is clearly an important reason why, in these countries, private consumption has not yet recovered to its pre-crisis level (see Chart 5).[17]

Chart 9

Household real labour income across countries

(index: 2008 = 100)

Sources: Eurostat and ECB calculations.

Note: Real labour income is measured as compensation of employees divided by the consumption deflator.

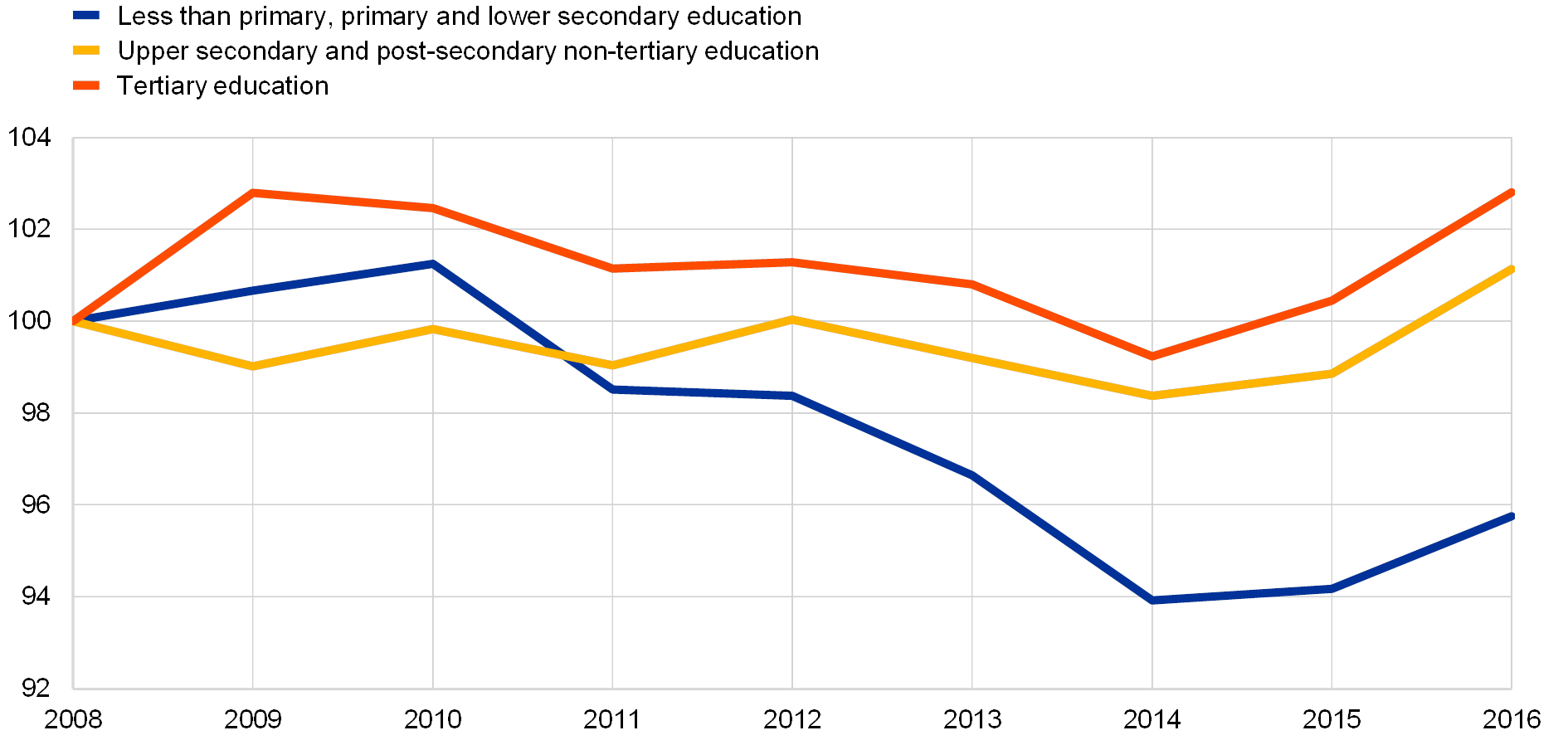

Income risk remains elevated in the lower part of the income distribution. While the recovery in the labour market has boosted household income growth over the past few years, a significant share of the population continues to face a high degree of income risk. Chart 10 shows how net household income for lower skilled workers has remained far below that for higher skilled workers (see also Box 2). This is even more true for low-skilled workers in countries that were more affected by the financial crisis (e.g. Italy, Spain).[18]

Chart 10

Net household income across skill groups

(mean equivalised net income, 2008 = 100)

Sources: Eurostat and ECB calculations.

Note: Equivalised disposable income is the total income of a household, after tax and other deductions, that is available for spending or saving, divided by the number of household members converted into equalised adults; household members are made equivalent by weighting each according to their age.

