- 15 APRIL 2021

- RESEARCH BULLETIN NO. 83

Making waves – Fed spillovers are stronger and more encompassing than the ECB’s

This article argues that European Central Bank (ECB) and Federal Reserve System (Fed) monetary policy spill over to other countries asymmetrically. At the bilateral level, the Fed’s impact on the euro area is material to firms’ financial conditions and economic activity. Conversely, the impact of the ECB’s actions on the US economy is minimal. On a global scale, both central banks’ monetary policies matter for other countries, but the Fed’s monetary policy has a more sizeable impact, particularly on foreign financial variables, such as corporate bond spreads.

Monetary policy in a globalised world

International trade and financial globalisation have made economies more interdependent and more exposed to each other’s domestic shocks. Economic theory suggests that globalisation affects the transmission mechanism of monetary policy and that its spillovers could strengthen the international dimension of monetary policy.[2] When monetary policy actions spill over abroad, this might at times complement policy choices in other countries and thus be a welcome externality. But at other times this might confront these countries with unfavourable policy choices. For example, they may find it harder to reconcile macroeconomic and financial stability without resorting to an enlarged set of policy tools. Only by exploring data can we shine a light on the extent to which monetary policy has acquired a global dimension.

Comparing spillovers originating from different central banks based on previous research is difficult. In past approaches, the estimation methodology, identification approach and sample period have differed widely. In what follows we summarise the findings of our recent paper (Ca’ Zorzi et. al, 2020), where we carefully disentangle the effects of ECB and Fed monetary policy. We compare the impact of each central bank’s monetary policy – both on the other’s economy and worldwide – using a unified and consistent methodological framework.

Identifying international spillovers

Spillovers are a potential side effect of monetary policy. Our identification approach disentangles the exogenous or “surprise” variation in monetary policy from the systematic response of monetary policy to economic developments, such as the latest inflation readings. During a sufficiently narrow time window around monetary policy announcements it is unlikely that events or news besides the policy announcement drive financial markets. The movement in interest rates during this short period therefore represents an exogenous effect of the monetary policy announcement – a surprise, unanticipated by financial markets given all available information, including the most recent economic developments. Additionally, our identification separates such exogenous monetary policy shocks from what the literature refers to as “central bank information” shocks.[3]

We estimate the impact of ECB and Fed monetary policy based on Bayesian vector-autoregression (BVAR) models for the years 1999 to 2018.[4] Our estimates represent the average effects of monetary policy over this period. Therefore, they encompass the effects of both conventional policies (e.g. setting interest rates) and unconventional policies (e.g. adding purchase programmes or broadening the range of eligible collateral).[5]

Bilateral spillovers between the euro area and the United States

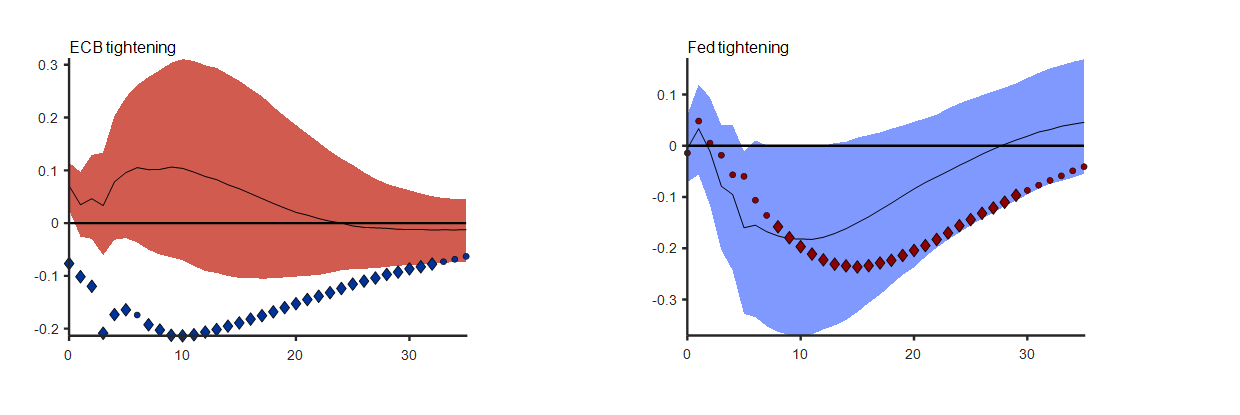

Even in a highly globalised world, both ECB and Fed monetary policies have a sizeable impact on domestic financial conditions, real activity and inflation. Surprise monetary policy tightening by either the ECB or the Fed raises domestic government and corporate bond yields, depresses domestic equity markets, and triggers an appreciation of the domestic currency as well as a fall in inflation and real activity. In Chart 1, below, the dotted lines show this strong effect on domestic real activity, measured here by industrial production.

