Sustainability of recent euro area investment banking strength and debt capital market intermediation

Published as part of the Financial Stability Review, November 2021.

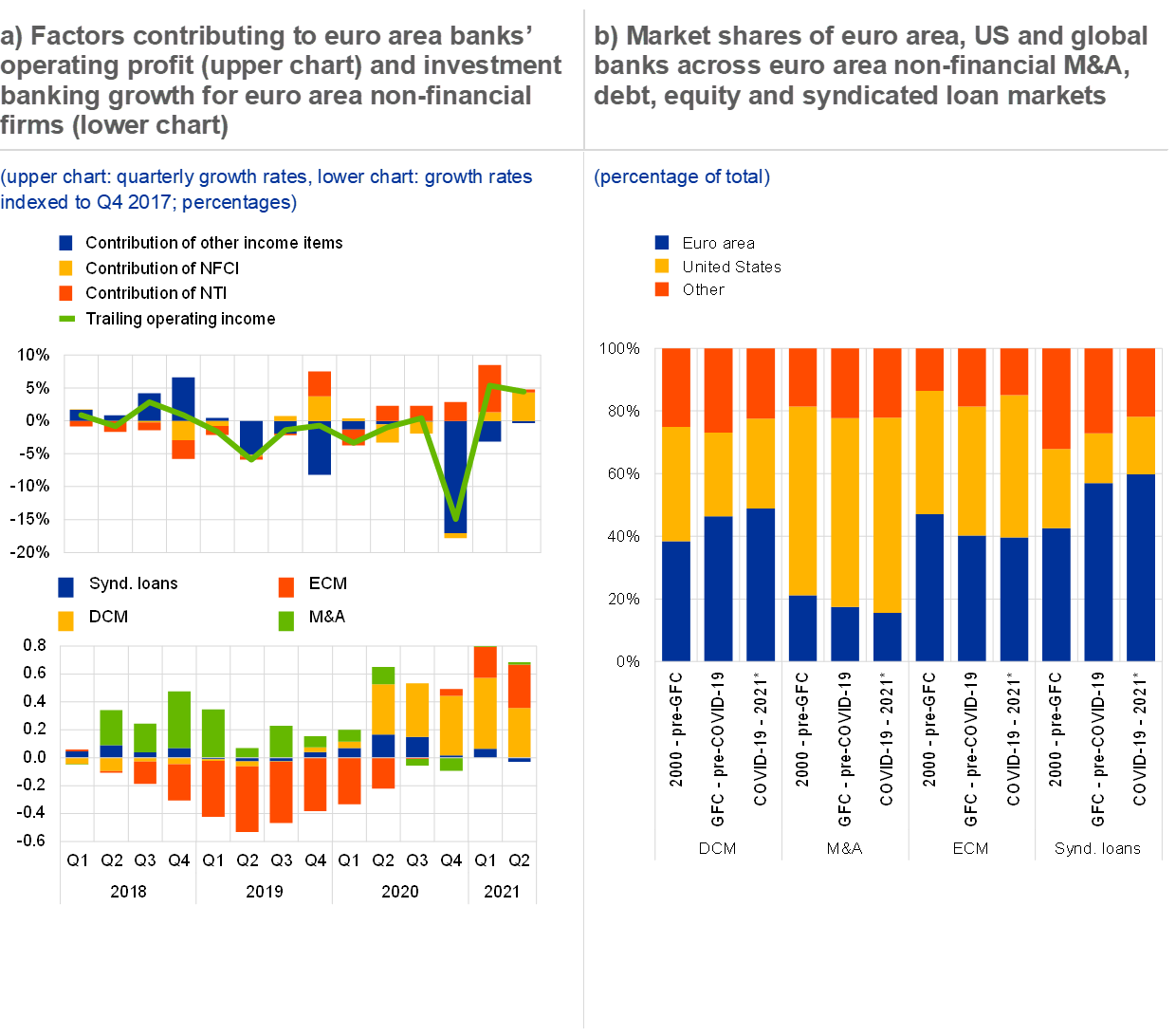

Investment banking revenues have contributed markedly to the recent increase in euro area banks’ non-interest income growth and the rebound in bank profitability (see Chart A, panel a, upper chart).[1] Internationally, in the last three years equity capital market (ECM) revenue has doubled, while debt capital market (DCM) and merger and acquisition (M&A) revenues have increased by around 50%, with only syndicated lending remaining more subdued. In the euro area, however, the most significant volume increase has come from debt instruments, which have long been the preferred source of corporate funding in the euro area, dominating over equity (see Chart A, panel a, lower chart). Despite the international growth in capital market volumes, market commentary before the pandemic suggested that investment banking was a weak aspect of European banking,[2],[3] with many large banks retreating from various market segments as they faced the fallout from the global financial crisis. Against this background, this box considers the recent developments in investment banking of euro area banks in relation to some of the prior trends and considers how sustainable the recent strength might be.

