Productivity, structural reforms and globalisation

Speech by Jürgen Stark, Member of the Executive Board of the ECBdelivered at the UnternehmerforumBrussels, 11 October 2007

It is a great pleasure to be here today and talk to you about the economic situation and outlook for the euro area economy. Nowadays the two big questions which many people have in mind when they think about this topic are: is the euro area economy at a turning point? And: what can we do to move to a path of high, sustainable growth? In my presentation, I will share some thoughts with you and provide some tentative answers. I will look at these issues from a particular angle.

First, I would like to discuss the recent economic developments and the uncertainty we face regarding the economic outlook. Part of the uncertainty relates to the assessment of labour productivity developments, which will be the main topic of the second part of my speech. Labour productivity is a, or even the, driving force behind economic growth. Assessing trends in labour productivity is therefore important, but it remains also a complicated task in real time. I will provide you with some evidence which shapes our assessment of recent productivity developments and put it into the context of the long-term slowdown that can be observed for the euro area. Future productivity performance will depend on the ability of governments to put into place the right policies and the ability of euro area economies to cope with the challenges of globalisation. This topic will conclude my talk today.

1 Euro area economic performance since 2006 and outlook

Growth in economic activity in the euro area accelerated during 2006 and remained strong in the first half of 2007 after a prolonged period of subdued growth, which began in 2001. Global economic growth was very dynamic, in particular in emerging Asia and with high growth rates in the new EU Member States. Moreover, different domestic demand components gained momentum. Investment dynamics benefited from an extended period of favourable financing conditions, balance sheet restructuring, strong corporate earnings and gains in business efficiency. Consumption also strengthened further, in line with the developments in real disposable income, which was increasingly supported by employment growth and improving labour market conditions.

Employment in the euro area increased by more than two million in 2006, an increase which was in line with the pattern of economic growth and contained real wages reflecting the impact of recent labour market policy measures. Employment growth was fairly evenly spread across age, gender and skill groups. It was marked by a significant rise in both permanent and full-time jobs and stopped the decline in employment among low-skilled workers. Thus it went beyond the increase in the employment rate among female and older workers as well as temporary and part-time job ratios observable in previous years. The strength of employment growth also translated into a sizeable reduction in the unemployment rate.

Turning to more recent developments, much of the information that has become available confirms the good fundamentals of the euro area economy as well as the sustained pace of economic growth, although it has moderated slightly from the rates observed in the second half of 2006.

However, preliminary data for the third quarter show strong industrial production and growth in the services sector remains solid. Also, labour market dynamics continue to be robust, thereby supporting private consumption growth. Corporate earnings and profitability have also been sustained. Data on activity from various confidence indicators and indicator-based estimates have declined but remain favourable. Survey indicators for the euro area services sector deteriorated on account of disappointing recent demand and the EC survey on consumer and business confidence dropped in September. The decline in confidence was reflected in all sectors apart from construction. While financial market volatility appears to have contributed to this decline, these indicators remain above their historical averages and therefore continue to point to sustained growth during the second half of 2007.

The recent financial turmoil has generally raised the degree of uncertainty about the outlook for economic activity in the euro area. Particular caution needs to be exercised when assessing any impact of financial market developments on the real economy. It thus remains necessary to gather additional information and examine new data before drawing further conclusions. The overall impact will depend on spillovers from the effects of financial market turbulence on the US economy and on global demand. In the euro area, it will largely depend on how the upheaval affects financing conditions and domestic demand. Regarding demand in the euro area, I already mentioned that, at this stage, there is little evidence of an impact beyond the decline in confidence indicators.

As for financing conditions, in our view the higher risk premia now embedded in stock prices and corporate bond prices largely reflect a correction of the past under-appreciation of risk. Debt and equity financing costs in markets and via monetary and financial institutions have increased in recent months, although corporate bond spreads are still not exceptionally high by historical standards. Moreover, heightened financial uncertainty seems, so far, to have led only to a limited ‘flight to safety’. Credit growth to households and especially corporations remains strong, although this may reflect, in part, the re-intermediation of financing onto bank balance sheets. The results of the October 2007 Bank Lending Survey suggest that euro area banks tightened somewhat credit standards applied to loans to households and firms in the third quarter of 2007 and expect to tighten them further in this quarter. However, more data are required to obtain a more comprehensive view of the impact of the financial market turbulence on financing conditions and money as well as credit growth.