Chart 1

Bilateral spillovers from a monetary policy tightening to real activity

Industrial production

(100 x log)

Notes: The left-hand panel shows the impulse response to an ECB tightening, and the right-hand panel the response to a Federal Reserve tightening, each over a period of 36 months. Quantities for the United States are plotted in red, quantities for the euro area in blue. The dotted lines show the response of domestic industrial production, with diamonds symbolising significance at the one-standard deviation level. The solid line shows the median impulse response of the corresponding spillover with a one-standard-deviation band. Sources: SDW, FRED.

The solid line with the blue confidence band in the right-hand panel highlights the impact of US monetary on the euro area: a Fed tightening leads to a reduction of euro area industrial production. Conversely, the impact of ECB monetary policy on the US economy in the left-hand panel is insignificant. There are two possible explanations: either the Fed has been able and quite determined to fully offset spillovers from ECB monetary policy; or, alternatively, the ECB’s monetary policy did not give rise to significant spillovers in the first place.

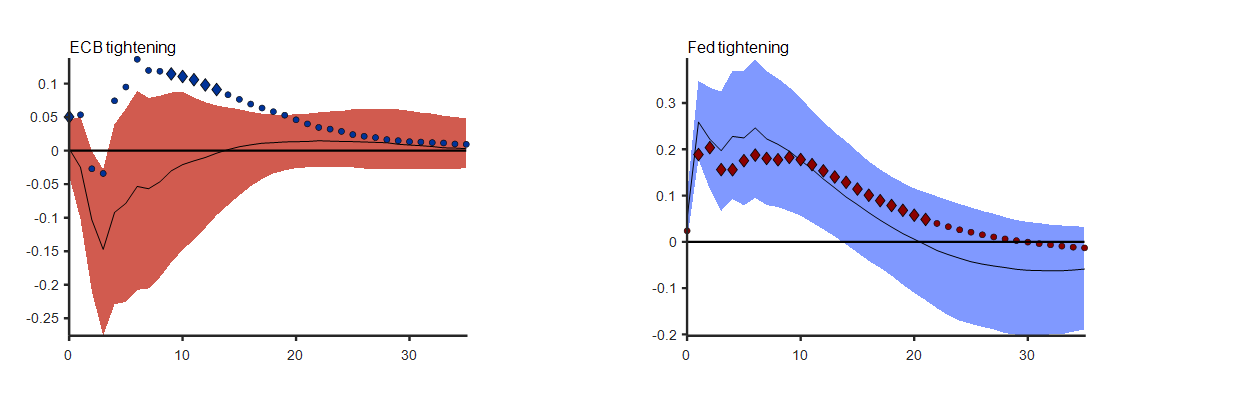

Chart 2

Bilateral financial spillovers from a monetary policy tightening

Corporate bond spreads

(below investment grade, all maturities, percentage points)

Notes: The left-hand panel shows the impulse response to an ECB tightening, and the right-hand panel the response to a Federal Reserve tightening, each over a period of 36 months. Quantities for the United States are plotted in red, quantities for the euro area in blue. The dotted lines show the response of domestic corporate bond spreads, with diamonds symbolising significance at the one-standard-deviation level. The solid line shows the median impulse response of the corresponding spillover with a one-standard-deviation band. The corporate bond spread is the option-adjusted spread between a corporate bond with a BBB or below investment grade rating and a government bond. Source: FRED.

By contrast, Fed monetary policy spillovers to the euro area are much larger. They significantly affect euro area financial conditions, especially corporate bond rates (Chart 2). This suggests that financial channels play a prominent role in Fed spillovers to the euro area.

