ECB staff macroeconomic projections for the euro area, March 2023

Overview

The ECB staff macroeconomic projections were finalised in early March 2023 before the recent emergence of financial market tensions. These tensions imply additional uncertainty for the outlook for inflation and economic growth.

Euro area economic growth slowed markedly during the second half of 2022, eventually stalling in the fourth quarter.[1] However, with energy supplies becoming more secure, energy prices have eased significantly, confidence has improved and activity should pick-up somewhat in the short-term. Lower energy prices are now providing some cost relief, particularly for energy-intensive industries, and global supply bottlenecks have largely dispersed. The energy market is expected to continue rebalancing and real incomes are expected to improve. With foreign demand also strengthening, and provided current financial market tensions subside, output growth is expected to rebound as of mid-2023, underpinned by a robust labour market. Nevertheless, the ECB’s ongoing policy normalisation and further rate hikes expected by markets will increasingly feed through to the real economy, with additional dampening effects stemming from a recent tightening in credit supply conditions. This, together with the gradual withdrawal of fiscal support and some remaining concerns about risks to the energy supply next winter, will weigh on economic growth in the medium term. Overall, annual average real GDP growth is expected to slow to 1.0% in 2023 (from 3.6% in 2022), before rebounding to 1.6% in 2024 and 2025. Compared with the December 2022 Eurosystem staff macroeconomic projections, the outlook for GDP growth has been revised up by 0.5 percentage points for 2023 owing to a carry-over from the positive surprises in the second half of 2022 and an improved short-term outlook. For 2024 and 2025, it has been revised down by 0.3 percentage points and 0.2 percentage points respectively, as the tightening of financing conditions and the recent appreciation of the euro outweigh the positive income and confidence effects of lower inflation.

The sharp adjustment in energy markets has led to a significant decline in price pressures, and inflation is now expected to fall at a faster pace. Energy inflation, which peaked above 40% last autumn, should turn negative in the second half of 2023 on the back of commodity prices, which have fallen below levels last seen before Russia’s invasion of Ukraine, strong base effects and the stronger euro exchange rate. The more benign energy commodity price outlook implies fiscal measures should play a somewhat lesser role in lowering energy prices in 2023 and, with the withdrawal of the measures, a smaller rebound is now expected in energy inflation in 2024. Inflation rates for other components of the Harmonised Index of Consumer Prices (HICP) are expected to start unwinding slightly later, as pipeline pressures related to cost pass-through, especially for food inflation, as well as lingering effects from past supply bottlenecks and the reopening of the economy, will still be present in the near term. Headline inflation is expected to fall below 3.0% by the end of 2023 and to stabilise at 2.9% in 2024, before moderating further to the inflation target of 2.0% in the third quarter of 2025 while averaging 2.1% for the year. In contrast to headline inflation, core inflation as measured by HICP inflation excluding energy and food will, on average, be higher in 2023 than in 2022, reflecting lagged effects related to indirect effects both from past high energy prices and from the past strong depreciation of the euro, which will dominate in the short term. The effects on core inflation from the more recent energy price declines and the euro’s recent appreciation will be felt only later in the projection horizon. The expected decline in inflation in the medium term also reflects the gradual impact of monetary policy normalisation. Nevertheless, tight labour markets and inflation compensation effects imply that wages are expected to grow at rates well above historical averages and, by the end of the horizon, stand in real terms at levels close to those of the first quarter of 2022. Compared with the December 2022 projections, headline inflation has been revised down across the projection horizon (by 1.0 percentage point for 2023, by 0.5 percentage points for 2024 and by 0.2 percentage points for 2025). The sizeable downward revision for 2023 is driven by large downward surprises related to energy inflation in recent months and much lower energy price assumptions, partially offset by upward data surprises for HICP inflation excluding energy and food. For 2024 and 2025, the downward revisions relate to a lower impact on energy inflation from the reversal of fiscal measures, more strongly fading indirect effects and an increasing pass-through of the euro’s recent appreciation.

Table

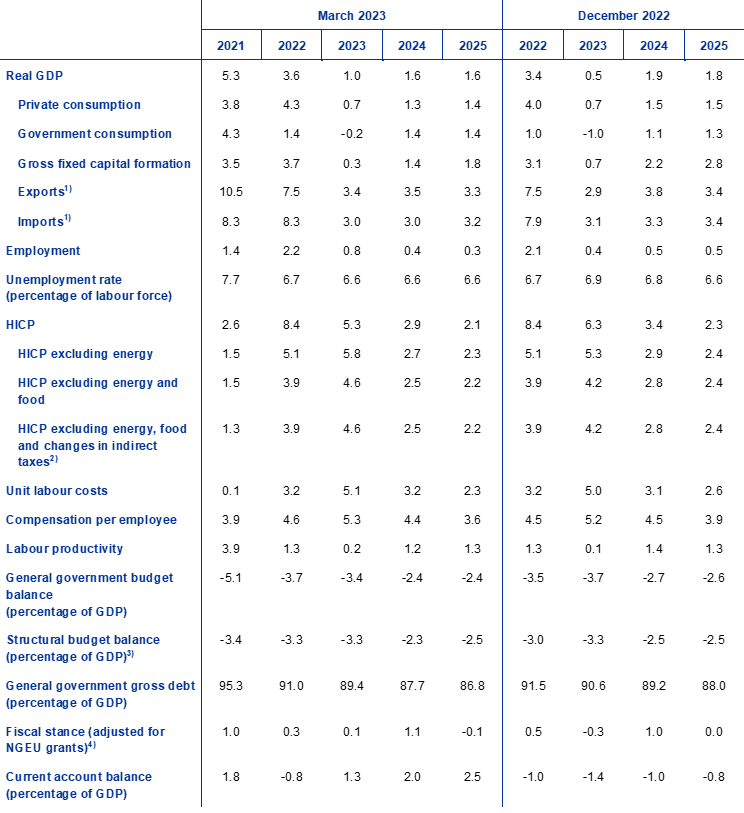

Growth and inflation projections for the euro area

(annual percentage changes)

Notes: Real GDP figures refer to seasonally and working day-adjusted data. Historical data may differ from the latest Eurostat publications owing to data releases after the cut-off date for the projections.

The uncertainty surrounding the staff projections is high, as the projections were finalised before the recent financial market tensions and risks relating to a further worsening of broader credit conditions and to a deterioration of confidence have increased. Other risk factors relate to the macroeconomic impact of monetary and fiscal policy in the euro area, higher second-round effects on wages and inflation, global monetary policy and energy commodity prices, which may, in turn, result from the reopening of the Chinese economy and potential gas shortages in Europe next winter. Reflecting the high uncertainty surrounding the outlook, the projections for growth and inflation are presented together with symmetric uncertainty bands (Charts 1 and 4), which are explained in Box 6. In addition, the report contains a scenario assessing the implications of a potentially stronger rebound in the Chinese economy (see Box 3) and a range of sensitivity analyses related to alternative paths for energy commodity prices (see Box 4).