Chart A

Investment banking has been a major driver of higher non-interest operating income since the pandemic, with euro area banks increasing their shares in debt and syndicated loan markets

Sources: Dealogic, Bloomberg Finance L.P. and ECB calculations.

Note: Panel a, upper chart: trailing quarterly operating profit. Panel a, lower chart: seasonally adjusted by taking the four-quarter moving average. Change compared with Q4 2017. Panel b: figures for the latest period include annualised projections for 2021. * - data up to October. DCM: debt capital markets; ECM: equity capital markets; GFC: global financial crisis; M&A: mergers and acquisitions; NFCI: net fee and commission income; NTI: net trading income.

Since the pandemic, euro area banks have increased their market shares in the two segments dominating the European investment banking landscape – debt and syndicated loans. At the same time, despite the recent increase in activity in the equity and M&A markets, euro area banks do not seem to have expanded their market presence. The economic and policy response to the pandemic has enhanced a well-documented increase in debt securities issuance during the past two years, spurred by the need for additional liquidity. Growth in corporate debt issuance in particular has increased the number of opportunities for investment banking arms to earn fees from bookrunning and intermediating related financing, hedging and market-making activities. While corporate debt issuance may slow in the years ahead as economic activity returns to pre-pandemic levels, a higher DCM share may suggest more sustained positive news for euro area banks, especially since other market segments continue to be dominated by non-euro area banks (see Chart A, panel b).

Chart B

Persistent home bias across the largest euro area countries, lower fees per deal and an increase in the number of bookrunners per deal have shaped the debt capital markets over the last decade

Sources: Dealogic and ECB calculations.

Notes: Panel a: bank domicile based on ultimate parent entity, market share based on apportioned deal value in euro, share in non-financial debt capital markets. Panel b: average fee as a share of deal volume, euro area non-financial debt capital markets; * refers to a projection based on deals placed in 2021.

In particular, lower-ranked investment banks have gained market share, perhaps benefiting from home bias in the debt capital markets, the increasing number of bookrunners per deal and broader trends.[4],[5] The debt market share of the top ten banks declined since the early 2000s from nearly 70% in 2001 to 57% currently, and the number of banks active in the debt capital markets has risen. This could reflect many factors. First, as corporate debt issuance has grown, so has the demand for investment banking, while home bias combined with bookrunning trends may have benefited local operators acting as junior partners.[6],[7] For instance, Italian and Spanish banks hold almost 30% of their own debt markets, while their market presence in other euro area countries is much less pronounced. By contrast, US investment banks seem to have achieved a stable presence of between 20% and 30% (see Chart B, panel a). Second, the last decade has also seen a doubling in the share of deals involving five or more bookrunners (see Chart B, panel b). By using multiple bookrunners, debt issuers widen the range of potential investors, which is especially useful as the average tranche size and the number of tranches in deals have increased significantly in recent years. More recently, during the pandemic, banks providing companies with additional liquidity may also have been rewarded for doing so by gaining a place in bond syndicates.[8]

Overall, although euro area investment banking has benefited from the recent boom in debt issuance, margins are under pressure, with few signs of growth in the more profitable equity and M&A activities. Euro area banks have relied heavily on expanding volumes for investment banking revenue growth, as the European debt capital markets generate less fee income per unit of debt issued compared with other capital market segments, reflecting the high share of investment-grade bond issuance in the euro area. Furthermore, while the dispersion of euro area DCM activity across a larger number of bookrunners may be positive for market competition and resilience, it has also weighed on fee income per deal (see Chart B, panel b). Meanwhile, the more profitable – albeit riskier – segments of the euro area capital markets (equity with a 1.6% fee, high-yield bonds with a 1.2% fee and to some extent also M&A activity with a 0.8% fee and leveraged loans with a 0.6% fee[9]) are relatively underdeveloped, and euro area banks operate at higher costs and with less geographical breadth than their global peers. This suggests that there is scope for euro area investment banks to strengthen their revenue base and make the recent upswing momentum in fees and trading income more permanent.

- Investment banking is defined as financial intermediation consisting of financial advisory, primary market and secondary market activities, as well as proprietary trading. See “The Role of Investment Banking for the German Economy”, Zentrum für Europäische Wirtschaftsforschung, October 2011.

- See, for example, the analyst’s report on Société Générale’s earnings for the second quarter of 2021.

- See, for example, “European Investment Banks Face A Continued Fight To Remain Competitive”, S&P Global, September 2020.

- “Can investment banking successfully embrace digitalisation?”, International Banker, March 2021.

- Lower-ranked investment banks are those outside the top ten largest investment banks in the euro area.

- “Too many banks spoil the bond issue”, Nasdaq, March 2021.

- “Arranger, bookrunner, MLA and other roles in financing transactions”, BBVA, June 2018.

- “Corporate Debt: How many investment banks does it take to sell a bond?”, Global Capital, January 2018.

- Source: Dealogic. For high-yield and leveraged loan deals, this reflects the global average fee.