Commentary on “Fifty Years of Monetary Policy: What Have We Learned?” by Adam Cagliarini, Christopher Kent and Glenn Stevens

By Jean-Claude Trichet, President of the ECB, at the Symposium for the 50th anniversary of the Reserve Bank of Australia, Sydney, 9 February 2010

It is a great pleasure to be here in Sydney today to celebrate the 50th anniversary of the Reserve Bank of Australia. My pleasure is all the greater to have this opportunity to discuss – on the basis of an excellent paper by Governor Stevens and his colleagues – the lessons to draw from central bank experience over the past half century.

Given the many common challenges that we have faced in the central banking community over this period, it is perhaps unsurprising that I find myself in large agreement with the paper’s main arguments.

Looking back over recent decades, I would highlight many of the same lessons for monetary policy making that Governor Stevens identifies: recognition of the fundamentally monetary origins of inflation; appreciation of the importance of expectations in the inflation process; the consequent centrality of central bank credibility; and the resulting significance of the institutional arrangements surrounding monetary policy making, especially central bank independence. Such considerations were central to the design of the European Central Bank and to its monetary policy strategy, which guides our monetary policy decisions today.

Looking forward, I would also identify many of the same challenges for monetary policy in the coming years. Against a background of recent financial crisis, the role of central banks in containing financial imbalances and asset price misalignments clearly warrants further attention. And I agree that the future interaction between monetary and fiscal policies is likely to be complex in many parts of the world, given the considerable increase in public deficits and debt levels.

Notwithstanding this high level of agreement, in the interests of promoting discussion I will focus the remainder of my remarks on bringing a “European perspective” to the debate. In the monetary policy making community, we should always strive to learn from each other – a process which naturally implies a focus on differences in approach across central banks. Yet we should be careful not to over-emphasise these differences, which are often only subtle or rhetorical in nature. Surely the main feature of the past half century of monetary policy making – and perhaps especially of the most recent decades – is a convergence of central bank practice around three elements: a focus on price stability as the objective of monetary policy; a public quantification of that objective, supported by greater transparency of decision making; and greater central bank independence.

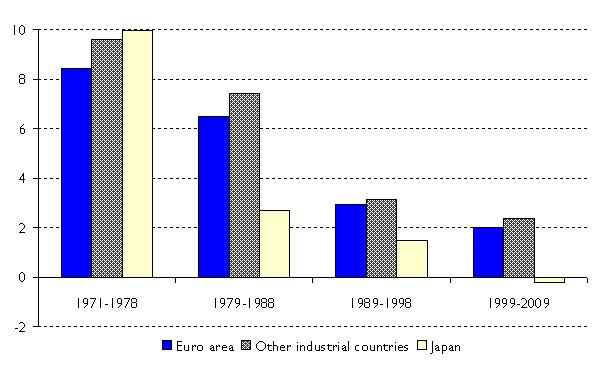

And, notwithstanding the substantial challenges we currently face, convergence around these three elements has produced impressive results. After the poor experience of the 1970s, inflation was reduced and a prolonged period of price stability established (see Figure 1). In the countries which would be part of the euro area as of January 1999, average inflation stood at over 8 percent in the 1970s and 6 percent in the ’80s, but has fallen to 2 percent since the introduction of the single currency. Price stability has established an important condition for greater economic prosperity.

Rule-based approach vs. constrained discretion

The increased credibility of central banks has been central to achieving this success. Since price setters are forward-looking, the evolution of price developments depends crucially on their expectations of future inflation. Anchoring private inflation expectations at levels consistent with price stability is therefore of the essence. This requires central banks to be credible. They must conduct monetary policy within a framework that convinces price setters that they will act in the future as necessary to maintain price stability.

In principle, central banks could offer an exhaustive list of how they would respond to any future eventuality. But in practice, it is impossible to foresee all future contingencies. I agree, in that regard, with John Taylor, [1] according to whom recent experience in the money markets has demonstrated that it is possible to observe “black swans” – even in places other than Australia!

