Monetary Policy and Private Expectations. Zolotas Lecture at the Bank of Greece

Speech by Jean-Claude Trichet, President of the ECBAthens, 25 February 2005.

Ladies and Gentlemen,

Xenophon Zolotas, long-serving Governor of the Bank of Greece and Prime Minister of his country, once said, with supreme synthesis, that “Political magic has always been anti-economic.” In history, monetary policy has sometimes reverted to magic in an attempt to eschew economic reality. The outcomes of such attempts are well-known and their magic has proven short-lived.

A decisive change in direction started, in a large part of the industrial world, 30 years ago as a result of a deeper understanding of the role of expectations in shaping economic behaviour. Today, solid and credible institutions have been put in place in many countries and have earned a respectable reputation of good policy management. Decades of experience accumulated from institutional evolution and advances in economic thinking have provided us with guidelines for designing credible institutions that are based on sound economic principles.

Clearly, the open-ended nature of economic progress confronts central banks with new and unprecedented challenges and will no doubt keep central banks occupied in the years to come with the issue of how to maintain expectations of low inflation and preserve credibility. The creation of the Euro is an example of such a challenge.

These will be my themes today. Governor and Prime Minister Zolotas was an early advocate of a monetary regime in which the formation of prices is fully protected from the influence of short-term considerations. So, some thoughts on expectations and their subtle interactions with institutions and policies might be an appropriate tribute to his memory.

Central banks’ long quest for macroeconomic stability

30 years ago the formation of expectations moved from a peripheral area of theoretical enquiry into the very core of macroeconomic thinking. Today, the economics of expectations and macroeconomics itself are largely coextensive. The trigger of this transformation was, as is well known, the rational expectations revolution, which started with the pioneering work by Robert Lucas (1972, 1973) and Thomas Sargent and Neil Wallace (1975).[1]

The upshot of the Rational Expectations hypothesis is that – at least in a world in which information is largely publicly available and speedily disseminated – individuals should not make predictable errors when formulating conjectures about their future. This does not imply that individuals will invariably forecast accurately if random movements are inevitable. But guesses about the future must be correct on average if individuals are to remain satisfied with the mechanism by which their anticipations are formulated. When agents diagnose systematic errors, they have an incentive to amend the basis of their forecasts. Expectations are thus the outcome of a decision process and this process responds and adapts to changing circumstances, in particular to possible changes in the behaviour of monetary authorities.

Understanding expectations formation as a process underscores the strategic interdependence that exists between expectations formation and economic institutions. Recognition of this interdependence by central bankers and legislators profoundly changed the way in which macroeconomic authorities view the nature of policymaking. Central bankers came to hold the view that monetary policy is not a sequence of isolated policy actions. If agents, when forming their expectations, seek to capture the general pattern of monetary policy, then the relevant problem to solve for central banks centres not only on the size and the timing of a given interest rate move in response to a particular state of the economy, but also and overall it relates to the strategy for repeatedly adjusting the policy instrument in response to the state of the economy, whatever this might be.

So, monetary policymakers and, gradually, legislators came to recognise that the meaningful set of choices that societies face relates to alternative monetary policy regimes, that is a clear specification of the central bank objective and of its strategy in managing economic events. The notion that monetary regimes are very powerful in shaping public expectations had received dramatic evidence when the old monetary policy order, the Bretton Woods arrangements, foundered. In those circumstances, private sectors in a large portion of the industrial world were left for years in the dark about the “true” objectives of monetary policy, and about the determination with which central banks were prepared to pursue it.

A new monetary order could not be established unless it tackled the problem of the mandate and of the strategy squarely. Building on a time-tested tradition of prudent central banking – which after all had survived in Germany, in Switzerland and in a number of other economies – a number of authors laid out the essence of the mandate problem.[2] It appeared that the anchoring of inflation and inflation expectations is primarily a matter of delegating monetary policy to an independent central bank with one overriding long-term objective: the maintenance of price stability.