1 Real economy

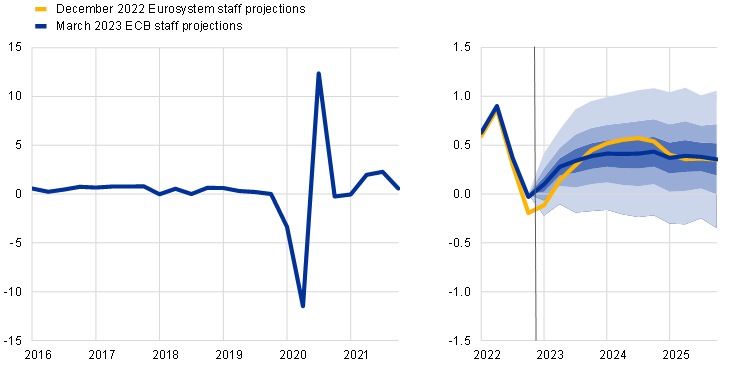

Growth in the euro area stagnated in the fourth quarter of 2022, with consumption dropping owing to high uncertainty, high energy prices and low confidence. However, growth still surprised on the upside on account of declining imports (Chart 1). Growth was 0.2 percentage points stronger than expected in the December 2022 projections, driven by a more positive net trade contribution – partly reflecting the mild weather and lower demand for energy imports – and a faster unwinding of supply chain disruptions. Industrial production declined at the end of the year, driven primarily by energy-sensitive industries, despite existing order backlogs and the easing of supply bottlenecks. Survey indicators suggest that the weakening of growth in the fourth quarter was broad-based across sectors.

Chart 1

(quarter-on-quarter percentage changes, seasonally and working day-adjusted quarterly data)

Notes: Historical data may differ from the latest Eurostat publications owing to data releases after the cut-off date for the projections (see footnote 1). The vertical line indicates the start of the current projection horizon. The ranges shown around the central projections provide a measure of the degree of uncertainty and are symmetric by construction. They are based on past projection errors, after adjustment for outliers (see Box 6). The bands, from darkest to lightest, depict the 30%, 60% and 90% probabilities that the outcome of real GDP growth will fall within the respective intervals.

GDP growth is projected to be marginally positive in the first quarter of 2023 and to strengthen in the second quarter of 2023 as supply bottlenecks are resolved, inflation moderates further and energy supply-related uncertainty dissipates. Although the positive surprise in the fourth quarter of 2022 reflected largely weaker imports and, as such, did not necessarily suggest stronger underlying growth momentum, the improved outlook as regards energy supply and prices contributed to a decline in uncertainty towards the end of the quarter. Consistent with this, business and consumer confidence and expectations have improved recently. The composite Purchasing Managers’ Index (PMI) for output rose in February to a nine-month high of 52.3 and is in positive territory for both manufacturing and services. However, the adverse inflationary impact on real disposable income is expected to impede notable growth in household spending at the start of the year, despite still strong fiscal support. Less than half of the large stock of excess savings built up during the pandemic is liquid.[2] Moreover, it is primarily concentrated among the wealthiest households, which limits its role in cushioning the impact of the adverse shocks to real income.[3] Overall, real GDP is expected to increase by 0.1% in the first quarter of 2023 and by 0.3% in the second quarter (revised up by 0.2 percentage points in both quarters from the December 2022 projections).

From the second half of 2023 onwards, GDP growth is projected to increase as real incomes rise and foreign demand strengthens, albeit tempered by tightening financing conditions and provided current financial market tensions subside. Growth is set to strengthen throughout 2023 and to stabilise in 2024-25, slightly above the pre-pandemic historical average. This reflects the resolution of supply bottlenecks, but also an unwinding of the supply shocks, improving confidence and the fading of uncertainty around the turn of the year 2022/23 related to future energy bills. Growth is expected to be also supported by easing inflationary pressures, allowing a recovery in real disposable income and consumption. Furthermore, foreign demand will strengthen, against a background of global energy prices that are much lower than previously projected. However, the impetus from these tailwinds will be dampened by tightening financing conditions – with higher interest rates also incentivising household savings – and the appreciation of the euro, the gradual withdrawal of fiscal support and still lingering concerns about the smooth rebalancing of the energy market in the medium term.

Tighter financing conditions are expected to have a negative impact on growth, while discretionary fiscal policy measures are estimated to have a broadly neutral impact on growth in 2023 and a mildly contractionary impact thereafter. Past changes in interest rates and market-based expectations at the cut-off date of the projections (as reflected in the technical assumptions for the staff projections, see Box 1) will have a negative impact on GDP growth, particularly in 2023 and 2024. In addition, in the ECB’s latest euro area bank lending survey, banks reported a substantial further tightening of credit standards and credit terms and conditions for loans to firms in the fourth quarter of 2022. This was the largest tightening reported since the euro area sovereign debt crisis. Banks expected a net tightening of a similar magnitude also for the first quarter of 2023. Additionally, they reported a continued tightening of credit standards for loans to households. Although a restraint in bank credit is expected to weigh especially on residential and business investment, the impact will to some extent be mitigated by the fact that the balance sheets of both households and firms are currently in a much more favourable position than in the past. The fiscal measures taken by euro area governments to compensate for high energy prices and inflation have broadly offset the negative impact of the withdrawal of previous coronavirus (COVID-19) pandemic and recovery-related measures in 2023. As many energy-related measures are expected to be withdrawn thereafter, the fiscal measures are likely to make a negative contribution of around 0.3-0.4 percentage points to growth in 2024-25 (see Section 2).

Table 1

Macroeconomic projections for the euro area

(annual percentage changes, unless otherwise indicated)

Notes: Real GDP and components, unit labour costs, compensation per employee and labour productivity refer to seasonally and working day-adjusted data. Historical data may differ from the latest Eurostat publications owing to data releases after the cut-off date for the projections.

1) This includes intra-euro area trade.

2) The sub-index is based on estimates of actual impacts of indirect taxes. This may differ from Eurostat data, which assume a full and immediate pass-through of indirect tax impacts to the HICP.

3) Calculated as the government balance net of transitory effects of the economic cycle and measures classified under the European System of Central Banks definition as temporary.

4) The fiscal policy stance is measured as the change in the cyclically adjusted primary balance net of government support to the financial sector. The figures shown are also adjusted for expected grants under the Next Generation EU (NGEU) programme on the revenue side. A negative figure implies a loosening of the fiscal stance. The fiscal stance, as well as the general government budget balance and the structural budget balance, has been adjusted for the fiscal projection period (2022-25) for the estimated impact of a statistical reclassification in Italy. For past data, affecting in part also the fiscal stance for 2022, this adjustment will be available in the context of Eurostat’s forthcoming April 2023 excessive deficit procedure notifications and the June 2023 Eurosystem projections.

Turning to the components of GDP, household real consumption is expected to recover gradually over the projection horizon as the inflation-induced drop in real income and high uncertainty related to energy supply fade. The contraction in the last quarter of 2022 was driven mostly by a decline in the consumption of non-durable and semi-durable goods (which include energy and food), while spending on durables continued to improve, reflecting an easing of supply constraints in the automotive sector and some government incentives for the purchase of electric vehicles. Private consumption is expected to grow modestly in 2023, in line with the drop in inflation and uncertainty related to energy security and pricing, and the recovery in confidence, also supported by fiscal measures. Beyond the short term, as inflation and energy supply-related uncertainty decline further and real incomes improve, consumption will continue to recover, growing slightly more strongly than real disposable income. Private consumption is unrevised for 2023 from the December 2022 projections, while it has been revised slightly down for the medium term owing to the impact of tighter credit standards and higher interest rates.