Falling unemployment should continue to support aggregate consumption growth. Households in the lower part of the income distribution (i.e. mostly lower skilled and/or younger workers) typically have a higher propensity to consume (see Chart 11). As the recovery in the labour market also reaches these households, aggregate consumer spending should receive additional impetus and continue to contribute to a low aggregate saving ratio (see Section 4.2). In addition, as the likelihood of becoming unemployed decreases also for low-skilled workers who are already employed, the available evidence suggests that they should also increase their consumption.[19] A lower unemployment rate not only increases income for those that find a job, but also increases the expected future income of those who are already employed (and face lower unemployment risk). All in all, this suggests that as long as the recovery in the labour market remains on track the underlying growth momentum of private consumption can be expected to continue.

Chart 11

Median consumption to income ratio by income quintile

(percentages)

Source: Eurosystem Household Finance and Consumption Survey.

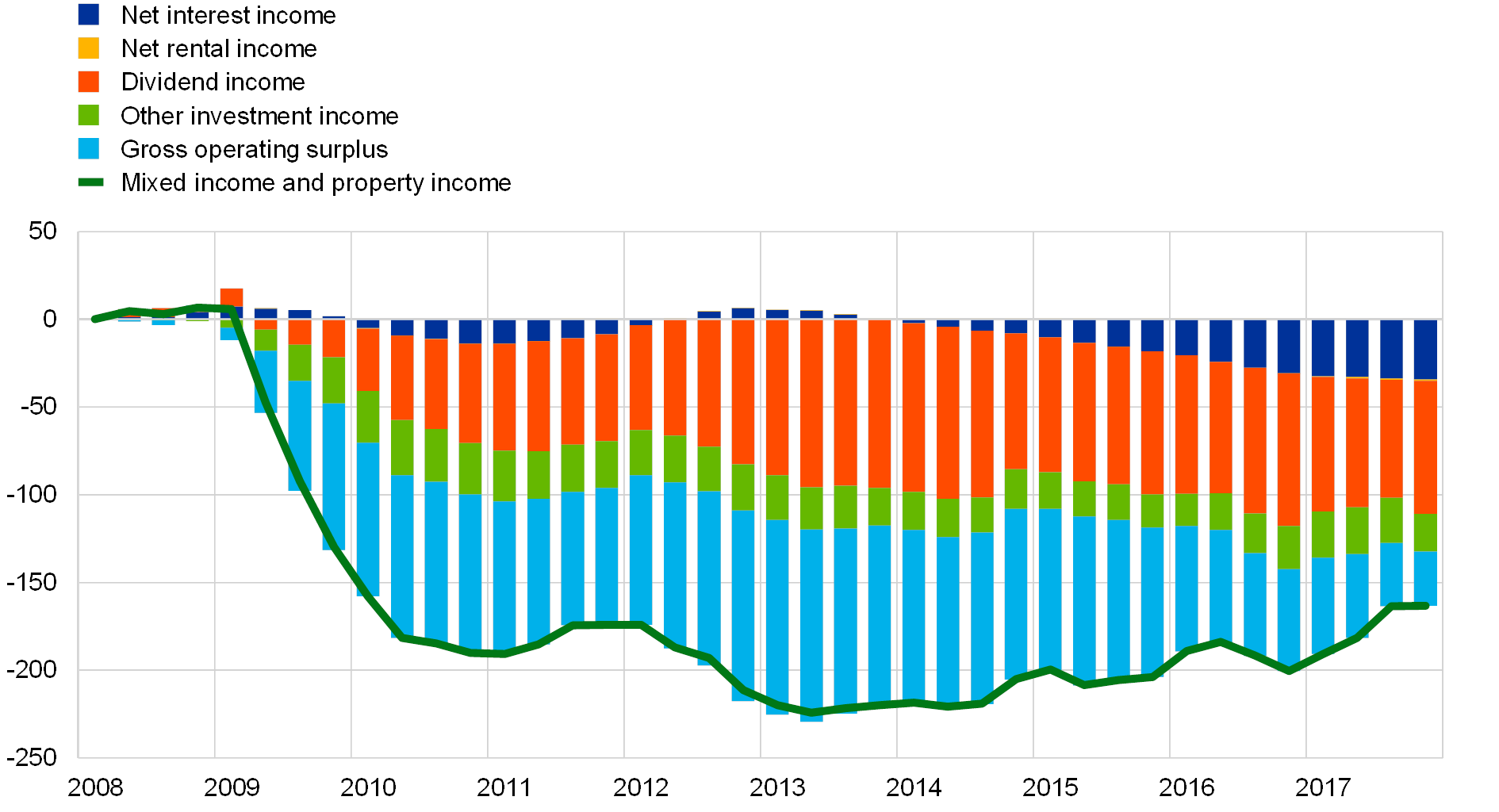

3.2 Property income

Property income has remained weak since 2013, but the impact on private consumption growth seems limited. Together with the fall in economic activity and corporate profitability, property income and mixed income from self-employment has fallen significantly since 2008. This is a normal phenomenon, as profits are strongly procyclical. It is also in line with evidence that income risk across the business cycle is concentrated in the left and the right tails of the income distribution.[20] Poorer households experience larger drops in income from job losses (see previous section), while richer households experience larger drops in property income. This is because aggregate asset holdings are concentrated at the top of the wealth distribution (see Chart 16). In 2013 real mixed income (gross operating surplus) started to increase again, but most other components of property income have remained subdued (see Chart 12). Firms have not yet started to distribute more profits to their shareholders. As richer households also tend to have a higher average saving ratio (see Chart 11), the dampening effect on private consumption may have been contained (see also Box 1).[21] Strong growth of labour income and weak growth of property income is also consistent with a subdued aggregate household saving ratio.

