Market infrastructures, together with markets and institutions, constitute one of the three core components of the financial system. The market infrastructure for payments[1] consists of the set of instruments, networks, rules, procedures and institutions that ensure the circulation of money. Its purpose is to facilitate transactions between economic agents and to support efficient resource allocation in the economy.

The Eurosystem has the statutory task of promoting the smooth operation of payment systems. This is crucial for a sound currency, the conduct of monetary policy, market functioning and financial stability. A key instrument which the Eurosystem uses for carrying out this task is the provision of payment settlement facilities.[2]

To this end, in 1999 the Eurosystem created the Trans-European Automated Real-time Gross settlement Express Transfer system[3] (TARGET) for the settlement of large-value payments in euro, offering a central bank payment service across national borders in the European Union (EU).

TARGET was developed to meet three main objectives:

- provide a safe and reliable mechanism for the settlement of euro payments on a real-time gross settlement (RTGS) basis;

- increase the efficiency of inter-Member State payments within the euro area;

- serve, most importantly, the needs of the Eurosystem’s monetary policy.

In May 2008 TARGET2 replaced the first-generation system, TARGET. Like its predecessor, TARGET2 is used to settle payments connected with monetary policy operations, as well as interbank payments, customer payments exchanged between banks, and transactions related to other payment and securities settlement systems, i.e. ancillary systems. As TARGET2 provides intraday finality, meaning that settlement is final for the receiving participant once the funds have been credited, it is possible to reuse these funds several times a day.

Since June 2015 TARGET2 participants have been able to open dedicated cash accounts (DCAs) on the TARGET2-Securities (T2S) platform[4], which they can use to settle the cash leg of their securities transactions. In addition, since November 2018 TARGET2 participants have been able to open DCAs for TARGET Instant Payment Settlement (TIPS).[5] TIPS is the service implemented by the Eurosystem for settling euro-denominated instant payments on an individual basis, around the clock.

Building on the synergies between the two market infrastructures, the Eurosystem has been working intensively to consolidate TARGET2 and T2S services. The project brings technical as well as functional enhancements. It allows changing market requirements to be met by replacing TARGET2 with a new RTGS system called T2 and it allows liquidity management to be optimised across all TARGET services. The new RTGS system will provide the market with enhanced and modernised services, which will also be available for currencies other than the euro. The messaging standard will migrate to ISO 20022, as for T2S and TIPS. In addition, the project will further strengthen cyber resilience capabilities and establish a single point of access to all Eurosystem market infrastructure services. It will support multi-vendor connectivity, thus allowing participants to choose between different connectivity options and fostering competition among network service providers.

TARGET2 offers harmonised market infrastructure services at EU level, as well as a single pricing structure. It provides ancillary systems with a harmonised set of cash settlement services and supports its users with enhanced liquidity management tools. In this manner, it contributes to financial integration, financial stability and liquidity efficiency in the euro area.

TARGET2 is accessible to a large number of participants. Approximately 1,000 credit institutions in Europe use TARGET2 to make payments on their own behalf, on behalf of other (indirect) participants or on their customers’ behalf. Taking branches and subsidiaries into account, over 43,000 banks worldwide (and thus all of the customers of these banks) can be reached via TARGET2.

The report and its structure

This report is the 22nd edition of the TARGET Annual Report. The first edition was published in 2001, covering TARGET’s first two years of operation (1999 and 2000). As in previous years, the report provides information on TARGET2 traffic, its performance and the main developments that took place in 2021. It is aimed mainly at decision-makers, practitioners and academics who need to have an in-depth understanding of TARGET2. We hope it will also appeal to members of the general public with an interest in market infrastructure issues and, in particular, TARGET2.

In addition to the core content, this report includes seven boxes on topics of particular relevance in 2021. The boxes focus, respectively, on the evolution of traffic in TARGET2; the update on TIPS pan-European reachability measures; the international perspective on cross-border payments in TARGET2; indirect participation in TARGET2; the external review carried out by Deloitte on incidents that affected TARGET services in 2020; an update on the TARGET2/T2S consolidation project and future RTGS services; and operational communication to TARGET2 participants.

In the report, references made to the first-generation TARGET system (which was in operation from January 1999 to May 2008) are also applicable to its second generation, TARGET2 (which replaced TARGET in May 2008).

Note

Liquidity transfers between TARGET2 and T2S/TIPS DCAs and payments processed on T2S/TIPS DCAs are not included in the TARGET2 indicators presented in this report.

Although both T2S and TIPS DCAs are legally part of TARGET2, these (technical) transactions are excluded from the calculations to prevent the system’s indicators from being artificially inflated and to make the figures more easily comparable from year to year. Nevertheless, as a matter of transparency, some general statistics on T2S and TIPS DCAs are provided on the ECB’s website.[6]

TARGET2 activity

In 2021 TARGET2 maintained its leading position in Europe, processing 90% of the total value settled by large-value payment systems in euro. TARGET2 also remained one of the largest payment systems worldwide. Compared with the previous year, the total turnover processed increased by around 4%, reaching €484.3 trillion.[7] The total volume of payments grew by 8.7% to 96.4 million transactions.

The highest daily turnover during the year was recorded on 24 December, with a total value of €2,772 billion, and the highest daily volume of payments was recorded on 6 April, when 580,290 transactions were processed.

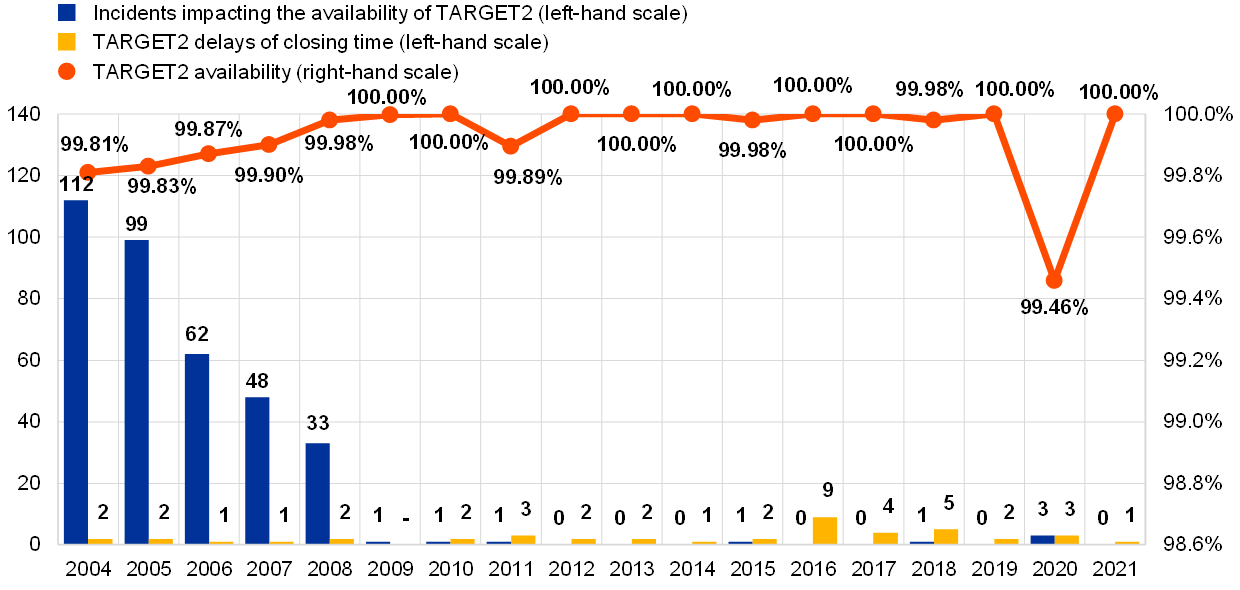

In 2021 the availability of TARGET2’s Single Shared Platform (SSP) stood at 100%.

1 Evolution of TARGET2 traffic

Table 1

Evolution of TARGET2 traffic

Note: There were 258 operating days in 2021 and 257 operating days in 2020.