Real disposable income is projected to stagnate in 2023, largely on the back of high inflation, but to recover in the outer years of the projection horizon, supported by resilient labour markets and strong growth in nominal wages. Real disposable income is estimated to have declined slightly in 2022 owing to high inflation and a negative contribution from overall net fiscal transfers to households. This reflects the withdrawal of pandemic support measures, despite resilient labour markets and additional fiscal measures related to high energy prices. Real disposal income is expected to stagnate in 2023 against a background of continued high – albeit declining – inflation, reflecting also a lower contribution from employment and non-labour income that more than offsets stronger wage growth, in a context of overall neutral fiscal support. As inflation is expected to decline further and the economic recovery to strengthen, real disposable income is expected to grow again in 2024 and 2025 to well above its pre-pandemic level.

The household saving ratio is expected to decline to close to its pre-pandemic level in 2023 and to broadly stabilise thereafter, providing only little additional support for private consumption. The saving ratio fell in 2022, as consumers’ behaviour largely normalised with the relaxation of pandemic-related restrictions. It is likely to have increased marginally in the last quarter of 2022 owing to the high uncertainty, despite the need to buffer consumption in view of deteriorating purchasing power. The saving ratio is projected to decline in 2023, helping to smooth consumption to some extent, as real disposable income stagnates. It should then broadly stabilise in 2024-25, close to its pre-pandemic level. This stability reflects the fact that downward pressures from diminishing energy-related uncertainty and lower inflation, which should bolster real income, are roughly offset by upward pressures from interest rate increases. Furthermore, the large stock of excess savings accumulated during the pandemic is not expected to provide much support for consumption, although there is still some decumulation of the excess savings acquired during the pandemic.

Box 1

Technical assumptions about interest rates, commodity prices and exchange rates

Compared with the December 2022 projections, the technical assumptions include tighter financing conditions, lower oil prices, significantly lower wholesale gas and electricity prices and an appreciation of the euro. The technical assumptions about interest rates and commodity prices are based on market expectations, with a cut-off date of 15 February 2023. Short-term interest rates refer to the three-month EURIBOR and market expectations are derived from futures rates, while ten-year government bond yields are used to proxy long-term interest rates.[4] Both short and long-term rates have risen since the cut-off date for the December 2022 projections and, relative to those projections, their paths have been revised up by 40-50 basis points on the back of further rises in ECB key policy rates and spillovers from monetary policies in other jurisdictions.

Table

Technical assumptions

Despite the reopening of the Chinese economy, the technical assumptions for oil prices have been revised down slightly owing to weaker demand and limited effects from new sanctions imposed on Russia.[5] The global economic slowdown has continued to weigh on oil prices through lower oil demand, while the reopening of the Chinese economy has led to an increase in expected oil demand from the second quarter of 2023. The International Energy Agency expects China’s oil demand to increase by 0.9 million barrels per day in 2023 (around 0.9% of global supply) amid weaker demand in the first quarter, following a surge in COVID-19 cases in the immediate aftermath of the economy reopening. Concerns about oil supply also weighed on oil prices, although markets took some comfort from the fact that the EU embargo and the G7 price cap on Russian crude oil have only had limited effects on the global oil market so far. At the same time, higher production in Kazakhstan and Nigeria has also supported the global oil supply since the December 2022 projections. The oil futures curve has shifted downwards since the December 2022 projections (by 4.3% for 2023, 2.3% for 2024 and 2.7% for 2025) and remains in backwardation. The oil price is assumed to stand at USD 83 per barrel in 2023 and to decline to USD 74 per barrel in 2025.

Wholesale gas and electricity prices have continued their sharp falls to below the levels prevailing before the war in Ukraine, while the assumed path for prices of carbon emissions allowances on the EU Emissions Trading System (ETS) has increased. Historically high gas storage levels have alleviated concerns about gas supply security in Europe this winter. Successful substitution of Russian gas supplies with liquified natural gas (LNG) helped Europe fill storage facilities ahead of the winter. Levels have remained high since then, owing to low demand during a very mild winter and effective EU gas-saving measures. Robust gas reserves have also left the EU in a better position to secure gas supplies ahead of the 2023-24 winter. The new assumptions entail a sharp downward revision to the assumptions for gas prices embedded in the technical assumptions of the December 2022 projections: 52.7% for 2023, 37.6% for 2024 and 26.2% for 2025. Wholesale electricity futures prices have also been revised down substantially, mirroring the change in gas price assumptions. As regards EU carbon allowances on the ETS, the assumed path based on futures contracts has been revised significantly upwards since the December projections (by 18%). The revision reflects, among other factors, a more resilient business cycle than previously anticipated by markets. Heightened volatility in ETS prices also reflects uncertainty related to the war in Ukraine, as well as the pricing implications of the EU finance ministers’ proposal to frontload the sale of emission certificates starting this spring.

Bilateral exchange rates are assumed to remain unchanged over the projection horizon, at the average levels prevailing in the ten working days ending on the cut-off date. This implies an average exchange rate of USD 1.08 per euro in 2023-25, which is 4.7% higher than in the December 2022 projections. The assumption for the effective exchange rate of the euro implies an appreciation of around 2% over the December projections.

Housing investment is projected to decline substantially further in the short term and to remain weak over the projection horizon, as financing conditions tighten and real disposable income stagnates. Rising mortgage rates and a sharp tightening in credit standards, reduced household purchasing power and persistently high construction costs will continue to weigh heavily on housing investment in the short term. This will lead to a continuation of the protracted decline in housing investment, which started in the second quarter of 2022 and is expected to bottom out only towards the end of 2024. This is broadly consistent with the latest PMI data on business expectations in the construction sector for the next twelve months, which recovered somewhat in January but remained well below the expansion threshold. Housing investment growth should turn positive again in 2025, supported by rising real disposable income and less adverse Tobin’s Q effects.[6] However, as mortgage rates are projected to stay high, housing investment growth will remain weak.

Business investment is expected to be weak in 2023 but to recover in 2024-25, albeit at a subdued pace in view of tightening financing conditions. Business investment contracted in the fourth quarter of 2022, affected in large part by an expected base effect related to a considerable rise in investment in intellectual property products (IPP) in Ireland in the previous quarter. Even excluding Ireland, euro area business investment is still likely to have fallen in the fourth quarter, reflecting ongoing uncertainty, weak demand, heightened concerns regarding energy prices and supply, as well as sharply higher interest rates and rising financing constraints. Business investment is expected to remain weak overall in 2023 but to recover somewhat over the course of the year. Incoming data for the capital goods sector in the first quarter suggest the steep decline in new orders seen at the end of 2022 has started to reverse and sector output looks to be growing again. Ongoing replacement and rationalisation, as well as broader efforts for increased digitalisation and the greening of production processes, have been reported by corporate contacts to be important drivers of investment plans in 2023, buoyed by NGEU funds. Overall, growth in total gross fixed capital formation has been revised down throughout the horizon compared with the December 2022 projections, as the impact of higher financing costs and tighter credit supply weigh increasingly on investment dynamics.

