Published as part of the ECB Economic Bulletin, Issue 3/2023.

The recent coronavirus (COVID-19) pandemic and the influx of migrants are leaving a mark on the demographic outlook for the euro area, with implications for the long-term economic outlook. This box reviews the demographic trends derived from the latest EUROPOP2023 population projections, which were published by Eurostat on 30 March 2023. These projections cover the size and structure of the population of all EU Member States for the period 2022-2100. Revisions in the demographic projections are driven by recent changes in birth rates, mortality rates and migration flows. In view of the long-term horizon, the projections are surrounded by a high degree of uncertainty. This box focuses on revisions compared with the previous update of the population projections, which were released in 2019, and their impact on economic growth prospects and fiscal sustainability in the euro area.[1]

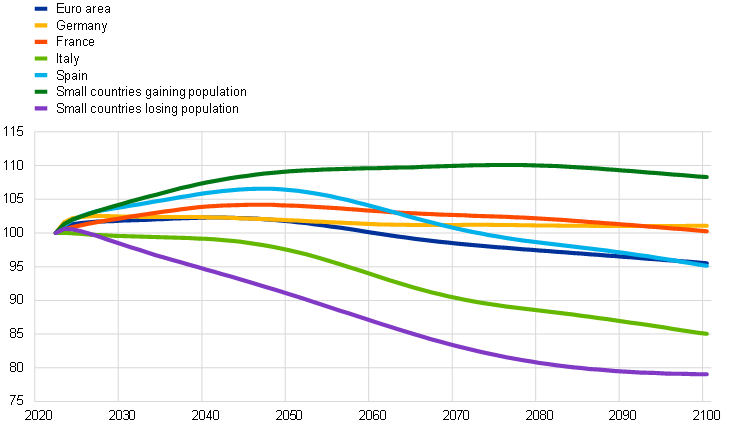

In line with previously expected long-term trends, the euro area’s population is projected to continue ageing and to shrink significantly over the coming generations. According to Eurostat’s updated projections, the euro area population is expected to decrease by 4.5% between 2022 and 2100, equivalent to 16 million fewer people, with the decline particularly pronounced in some countries (Chart A). Owing to the ageing population, the fall in the euro area’s working-age population (persons aged between 15 and 64) will be more severe than that of the overall population. The number of people of working age is expected to drop by 19%, from 221 million in 2022 to 180 million in 2100. This will lead to a rapid increase in the old-age dependency ratio, from 34% in 2022 to around 51% in 2050 and 60% in 2100 – that is, from one elderly person for every three working-age people in 2022 to just under two elderly people in 2100.

Chart A

Demographic projections for the euro area

(index 100 = population in 2022)

Source: Authors’ own calculations based on Eurostat data.

Notes: Demographic outlook based on EUROPOP2023 demographic projections. Total population corresponds to the population on 1 January of each year, as reported in the Eurostat annual demographic statistics data collection. “Small countries gaining population” refers to the population-weighted average of Belgium, Ireland, Cyprus, Luxembourg, Malta, the Netherlands and Austria (these countries’ populations are expected to grow between 2022 and 2100). “Small countries losing population” refers to the population-weighted average of Estonia, Greece, Croatia, Latvia, Lithuania, Portugal, Slovenia, Slovakia and Finland (these countries’ populations are expected to shrink between 2022 and 2100).