The uncertainty about financial institutions’ potential exposure to US sub-prime-related losses and to the valuation techniques of complicated structured credit products, however, does appear to have led to a lack of confidence among banks and thus tensions in the interbank money market. The ECB immediately reacted to the market tensions and continues to contribute to the smooth operation of money markets.

Turning to global demand factors, global economic activity remains resilient so far despite the turmoil. The impact of the US economic slowdown on world demand (and euro area foreign demand) has been largely offset by robust economic growth in emerging economies. But the financial turmoil has increased downside risks to the global economic outlook, intensifying those already stemming from possible further increases in oil and commodity prices, rising protectionist pressures and broader concerns about global imbalances. Against this background, international organisations and private forecasters have in fact been recently revising their projections for economic growth slightly downwards.

Let me now turn briefly to recent price developments and the outlook for inflation. According to Eurostat’s flash estimate, the annual HICP inflation rate increased strongly to 2.1% in September 2007, from 1.7% in August, having been below 2% for 12 consecutive months. A particularly strong effect from the decline of energy prices a year ago, combined with the recent substantial increase in oil prices, contributed significantly to this increase. Owing to this effect, we are now entering a period during which we expect the inflation rate to remain significantly above 2% in the remaining months of 2007 and in early 2008, before moderating again.

Looking at the performance of different HICP components shows that inflation remains high in unprocessed food – although it declined slightly to 2.4% in August – and in services prices. The acceleration of services prices since the start of the year, now standing at an elevated level of 2.6% for the fourth consecutive month, is partly explained by the impact of the rise in German VAT, but is also linked to the better ability of firms to pass higher costs on to customers. Capacity utilisation has risen over the past two years for manufacturing and services. Indicators suggest that it is still increasing in the services sector, and that price pressures along the production chain have strengthened further.

On food prices, I would like to make a small incidental remark. Food prices appear to be among the most important factors affecting the inflation perception of people. In Germany, as in other countries, the strong attention paid to food prices was certainly also supported by the press coverage of the issue. The overall contribution of food prices to actual inflation, however, is limited by their weight in the overall euro area HICP, which is approximately 12% for processed food and 8% for unprocessed food. This is one of the reasons why, at times, some discrepancies between the perceived inflation rate and actual inflation may emerge. [1] Of course in our economic analysis, we have to take actual price developments and people’s expectations affecting their spending and savings behaviour into account.

Risks to the outlook for price developments remain on the upside. They continue to include the possibility of further increases in the prices of oil and agricultural products as well as additional increases in administered prices and indirect taxes beyond those announced thus far. Moreover, taking into account the existence of capacity constraints, the favourable momentum of real GDP growth observed over the past few quarters and the signs of a further tightening of labour markets, with labour shortages increasingly being mentioned in surveys as a source of concern in the industry and services sectors, suggests that stronger than currently expected wage developments may occur. This may be coupled with an increase in the pricing power in market segments with low competition. Such developments would pose upward risks to price stability. It is therefore crucial that all parties concerned meet their responsibilities.

The ECB always cross-checks its assessment of price stability emerging from the economic analysis with the indications about medium to longer-term risks apparent from our monetary analysis. Without going into the details – because some of the elements were already mentioned before, when I discussed financial market and credit conditions – let me just say that our current monetary analysis identifies continued strong underlying rates of money and credit expansion and thus confirms the prevailing upside risks to price stability at medium to longer-term horizons. The current experience indeed confirms again the usefulness of the ECB’s approach. A broad assessment of underlying trends in money and credit growth is particularly important during the current period of financial market volatility, as the latter may increase the focus on short-term behaviour and developments at the expense of the necessarily medium-term orientation of monetary policy. At the same time, monetary and credit data can offer an important insight into how financial institutions, households and firms have responded to the financial market volatility. In this respect, monetary analysis adds significantly to the robustness of the assessment underlying our monetary policy decisions.