Box 2

The international environment

Global economic activity is expected to stay subdued in the first few months of 2023 and, while the reopening in China is expected to provide support to the global economy later this year, global growth is seen as remaining relatively contained over the whole projection horizon. Incoming survey data continue to suggest that a broad-based slowdown is under way. Global manufacturing output remained in contractionary territory in January. Moreover, while the reported pace of the contraction has slowed slightly compared with December, manufacturing output remains weak by historical standards and across major economies, dampened by high inflation, monetary policy tightening and elevated geopolitical uncertainty. World real GDP growth (excluding the euro area) is projected to decline to 3.0% this year, from an estimated 3.3% in 2022. For 2024 and 2025 a gradual increase in growth is expected, with rates of 3.2% and 3.3% respectively, as inflation declines and the reopening of China underpins growth. Compared with the December 2022 projections, world real GDP growth has been revised up by 0.4 percentage points for 2023 and 0.1 percentage points for 2024 but remains unchanged for 2025. A key factor behind these revisions is the improved outlook for China, as pandemic-related disruptions at the turn of the year are projected to give way to a faster recovery later on, when the economy is less constrained by the risk of renewed lockdowns. Despite these revisions, the outlook for China is subject to upside risks, with possible spillovers to global commodity prices and euro area foreign demand (see Box 3). Stronger growth in the United States – however also subject to heightened uncertainty – and a smaller decline in growth in Russia are seen as providing some additional support to the global economy this year. As regards Russia, the less negative outlook for growth largely reflects the carry-over effects of stronger than expected data outturns. The impact of the sanctions enacted late last year and of those to be implemented in the course of the first quarter of 2023 is assessed by ECB staff to remain sizeable, albeit somewhat smaller than the impact included in the December projections.

Global trade growth is projected to decline more sharply this year than world real GDP growth, but over the medium term both should grow at a similar pace. Global trade (excluding the euro area) is projected to grow at a relatively subdued pace in 2023, compared with its long-term average, marking a sharp deceleration from 2022. This reflects the fact that the unwinding of supply bottlenecks, which temporarily boosted trade growth in the second half of 2022, is expected to have a limited impact in the period ahead. Global trade growth should strengthen in 2024 and stabilise in 2025. Euro area foreign demand should follow a similar path, with the pace of growth declining to 2.1% this year (from 6.3% in 2022), before gradually picking up to 3.1% in 2024 and 3.3% in 2025. Projections for both global trade and euro area foreign demand have been revised upwards for 2023, but these revisions largely reflect stronger than previously estimated outturns in late 2022, leading to sizeable carry-over effects.

Table

The international environment

(annual percentage changes)

1) Calculated as a weighted average of imports.

2) Calculated as a weighted average of imports of euro area trading partners.

3) Calculated as a weighted average of the export deflators of euro area trading partners.

Price pressures in the global economy remain high, but sharp disinflation is projected in the export prices of euro area competitors. Global consumer price inflation averaged 8.0% last year and seems to have peaked at 8.8% in the third quarter of 2022. Gradual disinflation has emerged in monthly figures since then, supported by waning supply disruptions, falling energy prices and synchronised monetary policy tightening across the globe. However, resilient labour markets and strong wage growth, especially in key advanced economies outside the euro area, suggest that underlying inflation pressures in the global economy remain strong and the process of disinflation will be gradual. At the same time, export prices of euro area competitors (in national currencies) have been falling rapidly since peaking in the second quarter of 2022, on account of negative base effects for commodity prices, reflecting technical assumptions underlying the March 2023 ECB staff macroeconomic projections. While the contributions from domestic and foreign pipeline pressures remain significant, their inflationary impact is expected to dissipate in 2024.

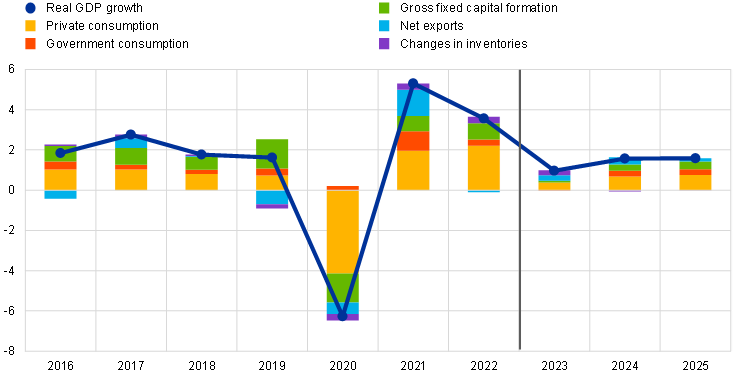

Euro area export growth is expected to recover as supply bottlenecks ease and foreign demand strengthens, supporting positive net trade contributions to GDP in 2023-25, while lower energy prices imply an improvement in the euro area terms of trade and the current account. In the last quarter of 2022, euro area real exports are estimated to have fallen marginally, despite a much more substantial contraction in foreign demand. At the same time, import volumes are estimated to have declined strongly, partly driven by a correction in energy imports as gas storage facilities were filled and by a strong import contraction in Ireland related to the volatility in IPP activities. This resulted in a positive contribution of net trade to real GDP growth. Export growth is expected to be supported in the short term by the earlier than expected easing of supply bottlenecks. The reopening of China should also boost demand for euro area consumer goods and exports of travel services. These should offset the dampening effect of competitiveness losses arising from the euro’s recent appreciation and both the energy price shock and the costs incurred due to the transition away from Russian gas to more expensive but reliable alternatives, at least in the short term. Net exports are expected to have a positive contribution to GDP growth also in 2024 and 2025, while moderating towards the end of the horizon (Chart 2). On the prices side, the substantially lower energy commodity price assumptions imply lower energy import prices from the end of 2022, bringing improvements in the euro area terms of trade and the current account[7], which stays positive until the end of the projection horizon and has been revised up strongly since the December projections. The revision in the current account projections reflects, on the one hand, data for the last quarter of 2022 showing a sharp improvement in the current account and, on the other hand, downward revisions in import prices and volumes over the projection horizon.

Chart 2

Euro area real GDP – decomposition into the main expenditure components

(annual percentage changes, percentage point contributions)

Notes: Data are seasonally and working day-adjusted. Historical data may differ from the latest Eurostat publications owing to data releases after the cut-off date for the projections. The vertical line indicates the start of the projection horizon.

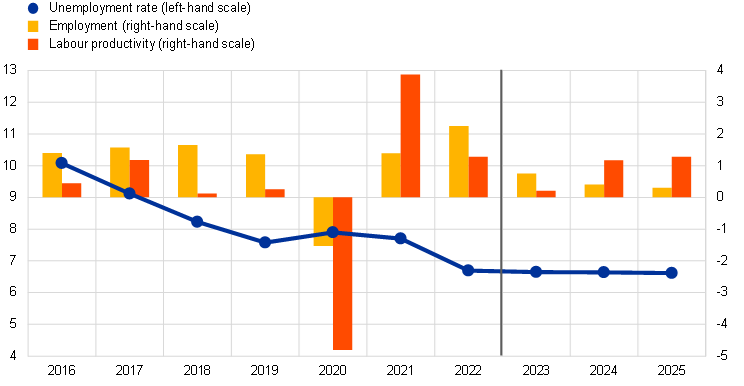

The labour market is projected to remain resilient, with unemployment remaining historically low over the projection horizon amid ongoing labour supply shortages (Chart 3). Employment grew by 0.3% in the fourth quarter of 2022, notwithstanding stagnant real GDP growth. It is projected to continue to increase over the projection horizon, albeit at a slower pace than in 2022 (0.8% in 2023, 0.4% in 2024 and 0.3% in 2025). The increase in employment follows a decline in the risk of an economic recession in the near term, with the slowdown in real activity in 2023 not resulting in an increase in layoffs. Instead it translates into an increase in labour hoarding in an environment of ongoing labour supply shortages. As a result, productivity growth is expected to decline to 0.2% in 2023, before recovering to 1.2% in 2024 and 1.3% in 2025. Against the background of an ongoing expected slight increase in the labour force, the unemployment rate is projected to remain around current levels of 6.6% throughout the projection horizon.