As the collective reflections progressed, this notion was sharpened to a considerable extent. Throughout the 1990s many central bank charters were stipulated with institutional independence and the primary mandate of monetary stability. The 1998 decision of the ECB Governing Council to characterise its understanding of price stability in quantitative terms can be traced to a shared perception that such stipulations could help focus inflation expectations more tightly. Recent empirical work indeed offers support to that perception. Monetary institutions that have been more explicit in delineating what they mean – in numerical terms – by “price stability” have been more successful in promoting lower inflation and lower output variability.[3]

However, an appropriate mandate is a necessary but not a sufficient condition for lasting macroeconomic stability. Important sources of instability in inflation expectations could still arise if the central bank – even one endowed with a clear mandate to preserve price stability – is not sufficiently clear as regards its own monetary policy concept and strategy. The decision taken by the Governing Council of the ECB in October 1998 to spell out the contours of its monetary policy strategy attests to the extent to which the notion of a monetary policy strategy has become operationally meaningful.

To secure stability, a central bank has to act forcefully and pre-emptively to nascent signs of inflation or deflation.[4]

* * *

To be sure, a world in which central banks’ intended policy measures and market views are perfectly aligned is likely to appear only in textbook analysis. However, central banks’ preoccupation with private expectations has established a new climate of mutual understanding with economic agents and the public at large. Central banks have stepped up the number of institutional fora and occasional gatherings at which they document their strategies and carefully explain their actions to broad audiences. In 1998, when designing its mode of communication on monetary policy, the ECB chose to be in the vanguard of this new practice.

As a consequence, the leverage of central bank pronouncements and actions over private economic behaviour has considerably strengthened. One of the central banks’ key tasks has become today guiding the markets and stabilising sentiment.

These reflections might inspire two questions. The first is: how did the new European monetary regime successfully impose itself in the broad perceptions of the public? And the second is: to which kind of new challenges and new battles should we be prepared? Let me try to respond to these two questions.

The transition to Economic and Monetary Union

How expectations react to a major change in policy regime is still an issue of contention. 20 years ago, the fathers of the rational expectations revolution espoused an optimistic position: if an institutional change – even an abrupt one – is sufficiently credible, expectations will focus instantly on the new equilibrium. Other scholars are more inclined to think that instant refocusing is unlikely. Agents should be expected to learn gradually about the new regime, and probe and test it with the benefit of time. The extraordinary episode of the convergence towards Economic and Monetary Union in Europe in the second half of the 1990s offers a laboratory case for discriminating between these two hypotheses.

The Maastricht Treaty came into force in November 1993. Its fundamental inspiration was the need to ensure that participants in EMU are like-minded in their pursuit of stability in economic and monetary affairs. It vested the European System of Central Banks with a very high degree of independence and safeguarded it against external interference. The new single monetary authority was to be indisputably devoted to one overriding objective, the maintenance of price stability in the euro area. In that respect, the Treaty embodied both the best monetary tradition available in Europe and the essence of the principles that had been distilled through years of academic reflection.

In addition, convergence criteria were designed to provide countries with yardsticks against which to measure their progress toward a true culture of stability in the run-up to Monetary Union. But the interpretation of the entry criteria remained a matter of debate for most of the years that followed the promulgation of the Treaty. Observers were divided. Some took the position that the Treaty’s criteria were too strict and ambitious, given the initial conditions from which a number of member countries had to start convergence. Others, from the perspective of the most stable economies in the EU, were convinced that they granted considerable, in fact excessive, latitude.

This debate between strictness and latitude left a margin of ambiguity, which largely affected the evolution of expectations prior to 1998. The perception that the criteria might be impossible to meet for countries too far off the benchmarks produced uncertainty over the number of countries able to participate in Monetary Union from the outset. On the other hand, the suspicion that the Maastricht criteria would tolerate a large dispersion of economic performances across countries produced anxiety that Monetary Union – if it were ever to materialise – could mean convergence to the average, rather than the best, standards of macroeconomic discipline.

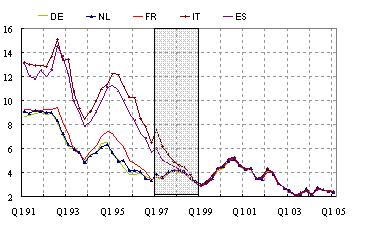

The power of a credible institutional change to bend expectations became evident in late 1996 and 1997. The latter part of 1996 saw a determined drive toward fiscal consolidation in Italy and Spain. This facilitated in those countries a sharp fall in interest rate premia at long maturities and an easing in monetary conditions more generally [see Charts 1d and 1a]. In June 1997, the Stability and Growth Pact was sealed in Amsterdam. It reassured the markets that the adjustment made in public finances in a large portion of the European Union would be lasting and would survive a country’s adoption of the euro. By the first half of 1997 interest rate differentials had been compressed to levels not seen in decades. Uncertainty surrounding the breadth of Monetary Union at its starting date thus quickly disappeared.

But a measure of anxiety remained about the standards that would apply in the new economic and monetary entity. This source of anxiety came to the surface in summer 1997, when the intermediate-maturity yields paid by those core countries which had reached complete alignment started to rise in sync [see Chart 1b and 1c]. The balance of market expectations seemed to be shifting toward a loose interpretation of the new regime. A conviction that was gaining ground was that the rapid descent of short-term rates in the converging economies of Italy, Spain and Portugal would be matched by a gradual increase in the short-term rates of the low-yield economies. The two paths would meet somewhere half-way.

This instability of market expectations did not go unnoticed in particular in the Central Banks issuing the currencies that had already converged. Signs of an upswing were still tentative and price strains were not yet fully in sight in this core currency area. Nevertheless, in October, pre-emptive action took place to forestall the build-up of an inflationary potential in the delicate phase of transition to monetary union. This interest rate move was a strong sign of determination. The policy message was reinforced through a consistent communication campaign which the Central Banks concerned, together with the European Monetary Institute, launched in the last few months of the year to explain the meaning of their action. The essence of the message was the following.

The assumption made by some observers and by part of the market literature, according to which the entry interest rates in the Euro on 1 January 1999 would be some kind of average of the interest rates of the composing currencies was totally wrong. On the contrary, the very construction of the Euro was based on total continuity with the most credible national currencies. The concept of the transition was based upon “benchmarking”, namely convergence towards the best performers and not convergence towards a mean. The modest interest rate increase that took place in a small number of economies was designed exclusively to preserve monetary stability and inflationary expectations for the corresponding currencies which were the benchmark for the Euro. The ECB itself, the soon to be born monetary authority, would be uncompromising in its role as guardian of price stability, in close continuity with its forebears. It was therefore fully justified that interest rate convergence inside the future Euro area would take place progressively on the basis of a merge of the different yield curves of the various currencies with the benchmark yield curve corresponding to the core currencies that had already converged.

How did markets react to that action? In particular, what was the impact of the October 1997 interest rate hike on long-term interest rates?

Before I answer that question, it could be instructive to reflect on the way markets typically react to an interest rate hike. A shift to a tighter policy raises short-term interest rates. Since longer-term rates are determined in good part as averages of expected future short-term rates, an initial tightening of policy – not to be immediately reversed – should exercise an upward pull on the yields paid by instruments with longer maturities. However, the factors determining long-term rates, notably those at the very long end of the term structure, are mostly associated with the premium to compensate for expected inflation and for the risk that inflation might vary widely over those horizons. Therefore, if the policy tightening is perceived as an effective action to restore or preserve conditions of price stability, then a hike in short-term rates does not necessarily suggest a rise in market rates on instruments with very long maturities. In fact, by soothing concerns about inflation looking far into the future, a policy hike could be reflected in a lower inflation premium and a decline in nominal long bond rates.

Indeed, empirical tests find that the sign of the overall response of long rates to a change in policy is not independent of the credibility rating that markets assign to the monetary regime in which they operate. With some simplification, two polar regimes have been identified. On the one side, a full-credibility environment is one in which there is no dispute over the “true” objective of monetary policy and about the central bank’s determination to do all it takes to keep inflation low and steady around that objective. Markets are not inclined to project an observed inflationary shock far into the future, as expectations are well-anchored. So, long-term rates are minimally affected by any inflation shock that might hit the economy in the current period, and by the monetary policy move that authorities might execute in response to it. Presumably, this is a world in which nominal long-term bond rates are most unresponsive to changes in policy. A world in which long bonds are regarded as a conservative type of investment, with stable and dependable real returns.

The opposite happens when inflation expectations are not firmly secured. In circumstances of incomplete credibility, an inflationary shock is more likely to be extrapolated far into the future, because inflation itself is more persistent, and because changes in the short-term rate are viewed as less effective in restraining inflationary pressures. In this regime, a policy tightening comes together with expectations of higher and more obstinate inflation in the future. So, long-term nominal yields will tend to move up in the aftermath of an interest rate hike.

A third typology is also conceivable: a situation in which markets perceive a shift from one regime to the other. Imagine that market participants were to regard a policy move as a signal dissipating all the ambiguity that might have existed before about the true objectives of monetary policy. Imagine that a single move in a particular situation were to show the foundations of a new regime, and show it to be more likely than the past regime to operate according to the rules of a full-credibility monetary standard. In this situation, one would expect to see an interest rate hike being accompanied by a decline in long-term rates.[5]

This brings me back to 1997. The evidence that we gather from that episode is very difficult to rationalise and highly controvertible, especially because the financial crises in Asia and Russia – which took place around the same time – might blur the picture as we look back to those times. Overall, the evidence certainly warrants closer and better scrutiny. But my reading of the episode is that it is consistent with a shift to a more credible policy regime.

After the announcement of October 1997 and the communication thereafter market rates reacted in a direction that few could have anticipated. Not only did the remaining spread between the converging economies and the core countries progressively disappear. Thus, the remaining ambiguity about the very nature of the convergence process finally dissipated. But many commentators and market participants – not to mention policymakers – noted that the benchmark yield curve itself was changing shape in a direction that demonstrated an additional clear break in expectations.[6]

This is without doubt a remarkable success. Yet, it is not one grounded in magic but based on a sequence of sound institutional, economic and monetary decisions.

Securing and reinforcing credibility

To sum up my understanding of why we have so impressively succeeded in mastering a smooth transition to the euro, I will mention six necessary conditions that had to be met and were met. Had only one of these conditions not been met, the transition would not have been a success. These conditions are the following:

Independence: full guarantee for the independence of the ECB was given by the Treaty and guaranteed by it;

Clarity: clear primary objective of price stability given by the Treaty to the new independent institution, the ECB;

Continuity: choice by the new institution of an arithmetic definition of price stability in the medium run for the euro area identical to the previous core definition of price stability;

Conceptual anchoring: choice by the new institution of the monetary policy concept based on a two pillar approach, with not only an economic pillar, but also a monetary pillar – helping, in particular, to anchor the long term side of the inflation expectations.

Transparency: decision to make public, from the very beginning, the arithmetic definition of price stability, the monetary policy strategy that would be applied by the ECB, as well as giving in real time the monthly diagnosis of the Governing Council and the reasons of the decisions taken on interest rates on the occasion of the press conferences following the meeting of the Governing Council;

Fiscal consistency: guarantees for sound fiscal policies enshrined in the Treaty in the form of the Maastricht criteria and appropriate implementation of these principles by the Stability and Growth Pact regulations.

It is my conviction that each and every of these six conditions were and are necessary. My personal conjecture is that the 6 together have proved to be a sufficient set of conditions to permit the full success of the transition. That being said, it remains absolutely remarkable that the real progress made in reducing inflation expectations in the core currency area in the few months leading up to the final decision over EMU participation in May 1998 was fully preserved at the moment of the transition and afterwards. I would suggest that economic research continue to work actively on the question of the optimality of the transition. After all, the setting up of the euro is historically the most important monetary reform of all times and this transition contains a wealth of information and lessons that have not yet been fully explored.

Anchoring solidly inflation expectations at a low level at the birth of the currency was a success. But credibility is never gained once and for all. It has to be permanently preserved and enhanced. That is the reason why for central bankers vigilance is always of the essence. To exert vigilance effectively and efficiently the anchoring and monitoring of inflation expectations, particularly on the long end of the time horizon, are both very important. Let me elaborate a little bit on that.

We know that excess volatility of expectations can be signalled by abnormal developments in monetary and credit conditions. This is likely to be the case when unsustainable surges in asset prices – propelled by flights of optimism, and sustained by unanchored expectations – are built on conditions of excess liquidity. The drifting of expectations away from the central bank objective toward chronic inflation or debilitating deflation has historically very often been associated with monetary imbalances foreshadowing and facilitating the process. So, broadening the scope of macroeconomic analysis to include a systematic monitoring of monetary and credit developments can offer a strong failsafe mechanism against the risk that, with inflationary pressures apparently at bay, the central bank might be encouraged to favour or tolerate boom-bust developments of credit and liquidity. The central bank committing to monitoring monetary developments and referring to a given path of long-run monetary growth – compatible with price stability and with steady-state growth for the real economy – has a powerful tool for anchoring long-term inflation expectations. The possibility that these expectations might not find a focal point, or might settle on a point inconsistent with the central-bank declared objective will be minimised.[7]

Monitoring a wide range of expectation indicators

The ECB also monitors a range of indicators that provide more direct evidence on inflationary expectations in the euro area.

It seems obvious that the way private agents form their anticipations will most likely differ in important dimensions across different types of agents. A central bank should thus not rely on a single indicator when monitoring these expectations but rather take a comprehensive and pragmatic approach that balances the information provided by various sources.[8] From this perspective, a single measure of expected inflation – one constructed on the basis of the central bank’s own internal analysis – might be particularly misleading.

By their very nature, inflation expectations are not directly observable. However, there exist two main ways to construct measures of inflation expectations. A direct way consists in asking people about their expectations of future inflation. A more indirect way is to extract the information revealed by observable financial data. The ECB makes constant use of both measures.

Direct measures of inflation expectations in the euro area are provided by a number of surveys. These are regularly analysed in the ECB’s Monthly Bulletin. One comes from the ECB Survey of Professional Forecasters. This is a quarterly survey conducted by the ECB. It asks experts affiliated with financial or non-financial institutions based within the European Union to forecast euro area inflation up to five years ahead. Importantly, survey respondents also provide a quantitative assessment of the uncertainty surrounding their forecasts in the form of ranges. The dispersion and asymmetry around the mean provide useful information about shifts in inflation expectations that might be in the pipeline.

Another measure of inflation expectations is provided by the survey conducted by Consensus Economics, a private firm. It asks private sector economists to give their short-term and long-term inflation expectations. A further source of information is the European Commission’s monthly Business and Consumer Survey. It asks a large number of manufacturing firms about their selling price expectations and consumers about their inflation expectations. This survey has some limitations however. It provides qualitative information only.[9] In addition, it is available only for a very short time period ahead (12 months). Despite these limitations, detected changes in the direction towards which firms’ and consumers’ expectations are heading may provide useful information.

The information that we gather from these diverse sources at present is consistent with a picture of stability. The mean point estimate for HICP inflation indicated by the respondents to the ECB survey in the 4th quarter of 2004 is close to and below 2%, in line with the ECB’s quantitative definition of price stability. This holds true for the expectations relating to the years 2005 and 2006, but also for the five-year period up to 2009. The uncertainty surrounding these forecasts is fairly small, implying that survey respondents assign only small probability to inflation outcomes outside the main scenario.

It has to be taken into account that a number of these measures – particularly those stemming from the “break-even” inflation rates extracted from the indexed bonds – remain imperfect indicators of inflation expectations, as several premia, most importantly an “inflation risk premium” but also a “liquidity premium,” are potentially embodied in their calculation. Changes in break-even inflation rates over time could therefore reflect changes in the level of expected inflation, changes in perceived uncertainty about future inflation, changes in the perception of the liquidity risk, or a combination of the three. In addition, their information content could be temporarily distorted by technical market or institutional factors and should therefore be interpreted with caution.