1.1 TARGET2 turnover

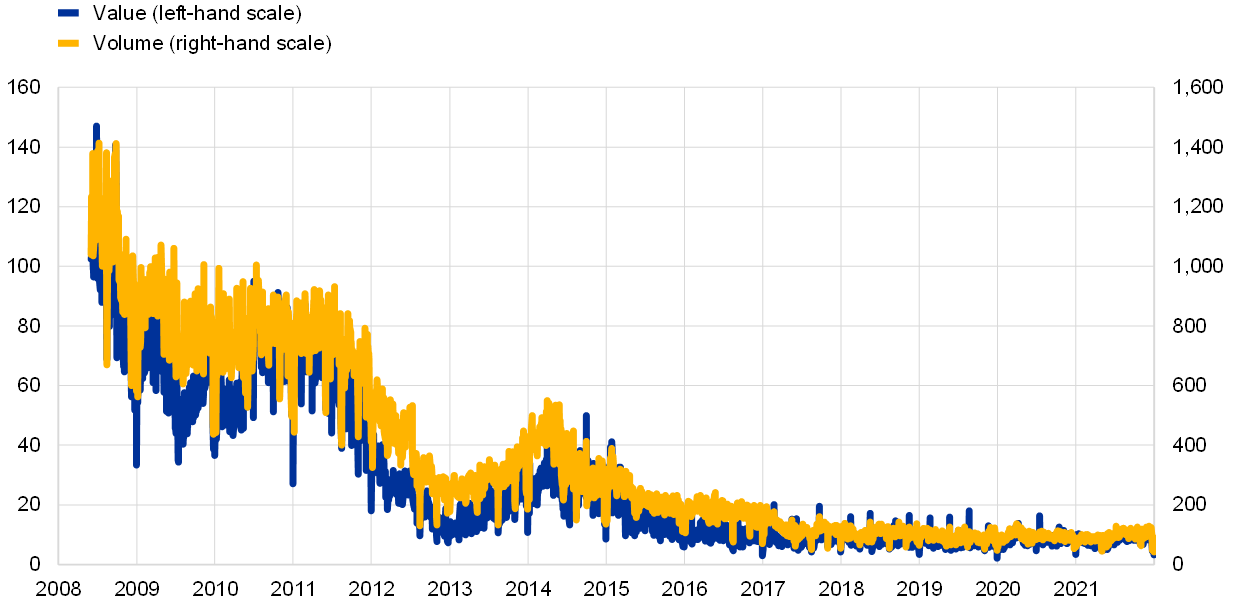

TARGET2 turnover in 2021 amounted to €484.3 trillion, corresponding to a daily average of €1.9 trillion. Chart 1 shows the evolution of the value of TARGET2 traffic over the last ten years. In 2011 and 2012 TARGET2 settlement values continued to recover after the slump caused by the financial crisis, with an annual growth rate of around 3%. The drop of 22% in 2013 was due mainly to a change in the statistical methodology, which involved some transactions ceasing to be included in the aggregate representing the turnover.[8] Overall, after two years of stable figures, TARGET2 turnover on RTGS accounts fell by almost 15% between 2015 and 2017, following the launch of T2S.[9] In 2018 the TARGET2 turnover stabilised, and in 2019, 2020 and 2021 it recorded annual increases of 2.0%, 5.6% and 3.9% respectively. These increases in turnover stemmed mainly from payments relating to operations with the central bank and from interbank payments.

Chart 1

TARGET2 turnover

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: TARGET2.

For activities involving market participants (i.e. excluding central bank and ancillary system transactions), interbank transactions (transactions exclusively involving credit institutions) accounted for 75% of the total value of payments in 2021, while the remaining share was composed of customer transactions (i.e. transactions processed on behalf of a non-bank party, be they individuals or corporate customers). This share has remained stable over the past few years (76% of interbank payments in 2020).

A comparison of the TARGET2 turnover and the euro area’s annual GDP (around €12 trillion) shows that TARGET2 settles the equivalent of the annual GDP in six days of operations. This reflects the role and efficiency of TARGET2, which provides intraday finality for transactions and allows the funds credited to the participant’s account to become immediately available for other payments. Consequently, the same euro can be reused several times by several TARGET2 participants in the same day.

Chart 2 depicts the average daily turnover generated in TARGET2 for each month in 2020 and 2021, thus showing the seasonal pattern of the system. While the general pattern for both years is very similar during the second half of the year, the values recorded in March 2020 are significantly higher than they were in the same period of 2021. The difference is largely attributable to the impact of the coronavirus (COVID-19) pandemic, which resulted in increased market activity during this month.

Chart 2

Average daily TARGET2 turnover

(EUR billions)

Source: TARGET2.

Chart 3 displays the highest and lowest daily TARGET2 values for each month of 2021, as well as the average daily values. The days with the highest peaks are usually at quarter-ends, typically on the last day of the month, owing to reimbursements and due dates in various financial markets. This seasonal pattern was also visible in 2021. However, the day with the largest turnover of the year, with a total value of €2,772 billion, was 24 December. This is largely due to the combination of “end of month, end of quarter and end of year” traditionally observed around Christmas time.

Chart 3

Monthly peaks, troughs and averages of TARGET2 daily values in 2021

(EUR billions)

Source: TARGET2.

Throughout 2021 the amplitude of TARGET2 turnover, expressed as the difference between the highest and the lowest values, was 51%, compared with 58% the previous year. Overall, the average values throughout the year followed a well-established seasonal pattern.

Peaks and troughs in the system’s values can also be influenced by other factors, such as TARGET2 holidays or the end of reserve maintenance periods. For example, the lowest values are typically recorded during the summer holidays and on days that are national holidays in some Member States or in other significant economies outside the EU. In 2021, for instance, the lowest values processed coincided with a public holiday in most European countries (Ascension Day on 13 May).

Finally, Chart 4 compares traffic developments in the world’s major payment systems. In particular, it depicts the daily average turnover in euro equivalents for the last 23 years of TARGET/TARGET2, Continuous Linked Settlement (CLS), Fedwire Funds (the US dollar-denominated RTGS system operated by the Federal Reserve System) and the Bank of Japan Financial Network System (BOJ-NET). Some common patterns, including the effect of the financial crisis on the number of processed transactions, can be identified across systems. However, the comparability of TARGET2 with other systems has been hampered by the change in the TARGET2 statistical methodology in 2013 and the migration of the securities settlement systems to T2S.[10] In the latter case, if the average daily volume in TARGET2 after 2015 is considered together with the average daily turnover for DCAs, which are technically held in T2S, total traffic continues to increase.[11]

Chart 4

Major large-value payment systems around the globe

(EUR billions)

Sources: TARGET2, Fedwire Funds Service (website of the Federal Reserve System); BOJ Time-Series Data (Bank of Japan website); ECB data.

1.2 Volume of transactions in TARGET2

After the low transaction volumes resulting from the financial crisis, TARGET2 traffic recovered, posting a positive trend between 2010 and 2013 (Chart 5). Although the number of transactions never reached pre-crisis levels, the system attracted around four million transactions more over that period. However, this trend reversed in 2014 and 2015 because after the period for migration to Single Euro Payment Area (SEPA) instruments ended,[12] there was once again a significant reduction in the customer payment segment, leading to lower TARGET2 volumes. On completion of the migration to SEPA, TARGET2 traffic stabilised at around 88 million transactions yearly. In 2021 the number of transactions increased significantly to more than 96 million.[13] This represents a historical peak since the launch of TARGET2 in 2008.

Chart 5

TARGET2 traffic

(left-hand scale: number of transactions in millions; right-hand scale: percentages)

Source: TARGET2.

The exact volume settled in TARGET2 in 2021 amounted to 96,354,615 transactions, corresponding to a daily average of 373,468 payments. Compared with the previous year, the overall number of processed payments grew by 8.7%, driven by a higher number of interbank and customer payments. More detailed information on the evolution of the different traffic segments is provided in Box 1.

In only two months in 2021 average daily volumes in TARGET2 calculated on a monthly basis were below the levels recorded for the corresponding months in 2020 (Chart 6). The biggest year-on-year difference, amounting to 17%, was observed in April and this trend continued for the rest of the year. The difference in April was largely due to the impact of the COVID-19 pandemic in 2020. Overall, Chart 6 indicates a seasonal pattern similar to that of the previous year.

Chart 6

Average daily TARGET2 volumes per month

(number of transactions)

Source: TARGET2.

The highest average daily volume was recorded in December, when it reached close to 400,000 transactions. This figure may be related to the high daily volumes normally observed at the end of the year.

Chart 7

Monthly peaks, troughs and averages of TARGET2 daily volumes in 2021

(number of transactions)

Source: TARGET2.

Chart 7 depicts the peaks and troughs in terms of the daily volume on RTGS accounts in TARGET2 in 2021 and the average daily volume for each month. As observed for the value-based figures, the peaks typically fall on the last day of the month, and are especially pronounced at quarter-ends for the same reasons (i.e. deadlines in financial markets or for corporate business). In 2021 the highest daily volume was recorded on 6 April (the day immediately following the Easter weekend, during which TARGET2 was closed for four consecutive calendar days), when 580,290 transactions were processed. This was the third-highest daily peak in TARGET2 since its launch. The lowest daily volume was recorded on 13 May (228,801 transactions), which was a public holiday in most European countries (Ascension Day).

Chart 8 shows the yearly moving average of TARGET2 volumes (i.e. the cumulative volume processed in the preceding 12 months) for each month. This indicator helps to eliminate the strong seasonal pattern observed in TARGET2 traffic. The variation of this cumulative volume from one year to the next is also presented as a percentage. The chart shows that the cumulative volume started to decline in the second half of 2008 with the onset of the financial crisis. The number of transactions continued to drop sharply almost until the end of 2009. After that TARGET2 volumes were roughly stable until the end of 2011. They then started to grow moderately until the end of the first quarter of 2014, when they reached their highest point since the crisis. Thereafter the cumulative volume started to drop for the reasons set out at the beginning of this section (SEPA migration) and in October 2014 the cumulative yearly growth rate turned negative and continued to decrease until mid-2017. The negative trend reversed in 2017 because of the increases observed in the customer and interbank payments segment. It then remained stable throughout 2018 and 2019. In 2020 TARGET2 volumes peaked temporarily in the first quarter as a result of the market turbulence driven by the COVID-19 pandemic. In 2021, after recording a slight decrease in the first quarter, TARGET2 volumes rose steadily over the rest of the year to reach their highest levels since the system was launched.

Chart 8

TARGET2 volumes

(left-hand scale: number of transactions in millions; right-hand scale: percentages)

Source: TARGET2.

Chart 9 compares the growth rate (between 2020 and 2021) of traffic in TARGET2 with the growth rates of major payment systems worldwide and the growth rate of SWIFT payment-related FIN traffic (categories 1 and 2). The chart reveals that the changes in traffic diverged significantly across systems. The largest increase – over 22% – was recorded by SIC (the Swiss payment system), while the largest decrease – around 2% – was recorded by EURO1.[14] This shows that TARGET2 benefited from a general increase in payment activities worldwide in 2021.

Chart 9

Comparison of the changes in traffic in some major large-value payment systems and SWIFT between 2020 and 2021

(percentages)

Sources: TARGET2, Fedwire Funds Service (website of the Federal Reserve System); SWIFT FIN Traffic (SWIFT website); BOJ Time-Series Data (Bank of Japan website); Key payment statistics (Bank of England website); Annual Statistics From 1970 to 2021 (the Clearing House website); SIC statistics (SIX website); and ECB data.

Box 1

The evolution of TARGET2 traffic in 2021

The Eurosystem has been carefully monitoring the evolution of TARGET2 volumes over time, especially considering their relevance for TARGET2 revenues and cost recovery. In 2021 monitoring was particularly strict to assess whether, in the second year of pandemic, any impact on TARGET2 traffic persisted. The purpose of this box is to share the insights gained from the analysis of 2021 volumes.

In 2021 customer payments accounted for 59.9% of total TARGET2 traffic in terms of volume, followed by interbank payments (26.8%), ancillary system payments (7.5%) and central bank operations (5.9%) (Chart A). Customer payment traffic increased by 8.6% compared with 2020, which is significant as the increase in 2020 compared with 2019 was only 1%. In particular, it shows that the number of customer payments has not been negatively affected, so far at least, by the uptake of instant payments in Europe. The increase was driven primarily by higher traffic in France (+22.1%), Spain (+13.5%) and Italy (+11%). Interbank payment traffic showed the greatest year-on-year increase, of 12.7% (the increase in 2020 compared with 2019 was 4%). This pattern was observed across all largest banking communities, in particular in Spain (+23.9%), France (+23.1%) and Germany (+11.1%). Central bank operations saw an inversion of last year’s decrease (-7.1%), with a rise of 1.6%, driven mostly by Belgium (+8.3%) and France (+5.4%). Ancillary system payments increased by 2.6% compared with 2020 (in that year, the change was -2.3% compared with 2019). Most countries showed a significant rise in the number of ancillary system payments, with only few exceptions. Notably, a sharp decline in this payment category was observed in Spain (-43.1%), similar to last year, owing to an ancillary system changing its settlement procedure.

Chart A

TARGET2 volume distribution and yearly growth rate by payment type in 2021

(left panel: number of transactions, millions: right panel; percentages)

Source: TARGET2, ECB calculations.

Note: there were 257 operating days in 2020 and 258 operating days in 2021.

Unlike in 2020, the different waves of the pandemic did not significantly influence the volumes settled in TARGET2 in 2021. Overall, between 4.1 million and 5.5 million customer payments were settled each month in 2021 (Chart B). Customer payments behaved in line with the seasonal patterns typical of the pre-pandemic period, decreasing in January and February, around April and May, and in August, while increasing towards the end of the year. In the last few months of 2021 customer payments rose progressively, exhibiting their usual year-end peak. Interbank payments ranged from 1.9 million to 2.5 million transactions per month in 2021 and followed a trend similar to customer payments, although it was less marked. By contrast, ancillary system payments and central bank operations were not significantly affected by seasonal effects.

Chart B

TARGET2 monthly volumes by payment type in 2021

(number of transactions in millions)

Source: TARGET2, ECB calculations.

Note: There were 257 operating days in 2020 and 258 operating days in 2021.

The fact that in 2021 TARGET2 volumes were on a recovery path after the first pandemic wave in 2020 is even more evident looking at the year-on-year growth rate of daily average payments each month (Chart C). In 2021 the only months that displayed negative growth rates in at least one payment category were those that had not been hit by the pandemic in 2020 (i.e. January and February) and March, when payments spiked owing to market uncertainty caused by the outbreak of COVID-19. Between April and December 2021 all payment categories experienced growth compared with 2020, although interbank payments experienced a less significant increase. Ancillary system payments saw their sharpest year-on-year decrease between January and March 2021 (-3.4% on average), while the average year-on-year change for customer payments was -1.4% over the same period. This was reflected in a drop of 0.8% at system level over these three months. The growth observed in the other months of 2021 largely offset the negative figures of the first quarter, resulting in yearly growth of 8.7% in daily average volumes.[15]

Chart C

Year-on-year change in daily average TARGET2 volumes in 2021

(percentages)

Source: TARGET2 and ECB calculations.

Note: There were 257 operating days in 2020 and 258 operating days in 2021. Total TARGET2 volumes include ancillary system payments, customer payments, interbank payments and central bank operations.

Overall, volumes settled in TARGET2 in 2021 marked a strong increase compared with 2020. The Eurosystem will continue monitoring traffic developments throughout 2022.

1.3 Interactions between TARGET2 and T2S

T2S is the Eurosystem’s pan-European platform for securities settlement in central bank money, bringing together both securities and cash accounts on a single technical platform[16].

T2S went live on 22 June 2015, with central securities depositories (CSDs) joining the platform for euro settlement in waves. The final migration wave was completed on 18 September 2017, thus making 2021 the fourth full year of operations. In addition, on 29 October 2018 Danmarks Nationalbank connected its RTGS and collateral management system, Kronos2, to T2S, so Danish kroner can now also be used to settle the cash leg of securities transactions in T2S. On the same date VP Securities (a Danish CSD that had already been using T2S for settlement in euro) migrated its Danish krone settlement to the platform.

Although the accounts are centralised on a single platform, the legal and business relationships of the holders of the securities and cash accounts remain with the CSDs and national central banks respectively. T2S DCAs are opened with the central banks and are used exclusively for the securities settlement business in T2S. Although they are technically held on the T2S platform, euro-denominated DCAs are legally part of TARGET2. Therefore, the rights and obligations of T2S DCA holders are reflected in the TARGET2 Guideline. At the end of 2021 there were 815 active euro-denominated DCAs on the T2S platform.

At the start of each T2S business day liquidity is sent from TARGET2 to T2S. Towards the end of the day any remaining liquidity on DCAs is swept back to the RTGS accounts in TARGET2. During the day liquidity can be freely transferred from TARGET2 to T2S and vice versa.

In 2021 there were an average of 614 inbound liquidity transfers from TARGET2 to T2S and 1,073 outbound liquidity transfers from T2S to TARGET2 each day.

Chart 10 shows the average cumulative central bank liquidity held in T2S on a daily basis between January and December 2021.[17]

Chart 10

Time distribution of liquidity in DCAs

(EUR billions; daily averages)

Source: TARGET2.

In terms of the intraday pattern, liquidity is injected into T2S at the beginning of the TARGET2 night-time phase (19:30 CET) and its level then remains fairly constant until the TARGET2 daytime processing (at 07:00 CET). After this more liquidity reaches T2S and fluctuations occur. There is a spike in the liquidity held in T2S before 16:00 CET, owing to participants sending liquidity to T2S to reimburse auto-collateralisation and to ensure the remaining transactions are settled. At 16:30 CET the liquidity in T2S decreases sharply as a consequence of the optional cash sweep that brings liquidity back from T2S to TARGET2. The next drop, to zero, is observed towards the end of the business day. This drop is related to the execution of the automated cash sweep from T2S to TARGET2 at 17:45 CET, when all remaining liquidity on DCAs is pushed from T2S back to TARGET2. The optional cash sweep is preferred to the automated cash sweep.

Chart 11 illustrates the daily average value of auto-collateralisation in T2S by month in 2021. Auto-collateralisation is intraday credit granted by a euro area central bank and triggered when a T2S DCA holder has insufficient funds to settle securities transactions.

The average use of auto-collateralisation on stock, i.e. where the credit received from the central bank is collateralised by securities already held by the buyer, remained relatively stable throughout the year. The average daily value was €19.51 billion.

The average usage of auto-collateralisation on flow, i.e. settlement transactions that are financed via credit received from a central bank and collateralised by securities that are about to be purchased, was slightly more volatile and peaked at €103.89 billion in March 2021. The average daily value was €96.27 billion.

On average, 16.85% of the total value of auto-collateralisation was represented by auto-collateralisation on stock and 83.15% by auto-collateralisation on flow in 2021.

Chart 11

Daily average value of auto-collateralisation for euro and Danish krone activity

(EUR billions)

Source: T2S.

Note: Amounts settled in Danish kroner are converted into euro at an exchange rate of DKK 1 = EUR 0.13.

1.4 Interactions between TARGET2 and TIPS

TIPS is a harmonised and standardised pan-European service for the settlement of instant payments in central bank money. TIPS went live on 30 November 2018 with a high capacity and 24/7/365 availability.

TIPS functionalities include the sending and receipt of instant payments, liquidity transfers and recalls of settled instant payment transactions, based on the ISO 20022 standard and in accordance with the SEPA Instant Credit Transfers (SCT Inst) scheme. These instant payments are settled on TIPS DCAs held with the respective national central banks.

Legally, euro-denominated TIPS DCAs fall within the perimeter of TARGET2, so the rights and obligations of TIPS DCA holders are included in the TARGET2 Guideline. At the end of 2021 there were 123 active euro-denominated TIPS DCAs and 9,134 reachable parties in TIPS.