In sum, available data suggests that economic activity in the euro area may continue to expand at rates close to potential output growth in the second half of 2007 and 2008. The sound fundamentals of the euro area economy – notably the healthy financial situation of the corporate sector and the strong labour market – bode well for a smooth absorption of the recent financial market turbulence. Global economic activity is expected to remain robust and to provide support for euro area exports and investment. Consumption in the euro area should contribute to growth in line with developments in real disposable income, as employment conditions remain supportive. At the same time, risks to price stability remain on the upside. There is, nevertheless, a high margin of uncertainty surrounding this outlook and risks for the economy are on the downside. They relate mainly to a potentially broader impact of the reappraisal of risk currently occurring in financial markets, possible disorderly developments related to global imbalances and protectionist pressures, as well as potential further oil and commodity price rises.

2 Labour productivity developments in the euro area

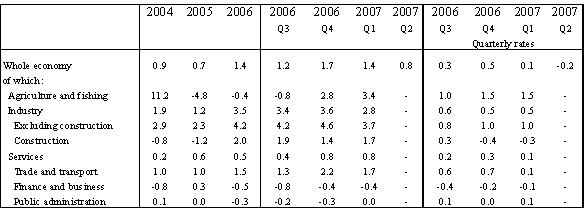

One piece of the information jigsaw that the ECB puts together in its assessment of the economic situation and the outlook is the development of labour productivity. When we look at recent developments, data released by Eurostat in spring 2007 showed a clear acceleration in labour productivity growth (per person) in 2006, reaching 1.4% growth compared with 0.7% in 2005. In year-on-year terms, labour productivity growth peaked at 1.7% in the fourth quarter of 2006. At sectoral level, positive developments in labour productivity were mainly driven by developments in industry (excluding construction). However, labour productivity growth in the services sector also showed signs of improvement, recording an increase of 0.8% year on year. These positive developments were welcomed by some economists as a reversal of previous trends and were regarded as the outcome of the successful implementation of recent market reforms. At the ECB, we were of the view that it was advisable to remain cautious as these developments may be cyclical. Unfortunately, the latest available national account data released by Eurostat in autumn 2007 have corroborated our concerns. The latest available data (see Table 1) show that labour productivity growth declined in the second quarter of 2007 and currently stands well below its peak at the end of 2006.

What makes this development complicated, as I said before, is the fact that the assessment requires the short-term, cyclical element to be disentangled from the longer-term trends or structural changes. Labour productivity – that is the output per unit of labour (either in terms of persons or hours worked) – may change due to the amount of capital or machinery put at the service of workers, technological progress or managerial efficiency gains, or the current economic situation leading to higher or lower capacity utilisation. Disentangling the short and longer-term nature of changes in all these factors in real time is probably difficult at company level, but even more complex at an aggregate level for sectors and the economy at the whole.

In practice, we use a wide range of indicators, including some time-series techniques, for our assessment. Simple trend estimates extracted from macroeconomic time series tend to be unreliable. Therefore, rather than focusing on one or more of these summary indicators, a real-time economic analysis of the degree of permanent changes in productivity (or productivity trend) incorporates a broader set of indicators.

From this perspective, several available indicators corroborate our view that the recent developments have to be seen rather as a cyclical phenomenon and not necessarily as a change in the underlying trend. First, our own estimates of trend labour productivity suggest that the trend has not shifted upwards by a big margin, if at all. Second, from a historical perspective, the pace of improvements in the services sector remains modest compared with that of the early 1990s. Third, although there has been a pick-up in the contribution made by innovation and other efficiency gains to labour productivity growth, this remains subdued by historical standards. Furthermore, the contribution from capital deepening, namely the growth in capital used per unit of labour, further suggests that recent developments in labour productivity may very well be associated with a cyclical pick-up in investment activity.

What makes the development important is the fact that productivity is a prime determinant of the speed of output growth per capita in the long run. As long as economies cannot expand their workforce and the amount of people employed indefinitely, growth has to come mainly from higher productivity through technological progress. A trend increase in productivity should therefore be factored into our assessment of potential output and the current cyclical position of the economy. Labour productivity growth has also direct implications for people’s wealth. Higher levels of long-term productivity growth through technological advances imply better investment opportunities in the future. All else being equal, it should lead to lower prices and allow for higher wages, since workers are more productive. This would increase people’s expected income and affect their patterns of consumption.

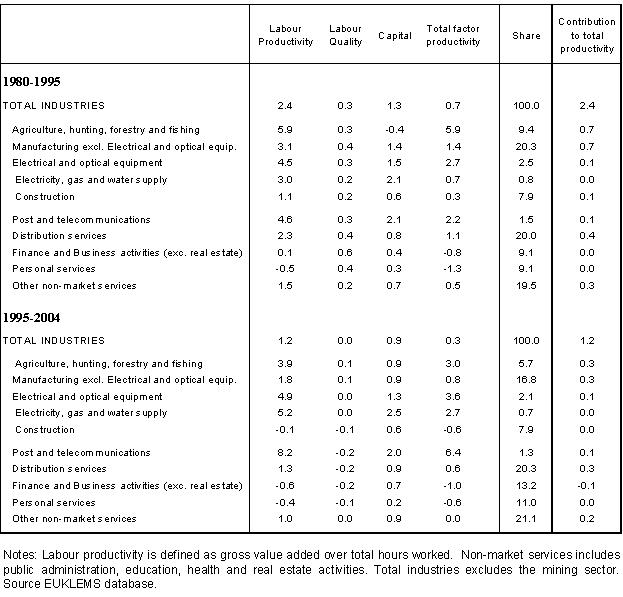

From this perspective, the assessment that recent productivity figures do not clearly point to a major ‘break’ with past developments is somewhat disenchanting since the euro area has been characterised by a sustained decline in labour productivity growth since the early 1960s. Measured per hour, labour productivity growth averaged 4.7% in the 1960s and 1970s, 2.2% in the 1980s and 1990s and around 1.3% at the beginning of this century. The slowdown in labour productivity growth in the euro area is a reflection of both lower growth in innovation and other efficiency gains (as proxied by the concept of total factor productivity, TFP) and lower growth in capital (i.e. machinery) used per unit of labour. From 1996 to 2004 the contribution to growth from capital deepening in the euro area was 0.9 percentage point, while it was 1.3 between 1980 and 1995.

When assessing the long-term slowdown, we have to take into account the fact that the reduction in the growth rate of capital deepening can probably be seen as the flip side of the employment-rich growth which we experienced over recent years. This reflects an environment of wage moderation and progress with labour market reforms which may have partly reversed the earlier trend to substitute labour, which had become more expensive due to wage increases outpacing productivity gains, in favour of capital, in the 1980s and early 1990s.

The slowdown appears more disappointing in view of the fact that it contrasts sharply with the very positive developments in labour productivity in other major economies, most noticeably the United States. The second half of the 1990s saw a period of sharp acceleration in productivity growth in the US (see Table 2). In the eyes of many observers, this was caused primarily by the innovations in the information and communication technology (ICT) sector. Together with the rapid pace of growth in the 1995-2000 period, it prompted some economists to suggest that the US economy was ready to pursue a new path of rapid growth. You will remember when the idea of a ‘new economy’ emerged.

The rate of growth of GDP in the euro area in the second half of the 1990s was significantly lower than in the US. Nonetheless, advocates of the new economy, i.e. believers in the radical implications that the new technologies have for potential growth, suggested that similar developments on this side of the Atlantic were likely to take place. The question is why this did not materialise.

The contributions from ICT technologies (e.g. computers and the internet) to labour productivity growth come from three main sources: a direct contribution from the production of ICT capital, a direct contribution from the use of ICT capital in the production of goods and services, and indirectly from possible ‘spillover’ effects from the use of ICT capital. These ‘spillover’ effects amount, among other things, to the possibility of introducing more advanced management techniques in the production process. [2]

When comparing the euro area with other major industrialised economies, we see (Table 2 in the Annex) that the direct contribution from ICT capital increased in both periods between 1980 and 1995 and between 1995 and 2004 in the euro area, the United States and the United Kingdom, but remains at a higher level in the United States and the United Kingdom. In addition, it is commonly acknowledged that the higher TFP growth, in particular in the US, reflects at least partly the spillovers from the development and adoption of ICT technologies as a so-called “general purpose technology” that affects the entire production sector. [3]

When looking at euro area productivity at sectoral level, we do not find any immediate evidence for such spillover effects in the non-high-tech ICT producing sectors [4] (see Table 3): First, the performance of traditional non-high-tech manufacturing industries deteriorated significantly. This is responsible for most of the labour productivity slowdown in the euro area. Second, the performance of non-high-tech services remained weak. While its contribution in relative terms is not as sizeable as that from the traditional manufacturing industries, this, however, should come as little consolation, as in absolute terms, labour productivity growth in these services industries has remained subdued. This is the more so when compared with developments in the US, which saw a large acceleration in productivity, especially in these industries, over the same period. [5]

Overall, there may be various forces underlying the slowdown, and I do not claim that my presentation provides a fully comprehensive picture. From the pattern of slowdown in the euro area, we can nevertheless conclude, when comparing with other industrialised economies, that one major reason lies in the failure of major euro area countries to take full advantage of new technologies or, at least, their lagged adjustment to the situation.

3 Productivity growth, market structure and globalisation

3.1 Market structure and productivity growth

Why might Europe have been less able to participate in the productivity pick-up and is it doomed to follow a continued slowdown? The performance of European countries can be traced back to existing policies and market rigidities. Policies have changed over the last decade and the impact of these policy reforms is partly visible, but the structural reforms identified in the Lisbon agenda still have the potential to further increase both labour productivity growth and therefore the long-term growth potential of the European economy. Major structural reforms are obviously not easy to achieve and require a high degree of ‘national ownership’ and commitment to the reform objectives agreed under the Lisbon process. The initiative of entrepreneurs has often been essential – certainly in Germany – in putting reform proposals on the agenda and keeping up the pressure to get them implemented.

The role played by research and development and education is key for innovation. Promoting R&D investment includes a better use of public procurement, more innovation-friendly regulation and stepping up the provision of targeted fiscal incentives to the private sector. Finland is currently the only country in the euro area which complies with the Lisbon target of 3% spending on R&D. Adequate systems to support R&D are of course not only a quantitative issue; increasing the efficiency of research at the same time is essential.

A highly educated labour force fosters prospects for innovation and facilitates the adoption of new technologies from abroad. [6]

In my view, a healthy economic environment consists of well-functioning product markets. This means an environment where competitive forces will reduce price margins, and therefore entrepreneurs have a strong incentive to allocate their resources in the most efficient way. An additional channel through which competition has an impact on labour productivity is via enhanced innovation, for when competitive pressures are strong there are more incentives to innovate so as to gain an advantage over rivals.

Numerous economic studies have documented the positive link between competition and innovation. [7] Against this background, it can be said that the removal of barriers to competition should be a policy priority of the European Commission. Some steps have been taken and their fruits are already visible. For example, the recent reforms implemented in the telecommunications sector show up in their high levels of labour productivity growth (see Table 3). It is also reassuring to know that most euro area countries have passed competition laws which are comparable in depth with the best legal frameworks available to other major OECD countries. With the exception of agricultural products, these countries score equally well in reducing trade restrictions and in not imposing excessive restrictions on foreign direct investment. However, more remains to be done as regards the pursuit of effective competition in the energy market and the implementation of the Services Directive.

Increasing competition, of course, also means that innovation needs appropriate protection. Incentives to invest in innovation would completely vanish if rewards were to be fully shared with competitors due to spillover effects and if the rights associated with the investment were left unprotected. Laws to protect property rights and the strict international enforcement of these laws remain indispensable.

A competitive and well-developed financial system is also a key to enhancing growth prospects. [8] A modern financial system boosts economic efficiency by channelling resources to the most profitable activities. A process of European financial integration is gradually taking place and considerable progress has been made, for instance, in capital markets and wholesale banking. However, the retail banking sector does not appear to have reached its potential yet, and competition seems insufficient in this area; it leaves European consumers and small and medium-sized enterprises unable to take full advantage of the benefits of EMU and the Single Market.

Inflexible labour markets have also been blamed for the labour productivity slowdown in the euro area. Labour market rigidities discourage the effective reallocation of labour. For example, it has been argued that American workers tend to invest more in general human capital, while European workers favour specific human capital investments. This may be partly linked to the fact that workers in the US have little unemployment protection and low unemployment benefits. On this score, employment protection legislation may have a particularly strong negative impact on industries subject to rapid technological change since it may preclude efficient matching of workers to jobs in view of new job requirements. Unfortunately, progress in increasing contractual flexibility, in particular for permanent workers, has been disappointingly slow in several euro area countries.

Labour market flexibility is not an issue of productivity growth only. Flexible labour markets in terms of wage and employment adjustment benefit both firms and workers. Contractual flexibility is essential in a world of technological change and globalisation – about which I will talk more in a minute – where workers can no longer count on job security. It enhances the opportunity to get into a new position and leads to higher employment security. Education and training systems need to help workers master transitions between jobs and keep up with technological developments. Flexible labour markets and efficient activation measures contribute to shorter periods of unemployment, which could otherwise lead to a decline in worker’s skills and productivity.

3.2 Globalisation and productivity growth

Let me now turn to the link between globalisation and productivity growth. In essence, globalisation means the increased international economic interdependence and the rapid integration of several emerging economies into global trade and production networks that we have experienced in recent decades. However, it also includes the growing internationalisation of financial markets and capital movements, a phenomenon which has intensified since the mid-1990s. Globalisation brings clear benefits to the economy, but at the same time poses significant challenges.

Let’s look at the benefits: first, trade liberalisation and globalisation enables an economy to obtain the cheapest products on the world market, and may, in turn, exert downward pressure on domestic prices through lower import prices, thereby increasing the real wealth of the importing economy. Globalisation implies welfare gains by having a dampening effect on consumer prices, while allowing producers to substitute cheaper intermediate goods, thereby increasing profit margins or improving their price competitiveness.

Second, globalisation has certainly helped to stimulate competition in domestic markets and to increase and diversify euro area trade linkages. In 1995, two-thirds of extra-euro area manufacturing imports came from industrialised, high-cost countries, whereas in 2005 their share had declined to around 50%. The decrease is distributed among the traditional major euro area trade partners (the United Kingdom, Japan, the United States), while the shift towards emerging, low-cost economies is mainly accounted for by increased imports from China and, to a lesser extent, the new EU Member States.

Third, and most importantly in the context of my presentation today, globalisation impacts on productivity through trade, capital mobility and the internationalisation of technology and R&D, which can lead to a reallocation of production processes. Trade increases incentives to specialise in higher- productivity sectors, produce economies of scale and encourages innovation. Inward and outward foreign direct investment implies opportunities to learn and adopt technologies and productivity-enhancing practices from abroad. At the same time, the internationalisation of R&D supports domestic innovation and technological progress. Immigration may also help to increase the matching efficiency of labour markets.

However, it is also true that globalisation presents challenges. In order to reap its potential gains, globalisation requires economies to adjust to the reallocation of production and the new competition from emerging markets in certain sectors. The tremendously increased supply of products from emerging markets may induce a reorganisation of production in euro area countries. This strengthens the need for occupational mobility and the capacity to also absorb low-skilled labour in new sectors. The restructuring of the economy may lead to an at least temporary decrease in productivity, which would be more protracted the ‘stickier’ the economy and less able to overhaul traditional production structures. This may imply that those countries where the pace of reforms has been slow may find themselves, paradoxically, in a worse position than in the past. Economies with uncompetitive product markets and rigid labour markets not only fail to adjust to technological change, but are also more vulnerable to shocks associated with the globalisation process.

Concluding remarks

I would like to conclude by saying that Europe is reforming its economy so as to adapt to the challenges of globalisation, technological change and ageing. Considerable progress has been achieved, as reflected in the significant rise in employment growth. Now the challenge is to also raise the level of productivity growth in all euro area countries. If this challenge is not met, it is hard to imagine that Europe will be able to achieve a higher growth path and to keep the wealth of its citizens. Monetary Union has been effective – and very successful – in supporting growth through a credible monetary policy which creates a stable macroeconomic environment and has lowered financing costs for a number of euro area countries through a reduction of risk premia.

EMU, moreover, gives impetus to European integration, particularly in financial markets, and to a further reduction of the barriers to competition. The Lisbon process now provides the tools to address the challenge of fully reversing the previous slowdown through further structural reforms. It will require the firm commitment of governments, entrepreneurs and workers to be successful and meet this challenge. I am still highly optimistic that we will succeed.

Annex

Table 1. Euro area labour productivity growth (annual % changes unless otherwise stated)

Note: Labour productivity is measured as value added over total employment. Source: Eurostat.

Table 2. Contributions to labour productivity growth

| EA | US | UK | JP | |||||

|---|---|---|---|---|---|---|---|---|

| 1980-95 | 1995-04 | 1980-95 | 1995-04 | 1980-95 | 1995-04 | 1980-95 | 1995-04 | |

| LP growth | 2.4 | 1.2 | 1.2 | 2.4 | 2.4 | 1.9 | 3.2 | 1.8 |

| Contributions: | ||||||||

| Labour quality | 0.3 | 0.0 | 0.2 | 0.3 | 0.3 | 0.5 | 0.3 | 0.3 |

| ICT capital | 0.3 | 0.4 | 0.4 | 0.6 | 0.5 | 0.7 | 0.4 | 0.3 |

| Other capital | 1.0 | 0.5 | 0.2 | 0.3 | 0.5 | 0.3 | 1.8 | 1.1 |

| TFP | 0.7 | 0.3 | 0.3 | 1.1 | 1.1 | 0.4 | 0.8 | 0.1 |

Notes: LP growth stands for labour productivity growth per hour worked; TFP stands for total factor productivity. Sources: ECB calculations using EUKLEMS data.

Table 3. Euro area labour productivity growth and contributions (annual average rates, in %)

-

[1] For a further discussion see the article entitled “Measured inflation and inflation perception in the euro area” in the May 2007 issue of the Monthly Bulletin as well as the box on “Recent food price developments in world markets and the euro area” in the September 2007 issue of the Monthly Bulletin.

-

[2] An early report from the OECD pointed to the potential consequences of the internet on TFP and expanded on the benefits that ICT brings in terms of new organisation of production and sales. See OECD (2000): A New Economy? The Changing Role of Innovation and Information Technology in Growth. Paris.

-

[3] See Stiroh, K. J. (2002): ‘Are ICT Spillovers driving the new economy?’ Review of Income and Wealth, Series 48, No 1, March.

-

[4] Unfortunately, standard correlation analysis between aggregate TFP and ICT capital growth does not suffice to confirm the existence of spillover effects. Other factors apart from possible spillovers could also explain a possible correlation between ICT capital growth and changes in TFP. These other factors are: i) mismeasured production inputs, ii) omitted variables that are correlated with ICT capital, and iii) the possibility of increasing returns to scale or imperfect competition.

-

[5] The primary sector contributed negatively to the slowdown despite its strong performance. However, its negative contribution is simply the outcome of the reallocation of labour to other industries in response to changes in domestic demand resulting from the completion of the modernisation process.

-

[6] See J. Temple (2001): “Growth effects of education and social capital in the OECD countries”. OECD Economic Studies, No 33, pp. 57-101.

-

[7] For a further extension of this topic see European Commission (2004), “The link between product market reforms and productivity: direct and indirect impacts”, the EU Economy: 2004 Review. Further evidence is also to be found in Griffith, R., R. Harrison and H. Simpson (2006): “The link between product market reform, innovation and EU macroeconomic performance”, DG-ECFIN Economic Papers No 243, February 2006.

-

[8] See, for example, S. Claessens and L. Laeven (2005), “Financial sector competition, financial dependence and growth”, Journal of the European Economic Association, Vol. 3, pp. 179-207.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts