A deep dive into crypto financial risks: stablecoins, DeFi and climate transition risk

A deep dive into crypto financial risks: stablecoins, DeFi and climate transition risk

Published as part of the Macroprudential Bulletin 18, July 2022.

Financial stability risks stemming from crypto-assets are rising, and the crypto-asset ecosystem has become more complex and interconnected. This issue of the Macroprudential Bulletin takes a deep dive into the risks and policy implications of several segments of the crypto-asset market. One central element is stablecoins, whose growth, innovation and increasing global use cases call for the urgent implementation of appropriate regulatory, supervisory and oversight frameworks before significant further interconnectedness with the traditional financial system occurs. Another fast-growing segment within the crypto ecosystem is decentralised finance (DeFi), whose novel way of providing financial services without relying on centralised intermediaries entails specific financial stability risks and regulatory challenges. Lastly, this issue highlights the climate transition risk for the financial sector stemming from the significant carbon footprint of certain crypto-assets like bitcoin and proposes potential measures that can be taken by authorities.

Crypto-assets have been around for more than a decade without playing a significant role in the financial system, but they are growing. In 2008 a software developer or group of developers using the pseudonym Satoshi Nakamoto deployed a source code that created bitcoin, aiming for it to become the first decentralised digital currency.[1] Since then, numerous crypto-assets and a complex and growing ecosystem around them have emerged, spanning subsegments from stablecoins to DeFi and non-fungible tokens (NFTs). Their explosive growth since the end of 2020 and increasing interlinkages with other parts of the financial system have led to an ongoing global policy debate about the relevance and risks of crypto-assets for the financial system.

Financial stability risks from crypto-assets are rising and could reach a systemic threshold. Recent analysis by the Financial Stability Board (FSB) and the ECB suggests that the nature and scale of crypto-asset markets are evolving rapidly. If current trends continue, crypto-assets will pose risks to financial stability. Crypto-asset markets thus need to be effectively regulated and supervised.[2] Dislocations in markets where crypto-assets are used could have spillover effects on regulated financial markets in the absence of timely regulatory intervention. The cross-border and global nature of the ever-growing crypto-asset universe calls for a holistic and coordinated approach among authorities.

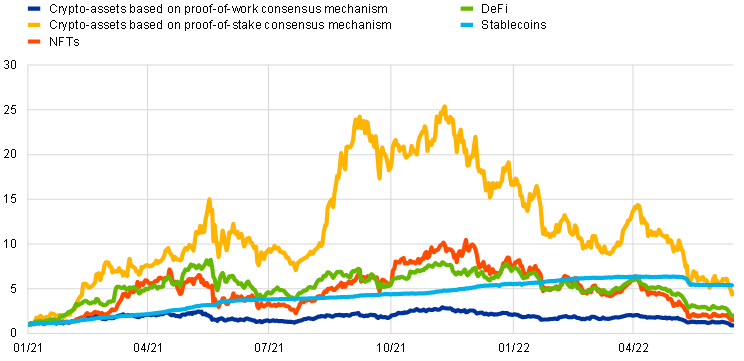

This issue of the Macroprudential Bulletin takes a deep dive into the risks and policy implications of several segments of the crypto-asset ecosystem. While major, unbacked crypto-assets such as bitcoin and ether continue to be the most popular such assets in the crypto universe, further types of crypto-asset have emerged and expanded considerably over the last two years (Chart 1). This has added complexity and new functionality within the crypto-asset ecosystem. Stablecoins, for example, have created further interlinkages by serving as collateral in crypto-asset derivative transactions or as liquidity providers in DeFi. At the same time, interlinkages between the crypto-asset ecosystem and the traditional financial system have grown due to increasing institutional interest.

Chart 1

Market capitalisation-indexed growth of selected segments of the crypto-asset ecosystem

(1 Jan. 2021 = 1)

Sources: CryptoCompare and ECB calculations.

Notes: Crypto-assets based on proof-of-work-consensus mechanism: bitcoin, ether. Crypto-assets based on proof-of-stake-consensus mechanism: Cardano, Solana.

Given stablecoins’ central role within the crypto-asset ecosystem, Adachi et al. (2022) analyse their role in crypto-asset markets and the possible implications for financial stability. Stablecoins are digital units of value that rely on tools to maintain a stable value relative to one or several currencies or other assets (including crypto-assets), or that make use of algorithms to maintain a stable value (so-called algorithmic stablecoins).[3] They were developed to address the high price fluctuations of unbacked crypto-assets such as bitcoin and ether, and their comparatively low price volatility predestines stablecoins for a number of functions where this property is needed. However, events in early May, when the algorithmic stablecoin TerraUSD crashed and the largest stablecoin (Tether) temporarily lost its peg, show that stablecoins may not be so stable after all. Against the backdrop of stablecoins’ rapid growth over the last year and their increasing global use cases and potential financial risk contagion channels, this article focuses on the role played by stablecoins within the wider crypto-asset ecosystem and beyond.

The critical function that some stablecoins serve in the wider crypto-asset ecosystem and for unbacked crypto-assets could have contagion effects for the financial system if at some point in the future unbacked crypto-assets pose a risk to financial stability. Given that the largest stablecoins serve a critical function for crypto-asset markets’ liquidity, this could have wide-ranging implications for crypto-asset markets if there is a run on or failure of one of the largest stablecoins. In turn, this could have contagion effects for the financial system if at some point in the future crypto-asset markets pose a risk to financial stability. A run on a stablecoin could also have contagion effects for the financial system through large-scale redemptions of reserve assets, which usually comprise traditional assets such as government bonds or commercial paper. The developments related to the crash of the algorithmic stablecoin TerraUSD exemplify the contagion within the crypto-asset ecosystem. Amid the ensuing crypto-asset market stress, the price of Tether came under pressure, with the largest stablecoin temporarily losing its peg. Tether faced large outflows of more than 10% of its market capitalisation, which it had to redeem by liquidating reserve assets. Meanwhile, other major collateralised stablecoins have seen small inflows.

Stablecoins fall short of what is required of practical means of payment in the real economy. To date, stablecoins’ transaction speed and cost as well as their redemption terms and conditions have proven inadequate for use in real economy payments. In addition, European payment service providers have not been very active in stablecoin markets thus far, and activities vary considerably between EU Member States.

Appropriate regulatory, supervisory and oversight frameworks need to be implemented urgently, before stablecoins become a risk to financial stability. Financial stability risks from stablecoins in the euro area are currently still limited. However, if growth trends continue at their current pace, this may change in the future. Existing stablecoins need to be brought into the regulatory perimeter with urgency. In the EU, the European Commission’s proposed Markets in Crypto-assets (MiCA) Regulation marks a significant milestone. It is a bespoke regime for the issuance and provision of services related to stablecoins and other crypto-assets and seeks to regulate the crypto-asset ecosystem in a holistic and comprehensive manner, for example by specifying that only e-money institutions and credit institutions are allowed to issue stablecoins and setting authorisation and prudential requirements for crypto-asset service providers. It should be implemented as a matter of urgency.

Another segment of the crypto-asset universe that has expanded rapidly over the last year is DeFi, taken up by Born et al. (2022) in the focus piece of this Macroprudential Bulletin. DeFi represents a novel way of providing financial services. It eliminates traditional centralised intermediaries and relies instead on automated protocols. To a large extent, it does not create novel financial products, but mimics those provided in traditional financial markets through technology-enabled innovation. However, certain features such as how assets are held, how trust is generated and how the system is governed distinguish it from traditional finance. DeFi is in many ways subject to the same vulnerabilities as traditional finance, including those caused by excessive leverage and risk taking, liquidity mismatches and interconnectedness. Its novel technology and method of service provision can however amplify certain vulnerabilities and incur additional specific risks. The crash of the stablecoin TerraUSD in early May exemplifies some of these vulnerabilities, as the size of DeFi measured by the sum of all digital assets deposited in DeFi protocols (“total value locked”) fell strongly in early May.

DeFi needs to be effectively supervised and regulated. The guiding principle of “same business, same risk, same rule” should apply to DeFi. The lack of traditional centralised entry points for regulation and its opaque and anonymous nature pose challenges for policymakers in terms of enforcement and effective regulation and supervision. As vulnerabilities start to build, an internationally coordinated approach is needed to mitigate risks from DeFi. This would entail a careful analysis to disentangle actual regulatory gaps from lack of enforcement. Where regulatory gaps are identified, relevant entry points for regulation as well as regulatory standards are needed.

Gschossmann et al. (2022) deal with climate transition risk in the light of certain crypto-assets’ significant carbon footprint. The functioning of certain crypto-assets (like bitcoin) uses a disproportionate amount of energy that clashes with public and private environmental policies and environmental, social and governance (ESG) objectives. Government intervention is likely. Markets and investors may not correctly price in such an intervention. As a result, climate transition risks are expected to increase in line with the increasing exposure of the financial sector to crypto-assets.

While governments are primarily responsible for policy, financial institutions and prudential standard-setters also have a role to play. Public authorities will have to evaluate whether the outsized carbon footprint of certain crypto-assets undermines their green transition commitments. Investors will have to assess whether investing in certain crypto-assets is in line with their ESG objectives. Financial institutions will have to incorporate the climate-related financial risks of crypto-assets into their climate strategy. For prudential standard-setters, several regulatory options exist to define capitalisation requirements. These range from a risk-sensitive approach in the form of risk-weighted add-ons to a capital deduction approach for all new exposures to crypto-assets with a significant carbon footprint.

References

Adachi, M., Bento Pereira Da Silva, P., Born, A., Cappuccio, M., Czák-Ludwig, S., Gschossmann, I., Paula, G., Pellicani, A., Philipps, S-M., Plooij, M., Rossteuscher, I. and Zeoli, P. (2022), “Stablecoins’ role in crypto and beyond: functions, risks and policy”, Macroprudential Bulletin, Issue 18, ECB, July.

Born, A., Gschossmann, I., Hodbod, A., Lambert, C. and Pellicani, A. (2022), “Decentralised finance – a new unregulated non-bank system?”, Macroprudential Bulletin, Issue 18, ECB, July.

Bullmann, D., Klemm, J. and Pinna, A. (2019), “In search for stability in crypto-assets: are stablecoins the solution?”, Occasional Paper Series, No 230, ECB, August.

ECB Crypto-Assets Task Force (2020), “Stablecoins: Implications for monetary policy, financial stability, market infrastructure and payments, and banking supervision in the euro area”, Occasional Paper Series, No 247, ECB, September.

Financial Stability Board (2022), Assessment of Risks to Financial Stability from Crypto-assets, February.

Gschossmann, I., van der Kraaij, A., Benoit, P-L. and Rocher, E. (2022), “Mining the environment – is climate risk priced into crypto-assets?”, Macroprudential Bulletin, Issue 18, ECB, July.

Hermans, L., Ianiro, A., Kochanska, U., Törmälehto, V-M., van der Kraaij, A. and Vendrell Simón, J.M. (2022), “Decrypting financial stability risks in crypto-asset markets”, Special Feature A, Financial Stability Review, ECB, May.

Nakamoto, S. (2008), A Peer-to-Peer Electronic Cash System, www.bitcoin.org.