From its inception, TIPS was designed with multi-currency capability. This means that on the request of a non-euro central bank TIPS is able to provide settlement in non-euro central bank money. Following the signing of a cooperation agreement between Sveriges Riksbank and the Eurosystem on 3 April 2020, instant payments in Swedish kronor are expected to be settled on the TIPS technical platform supporting the Swedish service RIX-INST as of May 2022. Instant payments in Danish kroner could also be available by November 2025, when Danmarks Nationalbank is planning to join TIPS. Moreover, in November 2021 Norges Bank expressed interest in entering into formal discussions on potentially joining TIPS and settling instant payments in Norwegian kroner. Building on the multi-currency capability, work to enable a cross-currency functionality, e.g. the settlement of instant payments between the euro and the Swedish krona, moved forward in 2021 and will continue in 2022.

Box 2

Update on TIPS pan-European reachability measures

On 24 July 2020 the ECB communicated the Governing Council decision to take significant steps to support the full deployment of the pan-European reachability of instant payments, an objective shared with the European Commission. According to the decision, by the end of an ad hoc migration period:

- all payment service providers (PSPs) that are reachable in TARGET2 and that adhere to the SCT Inst scheme must also become reachable in TIPS, either as a participant or as a reachable party;

- automated clearing houses (ACHs) must migrate their technical accounts from TARGET2 to TIPS.

The implementation of the pan-European reachability measures allows all PSPs that have adhered to the SCT Inst scheme to be reachable across the entire euro area, irrespective of which clearing and settlement mechanism (CSM) they are using for instant payments (i.e. TIPS or an ACH).

The advantages of these measures include the following:

- PSPs are able to comply with the SEPA regulation.[18] PSPs that have adhered to SCT Inst are able to comply with their legal obligation to support full reachability, without any need to become participants in multiple CSMs.

- Reachability is made a commodity, reflecting the fact that it is a legal requirement. Not only does TIPS benefit from 100% pan-European reachability, but all ACHs competing in the provision of instant payment services automatically include reachability as part of their service offer. Furthermore, ACHs no longer depend on bilateral agreements to establish links, and there is no potential credit exposure for cross-ACH transactions.

- Liquidity management is facilitated. ACH accounts can be funded and defunded from central bank money accounts in TIPS at any time (24/7/365), in contrast to the limitations imposed by the opening hours of TARGET2. This also enables liquidity to be moved from one ACH to another without any time limitation, which can be particularly valuable during long weekends.

- Participants can avail themselves of more options. Each PSP may decide independently (i) where to instruct an instant payment (in TIPS or in an ACH) and (ii) where to hold its liquidity and settle (in an ACH or in TIPS). The choice that one PSP makes in this respect does not depend on the choices of other PSPs.

In order to further support the development of the Single Market and SEPA, the pan-European reachability measures are ultimately aimed at supporting PSPs in enabling European citizens and businesses to give instructions for electronic payments to be made in euro from and to any country in real time, with the confidence that such payments will be settled and will not be rejected because of the inability to reach the beneficiary PSP. This is also a key element in supporting the continuous innovation of front-end solutions, which will benefit the euro community and pave the way for instant payments to become the “new normal”.

To ensure the timely implementation of the measures, the entire Eurosystem, including all national central banks (NCBs) and the ECB, assisted by monitoring market readiness. Dialogue with the market was established in different fora, including the Advisory Group on Market Infrastructures for Payments (AMI-Pay). To facilitate the onboarding process, the Eurosystem collaborated with the market, also taking advantage of the well-established communication channels between NCBs and their national communities. Regular Readiness Reports depicted the status of all NCB communities (i.e. PSPs and ACHs subject to the TIPS pan-European reachability measures) with regard to their readiness to migrate to TIPS. By 30 November 2021 294 PSPs had completed the onboarding process

ACHs were allocated to migration waves, spanning a period from December 2021 to February 2022, with a contingency wave in March 2022. At the end of 2021 six ACHs had migrated their technical accounts from TARGET2 to TIPS, and another five ACHs are expected to finalise their migration as planned in the respective waves in 2022.

1.5 Comparison with EURO1

EURO1 is the only direct competitor to TARGET2 among large-value payment systems denominated in euro. Thus, the market share of TARGET2 is defined as its relative share vis-à-vis EURO1, as shown in Chart 12.

The two systems are different by design, since EURO1 operates on a net settlement basis and only achieves final settlement in central bank money (in TARGET2) at the end of the day. Furthermore, they respond partly to different business cases, since only TARGET2 settles individual transactions in central bank money and processes ancillary system transactions and payments related to monetary policy operations.

However, the traffic in the two systems is made up largely of interbank and customer payments. This helps to explain, in part, the relative share of TARGET2 vis-à-vis EURO1, which is calculated on the basis of only these two payment categories. In 2021 the share of TARGET2 increased in terms of both the value and the volume of payments processed, with 91% of the value and 68% of the volume settled by large-value payment systems in euro.

Chart 12 does not give a full picture of the banks’ routing preferences vis-à-vis all systems, only a partial picture of the market’s preferences in relation to the settlement of large-value euro-denominated transactions. In particular, it does not reflect the extent to which payments are channelled through ACHs or correspondent banking arrangements.

Chart 12

Market share of volumes and values settled in TARGET2 vis-à-vis EURO1

(percentages)

Source: TARGET/Euro LVPS (ECB’s website).

Note: This chart is not affected by the change in the statistical methodology implemented in 2013, since the calculations are based on interbank and customer payments only, and do not include transactions with central banks, which were most affected by the methodological change.

1.6 Value of TARGET2 payments

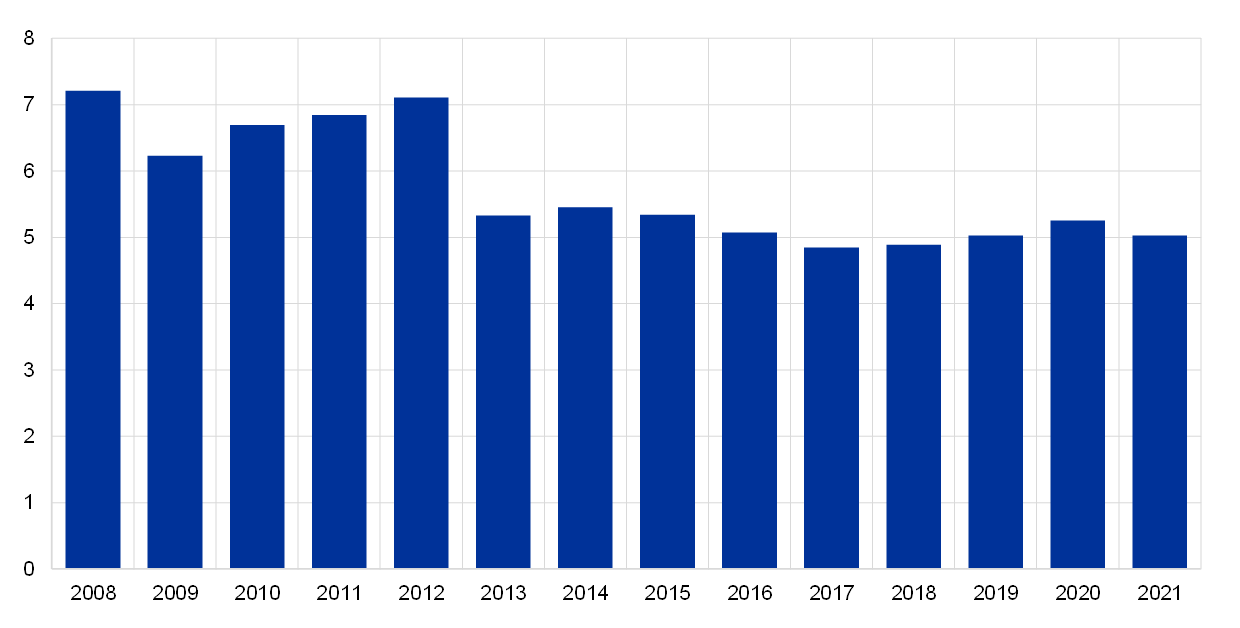

Chart 13 shows the evolution of the average value of a TARGET2 payment between 2008 and 2021.[19] The continuous decrease from 2015 to 2017 was largely related to the migration of securities settlement system traffic to T2S.[20] In 2021 the average value of a payment decreased slightly to €5.0 million, from €5.3 million in 2020.

Chart 13

Average value of a TARGET2 payment

(EUR millions)

Source: TARGET2.

Chart 14 illustrates the distribution of TARGET2 transactions per value band, indicating the shares, in terms of volume, that fall below a certain threshold. The picture remains similar to that of the previous year. Generally, about 70% of all TARGET2 transactions were for values of less than €50,000. Payments of more than €1 million accounted for only 9% of traffic.

Chart 14

Distribution of TARGET2 transactions across value bands in 2021

(percentages)

Source: TARGET2

On average, almost 189 payments with a value of more than €1 billion were made per day, accounting for 0.05% of payment flows. Given the wide distribution of transaction values, the median payment in TARGET2 is calculated as €6,500 which indicates that half of the transactions processed in TARGET2 each day are for a value lower than this amount. This figure confirms that TARGET2 offers a range of features attracting a large number of low-value transactions, especially those of a commercial nature. Although the picture has changed slightly since completion of the migration to SEPA, particularly with regard to commercial payments, TARGET2 is still widely used for low-value payments, in particular urgent customer transactions. This is not unusual in the field of large-value payments and is also observed in other systems worldwide. It remains to be seen whether the increased prominence of instant retail payments will have an impact on this in the future.

Chart 15

Intraday pattern: average value of a TARGET2 payment

(EUR millions)

Source: TARGET2.

Chart 15 depicts the average value of TARGET2 payments executed at different times of the day. The chart indicates that in 2021, as in previous years, TARGET2 settlement showed a strong intraday pattern. After the system opens at 07:00 CET, the hourly average value of transactions fluctuates minimally throughout the day. Between 09:00 CET and 13:00 CET, the average value increases slightly owing to the settlement of CLS and other ancillary system transactions. A more visible increase is recorded between 16:00 CET and 17:00 CET relating to an optional cash sweep from T2S DCAs to TARGET2 and ancillary systems such as EURO1 settling their cash balances in TARGET2. The last hour of operations, between 17:00 CET and 18:00 CET, is reserved for interbank transactions, while the cut-off time for customer payments is 17:00 CET. The average size of payments increases dramatically at this time, owing to banks squaring their balances and refinancing themselves on the money market. Overall, the last two hours of the TARGET2 operation are characterised by a limited number of transactions, albeit at very high values.

The average payment value in 2021 during the last TARGET2 opening hour was largely equivalent to that in 2020.

The chart does not take into account payments that take place before the start and after the end of the business day, since these transactions fall under the night-time settlement category (Section 1.7) and relate strictly to accounting practices, for example liquidity transfers from the local accounting systems of central banks or the fuelling of sub-accounts, as well as T2S DCAs.

1.7 Night-time settlement in TARGET2

TARGET2 operates during the day from 07:00 CET to 18:00 CET, and also offers the possibility of settling payments during the night. Although the system is open for regular payments from financial institutions and ancillary systems during the day-trade phase, night-time settlement is only for ancillary systems connecting via the Ancillary System Interface (ASI), as well as for liquidity transfers to/from T2S and TIPS.[21] Other operations, such as bank-to-bank transactions or customer payments, are only allowed during the day.

There are two night-time settlement windows: 19:30 CET to 22:00 CET and 01:00 CET to 07:00 CET. The two windows are separated by a technical maintenance window, during which no settlement operations are possible.

Since the system is closed during the night to any other form of payment processing, ancillary systems can take advantage of banks’ stable and predictable liquidity situations, thereby settling their transactions efficiently and safely. In general, the night-time windows are used mainly by retail payment systems. In 2021 on average around 1,881 payments, representing a value of €18.53 billion, were settled every night in TARGET2. Compared with 2020, this constitutes an increase of about 9% in terms of value of payments and 4% in volume terms and is roughly in line with overall TARGET2 traffic developments.

Chart 16 shows how the volumes and values settled in TARGET2 during the night have evolved since 2009. The increase in volume in November 2011 occurred as a result of the SEPA Clearer ancillary system starting to make use of the night-time settlement service in TARGET2. From then on, the number of payments settled at night increased steadily, notably in 2014, while values remained fairly stable. The trend reversed in 2015, with night-time settlement values and volumes decreasing continuously. As indicated above, the changes in the night-time settlement pattern in this period can be attributed primarily to securities settlement systems that had migrated their operations to T2S. Since December 2018 night-time settlement values and volumes have reached historically low levels because some ancillary system TARGET2 night-time settlement activity has moved to the day-trade phase.

Chart 16

Night-time settlement in TARGET2

(left-hand scale: number of transactions; right-hand scale: EUR billions)

Source: TARGET2.

1.8 Payment types in TARGET2

Charts 17 and 18 present a breakdown of TARGET2 volumes and turnover by type of transaction. Traffic is divided into four categories: payments to third parties (for example interbank transactions and customer transactions), payments related to operations with the central bank (such as monetary policy operations and cash operations),[22] ancillary system settlement, and liquidity transfers between participants belonging to the same group.

About 84% of the TARGET2 volume is made up of payments to third parties, i.e. payments between market participants. The volume of ancillary system settlement represents 7% of the total, while 7% is generated through operations with the central bank and the remaining 3% is linked to liquidity transfers. Overall, these figures were similar to those for the previous year.

Chart 17

Breakdown of TARGET2 volumes in 2021

(percentages)

Source: TARGET2.

Chart 18

Breakdown of TARGET2 turnover in 2021

(percentages)

Source: TARGET2.

With regard to turnover, payments between participants represent only 41% of total value. The value of ancillary system settlement represents 16% of the total volume, 19% is generated through operations with the central bank and the remaining 24% is linked to liquidity transfers. Overall, these figures were similar to those for the previous year.

The difference between volume-based and value-based indicators across payment categories stems from the fact that the average sums involved in monetary policy transactions, ancillary system instructions and liquidity transfers are typically much larger than payments to third parties.

1.9 The use of prioritisation

Priority options help TARGET2 participants optimise their liquidity usage by allowing them to reserve a certain amount of liquidity for specific payment priorities. When submitting payments in TARGET2, participants can assign them a priority: “normal”, “urgent” or “highly urgent”. In general, payments are settled immediately on a “first in, first out” basis, as long as sufficient liquidity is available in the participant’s RTGS account. However, if this is not the case, payments that cannot be settled immediately are queued according to priority. Participants can reserve a set amount of their liquidity for the “urgent” and “highly urgent” priority classes, and less urgent payments are made when excess liquidity is sufficient. This is a way of securing liquidity for more urgent payments. The priorities for pending transactions can be changed at any time via the information and control module (ICM).

Chart 19 gives an overview of the use of priorities in TARGET2 in terms of the overall TARGET2 volume in 2021. It shows that 86% of transactions were “normal” priority, 8% were “highly urgent” and the remainder were “urgent”. The distribution of the use of priorities when submitting payments to TARGET2 has been stable over the years.

Chart 19

Use of priorities in TARGET2 in 2021

(percentages)

Source: TARGET2.

1.10 Non-settled payments

Non-settled payments in TARGET2 are transactions that have not been processed by the end of the business day, for example, owing to erroneous transactions made by participants, a lack of funds in the account to be debited, or a sender’s limit being breached. The transactions are ultimately rejected. Chart 20 shows the monthly evolution of the daily average of non-settled payments in volume and value terms between 2009 and 2021.

In 2018 the average daily number and value of non-settled transactions fell sharply, driven mainly by the migration of one of the securities settlement systems to T2S at the end of 2017. As a result of its gross settlement model, some of its transactions were rejected, owing to either liquidity shortage or cancellation, and reported as non-settled TARGET2 payments. As in 2020, the average daily number of non-settled transactions in 2021 remained low, at 278. The average total value of these transactions decreased to €0.9 billion in 2021 compared with €2.2 in 2020.

Chart 20

Non-settled payments in TARGET2

(left-hand scale: number of transactions; right-hand scale: EUR billions)

Source: TARGET2.

Non-settled payments in 2021 represented less than 0.1% of the total daily volume and about 0.05% of the total daily turnover in TARGET2. These levels may be considered very low and confirm that liquidity was appropriately distributed across participants throughout that period.

1.11 Use of credit lines in TARGET2

The intraday credit line is a facility in TARGET2 through which banks can overdraw their intraday account against eligible collateral. In 2021 the average maximum intraday credit line at participant level slightly decreased when compared with the previous year, with an average of €1.81 billion. Usage also declined, with 2.5% of payments settled using the intraday credit line in 2021, compared with 3.3% in 2020 (Chart 21). This trend has been observed since the start of the ECB’s asset purchase programme (APP). It continued in 2020 and 2021 when additional stimulus was provided by the Eurosystem in response to the COVID-19 pandemic. With more central bank reserves available on their TARGET2 accounts, participants are less reliant on their intraday credit lines.

Chart 21

TARGET2 intraday credit line and its usage

Source: TARGET2.

Notes: The chart covers the period from June 2008 to December 2021. Figures represent monthly averages. The intraday credit line is calculated as the maximum intraday credit that can be accessed, on average, by one bank during the day against collateral posted. The usage of the intraday credit line represents the percentage of payments that are settled using the intraday credit line. Calculations exclude TARGET2 accounts that do not have an intraday credit line set and follow McAndrews, J. and Rajan, S., “The timing and funding of Fedwire Funds transfers”, Economic Policy Review, Federal Reserve Bank of New York, 2000.

1.12 Share of inter-Member State traffic

The share of inter-Member State traffic in TARGET2 indicates the percentage of traffic that is exchanged between participants belonging to different banking communities. Chart 22 shows that there has been a positive trend for both volume-based and value-based indicators since 2009. This trend reflects the increasing level of financial integration in the large-value payment segment, which is mainly supported by TARGET2. While this trend continued in 2021, with the share reaching 49% in volume terms, it decreased slightly in value terms to 43.8%.

Chart 22

Share of inter-Member State traffic in TARGET2

(percentages)

Source: TARGET2.

When analysing these data, it should be borne in mind that whether a payment is sent or received by a given banking community may depend more on a bank’s internal organisation than on its real geographical domicile. For example, a subsidiary of a French bank, located in Italy, because of its internal organisation, may send TARGET2 payments to another bank, also located in Italy, via its headquarters in France. In this case, the payment flow will be considered to be cross-border, even though the payment is taking place between two entities located in the same country. In contrast, banks located in European Economic Area (EEA) countries whose central banks do not provide TARGET2 services, such as the Czech Republic or Sweden, can participate in TARGET2 component systems provided by other central banks. For example, if a Swedish bank participating in TARGET2-Bank of Finland sends TARGET2 payments to banks in Finland that also participate in TARGET2-Bank of Finland, the payment flows will be considered to be domestic, even though they are taking place between entities located in different countries.

The inter-Member State payments depicted in Chart 22 were identified based on the national banking communities of the sending and receiving direct participants on the platform. Since it is also possible to connect to TARGET2 from a non-EEA country, for example, as an indirect participant or an addressable Bank Identifier Code (BIC) holder, changes in the cross-border share in terms of volume were also computed on the basis of the originator and the beneficiary of the payment, taking into account the full payment chain information (i.e. originator, sending settlement bank, receiving settlement bank and beneficiary). When calculating the inter-Member State shares based on the originator and beneficiary of the payment, the share of cross-border payments in 2021 stood at 62% in terms of volume and 40% in terms of value. Therefore, taking the full payment chain into account leads to a cross-border share that is significantly higher in volume but lower in value.

Box 3

Cross-border payments in TARGET2: an international perspective

As outlined in the Financial Stability Board’s “G20 roadmap for enhancing cross-border payments”,[23] drawn up in coordination with the Committee for Payments and Financial Market Infrastructures (CPMI), the G20 considers the enhancement of cross-border payments a priority, as they are instrumental to supporting economic growth, international trade, global development and financial inclusion. Cross-border payments typically take place via correspondent banking arrangements, which allow foreign banks to access the market for a certain currency via a direct participant of the payment system for that currency (i.e. the correspondent bank).[24] In Europe, a significant share of the payments originating from correspondent banking arrangements are channelled through Large-Value Payment Systems (LVPS), with the largest share of values settled via TARGET2.

So far, the analysis of cross-border traffic in TARGET2 has focused on the payments exchanged between two settlement banks directly connecting to TARGET2 via different central banks in Europe. In 2021 the share of inter-Member State traffic was 43.8% in value terms and 49.5% in volume terms.[25] However, by analysing the full payment chain, including the information on the indirect originator and beneficiary, it is also possible to identify the geographical area of the final counterparties involved in the transactions. This offers an international perspective on the role of TARGET2 in supporting cross-border activity and access to the euro market. In this case, the share of cross-border activity in TARGET2 reached 39.9% in value terms and 61.6% in volume terms in 2021 (see Section 1.12). The notable difference between these two methods of measuring cross-border activity deserves further investigation.

When considering the whole payment chain, TARGET2 traffic can be broken down into domestic traffic (i.e. within a euro area jurisdiction), traffic between different euro area jurisdictions, traffic between a euro area jurisdiction and a jurisdiction outside the euro area (also known as “one leg out transactions”), as well as traffic between extra-euro area jurisdictions. Domestic payments still represent the largest component of TARGET2 values, although, after the strong growth in the first four years of the system’s operation, they dropped sharply between mid-2012 and the beginning of 2013,[26] and accounted for 51.0% of the total in 2021 (Chart A). The other categories have been relatively stable throughout the whole period, with shares lower than 20%. The picture is different for the volume of payments. Despite a significant drop in 2017, coinciding with the migration waves to T2S, domestic payments accounted for the highest share of TARGET2 volumes until the beginning of 2020 (46.0% on average), when they were surpassed by cross-border payments between euro area and non-euro area countries, which were the main component of TARGET2 payments in 2021, with a share of 37.6%.

Chart A

TARGET2 traffic by counterparty location

(monthly totals; left panel: EUR billions; right panel: number of transactions)

Source: TARGET2.

Note: The category “EA domestic” comprises the traffic settled within the same euro area country, the category “between EA” comprises the traffic settled between two euro area countries, the category “between EA and non-EA” comprises the traffic settled between a euro area country and a non-euro area country and the category “between non-EA” comprises the traffic settled between two non-euro area countries.

Focusing on one leg out transactions, there is a visible asymmetry on the originator and the beneficiary sides (Chart B). Payments from non-euro area originators represented on average 25.3% of the monthly TARGET2 volumes until 2014, then progressively increased to an average of 33.1% in the last two years. In value terms, this share was on average 17.0% until 2014, then it progressively increased until 2018 and stabilised at around 23.0% in 2021.[27] Conversely, payments received by non-euro area beneficiaries display a similar share in volume and value terms, accounting for 24.9% and 23.4% of TARGET2 traffic in 2021 respectively, and they also display similar growth patterns over time. This asymmetry suggests a lower average payment size on the sending side than on the receiving side, and thus that the business cases on the sending side differ partially from the business cases on the receiving side. For example, payments from outside the euro area could be used to a larger extent to purchase goods and services in the euro area from other jurisdictions, as a lower payment size is a typical indication of a higher presence of retail transactions. Historically, originators and beneficiaries of payments in TARGET2 have been located predominantly in the United Kingdom, the United States and Switzerland, although their relevance tends to be lower on the beneficiary side in volume terms.

Chart B

Share of TARGET2 activity with non-euro area originators or beneficiaries

(monthly totals; percentages)

Source: TARGET2.

Note: The left panel shows the percentage of traffic with an originator located outside of the euro area, irrespective of the location of the beneficiary, whereas the right panel shows the percentage of traffic with a beneficiary located outside of the euro area, irrespective of the location of the originator.

The breakdown of interbank traffic by location of originator and beneficiary sheds light on the geographical distribution of payment flows in value terms, as these payments represent the main category contributing to TARGET2 turnover.[28] The shares have been relatively stable over time, with domestic and intra-euro area traffic only accounting for around half of the total interbank value (Chart C).[29] Conversely, in volume terms, customer payments, which can largely be considered retail payments, make up most of TARGET2 traffic. Between 2008 and 2021 the domestic share decreased, in line with the traffic between euro area countries, with an acceleration towards the end of the SEPA migration period (see Section 1.2). Over the same period one leg out customer payments grew from an average of 29.3% to 45.0% and customer payments between non-euro area countries increased from 3.7% to 9.0%. This indicates a greater use of TARGET2 to settle euro-denominated retail transactions involving counterparties outside the euro area. Overall, the breakdown by payment type suggests that TARGET2 has been facilitating the access of non-euro area actors to the euro market for both financial and commercial flows.

Chart C

Selected TARGET2 payment categories by counterparty location

(monthly totals; percentages)

Source: TARGET2.

Note: The category “EA domestic” comprises the traffic settled within the same euro area country, the category “between EA” comprises the traffic settled between two euro area countries, the category “between EA and non-EA” comprises the traffic settled between a euro area country and a non-euro area country and the category “between non-EA” comprises the traffic settled between two non-euro area countries. Interbank payments do not include intragroup transactions.

Looking at the originator and beneficiary of a payment makes it possible to identify the geographical area of the final counterparties involved in the transaction. In value terms, payments exchanged within the euro area, either domestically or between different countries, account for most of the TARGET2 traffic. However, interbank traffic alone accounts for a share of around 50%. In volume terms, the picture is different. The share of cross-border payments involving non-euro area counterparties has gradually increased over time and represented half of TARGET2 payments in 2021. Cross-border payments originating from outside the euro area typically display a lower average value compared with those received by non-euro area institutions, suggesting a growing share of transactions of a commercial nature coming into the euro area from the outside. Overall, these results show that TARGET2 has not only contributed to financial integration in Europe, but also substantially facilitates cross-border payments worldwide and access to the euro market, thus supporting the euro area economy and the international role of the euro.

1.13 Tiering in TARGET2

Tiered participation arrangements occur in a payment system when a direct participant of that system provides services that allow other participants to access the system indirectly. The indirectly connected participants benefit, in turn, from the clearing and settlement facility services offered by direct participants.

While indirectly connected parties, i.e. indirect participants and addressable BIC holders, benefit from the settlement facility that would otherwise be costly to access directly, these types of arrangement also entail risks. Tiered participation arrangements can create dependencies that may lead to overall credit, liquidity or operational risks for the payment system, its participants or the stability of the banking system. Close monitoring of the tiering level in TARGET2 is thus of paramount importance. It is also an oversight requirement under Article 17 of the SIPS Regulation.[30]

The image below shows the map of TARGET2 flows based on the location of the payment originators and final beneficiaries. The institutions at both ends of the payment chain are a reflection of the global reach of TARGET2.

Figure 1

TARGET2 transfers based on the location of the originator and final beneficiary banks

Source: TARGET2.

In 2021 the aggregate level of tiering by sender in TARGET2 reached around 6.78% in terms of value and 24.54% in terms of volume (Chart 23). This meant that, on average, for every euro sent by direct participants in TARGET2 during the year, only 6.78 cents were settled on behalf of indirectly connected parties outside their banking group perimeter. More than 75% of the tiered business (consolidated at banking group level) comes from outside the EEA, showing that TARGET2 makes it possible for institutions around the world to access the euro market.

Chart 23

Tiering by sender in TARGET2

(x-axis: ten-day moving averages; y-axis: percentages)

Source: TARGET2.

The largest indirect participant in terms of value sent (consolidated at banking group level) was ranked approximately 40th out of all TARGET2 participants in 2021.

Further analysis reveals that 59.15% of all direct participants in TARGET2 (consolidated at banking group level) did not conduct any business during the year on behalf of indirect parties. Overall, these statistics for 2021 point to a relatively stable and contained level of tiered participation in TARGET2.

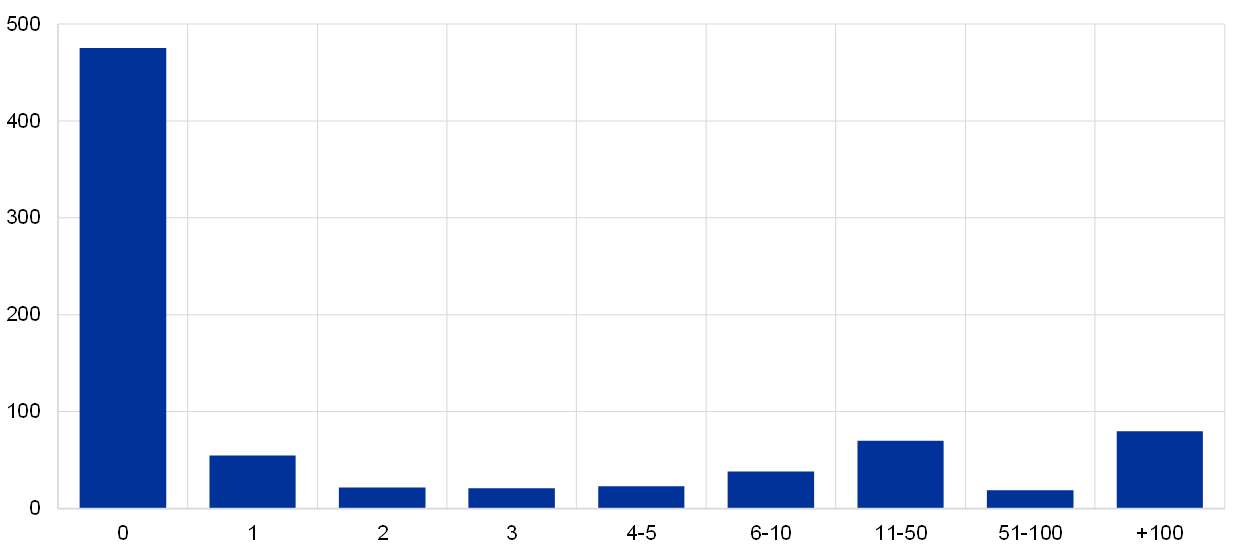

Chart 24 shows that around 475 direct participants do not send or receive any tiered payments while 55 send or receive payments on behalf of only one tiered banking group. At the other end of the spectrum, around 80 direct participants act as a settlement bank for more than 100 tiered banking groups.

Chart 24

Tiered groups per direct participant group

(x-axis: tiered participants; y-axis: direct participants)

Source: TARGET2.

Box 4

Indirect participation in TARGET2

Direct participants can send and receive payments on behalf of indirectly connected institutions in TARGET2 via tiered participation arrangements in the context of the correspondent banking business.[31] Indirectly connected institutions may be located within or outside the EEA and listed in the TARGET2 directory (see Section 3.2). However, they can be reached via TARGET2 even if they are not registered. One reason for this is that, in terms of its BIC, an institution can only be listed once as “indirect” in the TARGET2 directory, although it may, in practice, rely on multiple direct participants. There may also be other reasons why an indirect participant is not registered in the TARGET2 directory. This box looks into the traffic sent to TARGET2 by direct participants on behalf of registered and non-registered indirectly connected institutions.

Total tiered traffic sent to TARGET2 in 2021 stood at €32.5 trillion, corresponding to 23.5 million payments, and registered indirectly connected institutions accounted for 35.2% and 52.6% of the traffic in value and volume terms respectively. In other words, non-registered institutions accounted for a very significant share of indirect traffic, sending almost two-thirds of the tiered payments in value terms and almost half of the tiered payments in volume terms. This asymmetry suggests that the average payment size was higher for non-registered indirectly connected institutions than for registered ones.

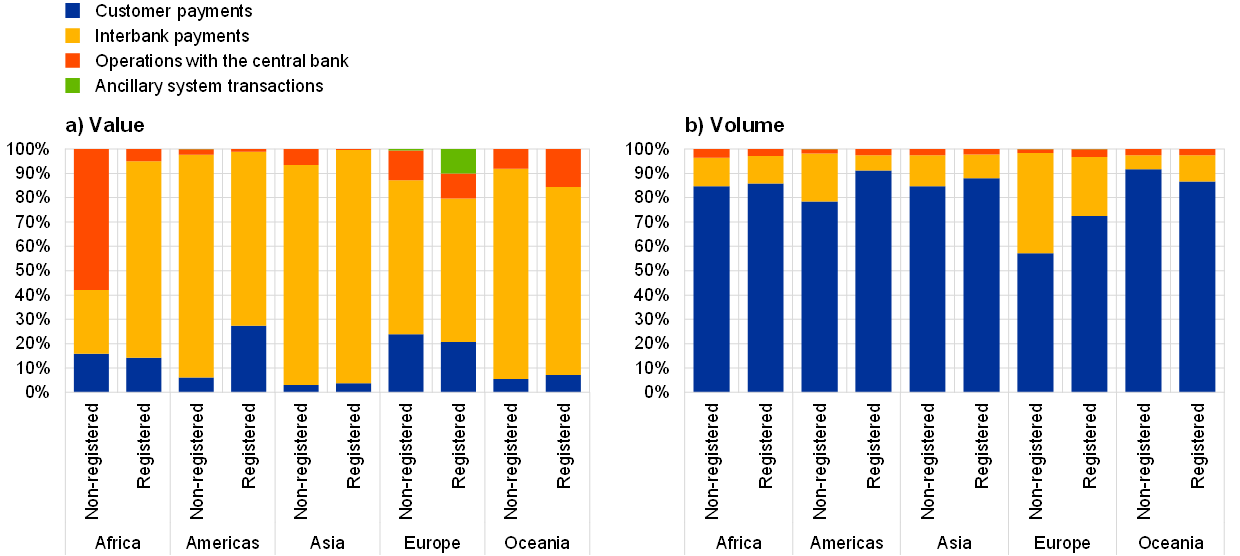

The share of TARGET2 traffic sent by registered and non-registered institutions was different across geographical areas and in value and volume terms (Chart A). Most of the payments sent by non-registered institutions originated in Europe (55.2% in value terms and 55.8% in volume terms), the Americas (29.3% in value terms) and Asia (17.4% in volume terms). Non-registered institutions accounted for more than half the tiered traffic in all geographical areas in value terms, ranging between 50.1% in Asia and 92.7% in the Americas, and volume, except for Asia and Europe, where they represented 44.7% and 43.1% of tiered traffic in volume terms respectively.

Chart A

TARGET2 tiered traffic by registration status and geographical area

(yearly totals; left panel: EUR trillion; right panel: number of transactions, millions)

Source: TARGET2.

Note: The geographical area is assigned based on the country code of the institution’s BIC.

Of the 7,931 indirectly connected institutions[32] that sent at least one tiered payment to TARGET2 in 2021, 2,508 institutions were registered in the TARGET2 directory and 5,423 were not (see Chart B). The share of non-registered institutions as a percentage of the total number of indirect institutions was high across all geographical areas, ranging from 62.2% in Europe to 81.6% in the Americas. At the same time, in 2021 each registered institution sent an average of 4,935 payments, while each non-registered institution sent an average of 2,059 payments. This suggests that registered institutions sent payments to TARGET2 more frequently than non-registered ones.

Chart B

TARGET2 indirectly connected institutions by registration status and geographical area

(number of BICs)

Source: TARGET2.

Note: The geographical area is assigned based on the country code of the institution’s BIC.

Payments sent by registered and non-registered institutions had a similar breakdown by payment type across geographical areas in 2021. In line with the statistics at system level, interbank payments were the main contributors to tiered TARGET2 traffic in value terms, whereas customer payments were the leading category in volume terms. Interbank payments represented 71.4% or more of the total values sent by registered and non-registered institutions in each geographical area, except for non-registered institutions in Africa (26.2%) and registered and non-registered institutions in Europe (58.9% and 63.2% respectively).[33] Customer payments accounted for a notably larger share of the volumes sent by registered institutions compared with non-registered ones in Europe (+15.3 percentage points) and in the Americas (+12.7 percentage points).

Chart C

TARGET2 payment categories by registration status and geographical area

(monthly totals; percentages)

Source: TARGET2.

Note: The geographical area is assigned based on the country code of the institution’s BIC. The category “interbank payments” also includes intragroup payments.

Overall, in 2021 a significant share of tiered traffic in TARGET2 was sent by indirectly connected institutions that were not registered in the TARGET2 directory. These institutions accounted for almost two-thirds of all tiered payments in volume terms and almost half of all tiered payments in value terms. Non-registered institutions represented the highest share of indirect participants across all geographical areas. These findings suggest that the number of counterparties reachable via TARGET2 is much higher than the number in the TARGET2 directory and hence the TARGET2 network is broader. At the same time, the lower average number of payments sent by non-registered institutions suggests that these institutions act less frequently compared with registered ones.

1.14 Money market transactions in TARGET2

Market participants use TARGET2 for settling unsecured money market transactions in central bank money. By applying the Furfine algorithm[34] it is possible to identify TARGET2 transactions which are related to money market loans, or, more precisely, to the unsecured overnight money market.[35] This unique dataset is updated regularly to obtain the latest information about the money market. Overall, TARGET2 transaction data provide a rich source of information for both the analysis of monetary policy implementation and TARGET2 operations. The importance of the money market is thus twofold: (i) it is an important vehicle for the redistribution of liquidity among TARGET2 participants, and (ii) it is a large-value and time-critical area of business that the operator needs to be aware of, in particular when dealing with abnormal situations.

The dataset has been developed using the TARGET2 Simulator environment and comprises data from June 2008 onwards.[36] In 2021 around 24,510 money market loans, with a total value of about €2.14 trillion, were identified. Overall, the amount of unsecured funds traded on the overnight market remained at low levels compared with the period before the financial and sovereign debt crises. Activity in 2021 was in line with 2020 and higher compared with 2019 (Chart 25).

Chart 25

Unsecured overnight money market activity in TARGET2

(daily totals, left-hand scale: EUR billions; right-hand scale: number of transactions)

Source: TARGET2.

Chart 26 complements this analysis by showing the cumulative distribution in value of all money market transactions during the day in 2021. On the lending leg, 50% of the total value is settled by around 15:35 CET, while 98% is settled by around 17:00 CET. This confirms the assumption that the last few hours of TARGET2 operations are particularly important for the interbank market. In terms of repayment, three-quarters of the loans are repaid by around 12:00 CET and 90% by around 14:30 CET. These patterns ensure that the repaid liquidity can be reused for payment purposes later that day.

Chart 26

Cumulative distribution of money market transactions during the day in value terms

(percentages)

Source: TARGET2.

1.15 Shares of national banking communities

The following two charts break down TARGET2 volumes and turnover according to the share of the biggest national banking communities contributing to its traffic.

Chart 27

Country contributions to TARGET2 volume

(percentages)

Source: TARGET2.

Chart 28

Country contributions to TARGET2 value

(percentages)

Source: TARGET2.

As in previous years, in 2021, the largest contributor to TARGET2 traffic in volume terms was Germany, which accounted for more than half of the transactions settled in the system. The addition of France, Italy, Spain, the Netherlands and Belgium increases the share of transactions to 88%, which is on a par with previous years. The shares of the biggest contributors to TARGET2 volumes remained stable.

Germany is also the main contributor by turnover, followed by France, Luxembourg and the Netherlands. The top four countries by turnover generated over three-quarters of the total value settled in TARGET2 in 2021. The concentration of turnover remained stable compared with the previous year.

It should be noted that the high concentration of both TARGET2 values and volumes in certain countries is not only due to the size of particular markets. It can also be attributed to the fact that since November 2007 the TARGET2 system has allowed the activities of banking groups to be consolidated in a single RTGS account held by the group’s head office, thereby increasing concentration in countries where a large number of these groups are incorporated.

1.16 Pattern of intraday flows

Chart 29 shows the intraday distribution of TARGET2 traffic, i.e. the percentage of daily volumes and values processed at different times of the day in 2021. This indicator is significant for the operator of TARGET2 as it represents the extent to which settlement is evenly spread throughout the day or concentrated at certain peak times. Ideally, the value/volume distribution should be as linear as possible to avoid liquidity and operational risk.

Chart 29

Intraday distribution of TARGET2 traffic in 2021

(percentages of daily volumes and values)

Source: TARGET2.

In value terms, the path is typically very close to linear distribution, indicating an even spread throughout the day, which, in turn, ensures the smooth settlement of TARGET2 transactions.

In volume terms, the curve is well above the linear distribution, with over one-fifth of transactions submitted to the system within one hour of the start of operations – including transactions sent at night by participants and warehoused payments – and almost half submitted within three hours of the start. One hour before the system closes, almost 100% of the TARGET2 volume has already been processed. A comparison with previous years shows no significant deviations.

Box 5

External review carried out by Deloitte on the incidents that affected TARGET services in 2020

In December 2020 the ECB appointed Deloitte GmbH to conduct an independent review of five major information technology-related incidents (not cyber incidents) which occurred in 2020, affecting payment transactions and securities processing of TARGET services. The review aimed to identify the root causes of the incidents, draw more general lessons and propose recommendations in the following six key areas: (i) change and release management, (ii) business continuity management, (iii) failover and recovery tests, (iv) communication protocols, (v) governance, and (vi) data centre and IT operations.

On 28 July 2021 the ECB published Deloitte’s independent review. The report included a detailed description of the relevant incidents, the impact that each had on TARGET services participants and the respective root causes. Deloitte also performed a thorough review of the procedures followed during the incidents, highlighting the weaknesses identified and issuing recommendations to address them.

In its response, the Eurosystem accepted Deloitte’s general conclusions and recommendations, and committed to decisively address them.

In the second half of 2021 the Eurosystem prepared an action plan to address in a timely manner the issues and recommendations raised by Deloitte. The action plan was broadened to include recommendations issued by the Eurosystem oversight function and the Internal Audit Committee in relation to the TARGET services incidents that took place in 2020. In addition, for the recommendations related to a specific TARGET Service, the Eurosystem sought to design response actions that would apply holistically across the different TARGET services and the T2-T2S consolidated system due to go live in November 2022.

Measures addressing several recommendations were agreed or implemented in 2021, while most of the remaining measures will be implemented in 2022. For some recommendations, market participants were also involved to ensure that their views were taken into account. For that purpose, dedicated sessions with the Advisory Group on Market Infrastructures for Payments (AMI-Pay), the Advisory Group on Market Infrastructures for Securities and Collateral (AMI-SeCo) and the T2S CSD Steering Group (CSG) were organised. These groups will also be regularly updated on the implementation of the action plan until its completion.

On 17 December 2021 the ECB published a summary of the action plan, which also indicates the respective deadlines for the implementation of the measures.

The action plan has been structured according to the six workstreams of the Deloitte review, i.e. (I) change and release management; (II) business continuity management; (III) failover and recovery tests; (IV) communication protocols; (V) governance; and (VI) data centre and IT operations, and the actions listed below were implemented in 2021.

Workstream I: change and release management

Strengthening the local technical change management with training sessions offered to external staff and ensuring strict application of the instructions included with the relevant changes. In addition, unsupervised work in secure areas is avoided by following a well-defined process that governs access to such areas.

Workstream II: business continuity management

A new technical procedure for activating the Enhanced Contingency Solution (ECONS I) was implemented by the 4CB in the fourth quarter of 2021 and included in the relevant processes and testing activities. The 4CB have also ensured that operational staff are fully trained and knowledgeable about the ECONS I activation procedures in all situations.

Workstream III: failover and recovery tests

The technical documentation supporting the operational recovery tests and the test calendar have already been amended. With regard to the improvement of contingency procedures testing, all TARGET2 central banks are required to perform monthly checks of their technical ability to connect to ECONS I and to the contingency network.

Workstream IV: communication protocols

The external communication protocols have already been improved following discussions with market participants held in February 2021. It is now, for example, easier for participants to access the RSS feed notification service, and the TARGET services section of the ECB website has been streamlined to show the operational status of the three services (TARGET2, T2S and TIPS) clearly on a single page along with a link to past communications (historical overview).

Workstream V: governance

The second line of defence has been fully implemented. The TARGET services risk management framework will ensure that specific criteria for the necessary independence, transparency and information sharing and participation in decision-making are implemented in line with the expectations set out in Annex 1 to the TARGET2 Guideline (ECB/2012/27).[37]

Workstream VI: data centre and IT operations

The recruitment process at 4CB, which encountered difficulties in recruiting new staff owing to the outbreak of the coronavirus (COVID-19) pandemic, has been restarted and aims to ensure that there is a suitable number of qualified staff across all functions of the 4CB, with a special focus on day-to-day operations.

2 TARGET2 service level and availability

In 2021 99.99% of all payments settled in the payments module of TARGET2 were processed in less than five minutes. This indicator shows clear progress compared with 2020, when it was negatively affected by three major incidents (Box 5).

Service delivery times and payment processing times generally remained stable in 2021, confirming the high performance level of TARGET2’s SSP. This excellent performance is advantageous for the banking community, particularly for its real-time liquidity management.

Payment processing times are measured for all the payments settled in TARGET2, with the exception of: (i) ancillary system settlement transactions using the ASI, (ii) payments settled during the first hour of operations (see the “morning queue effect” below) and, (iii) payments that have not been settled owing to a lack of funds or a breach of limit. In practice, around 30% of all TARGET2 payments fall into these three categories, meaning that the statistics on processing times apply to around 70% of the system’s traffic.

99.98%[38] of requests or enquiries were processed in less than one minute and only 0.02% in one to three minutes, with levels remaining the same as in 2020.

Chart 30 helps to better quantify the system’s performance by showing the distribution of processing times on the SSP, i.e. the percentage of traffic with a processing time below a certain number of seconds. The reference point taken is the peak day of the year recorded by the SSP, namely 6 April 2021, when 580,290 payments were settled. The chart shows that on this day 50% of transactions were settled within 26 seconds and 90% within 38 seconds, thereby confirming the system’s high level of performance.

Chart 30

Processing times on 6 April 2021, excluding the first hour

(x-axis: seconds ; y-axis: percentages)

Source: TARGET2.