Published as part of the ECB Economic Bulletin, Issue 1/2023.

This box analyses how the increase in energy prices since autumn 2021 has affected euro area aggregate industrial production and import volumes. In autumn 2021 gas supplies from Russia to the European Union (EU) were cut significantly, contributing to the slow replenishment of gas inventories in Europe ahead of the winter season. Between September 2021 and October 2022 average euro area consumer and producer energy prices increased by 49.5% and 93.4% respectively. In the same period euro area industrial production excluding construction and import volumes excluding energy grew by 2.3% and 10.3% respectively. This box shows that the adverse energy supply shocks have been offset by a simultaneous easing of supply bottlenecks, a related workout of backlog orders and recovering demand which benefited from the effects of reopening following the coronavirus (COVID-19) pandemic. There are signs that imports, particularly of intermediate goods, partly replaced domestic manufacturing production in more energy-intensive sectors, as imports were relatively cheap compared to domestic production.

A decomposition into high and low energy-intensive goods shows that, while domestic production of high energy-intensive goods weakened from the second quarter of 2022, imports of the same goods picked up before stabilising at the end of the year. These developments are in line with the expectation that adverse energy supply shocks raise production costs, which can cause a drop in output and an increase in imports from countries that are less dependent on global energy production. The decline in output of euro area energy-intensive manufacturing started in mid-2022 (Chart A, panel a), while manufacturing imports of energy-intensive goods from outside the euro area started to increase around one year earlier (Chart A, panel b).[1] Euro area countries imported more in sectors relatively more exposed to increases in energy prices from trade partners that were less affected by the energy price shock. For instance, the chemical industry in Germany reportedly started importing ammonia in mid-2022 rather than producing it itself, owing to the high volume of gas required in its production.

Chart A

Euro area industrial production and imports

a) Manufacturing industrial production by sub-sector

(percentage changes in industrial production and percentage point contributions relative to January 2020)

b) Manufacturing import volumes by sub-sector

(percentage changes in import volumes and percentage point contributions relative to January 2020)

Sources: Eurostat, Trade Data Monitor and ECB staff calculations.

Notes: Data are seasonally-adjusted. Industrial production indices for individual sectors are aggregated with value-added weights. Imports are computed from volume indices of manufactured goods imports and import shares at the sectoral level. Low (high) energy-intensity sectors are defined as those with an energy intensity lower (higher) than that of the median sector. Energy intensity is calculated as energy inputs (direct and indirect) as a percentage of total inputs. The identified energy-intensive manufacturing sub-sectors are manufacture of food, beverages and tobacco products; manufacture of wood and products of wood and cork (except furniture); manufacture of paper and paper products as well as reproduction of recorded media; manufacture of chemicals and chemical products; manufacture of rubber and rubber products; manufacture of other non-metallic mineral products; and manufacture of basic and fabricated metals. Manufacture of coke and refined petroleum products is excluded as it is part of the energy industrial grouping. Latest observations are for October 2022.

Besides energy costs, factors such as the recovery in demand, the easing of supply chain disruptions and the resulting increase in import competition have played a key role in the dynamics of domestic production and imports since mid-2022. The rise in energy prices was not the only cause of the sharp rise in import volumes. In particular, supply chain disruptions eased, thanks to the logistical improvement in global container vessel activity and the easing of pandemic lockdown measures in some Asian countries exporting intermediate inputs.[2] For instance, in the ECB’s Corporate Telephone Survey, non-financial companies operating in the chemical and metal sectors reported increased import competition following the recent easing of global freight prices and logistical disruptions. The reduction of supply chain disruptions has been a key factor behind the resilience of industrial production as well as the rise in import volumes. The output increases in sectors with lower energy intensity (Chart A, panel a) suggest that the recovery in demand and the easing of supply bottlenecks supported production and imports in 2022. At the same time, energy-intensive production sectors faced much higher energy costs in 2022, and this was behind the drop in output.

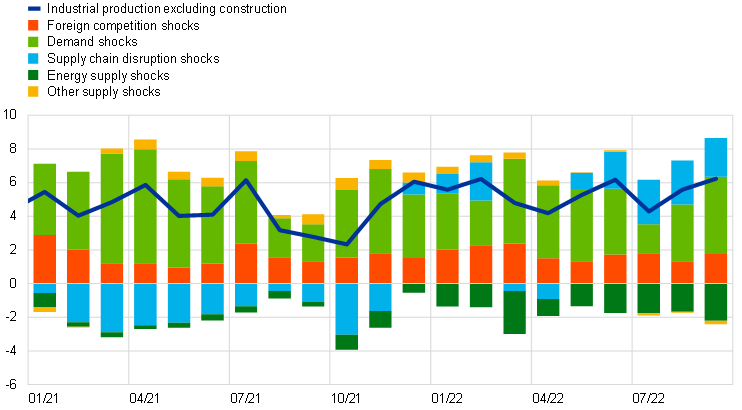

Empirical analysis confirms that energy supply issues and bottlenecks in production processes played a key role in the developments in aggregate industrial production and aggregate import volumes (excluding energy) in 2022. We use a structural vector autoregression (SVAR) model to quantify the relative role of energy and foreign competition shocks in comparison to other key shocks, such as demand, supply chain disruption and other cost-push shocks. The analysis uses the Harmonised Index of Consumer Prices (HICP), industrial production (excluding construction), Purchasing Managers’ Index (PMI) suppliers’ delivery times, consumer energy prices and import volumes of goods excluding energy. A foreign competition shock is defined here as a shock that increases import volumes and lowers domestic production and prices. According to the model, on aggregate industrial production reacts rapidly and negatively to energy shocks, while there is a marginal positive impact on non-energy import volumes in the short term. The results suggest that adverse energy supply shocks reduced industrial output by about 2% between September 2021 and September 2022 (Chart B, panel a). This decline was partly offset by imports of cheaper non-energy foreign goods, which increased by 1.4% as a result of the energy shock over the same period (Chart B, panel b). Conversely, the downward impact of supply chain disruptions on industrial production declined substantially in the first half of 2022, and the subsequent easing of bottlenecks contributed positively and strongly to the output expansion and the rise in import volumes in the second half of 2022. Demand forces, driven by households’ desire to spend after pandemic-related restrictions were eased, also contributed positively to industrial production and imports in 2022.

Chart B

Contributions of factors to euro area aggregate industrial production and import volumes excluding energy

a) Euro area industrial production excluding construction

(percentage deviation from baseline, cumulative from October 2020 to September 2022)

b) Euro area manufacturing import volumes (excluding energy)

(percentage deviation from baseline, cumulative from October 2020 to September 2022)

Sources: Eurostat and ECB staff calculations.

Notes: The model is based on euro area aggregate data from January 1999 to September 2022 and the shocks are identified using the method employed in Antolín-Díaz, J. and Rubio-Ramírez, J.F., “Narrative Sign Restrictions for SVARs”, American Economic Review, Vol. 108, No 10, October 2018, pp. 2802-2829; but with sign contribution restrictions as in De Santis, R.A. and Van der Veken, W., “Deflationary financial shocks and inflationary uncertainty shocks: an SVAR investigation”, Working Paper Series, No 2727, ECB, September 2022. The assumed sign restrictions at impact are as follows: demand shocks imply HICP (+), HICP energy (+), industrial production (+), import volumes (+) and PMI suppliers’ delivery times (-); energy supply shocks imply HICP (+), HICP energy (+), industrial production (-) and PMI suppliers’ delivery times (-); supply chain disruption shocks imply HICP (+), industrial production (-) and PMI suppliers’ delivery times (-); other supply shocks imply HICP (+) and industrial production (-); foreign shocks imply HICP (-), industrial production (-) and import volumes (+). The assumed narrative restrictions are as follows: the largest contribution to forecast errors in the PMI suppliers’ delivery times in April 2020 is attributed to supply chain disruption shocks; the largest contribution to forecast errors in HICP energy in October and November 2021 is attributed to energy supply shocks. It is also assumed that demand shocks have a negative sign in March and April 2020. Production and import volumes represent overall euro area numbers, including both high and low energy-intensive sectors.

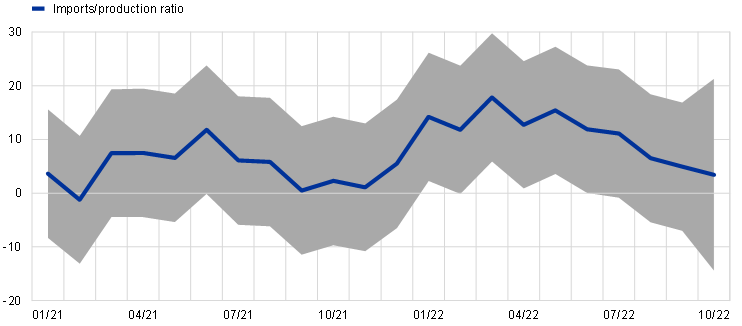

Sectoral analysis shows that producers in energy-intensive sectors started substituting own production with cheaper imports in early 2022. Energy-intensive producers have reduced their output and substituted it with imports since the beginning of 2022, broadly coinciding with the start of the Russian invasion of Ukraine. However, on average this effect came to an end in autumn 2022 (Chart C), albeit with heterogeneity across sectors.[3] These developments are not due to favourable energy supply shocks at the end of the period under consideration, as energy prices continued to rise until October 2022, but to the response of the variables to the energy shocks in the medium term. These findings are in line with the results obtained with the SVAR, according to which, while energy shocks have stronger effects on industrial production than non-energy imports on aggregate in the short term, they have similar effects in the medium term. The imports/production ratio in energy-intensive sectors increased on average by 11% compared to non-energy-intensive sectors in 2022 as energy producer prices rose. The rise in domestic production costs associated with more expensive energy seems to be behind the substitution with cheaper imports.

Chart C

Imports/industrial production ratio of energy-intensive sectors over time

(percentage difference from non-energy-intensive sectors)

Sources: Eurostat, Trade Data Monitor and ECB staff calculations.

Notes: 19 euro area countries and 21 sectors, excluding energy. Event study comparing the imports/production ratio in high energy-intensive sectors (treatment group) to low energy-intensive sectors (control group). The reference month is January 2019. The grey area represents the 95% significance bands. Latest observations are for October 2022.

Econometric evidence confirms that imports tend to substitute domestic production when energy costs are high. A sectoral analysis suggests that manufacturing output growth in the euro area tends to decline relative to import growth if energy costs are high.[4] This indicates that imports partly replaced domestic output in sectors where energy costs increased. Using this estimate and the empirical percentile distribution according to their respective energy cost index, the sectors experiencing the largest negative correlation between production and imports are the most energy-intensive sectors, such as non-energy producing mining and quarrying activities, chemicals, non-metallic mineral products, basic metals and paper industries (Chart D), particularly since mid-2021 when energy costs rose in an unprecedented way.

Chart D

Marginal effects of imports on production in industries with different energy intensities (the higher the percentile, the higher the energy intensity)

(x-axis: percentile of energy cost increase; y-axis: correlation coefficient)

Sources: Eurostat, Trade Data Monitor and ECB calculations.

Notes: Results from a panel regression with 2-digit sectors in euro area countries, where output volume growth is regressed on its lags, contemporaneous sector-country level and lags of import growth, an index for energy costs (change in country-level energy prices times sector-country level energy intensity), its interaction with import growth and a set of fixed effects (country-sector and country-time). Dotted lines represent 95% significance bands.

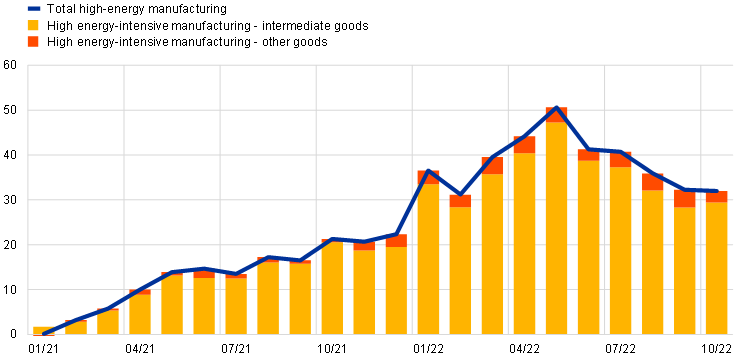

Import substitution implies a net loss of intermediate domestic output, but it helps to maintain production of final products thanks to cheaper inputs. Importing final products rather than producing them domestically should have a negative effect on net exports and value added. However, importing intermediate products helps companies to continue to produce final products domestically and therefore limits the negative impact of the energy price rise. The net effect on euro area economic activity depends on the type of substituted goods: final or intermediate. The more downstream the imported products are, the larger the loss of economic activity is likely to be because a larger fraction of the goods production is moved abroad. Chart E shows that developments in energy-intensive imports in energy-intensive sectors were mostly driven by intermediate products, suggesting that import substitution contributed to the resilience of domestic output.

Chart E

High energy-intensive manufacturing imports by type of product

(percentage changes in import volumes and percentage point contributions relative to January 2020)

Sources: Eurostat, Trade Data Monitor and ECB staff calculations.

Notes: Data are seasonally-adjusted. Imports are computed from volume indices of manufactured goods imports and import shares at the sectoral level. Low (high) energy-intensity sectors are defined as those with an energy intensity lower (higher) than that of the median sector. Energy intensity is calculated as energy inputs (direct and indirect) as a percentage of total inputs. The identified energy-intensive manufacturing sub-sectors are manufacture of food, beverages and tobacco products; manufacture of wood and products of wood and cork (except furniture); manufacture of paper and paper products as well as reproduction of recorded media; manufacture of chemicals and chemical products; manufacture of rubber and rubber products; manufacture of other non-metallic mineral products; and manufacture of basic and fabricated metals. Manufacture of coke and refined petroleum products is excluded as it is part of the energy industrial grouping. Latest observations are for October 2022.

Energy intensity is calculated for each sector in each country as the energy used as a (direct and indirect) input as a percentage of total inputs, using the OECD input-output database. See the box entitled “Natural gas dependence and risks to euro area activity”, Economic Bulletin, Issue 1, ECB, 2022.

For a detailed analysis of these factors and their economic impact, see Lane, P.R., “Bottlenecks and monetary policy”, The ECB Blog, ECB, 10 February 2022; and the boxes entitled “Supply chain bottlenecks in the euro area and the United States: where do we stand?”, Economic Bulletin, Issue 2, ECB, 2022; “What is driving the recent surge in shipping costs?”, Economic Bulletin, Issue 3, ECB, 2021; “The semiconductor shortage and its implication for euro area trade, production and prices”, Economic Bulletin, Issue 4, ECB, 2021; “The impact of supply bottlenecks on trade”, Economic Bulletin, Issue 6, ECB, 2021; and “Sources of supply chain disruptions and their impact on euro area manufacturing”, Economic Bulletin, Issue 8, ECB, 2021.

Chart C shows the estimated computed using the following econometric specification: , where the dependent variable is the natural logarithm of the imports/production ratio. The treatment (control) group features all the sectors above (below) the median in term of energy intensity (direct and indirect) in the production process. The econometric model controls for the average imports/production ratio of the sector in each country using country-sector fixed effects and for country-specific shocks using country-month fixed effects. The database includes 21 manufacturing sectors (excluding energy) and 19 euro area countries.

Output volume growth is regressed on its lags, contemporaneous sector-country level and lags of import growth, an index for energy costs (change in country-level energy prices times sector-country level energy intensity), their interaction and a set of fixed effects (country-sector and country-time). Results are robust to the use of alternative sets of fixed effects, such as time and country-sector, country-time and sector-time, and to the inclusion of proxies for country-level demand (e.g. European Commission production expectations and PMI orders series) and relative prices of imports and production. The panel includes 22 sectors in each of the 19 euro area countries from January 2015 to September 2022.