Chart 3

Euro area labour market

(percentage of labour force, annual percentage changes)

Note: The vertical line indicates the start of the projection horizon.

Compared with the December 2022 projections, real GDP growth has been revised up by 0.5 percentage points for 2023 and down by 0.3 percentage points for 2024 and 0.2 percentage points for 2025. The upward revision for 2023 reflects a positive carry-over effect from the surprise in the second half of 2022 – largely on account of the lower demand for energy imports – and upward revisions to the short-term outlook. The latter are driven by the faster than expected adjustment of the energy market and significant moderation in energy inflation, the related drop in uncertainty and improving confidence, as well as the fast unwinding of supply chain disruptions. Beyond the short term, GDP growth has been revised down in 2024-25 on account of stronger monetary policy tightening effects leading to an upward revision in interest rates, the recent sharp tightening in credit supply conditions and the appreciation of the euro outweighing the positive income and confidence effects of lower inflation.

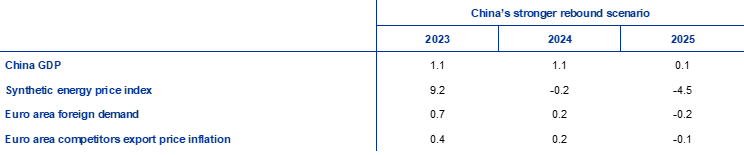

Box 3

Spillovers to the euro area in a scenario of a stronger rebound in China’s economy

This scenario considers a stronger rebound in the Chinese economy compared with the path included in the baseline projections, triggering also a rise in international commodity prices. The scenario assumes a stable pandemic situation in China, with no further large waves of coronavirus infection and ensuing strict containment measures. This situation would be conducive to a quicker rebound in consumer confidence and a stronger recovery in demand, with positive effects also on the residential real estate sector. The scenario assumes that the pace of economic activity picks up markedly, particularly from the second quarter of 2023, as the negative impact from the large wave of infections at the turn of the year dissipates faster than in the baseline. This is expected to restore China’s real GDP to its pre-pandemic trajectory, bolstering also euro area foreign demand.[8] This scenario also envisages upward impacts on international commodity prices, especially gas prices, caused by a stronger rebound in Chinese demand, which is likely to translate into higher export price inflation for euro area competitors. However, these effects are assumed to reverse in 2025 (Table).[9]

Table

Scenario assumptions

(deviations from annual percentage changes in the March 2023 baseline projections, in percentage points)

Notes: The assumptions for the euro area variables are obtained based on a positive demand shock in China using the ECB-Global model. The synthetic energy price index is an average of developments in crude oil and wholesale gas prices using import weights.

The scenario of a stronger rebound in China implies limited effects on euro area growth and inflation. In the scenario, euro area real GDP would increase by an additional 0.1 percentage point in 2023 compared with the March 2023 baseline, mostly owing to higher world (euro area foreign) demand (Chart, panel a).[10] The shock would also entail stronger Chinese demand for commodities, which – taken in isolation – does not pose risks for euro area gas storage levels but would put additional pressures on commodity prices. This would in turn raise euro area inflation by 0.2 percentage points in 2023 and 2024 (Chart, panel b). The impact would fade away by the end of the projection horizon as the demand-supply balance in the commodity market is re-established.

Chart

Impact on euro area real GDP growth and HICP inflation in a scenario of a stronger rebound in China than embedded in the March 2023 baseline projections

(deviations from the March 2023 baseline projections, in percentage points)

Sources: Simulations using ECB-BASE and ECB staff calculations.

Notes: The simulations are conducted under a forecast setting with backward-looking expectation formation and with exogenous monetary and fiscal policy.

The estimated spillovers from China’s reopening to the euro area outlook are surrounded by some uncertainty. Any stronger growth in China from its reopening would likely be led by consumption, with a lower import intensity than that of the investment-related sector, implying that trade spillovers could be lower. This is particularly relevant for the euro area, as its exports to China mostly relate to investment products, whereas consumer products – including travel-related products – represent less than a quarter of its exports to China and only 0.45% of euro area GDP. Input-output analysis confirms that a consumption-led economic rebound in China would generate smaller spillovers for the euro area than an investment-led upturn, as the value added absorbed by Chinese final consumption is about 20% smaller than the value added absorbed by Chinese investment demand. Hence, effects may be milder than in the model simulations presented above. Furthermore, lingering weakness in the residential real estate sector and pandemic-related scarring effects might have also had an impact on potential growth, making a return of the Chinese economy to its pre-pandemic trend less likely. In addition, a stronger rebound in China could be accompanied by some positive global supply effects, thus supporting disinflation in traded goods. On the other hand, the euro area export channel might prove stronger on account of large and increasing euro area export market shares in consumer goods in China.

2 Fiscal outlook

The changes in discretionary fiscal policy measures have been relatively limited at the euro area level since the December 2022 projections.[11] In the absence of major budget news, revisions in fiscal assumptions are mostly related to the downward rescaling of fiscal support measures in response to the energy crisis and high inflation to about 1.8% of GDP, from more than 1.9% of GDP in the December projections. The rather limited revision at the euro area level is, however, the result of considerable country heterogeneity. On the one hand, the substantial fall in wholesale energy prices entails lower fiscal costs of certain measures, in particular the gas and electricity price caps enacted in several countries, depending on the country-specific design of these measures and the characteristics of their energy markets. On the other hand, a large share of the fiscal support (almost 60%) – primarily those measures offering direct income relief or enacted VAT rate cuts – does not depend directly on energy prices. Moreover, for several countries, the fiscal support has been revised up since the December projections, following the extension of measures into 2023 or updated estimates based on final budget laws. Other revisions are related to lower financing of the energy support, such as revenues from windfall taxes on energy sector profits. Reflecting these revisions and a statistical reclassification of fiscal data in Italy, the euro area fiscal stance adjusted for NGEU grants is projected to be broadly balanced in 2023, to tighten considerably in 2024 – as about 70% of the energy and inflation support from 2023 is assumed to be withdrawn – and to remain broadly balanced in 2025. Substantial fiscal support nonetheless remains in the March 2023 baseline projection, reflecting the strong fiscal expansion during the pandemic crisis, with significant uncertainty around the size of energy support in view of the recent decline in energy prices.

The euro area fiscal outlook is set to improve over the projection horizon. After the significant decline estimated for 2022, the euro area budget deficit is projected to continue to decline somewhat in 2023 and more significantly in 2024 (to 2.4% of GDP), remaining unchanged in 2025.[12] The decline in the budget balance at the end of the projection horizon, compared with 2022, is explained by the improvement in the cyclically adjusted primary balance, followed by a better cyclical component, while interest payments gradually increase as a share of GDP over the projection horizon. Euro area debt is projected to continue to decline, albeit more slowly after 2022, to slightly below 87% of GDP by 2025. This is mainly on account of negative interest rate-growth differentials, which more than offset the persisting primary deficits. Nevertheless, in 2025, both the deficit and the debt ratios are expected to remain above pre-pandemic levels. Compared with the December projections, the budget balance path has been revised up over 2023-25, albeit only marginally at the end of the projection horizon, while interest payments have increased over 2024-25. The debt ratio has been revised down, reflecting mainly the improvement in the primary balance path.

3 Prices and costs

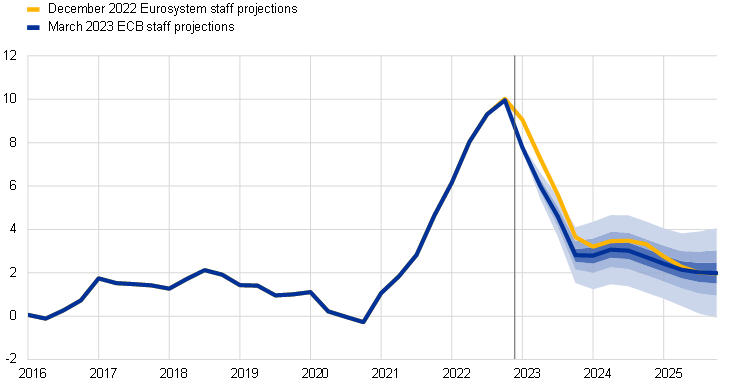

HICP inflation is projected to average 5.3% in 2023, before decreasing to 2.9% in 2024 and 2.1% in 2025. The baseline projection sees headline inflation declining from 10.0% in the fourth quarter of 2022 to 2.8% in the fourth quarter of 2023, then hovering around 3.0% in 2024, before falling to the ECB’s inflation target of 2.0% only in the third quarter of 2025 (Chart 4). This decline in headline inflation over the projection horizon reflects declines in the annual rates of change of all main components to varying degrees and is affected by fiscal policy measures and commodity price assumptions (Chart 5).

Chart 4

Euro area HICP inflation

(annual percentage changes)

Notes: The vertical line indicates the start of the current projection horizon. The ranges shown around the central projections are based on past projection errors, after adjustment for outliers (see Box 6). The bands, from darkest to lightest, depict the 30%, 60% and 90% probabilities that the outcome of HICP inflation will fall within the respective intervals.

Headline inflation is expected to fall significantly in the course of 2023 while remaining at elevated levels, driven by downward energy-related base effects, declines in energy prices and easing pipeline pressures. HICP energy inflation should contribute significantly to this decline, owing predominantly to large downward base effects from the strong rise in energy commodity prices in 2022 and to a gradual pass-through of the much lower oil, gas and electricity price assumptions. Accordingly, the decline in HICP energy inflation over the projection horizon reflects decreases in all its main components (transport fuel, gas and electricity prices). Food inflation is also expected to decline noticeably on account of easing pipeline pressures. Inflation dynamics in the unprocessed food component have been weakening since last autumn as upward price pressures from the drought in Europe last summer fade. At the same time, price pressures from the processed food component have continued to be significant, putting further upward pressure on food inflation in the short term. Still, over the course of 2023, gradually easing pipeline price pressures for consumer food prices resulting from decreasing farm gate price assumptions, lower energy and other input prices, together with downward base effects, should lead to declines in food inflation. HICP inflation excluding energy and food is projected to moderate gradually in the course of 2023, as easing pipeline pressures are envisaged to outweigh upward pressures from strengthening wage growth. In particular, upward pipeline pressures from the strong increases in input prices and the past depreciation of the euro are expected to diminish, reinforced by downward impacts from the euro’s more recent appreciation and lower indirect effects given the much lower energy price assumptions. Easing pressure from past supply bottlenecks and reopening effects should support the expected decline in HICP inflation excluding food and energy this year. Profit margins, which expanded in 2022, are also expected to start to moderate as competitive pressures start to take effect. The decline in HICP inflation excluding energy and food will initially be driven by non-energy industrial goods inflation while more robust wage growth will imply greater persistence in services inflation, which is expected to remain strong throughout 2023. Changes in HICP weights have had a downward impact on HICP inflation excluding energy and food in the first months of 2023 and are expected to have an upward impact in the third quarter, while they should have a negative impact on headline inflation for 2023 as a whole.

Following an uptick in 2024, related to the unwinding of fiscal measures, energy inflation is expected to pull headline inflation down in 2025. This pattern reflects the assumed downward-sloping profile for oil, gas and electricity prices. Following a negligible contribution to headline inflation, on average, in 2023, a rebound in 2024 is mainly due to the phasing out of many government measures to dampen gas and electricity inflation. Overall, the energy and inflation compensatory fiscal measures, which are expected to have a downward impact of 0.3 percentage points on HICP inflation in 2023, should have an upward impact of around 0.5 percentage points in 2024 and 0.2 percentage points in 2025 on their withdrawal.[13]

HICP food inflation is expected to decline in the outer years of the projection horizon in line with commodity price assumptions. The assumed decline in energy commodity prices plays an important role also in lower food price inflation, given the intensive use of energy in food production, especially of processed food products. Moreover, farm gate prices are assumed to decline slowly over the projection horizon.

Over the medium term, HICP inflation excluding energy and food is expected to moderate as pipeline price pressures gradually ease (compounded by recent falls in energy prices) and the tighter monetary policy is transmitted to the economy, while historically high wage growth will contribute to keeping core inflation elevated. The expected decline from 4.6% in 2023 to 2.2% in 2025 follows the unwinding of upward impacts from supply bottlenecks and the effects of the reopening of the economy, coupled with lagged effects from the slowdown in growth and an easing of indirect effects from the rise in energy prices. While the sharp downward corrections to wholesale energy prices imply lower indirect effects compared with previous projections, these prices remain elevated by historical standards and are only passing through gradually. The net effects are therefore still estimated to be positive but to diminish over the full projection horizon. Similarly, the upward pressure on core inflation from the lagged effects of the past depreciation of the euro is now less than previously assumed owing to the euro’s recent appreciation, which is partly related to the more restrictive monetary policy in the euro area. At the same time, persistently high wage growth will imply core inflation of 2.2% in 2025, considerably above its historical average.

Chart 5

Euro area HICP inflation – decomposition into the main components

(annual percentage changes, percentage points)

Note: The vertical line indicates the start of the current projection horizon.

Wages are projected to grow at elevated rates, reflecting tight labour markets, increases in minimum wages and inflation compensation, with real wages eventually returning to pre-pandemic levels. Wage growth is projected to average 5.3% in 2023, before declining to averages of 4.4% in 2024 and 3.6% in 2025. For 2023, the figure has been revised up slightly compared with the December projections, on account of a likelihood of stronger pressure to recoup purchasing power losses. However, for 2024 and 2025, the figures have been revised down, reflecting less of a need for inflation compensation. By the end of the horizon, real wages are expected to return to the levels seen in the first quarter of 2022. Growth in unit labour costs is expected to pick up further in 2023, amid rising wage and falling productivity growth, before starting to fall back as wage growth moderates and, in particular, as labour productivity growth picks up in line with the expected strengthening in economic activity.

Profit margins are expected to continue to expand in the short term, reflecting a high pass-through of cost pressures in a high inflation environment, before being squeezed in 2024 and recovering slightly in 2025. The rise in profit margins, which started in 2021, is expected to continue in the short term. This indicates a low absorption of the terms-of-trade pressures by profit margins and hence a high pass-through of these cost increases to selling prices. Moreover, some producers are also likely to continue to take advantage of the high inflation environment and the reduced competitive pressures that were associated with the global demand and supply imbalances. In 2024, profit margins are expected to decline somewhat, buffering the relatively strong labour cost growth. In 2025, profit margins are seen as again increasing somewhat as the decline in labour cost growth allows more room in pricing.

Following its surge in 2022, the annual growth rate of import prices is expected to moderate sharply in 2023, implying strongly reduced external price pressures over the full projection horizon. Having increased by nearly 18% in 2022, the import deflator is expected to drop sharply, in line with the assumed declines in oil, gas and other commodity prices, and vanishing supply bottlenecks for imported inputs. Over the medium term, this deflator is expected to develop broadly in line with its historical average of 1.1%.

Compared with the December 2022 projections, headline HICP inflation has been revised down for all years of the projection horizon (by 1.0 percentage point for 2023, by 0.5 percentage points for 2024 and by 0.2 percentage points for 2025). The large downward revision in 2023 is driven by large downward surprises for energy inflation and the much lower energy price assumptions, partially offset by upward data surprises for HICP inflation excluding energy and food. A lower impact from the reversal of fiscal measures on energy inflation, more strongly diminishing indirect effects and an increasing pass-through of the recent exchange rate appreciation explain the downward revisions for 2024 and 2025.

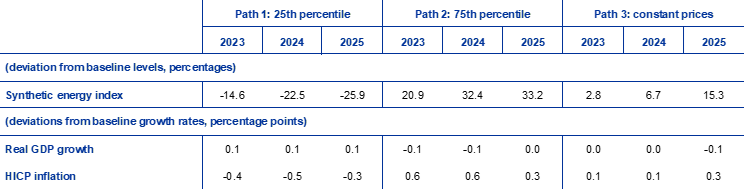

Box 4

Sensitivity analysis: alternative energy price paths

Given the significant uncertainty surrounding future energy price developments, various sensitivity analyses assess the mechanical implications for the baseline projections of alternative paths. This box first considers the risks to the short-term inflation outlook from possible exceptionally strong movements in energy commodity prices, drawing on the recent experience of high volatility in energy commodity prices. Thereafter, the impact of less extreme alternative paths for energy prices – drawing on market expectations or assuming no changes from current levels – on real GDP growth and HICP inflation throughout the entire projection horizon is assessed.

Alternative paths of oil and gas prices, based on recent experience, would imply the short-term outlook for HICP inflation could range from 5.3% to 7.0% in the second quarter of 2023. Strong short-term volatility, as observed over the past year, is usually not captured by the option-implied distribution around futures (which is discussed below). To assess such short-term sensitivity, one possibility is to consider upper and lower boundaries for short-term variations in oil and gas prices and then to derive forecasts for near-term inflation based on this range. In this sensitivity analysis, the range set for oil is from USD 55 to USD 125 per barrel and the range set for wholesale gas prices is from €20 to €150 per MWh. These prices, which are assumed to hold from March 2023 to June 2023, are fed into the set of energy equations (for fuels, electricity and gas) used by ECB staff for forecasting short-term inflation. The assumed maximum increases in oil and gas prices would lift headline HICP inflation by 0.1 percentage points in the first quarter of 2023 and by 1.0 percentage point in the second quarter of 2023, compared with the baseline projection. The assumed maximum decreases in oil and gas prices would reduce headline inflation by 0.2 percentage points in the first quarter of 2023 and by 0.7 percentage points in the second quarter of 2023.

Chart

Alternative paths of HICP inflation in the short term

(annual percentage changes)

Looking at the entire projection horizon, alternative paths for energy prices are derived from option-implied oil and gas prices and a constant price path. In this sensitivity analysis, a synthetic energy price index is used, which combines the oil and gas futures prices using import weights. Alternative downside and upside paths are derived from the 25th and 75th percentiles of the option-implied neutral densities for both oil and gas prices on 15 February 2023 (the cut-off date for the technical assumptions). Both distributions are skewed to the upside, suggesting some upside risks to the technical assumption of the March 2023 ECB staff projections. In addition, a constant price assumption is considered for both oil and gas prices.

The impacts of these alternative paths are assessed using a range of Eurosystem and ECB staff macroeconomic models, on the basis of a synthetic energy index. The average impacts on real GDP growth and inflation across these models are shown in the table below. The results for the 75th percentiles imply upward deviations from baseline HICP inflation projections of 0.6 percentage points in 2023-24, followed by 0.3 percentage points in 2025. The scenario based on the constant price path suggests smaller impacts in 2023-24 but a similar upward deviation for HICP inflation in 2025. By contrast, in the scenario based on the 25th percentile, the impacts on HICP inflation are -0.4, -0.5 and -0.3 percentage points for 2023, 2024 and 2025, respectively. Impacts on real GDP growth are -0.1 percentage points in both 2023 and 2024 for the 75th percentile, while the 25th percentile path would imply that GDP growth is 0.1 percentage points higher in each year of the projection horizon. The constant price path assumption would have a negligible impact on GDP across the projection horizon.

Table

Impacts of alternative energy price paths

Notes: In this sensitivity analysis, a synthetic energy price index that combines oil and gas futures prices is used. The 25th and 75th percentiles refer to the option-implied neutral densities for the oil and gas prices as at 15 February 2023. The constant oil and gas prices take the respective value as at the same date. The macroeconomic impacts are reported as averages of a number of ECB and Eurosystem staff macroeconomic models.

Box 5

Forecasts by other institutions

Forecasts for the euro area are available from both international organisations and private sector institutions. However, these forecasts are not directly comparable with one another or with the ECB staff macroeconomic projections, as these were finalised at different points in time. Additionally, these projections use different methods to derive assumptions for fiscal, financial and external variables, including oil, gas and other commodity prices. Finally, there are differences in working day adjustment methods across different forecasts.

Table

Comparison of recent forecasts for euro area real GDP growth and HICP inflation

(annual percentage changes)

Sources: Consensus Economics Forecasts, 16 February 2023 (data for 2025 taken from the January 2023 survey); European Commission Winter 2023 Economic Forecast (Interim), 13 February 2023; ECB Survey of Professional Forecasters, 3 February 2023; IMF World Economic Outlook Update, 30 January 2023; OECD November 2022 Economic Outlook 112, 22 November 2022.

Notes: The ECB staff macroeconomic projections report working day-adjusted annual growth rates, whereas the European Commission and the IMF report annual growth rates that are not adjusted for the number of working days per annum. Other forecasts do not specify whether they report working day-adjusted or non-working day-adjusted data. Historical data may differ from the latest Eurostat publications owing to data releases after the cut-off date for the projections.

The March 2023 ECB staff projection for GDP growth is above or at the upper end of the range of other forecasts for 2023-24 but within the range for 2025, while the projection for HICP inflation is below the range of other forecasts for 2023 but within the range thereafter. The ECB staff GDP growth projection is marginally above the range of other forecasts for 2023. For 2024, the ECB staff projection is in line with the IMF projection but somewhat above other forecasts, especially the Consensus Economics forecast, while for 2025 it is similar to other forecasts. As regards HICP inflation, the ECB staff projection is below all other forecasts for 2023, most likely as it takes account of the most recent declines in energy prices. For the remainder of the horizon, it is within the range of other forecasts.

Box 6

Illustrating the uncertainty surrounding the projections

As any forward-looking exercise, economic projections are intrinsically surrounded by uncertainty. Although not directly observable, uncertainty in projections basically reflects the degree of confidence that forecasters have about the projections point forecast and, more generally, the economic outlook. Uncertainty regarding Eurosystem/ECB staff projections might originate from different sources, such as conditioning assumptions, future shocks (e.g. size and nature) and the underlying forecasting models.