Chart 12

Decomposition of the change in real household property income

(EUR billions, four-quarter moving sums, constant 2010 prices)

Sources: Eurostat and ECB calculations.

Despite exceptionally low interest rates, household net interest income has hardly been affected.[22] While interest earnings declined significantly, interest payments have also decreased considerably. Between the third quarter of 2008 and the fourth quarter of 2017 interest payments fell by about three percentage points relative to disposable income. The drop in interest earnings has been comparable to the drop in interest payments, meaning that the average euro area household’s net interest income has been largely unaffected. Lower interest rates have mainly redistributed resources from net savers to net borrowers. As net borrowers typically have a higher propensity to consume than net savers, this redistribution channel of lower interest rates supports aggregate consumption.[23]

The net interest income of the household sector has remained fairly stable in Germany and France, but less so in Italy and Spain. Evidence from the sectoral accounts (see Chart 13) shows that in Germany and France the drop in interest earnings and payments has been comparable, meaning that lower interest rates have had a minimal effect on the net interest income of the household sector as a whole. Conversely, in Italy, the drop in household interest earnings has been much larger, as Italian households hold a relatively large amount of interest-bearing assets, whereas they are relatively less indebted. In Spain, the drop in interest payments has been significantly larger than the fall in interest earnings. The larger decline in interest payments in Spain is explained by both the high stock of household debt (see Section 4) and the fact that a large share of mortgages have adjustable interest rates. This is an important factor in the transmission of monetary policy to private consumption, as there is evidence that it has a relatively larger effect in countries with adjustable-rate mortgages.[24]

Chart 13

Change in net interest income across countries (2008‑17)

(percentage of gross disposable income, percentage points)

Sources: Eurostat and ECB calculations.

3.3 The 2014‑15 drop in oil prices

In 2014‑15 lower energy prices contributed significantly to the expansion in private consumption. It was also in this period that professional forecasters made the largest upward revisions to their consumption growth forecasts (see Chart 2). The overall decline in oil prices since the second half of 2014 has provided households with a windfall gain. Typically, from a historical perspective, consumption reacts with a lag to changes in oil prices. A model-based forecast in the spirit of Edelstein and Kilian suggests that in 2014‑15 private consumption reacted more quickly to the oil price decline than it had in previous episodes of falling oil prices (see Chart 14).[25] This is also evidenced by the relatively muted response of the household saving ratio to the windfall gain. Since 2016 the support from lower oil prices for consumption growth has faded. Going forward, the latest oil price increase between mid-2017 and mid-2018 is expected to dampen consumer spending somewhat.

Chart 14

Private consumption after the 2014‑15 oil price drop

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The conditional forecast is constructed using the model in Edelstein and Kilian for the euro area. It shows the model-based forecast of consumption conditional on the observed oil prices.

4 Developments in household wealth and debt

The strength of the household sector’s balance sheet is a key determinant of private consumption. First, increases in household wealth make households richer and therefore also more inclined to consume. This is the standard wealth effect (see also Box 1).[26] Second, the strength of the household balance sheet also determines the availability of credit to households, and therefore their ability to smooth consumption over the business cycle. As balance sheets are typically weaker during recessions and stronger during expansions, there is a strong link between the strength of the balance sheet and consumption growth. This is the financial accelerator channel. Chart 15 illustrates how banks’ credit standards have co-moved with the growth of households’ net worth since 2003. Especially after periods of large increases in leverage, asset price falls can lead to large drops in net worth and generate significant deleveraging pressures that may persistently affect consumption dynamics.[27] This section provides more details about how changes in households’ assets and liabilities have affected recent consumption growth.

Chart 15

Credit standards and households’ net worth in the euro area

(left-hand scale: annual percentage changes; right-hand scale: weighted net percentages)

Source: ECB and ECB calculations.

Note: The bank lending survey asks banks how the credit standards applied to the approval of loans to households for consumer credit have changed over the preceding three months. An increase (decrease) represents a tightening (easing) in credit standards.

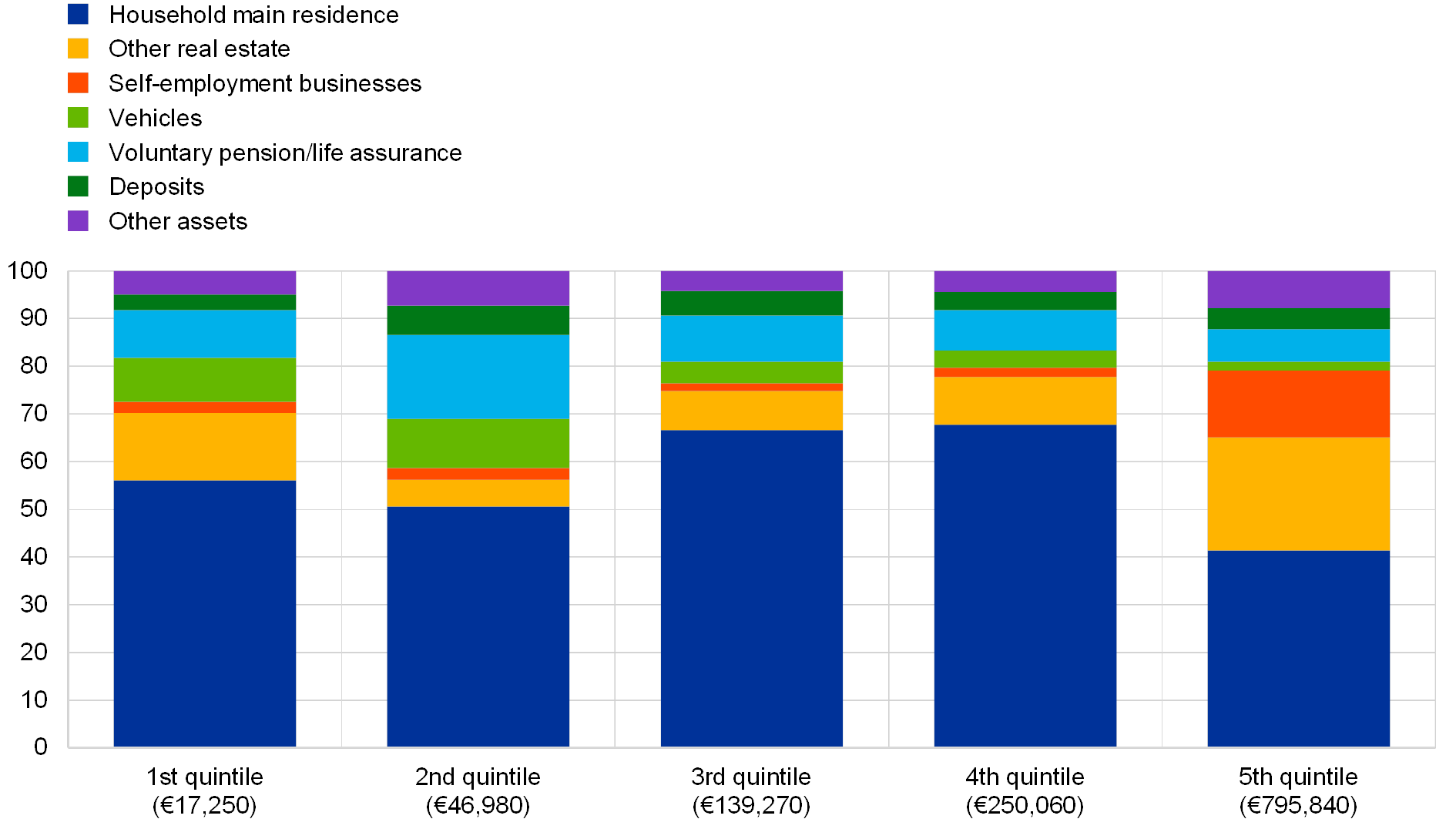

4.1 Household wealth

House price changes can have significant accelerator effects on private consumption. The reason for this is that for most households the main residence is their largest asset (see Chart 16). Housing wealth also tends to be more evenly distributed than financial wealth, which is mainly held by the top quintile of the wealth distribution.[28] Moreover, housing is typically also an asset that is financed by debt (i.e. through leverage), so that house price changes can have even larger effects on households’ net worth. This may explain why, over the business cycle, housing wealth is often found to be more important for private consumption than financial wealth, despite similar direct wealth effects (see also the short-run elasticities reported in Box 1).[29] As the euro area housing market is segmented across countries, cross-country developments in housing wealth have been very heterogeneous.

Chart 16

Average portfolio by net wealth quintile, euro area

(percentages)

Source: Eurosystem Household Finance and Consumption Survey.

Note: The amounts in parentheses show the total size of the average portfolio in each quintile.

Housing wealth has developed very heterogeneously across euro area countries. While housing wealth in Germany started to increase significantly in 2013, in France it remained virtually flat over the same period (see Chart 17). In Spain housing wealth has started to increase again recently, but remains about 30% lower than before the Great Recession. In Italy, housing wealth has declined gradually. This contrasts with financial wealth, where developments have been much less heterogeneous across countries. Consequently, housing wealth seems also more relevant than financial wealth for explaining persistent cross-country differences in private consumption (see Chart 5).

Chart 17

Household real housing wealth across countries

(index: Q1 2008 = 100)

Sources: ECB, Eurostat and ECB calculations.

Note: Household real housing wealth is computed as nominal housing wealth divided by the private consumption deflator.

4.2 Household debt and saving

Decreasing household indebtedness underscores the sustainability of the expansion in private consumption. It has been argued that the current economic expansion is less sustainable, as it is based on private consumption and the accumulation of new debt.[30] This argument is mainly based on the presumption that consumption-led recoveries are always driven by an increase in household indebtedness. This does not apply to the current expansion in euro area consumption. In contrast to the period before the crisis, steady euro area consumption growth has been coupled with a gradual decrease in household indebtedness, which in the euro area has now stabilised around its pre-crisis level (see Chart 18). Moreover, while certain countries have still seen some increases in household indebtedness towards the euro area average (e.g. France), cross-country differences have significantly diminished on account of the strong decreases in those countries where the household sector was most indebted (e.g. Spain).

Chart 18

Household indebtedness

(percentage of gross disposable income)

Sources: ECB, Eurostat and ECB calculations.

Note: Based on four-quarter sums of gross disposable income.

While the household saving ratio remained low, weak household investment has contributed to further deleveraging. Following a temporary increase in the household saving ratio during the 2008‑09 recession, the saving ratio has been gradually declining since 2011. Chart 19 shows how the low household investment ratio gave rise to a high net lending position of the household sector, reflecting lower household borrowing than before the financial crisis. In contrast with household investment, recent consumption growth does not seem to be affected very much by deleveraging pressures. This pattern is strongest in those countries that experienced a boom-bust cycle in the housing market (e.g. Spain).

Chart 19

Household saving and investment ratio

(percentage of gross disposable income)

Sources: Eurostat and ECB calculations.

Since 2013 household deleveraging has changed from “active” to “passive”, making the expansion in consumption more self-sustaining. At the beginning of 2013 the contribution of nominal disposable income to the change in the household debt ratio (as a percentage of gross disposable income) was still close to zero (see Chart 20). Before the start of the current economic expansion, households’ real disposable income was still contracting and inflation falling. As lower asset valuations gave rise to deleveraging pressures, households had to repay loans and refrain from new borrowing (i.e. there was active deleveraging). Once the economic expansion gained traction households’ nominal disposable income growth gradually accelerated, leading to further decreases in household indebtedness. Higher nominal growth led to improvements in balance sheets and contributed to a self-sustaining increase in spending and economic activity (i.e. passive deleveraging took place). Over the past few years, households have again been increasing their debt, although household indebtedness continued to fall relative to income. These higher debt flows reflected loans for house purchase as the recovery in the housing market gradually progressed, as well as higher demand for consumer credit as purchases of durable goods (e.g. cars) increased again.[31]

Chart 20

Changes in household debt ratio

(annual percentage point differences)

Sources: ECB, Eurostat and ECB calculations.

Note: Based on seasonally-adjusted quarterly gross disposable income.

Box 2 Monetary policy, household inequality and consumption

Monetary policy affects individual households differently depending on the composition of their income and wealth. This box estimates how the unemployment rate, income and wealth of different households are affected by the non-standard monetary policy measures recently implemented by the ECB.[32] The results below are based on a simulation which, first, identifies the aggregate effects of an exogenous expanded asset purchase programme (APP) shock (designed to capture the effect of the APP announcements) on asset prices[33] and income, using a vector auto‑regressive model. Then, such aggregate effects are distributed across individual households using micro data on income, wealth and their components from the Eurosystem Household Finance and Consumption Survey.[34]

Chart A

Response of unemployment and net wealth to the asset purchase programme

(upper chart: percentage point change in unemployment rate by income quintile; lower chart: percentage change in median net wealth by net wealth quintile)

Sources: Eurosystem Household Finance and Consumption Survey, and ECB calculations.

Notes: The upper chart shows the decline of unemployment rate in percentage points across quintiles of household income four quarters after the impact of the asset purchase programme (APP). The lower chart shows the increase in median net wealth in percent by net wealth quintile four quarters after the impact of the APP. The numbers in parentheses show the initial level of the unemployment rate and median net wealth in each quintile. Data relate to an aggregate of Germany, Spain, France and Italy.

The APP has substantially reduced the unemployment rate in the lower part of the income distribution.[35] The upper chart above shows how the aggregate decline in the unemployment rate is distributed across various income groups of households. In particular, the chart displays the decrease in the unemployment rate across the five income quintiles, four quarters after the impact of the APP shock. The aggregate decline in the unemployment rate by about 0.7 percentage point affects individuals very heterogeneously and is heavily skewed towards the households with incomes in the lowest 20%, whose unemployment rate falls by more than 2 percentage points. By contrast, the unemployment rate in other income quintiles falls by less than 0.5 percentage point. The key reason for this finding is that the level of unemployment is much higher in the lower parts of the income distribution.

The decline in unemployment rates among households with lower incomes reduces income inequality. Changes in unemployment rates substantially affect household income: incomes increase considerably as households start earning wages (instead of receiving unemployment benefits). Mean income in the lowest income quintile rises by about 3%, while mean income in other parts of the distribution increases by about 0.5%. These changes reduce income inequality: the Gini coefficient, a common measure of inequality, is estimated to decline from 43.1% to 42.8%.

The APP has modestly increased household net wealth across the wealth distribution. As shown in the lower panel of Chart A, the median net wealth among households in the lowest net wealth quintile increases by 2.5%, while in the other quintiles it rises by around 1%. House prices play a key role in these changes, as housing wealth makes up about 70-80% of total household assets and this share is stable across the distribution (possibly with the exception of the very top tail). In addition, the response of stock prices is estimated to be small and transitory. The increase in wealth among the lowest quintile is partly driven by the high leverage of these households. These changes only negligibly affect inequality in net wealth (as measured by the Gini coefficient).

The developments in income and wealth are likely to affect consumer spending. A key factor determining how spending responds to changes in income is the MPC, the response of spending to a transitory increase in income. Substantial empirical literature has documented that households with lower incomes and low liquid assets tend to act in a hand-to-mouth manner: they tend to be liquidity constrained and their consumption is highly sensitive to transitory changes in income. In the euro area almost 25% of households hold little liquid assets and live hand-to-mouth; these households have MPCs of around 0.3, while the remaining households with ample liquid assets are well insured and have much lower MPCs, of around 0.1 or less.

The response of aggregate consumption to monetary policy is disproportionately affected by constrained households. This happens for two reasons. First, as estimated, incomes of households in the lower parts of the distribution are disproportionately stimulated by the APP. Second, these households also tend to have substantially higher MPCs. The response of spending by these households is determined as a product of the two numbers and is consequently substantially stronger than that of households in the upper part of the distribution. Ampudia et al.[36] document that this indirect income channel of monetary policy, which operates by stimulating employment and labour income, is stronger than the intertemporal substitution channel (which operates through households reducing saving and increasing spending following an interest rate cut). The indirect income channel accounts for around 80-90% of the total effect of monetary policy on the spending of “hand-to-mouth” households and for a substantial part of the overall reaction of the remaining households. In the aggregate, the indirect channel makes up about 60% of the total effect. Finally, these calculations also imply that the APP compresses the distribution of consumer spending across households, as the consumption of “hand-to-mouth” households is stimulated more strongly than that of well-insured households.

5 Conclusions

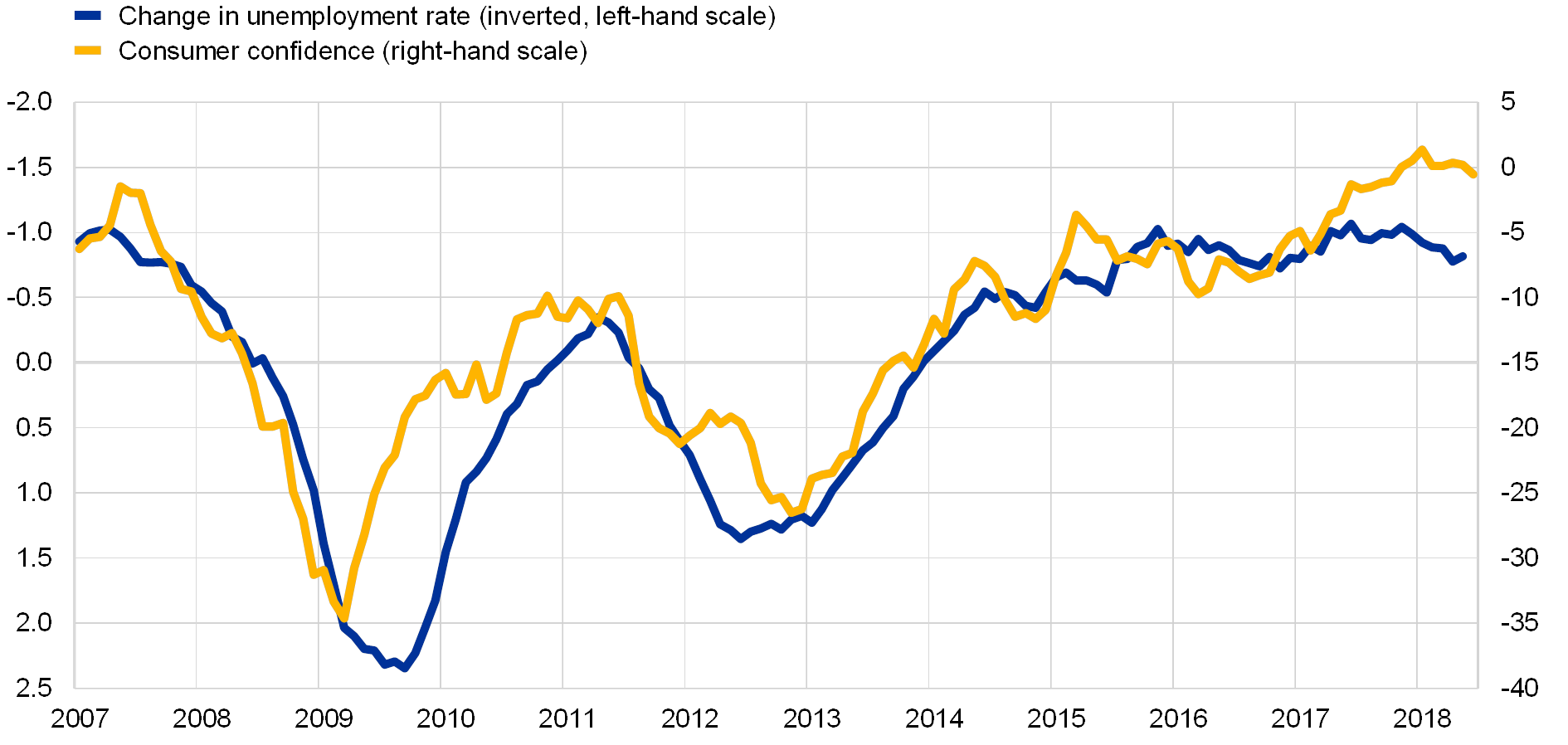

Private consumption has been a main driver of the recent economic expansion, but there is still scope for further growth. In the euro area private consumption has clearly recovered from the losses during the financial crisis. While the growth of consumption has been low compared with previous expansions, since 2013 it has exceeded initial expectations. This has been largely driven by the recovery in the labour market, even though unemployment in some countries and for some groups of workers remains higher than before the financial crisis. Looking forward, as labour markets continue to improve, consumer confidence should remain elevated and private consumption should rise further (see Chart 21).

Chart 21

Change in unemployment rate and consumer confidence

(left-hand scale: annual percentage point differences, right-hand scale: net percentage balances)

Sources: European Commission (Directorate-General for Economic and Financial Affairs), Eurostat and ECB calculations.

The ECB’s accommodative monetary policy has contributed considerably to the expansion of private consumption. There is increasing evidence that monetary policy supports private consumption especially via financially constrained (e.g. unemployed or indebted) households. This highlights the role of heterogeneity in the transmission of monetary policy. At the same time, accommodative monetary policies have also directly decreased income and wealth inequality. Finally, there is little evidence that low interest rates have led to generalised increases in household indebtedness, supporting the view that the overall economic expansion is sustainable.

- See Friedman, M., “A Theory of the Consumption Function”, Oxford Publishing Company, 1957; and Hall, R., “Stochastic Implications of the Life Cycle-Permanent Income Hypothesis: Theory and Evidence”, Journal of Political Economy, Vol. 86, 1978, pp. 971‑987.

- See for instance Deaton, A., “Saving and liquidity constraints”, Econometrica, Vol. 59, 1991, pp. 1221‑1248; Stein, J., “Prices and trading volume in the housing market: a model with down‑payment effects”, Quarterly Journal of Economics, Vol. 110, 1995, pp. 379‑406; and Ahn, S., Kaplan, G., Moll, B., Winberry, T. and Wolf, C., “When Inequality Matters for Macro and Macro Matters for Inequality”, NBER Macroeconomics Annual, Vol. 32, 2017.

- See also the box entitled “Factors sustaining the ongoing recovery”, Annual Report, ECB, 2016.

- See Kharroubi, E. and Kohlscheen, E., “Consumption-led expansions”, BIS Quarterly Review, Bank for International Settlements, March 2017.

- See also Vermeulen, P., “The recovery of investment in the euro area in the aftermath of the Great Recession: how does it compare historically?”, Research Bulletin, No 28, ECB, 2016.

- See for instance Fernald, J., Hall, R., Stock, J. and Watson, M., “The disappointing recovery of output after 2009”, Brookings Papers on Economic Activity, 2017, pp. 1‑54.

- See Pistaferri, “Why has consumption remained moderate after the Great Recession?”, paper presented at the Federal Reserve Bank of Boston’s 60th Economic Conference “The Elusive ‘Great’ Recovery: Causes and Implications for Future Business Cycle Dynamics”, 14 October 2016.

- See “Consumption of durable goods in the ongoing economic expansion”, Economic Bulletin, Issue 1, ECB, Frankfurt am Main, 2018.

- In 2009 consumption of durable goods was temporarily supported by the car scrappage schemes in several countries, which pushed up car sales. See “Recent developments in the consumption of durable goods in the euro area”, Monthly Bulletin, ECB, Frankfurt am Main, May 2014.

- See “Reabsorption of the pent-up demand for consumer durables”, Economic Bulletin, Issue 4, Banco de España, 2017.

- This is confirmed by evidence from France and Finland in the 1980s and 1990s – for which longer time series are available – that shows that as the economy recovers, the path of these two components of private consumption converges again.

- See also McCarthy, J., “Discretionary services spending has finally made it back (to 2007)”, Liberty Street Economics, 16 October 2017.

- See Granger, C.W. and Jeon, Y., “Thick modelling”, Economic Modelling, 21, 2004, pp. 323‑343.

- In technical detail, a five-step process selects those error correction model specifications with: 1) statistically significant coefficients, with the exception of the constant; 2) adjusted R-squared of at least 0.60; 3) no residual autocorrelation; 4) an out-of-sample forecast accuracy gain of at least 15% compared with a benchmark model consisting of only disposable income, financial and non-financial wealth; and 5) an economically meaningful sign of the coefficients. For a detailed description, see de Bondt, G.J., Gieseck, A. and Zekaite, Z., “Income and wealth effects: a thick modelling approach for euro area private consumption”, paper presented at the EcoMod2018 conference, Venice, 4‑6 July 2018.

- For empirical evidence on euro area wealth effects, see Slacalek, J., “What drives personal consumption? The role of housing and financial wealth”, B.E. Journal of Macroeconomics, Vol. 9(1), 2009, pp. 1‑35; and Sousa, R.M., “Wealth effects on consumption: evidence from the euro area”, Working Paper Series, No 1050, ECB, Frankfurt am Main, May 2009.

- See “Labour supply and employment growth”, Economic Bulletin, ECB, Frankfurt am Main, Issue 1, 2018.

- This is also consistent with recent empirical research showing that consumers tend to respond more strongly to negative than to positive income shocks; see Christelis, D., Georgarakos, D., Jappelli, T., Pistaferri, L. and van Rooij, M. “Asymmetric Consumption Effects of Transitory Income Shocks”, CSEF Working Paper, 476.

- In Germany, the unemployment rate for low-skilled workers has fallen from around 20% to below 10% since 2005.

- See Dynarski and Sheffrin, “Consumption and unemployment”, The Quarterly Journal of Economics, Vol. 102(2), 1987, pp. 411‑428; Campos R. and I. Reggio, “Consumption in the shadow of unemployment”, European Economic Review, Vol. 78(C), 2015 pp. 39‑54; and Christelis, D., Georgarakos, D., Jappelli, T. and van Rooij, M., “Consumption uncertainty and precautionary saving”, DNB Working Paper, 496.

- See Guvenen, F., Ozkan, S. and Song, J., “The Nature of Countercyclical Income Risk”, Journal of Political Economy, Vol. 122, 2014, pp. 621‑660.

- See also Dynan, K., Skinner, J. and Zeldes, S., “Do the rich save more?”, Journal of Political Economy, Vol. 112, 2004, pp. 397‑444.

- See the box entitled “Low interest rates and households’ net interest income”, Economic Bulletin, Issue 4, ECB, Frankfurt am Main, 2016.

- See Auclert, A., “Monetary policy and the redistribution channel”, NBER Working Papers, No 23451, 2017.

- See Calza, A., Monacelli, T. and Stracca, L., “Housing finance and monetary policy”, Journal of the European Economic Association, Vol. 11, 2013, pp. 101‑122.

- See Edelstein, P. and Kilian, L., “How sensitive are consumer expenditures to retail energy prices?”, Journal of Monetary Economics, Vol. 56, 2009, pp. 766‑779.

- See Poterba, J., “Stock market wealth and consumption”, Journal of Economic Perspectives, Vol. 14, 2000, pp. 99‑118; and Slacalek, “What Drives Personal Consumption? The Role of Housing and Financial Wealth”, The B.E. Journal of Macroeconomics, Vol. 9, October 2009, pp. 1‑37.

- See Mian, A., Rao, K. and Sufi, A., “Household balance sheets, consumption, and the economic slump”, Quarterly Journal of Economics, Vol. 128, 2013, pp. 1687‑1726.

- See Adam, K. and Tzamourani, P., “Distributional consequences of asset price inflation in the euro area”, European Economic Review, Vol. 89, 2016, pp. 172‑192.

- Iacoviello, M., “Housing wealth and consumption”, Federal Reserve Board Working Papers, No 1027, 2010.

- See Kharroubi, E. and Kohlscheen, E., “Consumption-led expansions”, BIS Quarterly Review, Bank for International Settlements, March 2017.

- See “Recent trends in consumer credit in the euro area”, Economic Bulletin, Issue 7, ECB, Frankfurt am Main, 2017; and “Consumption of durable goods in the ongoing economic expansion”, Economic Bulletin, Issue 1, ECB, Frankfurt am Main, 2018.

- We focus on the expanded asset purchase programme (APP), which was started in January 2015 as a way to address the risks of a long period of low inflation. The APP is modelled as a 30 basis point decrease in the term spread, i.e. the difference between the long-term and short-term interest rates.

- The model includes house and stock prices and interest rates (which determine bond prices).

- See also Constâncio, V., “Inequality and macroeconomic policies”, speech delivered at the Annual Congress of the European Economic Association, Lisbon, 22 August 2017.

- The bulk of the changes in income are driven by individuals becoming employed, the probability of which is in turn dependent on their demographics (such as age, education, marital status and the number of children they have). More specifically, we estimate a probit model with the employment status as the dependent variable, which captures some heterogeneity in the probability of employment across households. The model is then used to simulate which individuals become employed.

- Ampudia, M., Georgarakos, D., Slacalek, J., Tristani, O., Vermeulen, P and Violante, G.L., “Monetary policy and household inequality”, Working Paper Series, No 2170, ECB, Frankfurt am Main, July 2018.