Central banks therefore need to adopt a framework which attempts to strike a balance between: on the one hand, application of a specific rule fostering predictability; and, on the other, a completely discretionary approach offering flexibility in the face of unforeseen circumstances.

The inflation targeting strategy adopted in Australia is one attempt in this direction. Governor Stevens describes this as a framework of “ constrained discretion ”. The ECB’s monetary policy strategy is another. We have often described our approach as being “ rule-based, but not rule-bound ”.

Is there a fundamental difference between “rule-based” behaviour and “constrained discretion”? I do not think so. Rather the differences of language reflect different historical experience and cultural norms. In Europe – which has historically experienced high levels of inflation, and even hyperinflation – throughout the past fifty years there has been a preference for rules to constrain policy makers, so as to avoid previous mistakes. Australia’s experience, which is in line with the experience of English-speaking countries, has been different.

Medium-term orientation and monetary analysis

Whether characterised as “constrained discretion” or “rule-based, but not rule bound”, modern monetary policy frameworks accord central banks a certain “degree of freedom” in their decision making. To what ends should this freedom be put?

To be clear, it is crucial that price stability is maintained over the medium term. But it is neither feasible nor desirable for inflation to be targeted on a short term basis. Within the academic literature, this is recognised in the so-called “flexible inflation targeting” framework. [2] This framework explicitly foresees the use of monetary policy to smooth developments in economic activity over the business cycle, while anchoring longer-term inflation expectations at levels consistent with price stability.

From the outset, such considerations were also recognised in the ECB’s strategy. We have always acknowledged the need to avoid excess volatility in output and nominal interest rates, which would have resulted from excessive “fine tuning”. [3] Our approach is characterised by a medium-term orientation, which recognises that – given lags in monetary policy transmission and the inevitable short-term shocks to price developments – we should not attempt to “micro-manage” price developments. Rather we evaluate risks to price stability at the medium-to-longer term horizon.

The literature has focused on the use of monetary policy to smooth output in the relatively shorter run. But the flexibility accorded by a “rules-based, but not rule-bound” approach can be oriented in other directions. For example, it can be used to contain financial imbalances, by applying the same approach as we adopt when facing other sources of inflationary pressure. If the slow accumulation of financial imbalances poses a threat to macroeconomic and price stability over the longer term, then we can respond to it in a commensurate manner, even if this response implies tolerating some inflation volatility in the shorter run.

At the ECB, we emphasise one tool which we believe helps us maintain a medium term orientation: the monetary analysis.

This is perhaps the most clearly recognisable distinguishing feature of the European approach. European central banks have always given prominence to assessing monetary dynamics and asset prices when preparing monetary policy decisions. At the ECB, we have always foreseen that the close monitoring of monetary and credit developments would provide important elements of a framework for addressing asset price misalignments. [4]

One particular focus of our monetary analysis is the low-frequency trend in money and credit developments, which is associated with the emergence of imbalances. This focus allows us both to assess risks to price stability in the medium to long term and, simultaneously, to lean against excessive money, credit and asset price growth in our interest rate decisions. Such considerations influenced our interest rate decisions in 2004 and 2005. These decisions were criticised at the time by a number of observers, including governments and the IMF. With the benefit of hindsight, they appear particularly well-judged. Certainly, this approach has helped to create greater symmetry in our response to asset price developments, and it was at the time an important ingredient in the decision. [5]

Global developments matter

The importance of monitoring money and credit developments is beginning to be more recognised by academics, as well as in the policy debate. For example, leading academics have argued in favour of defining and monitoring new monetary indicators to detect the build-up of leverage within the financial sector. [6]

Of course, recognising the importance of monetary analysis does not necessarily simplify the task of interpreting monetary and financial developments. Experience has shown that ongoing financial innovation makes the interpretation of the monetary data particularly challenging. Therefore, we are continuously seeking to sharpen and deepen our understanding of monetary and financial developments.

One result derived from this ECB research relates to the identification of the global nature of asset price boom - bust cycles and associated financial crises. This suggests that there should be global concern over the monetary and credit developments that underpin these episodes. Not surprisingly, recent ECB research suggests that global variables – rather than only national or regional indicators – can enhance our ability to identify a build-up of financial imbalances. [7] I take this opportunity to raise awareness in the central banking community of the importance of monetary analysis and its implications, both for economies individually and globally.

Concluding remarks

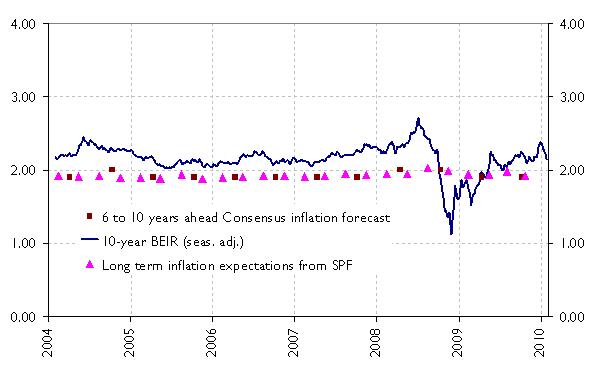

We are emerging from the uncharted waters navigated over the past few years. But as central bankers we are always faced with new episodes of turbulence in the economic and financial environment. While we grapple with how to deal with ever new challenges, we must not forget the fundamental tenets that we have learned over the past decades. Keeping inflation expectations anchored remains of paramount importance, under exceptional circumstances even more than in normal times. Our framework has been successful in this regard thus far (see Figure 2).

The RBA has operated through fifty turbulent years of monetary policy making. As recent experience has shown, there will be a need for innovation by central banks to meet novel challenges. But the lessons of the past fifty years – and, in particular, our success in anchoring inflation expectations – should remain uppermost in our minds.

Figure 1: Inflation developments in industrial economies

percent per annum, averages of quarterly data

Note: “Other industrial countries” denotes the (equally weighted) average of CPI inflation rates in Australia, Canada, the United Kingdom and the United States.

Source: OECD and Euro Area Wide Model database.

Figure 2: Measures of longer-term inflation expectations in the euro area

percent per annum, 5-day averages of daily data

Note: Data in percent; BEIR denotes the Break-Even Inflation Rate; SPF denotes the ECB Survey of Professional Forecasters

Source: Consensus Economics, Reuters, ECB Calculations

-

[1]J. Taylor and J.C. Williams (2009), “A black swan in the money market,” American Economic Journal: Macroeconomics 1(1), pp. 58-83.

-

[2]L.E.O. Svennson (1998), “Inflation targeting in an open economy: Strict or flexible inflation targeting?”, Victoria Economic Commentaries 15(1).

-

[3]ECB (1999), “The stability-oriented monetary policy strategy of the Eurosystem”, Monthly Bulletin (January).

-

[4]EMI (1997), “The single monetary policy in Stage Three: Elements of the monetary policy strategy of the ESCB.” O. Issing (2002), “Why stable prices and stable markets are important and how they fit together”, Monetary Stability Foundation, Frankfurt am Main.

-

[5]See in particular J.C. Trichet (2009), “Credible alertness revisited”, intervention at the symposium “Financial stability and macroeconomic policy”, Jackson Hole, Wyoming, August 2009.

-

[6]T. Adrian and H.S. Shin (2008). “Financial intermediaries, financial stability, and monetary policy,” presented at the Federal Reserve Bank of Kansas City Jackson Hole Symposium

-

[7]See L. Alessi and C. Detken (2009). “Real time early warning indicators for costly asset price boom/bust cycles: A role for global liquidity,” ECB working paper no. 1039.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts