Published as part of the ECB Economic Bulletin, Issue 8/2022.

On 22 November 2022 the European Commission released its opinions on the draft budgetary plans (DBPs) of euro area countries for 2023.[1] Owing to the continued application in 2023 of the general escape clause of the Stability and Growth Pact (SGP), the assessment by the Commission followed the practice of the two previous years, focusing on the compliance of the DBPs with fiscal policy recommendations that are more qualitative than quantitative in nature.[2] These recommendations were adopted by the Council on 12 July 2022. At that time, the Council also advised euro area countries to adopt differentiated fiscal policies in 2023, in particular recommending countries with high levels of government debt to ensure a prudent fiscal policy. In operational terms, this means keeping the growth in nationally financed primary current expenditure, net of discretionary revenue measures, below the growth in potential output over the medium term. Euro area countries with low or medium levels of government debt were recommended to ensure that the growth in nationally financed current expenditure is in line with an overall neutral policy stance. In both cases, it was recognised that government expenditure plans would need to take into account the ongoing temporary and targeted support for households and firms via energy-related compensatory measures and for people fleeing Russia’s war of aggression against Ukraine. Euro area countries were also advised to expand public investment for the green and digital transitions and for energy security.[3]

In its assessment of whether the budgetary plans for 2023 are in line with the Council’s recommendations, the Commission focused on the compliance of countries with an indicator developed in the context of the coronavirus (COVID-19) crisis which adjusts the SGP expenditure benchmark.[4] First, this indicator takes into account the expenditures financed with EU grants under the Recovery and Resilience Facility (RRF) or with other EU funds. These financing sources provide a fiscal impulse to the economy but are not reflected in the budget balances of euro area countries, given that they are recorded equally as both revenue and expenditure. Second, the indicator nets out temporary emergency measures taken in response to the COVID-19 pandemic. Importantly, the expenditure aggregate underlying the indicator includes expenditure measures adopted in response to the energy crisis as well as nationally financed government investment. The Commission assessed the level of compliance with the Council’s recommendations of 12 July 2022 on the basis of an assessment of developments in these expenditure items.

According to the Commission assessment, the DBPs of euro area countries for 2023 are broadly in line with the fiscal policy recommendations of the Council, with a few exceptions. Among the countries with high levels of government debt, the Commission assessed the DBP of Belgium to be only partly in line with the recommendation, given that the growth in nationally financed current expenditure exceeds potential output growth. For Portugal, the Commission, while providing an overall positive assessment, saw risks of partial compliance should the energy-related compensatory measures not be unwound as planned.[5] Among the group of countries with low or medium levels of government debt, the DBPs of Germany, Estonia, Lithuania, Luxembourg, the Netherlands, Austria, Slovenia and Slovakia were assessed to be partly in line with the recommendation, given the expansionary rather than neutral contributions of their nationally financed net current expenditure to the overall orientation of fiscal policies in 2023.[6] All euro area countries plan to finance public investment for the green and digital transitions and for energy security, including by making use of the RRF and other EU funds, as recommended by the Council.

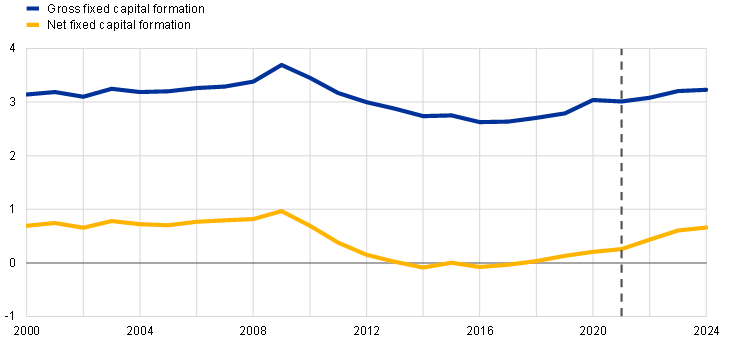

The Commission assessment emphasised the euro area-wide rise in government investment since 2018, which has continued in 2020-22 despite the shocks stemming from COVID-19 and the Russian war in Ukraine. While being moderate in terms of percentage of GDP, the increase in government investment since the pandemic contrasts with the pattern observed in the aftermath of the global financial crisis, when gross government investment declined by more than one percentage point of GDP and net investment – which takes into account the depreciation of the capital stock – turned negative between 2014 and 2017 (Chart A).

Chart A

Euro area public investment, 2000-2024

(percentages of GDP)

Source: European Commission (AMECO database).

Notes: The years 2022-24 are taken from the European Commission’s autumn 2022 forecast. The dashed vertical line indicates the beginning of the forecast horizon.

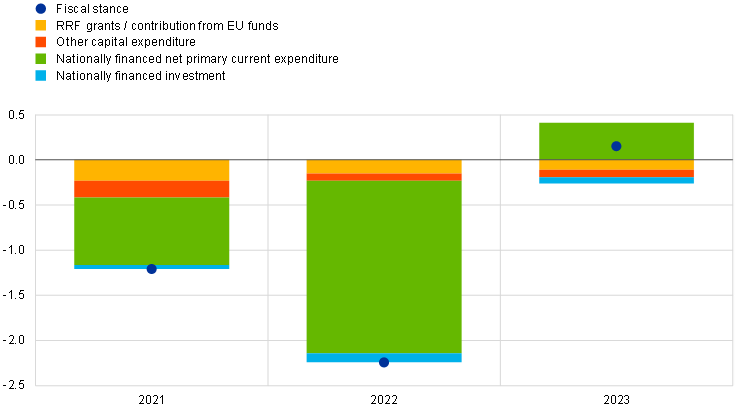

According to the Commission, fiscal policies may become expansionary in 2023 in an environment of still elevated inflation. According to the Commission’s autumn 2022 forecast, which incorporates the DBPs for 2023, the fiscal expansion based on the adjusted indicator described above will amount to around 2.2% of GDP in 2022, while broadly neutral fiscal policies are projected for 2023.[7] The Commission’s projections include a net budgetary impact of 0.9% of GDP from the measures aimed at mitigating the impact of high energy prices on households and firms in the euro area in 2023, down from 1.3% of GDP in 2022. The Commission also estimated that, if existing measures were extended throughout 2023, their cost could increase by an additional 1% of GDP, reaching close to 2% of GDP in 2023, thus rendering fiscal policies more expansionary.

The latest Eurosystem staff projections include a significantly larger amount of energy-related support measures than in the Commission’s baseline, pointing to an expansionary fiscal stance in 2023. The aggregate euro area energy support, as embedded in the macroeconomic outlook of the December 2022 Broad Macroeconomic Projections Exercise (BMPE), is estimated at around 2% of GDP. [8] This is significantly larger than projected by the Commission in its autumn 2022 forecast and reflects, among other things, a later cut-off date for projections, whereby more support measures are sufficiently specified to fulfil the criteria for consideration in the December BMPE fiscal assumptions.[9]

Chart B

Commission assessment of fiscal policy orientation, 2021-23

(percentages of GDP)

Source: European Commission (AMECO database).

Notes: For its assessment of the euro area fiscal stance, the Commission used the adjusted expenditure benchmark approach explained in the text. A negative (positive) figure points to an expansionary (contractionary) stance.

To ensure that fiscal policies do not add to inflationary pressures while safeguarding debt sustainability and supporting the growth-friendliness of public finances, it is important that policies are targeted, tailored and temporary. From a monetary policy viewpoint, energy support measures need to be further adjusted in accordance with these “three Ts”, i.e. the measures should be (i) targeted to the most vulnerable so that the size of the fiscal impulse is limited and benefits those who need it most, (ii) tailored so that measures do not weaken incentives to cut energy demand, and (iii) temporary so that the fiscal impulse is maintained no longer than strictly necessary. Given the expected deactivation of the SGP’s general escape clause as of 2024, a timely agreement on a reform of the EU economic governance framework will be essential as it will help orient fiscal policies going forward.[10] Overall, a gradual, realistic and sustained reduction of public debt where needed should be combined with an improved quality of government budgets and sustained public investment to support potential growth as well as the green and digital transitions.

See “Communication from the Commission to the European Parliament, the Council and the European Central Bank on the 2023 Draft Budgetary Plans: Overall Assessment”, European Commission, 22 November 2022; and “Recommendation for a Council Recommendation on the economic policy of the euro area”, European Commission, 22 November 2022. The DBPs of Italy and Latvia were submitted by the outgoing governments on a “no policy change” basis and were therefore not assessed by the Commission at the time of its autumn package. Following submission of the update on 21 November 2022, the Commission published its opinion on the Italian DBP on 14 December 2022.

The general escape clause was introduced as part of the “six-pack” reform of the SGP in 2011. It can be activated in the case of an unusual event outside the control of the Member State concerned which has a major impact on the financial position of the general government, or in periods of severe economic downturn for the euro area or the EU as a whole. When the clause is activated, Member States may temporarily depart from the fiscal adjustment requirements under both the preventive and corrective arms of the Pact, provided this does not endanger fiscal sustainability in the medium term.

In addition to the Council’s Recommendations, in its statement of 11 July 2022 on fiscal policy orientations for 2023, the Eurogroup considered that, for the euro area, supporting overall demand through fiscal policies in 2023 was not warranted in view of the prevailing economic circumstances, notably the inflationary dynamics.

The Commission computes this indicator capturing the orientation of fiscal policies by gauging the annual increase in net expenditure relative to ten-year potential growth and the growth rate of the GDP deflator. Following the Council’s recommendations on the 2021 stability programmes, the underlying net expenditure aggregate was adjusted to include expenditure financed by RRF grants and other EU funds and to exclude the temporary emergency measures related to the COVID-19 crisis. In addition to the contribution from EU-financed expenditure, the Commission’s assessment includes the contributions to the overall fiscal stance from different nationally financed expenditure aggregates, namely (i) investment, (ii) other capital expenditure and (iii) current primary expenditure (net of discretionary revenue measures). This indicator differs from the measure that has traditionally been used to assess the fiscal stance within the European System of Central Banks (ESCB) based on the concept of the cyclically adjusted primary balance (see Section 6 of this issue of the Economic Bulletin).

Given the overall assessment by the Commission of the DBP of Portugal, the Eurogroup statement on draft budgetary plans for 2023 – issued on 5 December 2022 – emphasised the progress made by Portugal in terms of deficit and debt reduction.

According to the Commission analysis, in the case of the Netherlands, while the contribution of nationally financed primary current expenditure to the fiscal stance is broadly neutral, the overall orientation of fiscal policies is expansionary.

See Section 2 on the fiscal outlook in the “December 2022 Eurosystem Staff Macroeconomic Projections”.

The projections for fiscal variables in the BMPE are carried out under the responsibility of the Working Group on Public Finance. The fiscal projections are fully consistent with the macroeconomic projections and take into account the most recent information, for example the latest data releases, budget laws, supplementary budgets, and stability and convergence programmes. The fiscal projections incorporate only those measures that have been approved by national parliaments or that have already been defined in sufficient detail and are likely to pass the legislative process. For more information, see ECB, “ A guide to the Eurosystem/ECB staff macroeconomic projection exercises” July 2016.

See “Communication on orientations for a reform of the EU economic governance framework”, European Commission, 9 November 2022.