During the first half of 2004 break-even inflation rates for the euro area displayed a slight upward movement, unlike the survey evidence reviewed before. In recent months this movement has been partially reversed. While the different behaviour of break-even inflation rates and survey expectations may reflect a time variation in the risk premium contained in nominal bond yields, due for instance to uncertainties associated with the recent increases in energy price, these recent developments have not gone unnoticed at the ECB.[10] Whether the movements in the break-even inflation rates, which are fairly small in absolute terms, reflect or not underlying changes of various risks premia is not yet clear. We are looking at it very carefully.

Concluding remarks

A renewed fellowship between the academic community, the markets and central banks – so uncharacteristic if viewed from the angle of the dissonances of the ancient past – has been beneficial to the design of appropriate institutions and monetary strategies that allow central banks to effectively deliver the results society ultimately needs: stability and predictability in monetary matters.

What matters most is that inflation, thanks to these conceptual advances, has become a mean-reverting process, making occasional deviations from price stability a temporary event. We are living in a world where the possibility of solidly anchoring long term inflation expectations and eliminating the correlation between these long-term inflation expectations and actual inflation has become reality.

The ECB and the Eurosystem are proud to have been at the forefront of these advances. Not only have they fully preserved the solid anchoring of inflation expectations all along the past six years, but they have proved that it was possible to ship to the new currency, from day one of its existence, the best anchoring that was available in Europe, which was a major contribution for sustainable growth and job creation. I am fully conscious of the exceptionally high level of confidence and trust the private sector is bestowing on us. This trust is well placed. Economic agents, market participants and our fellow citizens of Europe can be assured that we are determined to remain worth it in all the years to come.

Charts

Chart 1. Interest rates in Germany, France, Spain, Italy and the Netherlands (1991-2005)

Annual percent

| Chart 1a: 3-month interest rates | Chart 1b: 2-year interest rates |

|

|

| Chart 1c: 5-year interest rates | Chart 1d: 10-year interest rates |

|

|

Sources: Datastream.

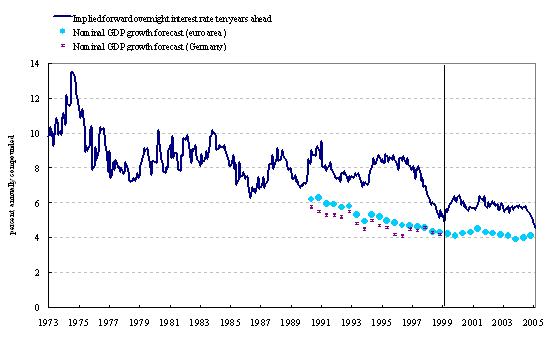

Chart 2. German implied forward overnight interest rates ten years ahead

Sources: Consensus Economics, Deutsche Bundesbank and ECB calculations. Last observation: January 2005.

Note: The implied forward overnight rate is the nominal rate expected to prevail in 10 years time. It is constructed on the assumption that the terminal value of a portfolio invested in t-period bond is equal to that of the portfolio continually reinvested at the overnight interest rate.

-

[1] Robert Lucas (1972), “Expectations and the neutrality of money,” Journal of Economic Theory, 4, pp. 103-124 and Robert Lucas (1973), “Some international evidence on output-inflation trade-off”, American Economic Review, Vol. 63(3), pp. 326-334. Thomas Sargent and Neil Wallace (1975), “Rational Expectations, the optimal monetary instrument and the optimal money supply rule,” Journal of Political Economy, Vol. 83(2), pp. 241-254.

-

[2] Robert Barro and David Gordon (1983), “A Positive Theory of Monetary Policy in a natural rate model”, Journal of Political Economy, Vol. 91, pp. 589-610; Kenneth Rogoff (1985), “The Optimal Degree of Commitment to and Intermediate Monetary Target”, Quarterly Journal of Economics, Vol.100, pp.1169-1189.

-

[3] Antonio Fatás, Ilian Mihov and Andrew Rose (2004), “Quantitative Goals for Monetary Policy”, working paper, available at http://www.insead.fr/%7Efatas/quant.pdf. Further evidence on the stability and anchoring properties of expectations is provided in Efrem Castelnuovo, Diego Rodriguez-Palenzuela and Sergio Nicoletti-Altimari (2003) in “Definition of price stability, range and point inflation targets: the anchoring of long-term inflation expectations”, ECB Working Paper No 273.

-

[4] Richard Clarida, Jordi Gali and Mark Gertler (1999) provide extensive discussion of the so-called “Taylor principle” in “The Science of Monetary Policy: a New Keynesian Perspective”, Journal of Economic Literature, American Economic Association, Vol. 37(4), pp. 1661-1707.

-

[5] That the response of long-term rates to a change in policy depends on the credibility of the monetary policy regime is conjectured in Marvin Goodfriend (1998), “Using the term structure of interest rates for monetary policy”, Federal Reserve Bank of Richmond Economic Quarterly, Vol. 84/3. Empirical confirmation of that conjecture is provided in Jagjit Chadha and Joe Ganley (1998), “Monetary policy, inflation persistence and the term structure of interest rates: Estimates for the United Kingdom, Germany and the United States” in Ignazio Angeloni and Riccardo Rovelli (eds.), “Monetary policy and the term structure of interest rates”, London: McMillan. Further support is found in Tore Ellingsen and Ulf Söderström (2001), “Monetary policy and market interest rates”, American Economic Review, Vol. 91(5), pp. 1594-1607.

-

[6] One possible interpretation is that markets were growing more convinced that the new regime would embody an even larger amount of credibility than they had attributed to the national central banks with the best monetary record in Europe. In this respect, it should also be noted that in January 1997 the Deutsche Bundesbank had revised its “price norm,” i.e. the “unavoidable inflation rate” that was used for the calculation of the monetary target, from 2% to a range between 1½ and 2%, whilst the Banque de France, for instance, was referring to less than 2 per cent as its definition of price stability. It is a remarkable achievement that the definition of price stability as “less than 2 per cent” was shipped intact to the whole union. This remarkable transition might have been helped by the fact that international financial markets were internalising the dawn of a new era of low inflation and high credibility across a wide range of industrial countries in precisely that very same period. This interpretation receives some support from the fact that US long-term bond rates and the implied forward short-term rates were declining as well.

-

[7] Lawrence Christiano and Massimo Rostagno (2001) present a theoretical framework that highlights the role of money in anchoring long-term inflation expectations in “Money Growth Monitoring and the Taylor Rule”, NBER Working Paper No 8539. Lawrence Christiano, Roberto Motto and Massimo Rostagno (2003) discuss the role of money in restoring stability under a liquidity trap situation in “The Great Depression and the Friedman-Schwartz hypothesis,” Journal of Money, Credit and Banking, Vol. 35(6), pp. 1119-1197.

-

[8] The monetary policy implications generated by a heterogeneously informed private sector are discussed in Klaus Adam, (2004), “Optimal Monetary Policy with Imperfect Common Knowledge”, CEPR Discussion Paper No 4594; the value of private sector expectations for a stability-oriented central bank is discussed in Athanasios Orphanides and John Williams (2003), “Inflation scares and forecast-based monetary policy”, Federal Reserve Bank of Atlanta Working Papers No 2003-21.

-

[9] Research at the ECB has derived quantitative estimates from the qualitative survey data. See Magnus Forsells and Geoff Kenny (2002), ‘The Rationality of Consumers’ Inflation Expectations: Survey-Based Evidence for the Euro-Area’, ECB Working Paper No 163.

-

[10] Ongoing research at the ECB aims at quantifying and modelling the risk premium contained in nominal bond yields but it is still too early to draw definite conclusions. See Peter Hördahl, Oreste Tristani and David Vestin (2005), ‘A joint econometric model of macroeconomic and term structure dynamics’, Journal of Econometrics (forthcoming). A recommendation that central banks should carefully monitor private sector expectations is strongly made in George Evans and Seppo Honkapohja (2003), “Adaptive learning and monetary policy”, CEPR Working Paper No 3962.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts