Employment growth and GDP in the euro area

Published as part of the ECB Economic Bulletin, Issue 2/2019.

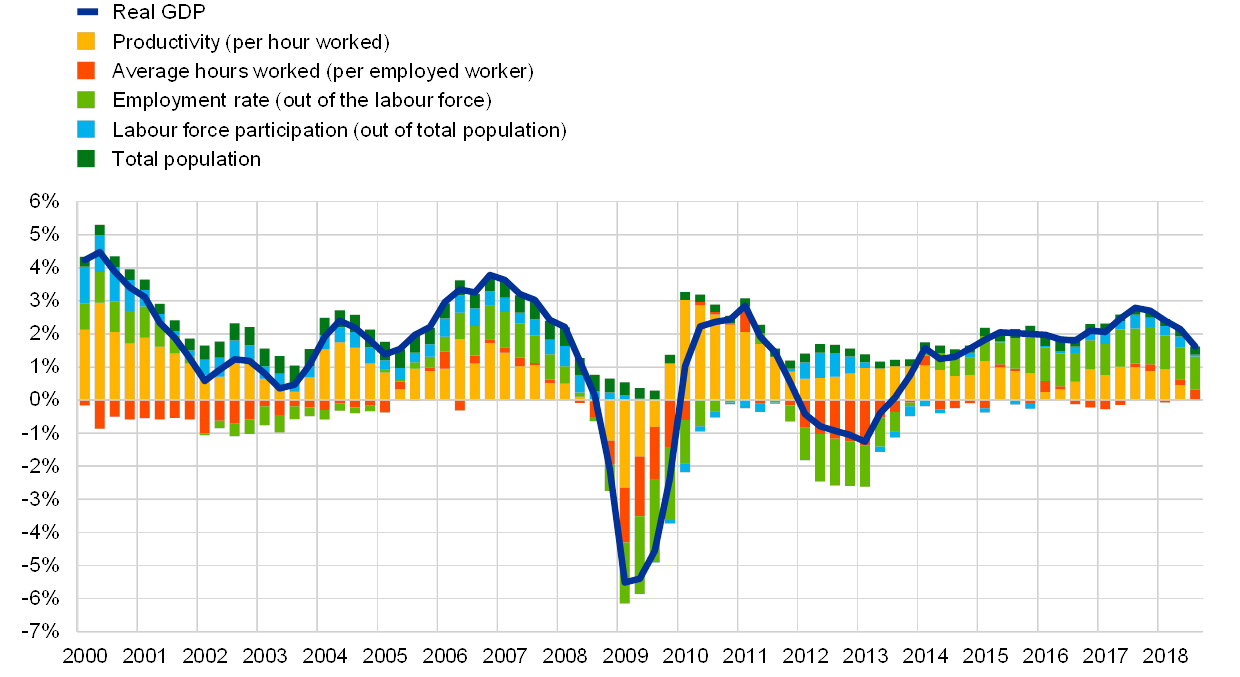

This box analyses developments in the euro area labour market with respect to recent changes in GDP growth. The labour market remained relatively robust throughout 2018, in spite of the slowdown in real GDP growth. A decomposition of GDP into labour productivity, labour market outcomes and demographic trends shows a larger contribution to real GDP growth from employment (see Chart A). In the first three quarters of 2018, economic growth was strongly supported by employment growth and by the stable decline in the unemployment rate. These developments contrast sharply with trends during the early period of the recovery and highlight the strength of the labour market in the euro area against the background of the slowdown in GDP growth in 2018. Indeed, despite the considerable heterogeneity observed across different euro area countries, the aggregate euro area unemployment rate was, in December 2018, at its lowest since October 2008, with the employment-to-population ratio higher than in 2008[1].

Chart A

Decomposition of real GDP growth

(percentages, year-on-year growth rates)

Sources: Eurostat and ECB staff calculations.

Notes: Real GDP is decomposed into labour productivity (real GDP/total hours worked), average hours worked per employed worker, employment rate (total employment/labour force), labour force participation rate (labour force/population) and total population. The labour force is defined as the sum of employed and unemployed workers.

An estimated simple static relationship between employment/unemployment and GDP illustrates the good labour market performance since the beginning of the recovery in the euro area (see Chart B). Employment growth was 0.4 percentage point above its expected level at the end of 2018, based on a long-term static relationship between employment and GDP growth. These positive employment residuals since the start of the recovery became even more accentuated in the last three quarters of 2018, as the year-on-year GDP slowdown was not accompanied by a proportionate deceleration in employment growth. The positive residuals are also translated into positive residuals of growth in total hours, i.e. total hours have grown by more than would be expected given the rate of GDP growth. Similarly, the unemployment rate also indicates a strong labour market performance, trending below its expected value, as estimated by the traditional static Okun’s law. The observed strength of the labour market is broad-based across countries[2], with the Okun relationship consistently showing a stronger than expected labour market performance, which may be due to structural reforms that contributed to higher employment creation during the recent economic recovery[3].

Chart B

Residuals from static Okun estimates

(percentage points)

Sources: Eurostat and ECB staff calculations.

Notes: Estimates based on data for the period between the first quarter of 1998 and the third quarter of 2018. Residuals from a static Okun relationship that relates the year-on-year changes in the unemployment rate, the year-on-year growth rate in total employment and the year-on-year growth rate in total hours to the contemporaneous year-on-year growth rate in real GDP.

However, the current labour market performance will be dependent on the nature of the shocks affecting the observed slowdown in real GDP. A static Okun approach conveys a long-term relationship between real GDP growth and labour market outcomes, ignoring both short-run and long-run dynamics on the adjustment of the labour market to fluctuations in the business cycle. Allowing for a dynamic specification to assess the time profile between real GDP growth and labour market outcomes would show that the labour market performance depends not only on current changes in real GDP growth but also on past GDP innovations[4]. In addition, as the implied Okun elasticities are below unity, fluctuations in real GDP growth might imply a somewhat protracted and mitigated response of total employment, the unemployment rate and total hours. Moreover, the current strong labour market performance and its subsequent path could also be affected by the specific nature of the shocks hitting the economy.

Overall, these results highlight the strong labour market dynamics since the beginning of the recovery and underline the recent robustness of the labour market in the face of the recent slowdown in real GDP in 2018. Indeed, while GDP growth decelerated by 0.7 percentage point during 2018, employment growth decelerated only by 0.2 percentage point, with the static Okun residuals becoming even more negative for unemployment and more positive for employment and total hours. However, the labour market is also characterised by a protracted response to changes in GDP, and that will be one of the various factors influencing how the labour market evolves in subsequent quarters.

- Heterogeneity in unemployment rates remains high, as more than 15 percentage points separate the highest and lowest rates of euro area countries. The employment-to-population ratio, defined here as total employment divided by the segment of the population aged 15-74, increased by 0.8 percentage point, from 58.7% to 59.5%, between the third quarter of 2008 and the third quarter of 2018.

- The exceptions for the third quarter of 2018 are: Italy, with negative employment residuals but positive total hour and negative unemployment rate residuals; Estonia, with negative employment and total hour residuals but positive unemployment rate residuals; and Malta, with positive employment, total hour and unemployment rate residuals.

- See, for example, the box entitled “Recent employment dynamics and structural reforms” in the article “The employment-GDP relationship since the crisis”, Economic Bulletin, Issue 6, ECB, 2016, and the box entitled “Labour and product market regulation, worker flows and output responsiveness” in “Structural policies in the euro area”, Occasional Paper Series, No 210, ECB, June 2018.

- See the box entitled “A quantitative investigation of the euro area employment-GDP relationship” in “The employment-GDP relationship since the crisis”, Economic Bulletin, Issue 6, ECB, 2016.