Up until the pandemic, uncertainty surrounding the Eurosystem/ECB staff projections was illustrated in public communication through symmetric ranges around the point forecast, derived from past projection errors. Since not all uncertainties are quantifiable or easily so, the ECB, like several peer institutions, relied on past projection errors as a catch-all proxy for uncertainty. This uncertainty was illustrated through ranges whose width was twice the mean absolute value of these projection errors, with outliers excluded from the error sample. In addition, the distribution of the projections was assumed to be perfectly symmetric, indicating thereby the level of uncertainty with no information on the balance of risks to the projections, the latter being communicated in the Monetary Policy Statement.

In the immediate aftermath of the pandemic, uncertainty was illustrated through alternative scenarios against the background of the exceptional size and nature of the shocks hitting the euro area economy. The pandemic triggered unprecedented measures by the public and private sectors to contain the spread of the virus. The sizeable economic effects of these measures and their unpredictability implied an unprecedented level of uncertainty for the projections that the standard computation of the ranges was not able to properly reflect. Moreover, the strength of the reopening of the global economy following the removal of pandemic-related restrictions and the Russian invasion of Ukraine were additional exceptional economic shocks that maintained the uncertainty to the economic outlook at unusually high levels. To better illustrate this level of uncertainty, alternative scenarios stemming from different assumptions about the future evolution of the pandemic and the associated containment measures, or the availability of natural gas in the euro area, were published. These scenarios, in retrospect, were effective in capturing the high level of uncertainty experienced.

The uncertainty surrounding the March 2023 projections is illustrated through symmetric fan charts, derived from past projection errors, and by construction does not reflect the increased uncertainty due to the recent financial market tensions (Charts 1 and 4). The methodology to derive the ranges used in these fan charts follows broadly the principles applied in the pre-pandemic period, which assumes a normal distribution of the past absolute projection errors, adjusted for outliers.[14] Outliers are removed to illustrate uncertainty in times not affected by exceptional developments. This may lead to an underrepresentation of current uncertainty related to the recent financial market tensions. Rather than being represented by a unique symmetric range as in the pre-pandemic period, uncertainty is now illustrated through three different – still symmetric – ranges. These reflect different prediction intervals (30%, 60% and 90%) to allow for a more nuanced representation of uncertainty. The intervals represent the probabilities that the future observation would fall within the respective range if the average shocks observed over the historical period, excluding exceptional events, were to materialise again.

© European Central Bank, 2023

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISBN 978-92-899-5724-3, ISSN 2529-4466, doi: 10.2866/007849, QB-CE-23-001-EN-N

HTML ISBN 978-92-899-5727-4, ISSN 2529-4466, doi: 10.2866/478445, QB-CE-23-001-EN-Q

The cut-off date for technical assumptions, such as those for oil prices and exchange rates, was 15 February 2023. The projections for the global economy were finalised on 16 February and the macroeconomic projections for the euro area were finalised on 1 March 2023. Historical data for the euro area also include Croatia for all variables except the Harmonised Index of Consumer Prices (HICP). The current projection exercise covers the period 2023-25. Projections over such a long horizon are subject to very high uncertainty, and this should be borne in mind when interpreting them. See the article entitled “The performance of the Eurosystem/ECB staff macroeconomic projections since the financial crisis”, Economic Bulletin, Issue 8, ECB, 2019. See also http://www.ecb.europa.eu/pub/projections/html/index.en.html for an accessible version of the data underlying selected tables and charts. A full database of past ECB and Eurosystem staff macroeconomic projections is available at https://sdw.ecb.europa.eu/browseSelection.do?node=5275746.

The liquid component of excess savings is calculated as the amount of accumulated bank deposits of households that exceeds the level observed in the fourth quarter of 2019, both scaled with disposable income.

For the concentration of savings, see M. Dossche, D. Georgarakos, A. Kolndrekaj and F. Tavares, “Household saving during the COVID-19 pandemic and implications for the recovery of consumption”, Economic Bulletin, Issue 5, ECB, 2022.

The assumption for euro area ten-year nominal government bond yields is based on the weighted country average of ten-year benchmark bond yields, weighted by annual GDP figures and extended by the forward path derived from the ECB’s euro area all-bonds ten-year par yield, with the initial discrepancy between the two series kept constant over the projection horizon. The spreads between country-specific government bond yields and the corresponding euro area average are assumed to be constant over the projection horizon.

The technical assumptions for commodity prices are based on the path implied by futures markets, taking the average of the two-week period ending on the cut-off date of 15 February 2023.

Tobin’s Q is the value of an existing house divided by its construction cost.

In accordance with the balance of payments definition.

The scenario is based on the assumption that the Chinese dynamic zero-COVID strategy was the primary factor limiting the economy’s ability to return to its pre-pandemic trajectory. Thus, removing this constraint allows consumption to fully recover. In addition, the scenario assumes that the property sector would benefit from higher consumer confidence and thus recover more strongly than expected. Improved sentiment could also support property prices, further reinforcing a positive feedback loop between consumption and housing, given the critical role that housing plays in Chinese households’ wealth.

Higher Chinese demand is mapped into higher oil and gas prices using assumptions for oil demand provided by the International Energy Agency (IEA) and scaled by the relative sizes of the GDP shock, as well as the elasticity between oil demand and oil prices taken from D. Caldara, M. Cavallo and M. Iacoviello, “Oil price elasticities and oil price fluctuations”, Journal of Monetary Economics, Vol. 103, 2019. For the gas market, ECB staff estimates are based on a Bayesian vector autoregressive model for the European gas market and IEA estimates of gas-to-oil switching in China. In addition, for gas prices the scenario assumes that Chinese LNG demand rebounds fully to 2021 levels with no gas-to-oil switching. The scenario also includes a higher sensitivity of European gas prices to supply shocks in a tight European gas market.

The model estimates the effect on the euro area aggregate without considering cross-country heterogeneity and resulting spillovers.

The fiscal projections incorporate only those discretionary measures that, at the time of the cut-off date, have already been approved by parliaments or that have been endorsed by governments and that are specified in detail and likely to pass the legislative process.

This is mainly due to a large reclassification in the Italian fiscal data, in the absence of which the euro area deficit would have temporarily increased in 2023. Over the current projection horizon, this reclassification implies an upward revision of the euro area fiscal deficit of about 0.3 percentage points of GDP in 2022 and an estimated downward revision of around 0.1 percentage points over 2023-25.

These impacts are relative to a counterfactual path of inflation without the fiscal measures. The impacts are heterogeneous across countries, reflecting the different measures taken in each country. For example, indirect tax measures reduce prices and inflation when introduced and increase them when phased out. When fiscal measures are used to cap prices, the size of the rebound in inflation depends on whether they are still binding, which in turn depends on developments in wholesale energy prices, as well as the extent and speed at which past price increases have been passed on to consumer prices. Other measures relate to transfers to households – such measures have a smaller and less direct impact on inflation by supporting demand.

The mean absolute errors are computed as the mean of the absolute differences between the projection for a given quarter and the realisation as available at the following quarter. The current sample for the projection errors covers the period from the fourth quarter of 1998 to the fourth quarter of 2022 and will be updated with each projection round. While all projected variables are surrounded by uncertainty, only ranges for real GDP growth and HICP inflation are illustrated.

-

16 March 2023