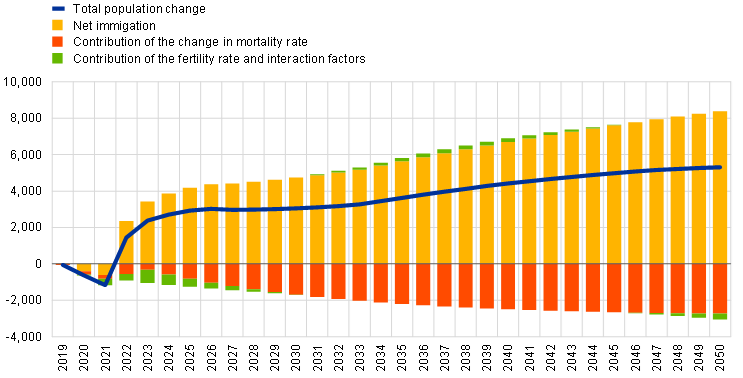

The pandemic and the influx of migrants have affected the demographic outlook for the euro area relative to the 2019 population projections in different ways, with a positive net impact. The euro area population, including Croatia, is projected to rise from 347 million in 2022 to a peak of 355 million in 2041 – four years later than previously projected. The euro area population is now expected to be 0.7% larger in 2025 and 1.4% larger at the 2050 horizon than previously projected. The bulk of revisions in demographic trends is accounted for by much stronger net immigration, from Ukraine and other countries (Chart B). Net migration is projected to normalise by 2025 but remain slightly above the level of the EUROPOP2019 estimates throughout the projection horizon.[2] As most migrants are of working age, this tends to ease demographic pressures on labour supply and public finances. At the same time, the pandemic has significantly increased the mortality rate in euro area countries, particularly among the elderly.[3] These developments outweigh the adverse effect of the pandemic on fertility rates in most countries.[4] Taking into account all the different recent developments, the old-age dependency ratio is projected to improve by 0.6 percentage points by 2025 and 1.4 percentage points (to 51%) by 2050 relative to the 2019 projections. Some euro area countries have benefited more from these recent demographic developments than others (Chart C).[5]

Chart B

Revisions in the demographic outlook for the euro area

(in millions)

Source: Authors’ own calculations based on Eurostat data.

Notes: Revised demographic outlook calculated as the difference between the EUROPOP2019 and EUROPOP2023 demographic projections. The change in total population combines net immigration and the natural population change. The natural population change is the difference between the number of live births and deaths during a given period.

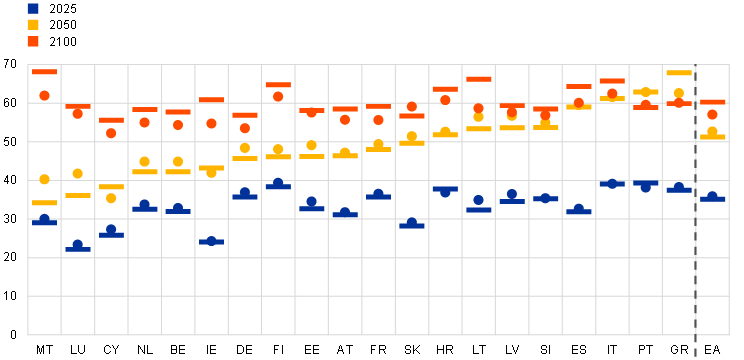

Chart C

Projections for old-age dependency ratios in euro area countries

(percentages)

Source: Authors’ own calculations based on Eurostat data.

Notes: Bars show old-age dependency ratios according to EUROPOP2023 demographic projections. Markers show old-age dependency ratios according to EUROPOP2019 demographic projections. Countries ranked according to the 2050 old-age dependency ratio in the EUROPOP2023 demographic projections. The old-age dependency ratio is defined as the number of persons aged 65 and over per 100 working-age persons (aged 15-64).

The improved demographic outlook relative to EUROPOP2019 is expected to have some positive impact on the growth outlook for the euro area over the next 30 years. An ageing and shrinking population has negative repercussions for the economic outlook through various channels.[6] In particular, it is expected to hold back potential output growth, primarily through a shrinking labour supply and possibly through other components of potential growth like labour productivity growth. A relative increase in the number of older workers within the workforce, combined with an observed hump-shaped profile of age-specific productivity, would yield a downward impact on potential output. However, structural changes, such as a higher share of occupations that can be performed at a higher age, also shift the age-specific productivity profile. Furthermore, as ageing also affects labour productivity via other channels such as physical and human capital accumulation and consumption patterns, the overall impact on aggregate productivity is not clear.[7] The demographic outlook may also have far-reaching implications for the conduct of monetary policy through its impact on the natural rate of interest and inflationary pressures.[8] The somewhat more positive outlook for euro area demographics is expected to alleviate these pressures to some degree.

At the same time, the improved demographic outlook is also likely to ease the cost-of-ageing pressures on public finances. The 2021 Ageing Report shows that age-related expenditure – public expenditure for pensions, healthcare, long-term care and education – is projected to increase by 2.4 percentage points under the reference scenario, from around 24.6% of euro area GDP in 2019 to over 27% in 2050.[9] The rise is mainly due to increased expenditures for health and long-term care, while pension expenditure increases are contained as a result of past pension reforms, including measures reducing the benefit ratio and increasing the retirement age.[10] According to EUROPOP2023, the more benign demographic outlook is expected to somewhat ease the pressure on age-related expenditures. The higher mortality rate stemming from the pandemic had adverse consequences in the short term but will reduce future needs for health and long-term care, as it primarily affected the elderly population. At the same time, the migration of working-age people into EU Member States improves the old-age dependency ratio and reduces the funding pressure on pension systems.

Model-based estimates suggest a small positive impact on potential GDP growth and public finances over the next decades. Results are obtained from running the overlapping generations model of de la Croix and Docquier (2007), calibrated for the euro area with actual historical data and the EUROPOP2019 and EUROPOP2023 projections (Table A).[11] Simulations suggest a gain of around 0.1 percentage points compared with the EUROPOP2019 projections in potential growth per year until 2050 from the path of the population structure embedded in the revised projections. This is mainly driven by the positive impact of net immigration on the labour force. The stronger labour supply, assuming gradual integration of migrants into the labour market, also exerts a minimal downward impact on wage growth. Finally, the change in the population structure has a small favourable impact on pension expenditure, reducing it at a given pension level by 0.2-0.3 percentage points of euro area GDP until 2050.[12]

Table A

Impact of updated projections on annual real GDP growth, wages and pension expenditure

(in percentage points)

Sources: Authors’ own calculations based on de la Croix and Docquier (2007).

Overall, however, a shrinking and ageing European population continues to pose significant challenges to the euro area economy. Labour and pension market reforms should be geared towards increasing the labour force participation rate. At the same time, governments should speed up technological progress and digitalisation, in line with the policies laid down in the national Recovery and Resilience Plans. Higher age-related expenditure and a smaller tax base in the working-age population is likely to put increasing pressure on public finances. In particular, countries that already have vulnerable public finances should refrain from rolling back past pension reforms that have significantly contributed to improving the sustainability of their pension systems. Rebuilding fiscal buffers that declined during the pandemic and energy crisis would contribute to catering for increasing health and long-term care costs.

EUROPOP2023 population projections are deterministically calculated based on the assumption of the continuation of current trends, as well as a partial convergence to the EU average. Revisions are mainly made on account of a function of three demographic events: births, deaths and migratory flows, each of which shapes the population structure over time. Cf. “Population projections in the EU - methodology”, Eurostat (2023). Some revisions may also be on account of changes in the projection methodology.

The upward revision to net immigration is derived from mechanical assumptions based on past migration and motivated by factors including expected migration flows triggered by climate change. For Ukrainians under temporary protection, a gradual return of two thirds of this population over ten years from 2025 onwards is assumed.

With ever-increasing life expectancies, mortality rates have been on a downward trend over time in the EU. COVID-19 caused a sudden, temporary decline in life expectancy in the EU, from 81.3 years in 2019 to 80.1 years in 2021. Cf. “The impact of demographic change in a changing environment”, European Commission, 2023. Mortality rates are assumed to gradually converge to the previous path of declining mortality rates of Eurostat’s EUROPOP2019 projections.

Although fertility rates had largely recovered in most countries by the end of 2021, the latest EUROPOP projections entail smaller increases in fertility rates over the horizon than previously assumed, which are partially compensated over time by the stronger population growth from immigration.

The demographic projections have been revised most favourably for Lithuania, where the population is now projected to grow rather than shrink at the 2025 horizon. By 2050, the population is now expected to increase in Luxembourg by 39% (+20 percentage points) and in Malta by 43% (+15.0 p.p.). In contrast, other countries are now expected to suffer a weaker population dynamic. Cumulative population growth projections over the next 30 years have been revised down to 9% for Cyprus (-7.0 p.p.) and to -14% in Greece (-5.0 p.p.). The change in the demographic outlook is reflected in a somewhat less bleak projection for the old-age dependency ratio in many countries. By 2050, the ratio has been revised down to 34% in Malta (-6.0 p.p.) and 36% in Luxembourg (-5.6 p.p.). At the same time, the projection for the ratio has been revised up to 38% in Cyprus (+3.0 p.p.) and 68% in Greece (+5.3 p.p.).

See the box entitled “The impact of the influx of Ukrainian refugees on the euro area labour force”, Economic Bulletin, Issue 4, ECB, 2022.

See Bodnár., K. and Nerlich., C., “The macroeconomic and fiscal impact of population ageing”, Occasional Paper Series, No 296, ECB, Frankfurt am Main, June 2022.

See Goodhart, C. and Pradhan, M., The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, Palgrave Macmillan, 2020.

European Commission, “The 2021 Ageing Report - Economic & Budgetary Projections for the EU Member States (2019-2070)”, Institutional Paper, No 148, May 2021.

In the meantime, some of the pension reforms included in the 2021 Ageing Report have been reversed and are likely to lead to more pessimistic projections for euro area age-related expenditure in the forthcoming 2024 Ageing Report.

This is a computable general equilibrium model with overlapping generations of individuals. Cf. de la Croix, D. and Docquier, F., “School Attendance and Skill Premiums in France and the US: A General Equilibrium Approach”, Fiscal Studies, Vol. 28, No 4, 2007, pp. 383-416.

After 2060, with the migrants ageing and the effect of lower fertility rates becoming more important, the positive impact from the changed demographic outlook reverses and all impacts switch sign, though gradually.