Global effects of ECB and Fed monetary policy

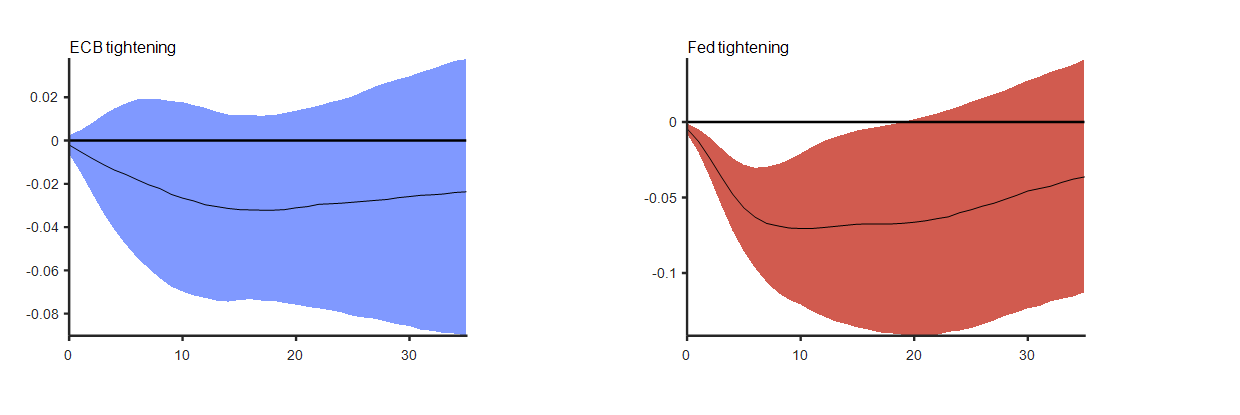

This asymmetry between the ECB and Fed monetary policy goes beyond the bilateral transatlantic spillovers. It is evident also in their cross-border impact on emerging market economies (EMEs). Consistent with the dominant role of the US dollar in the international monetary system, Fed monetary policy elicits large spillovers to both financial conditions and real activity in EMEs (Chart 3). By contrast, spillovers from ECB monetary policy are largely confined to trade.[6] Unlike the bilateral spillovers between the euro area and the United States, our findings suggest that ECB and Fed monetary policy actions may give rise to policy trade-offs in EMEs if the policy cycles are not in sync.

Chart 3

Effects of a monetary policy tightening on EMEs

Real GDP of EMEs

(USD, 100 x log)

Notes: The solid line shows the median impulse response surrounded by a one-standard-deviation band over a period of 36 months. In the left-hand panel are the responses to an ECB tightening, in the right-hand panel the responses to a Fed tightening. GDP is shown measured at prices and exchange rates in 2010, seasonally adjusted, in US dollars, based on a cubic spline interpolation from quarterly data, including the countries: Bolivia, Botswana, Brazil, Chile, China, Costa Rica, Ecuador, El Salvador, Hong Kong, India, Indonesia, Israel, Jordan, Kazakhstan, South Korea, Malaysia, Mexico, Paraguay, Peru, the Philippines, Poland, Russia, Singapore, South Africa, Taiwan, Thailand, Turkey, Uruguay. Sources: Haver Analytics, ECB calculations.

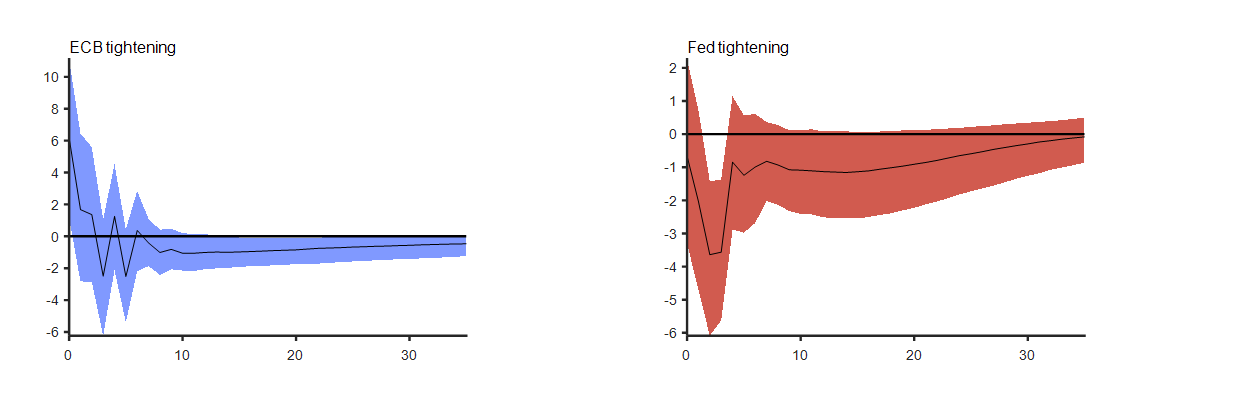

Our findings suggest a key role for financial channels as a conduit of US monetary policy spillovers, especially towards EMEs. Fed monetary policy actions can have major implications for global financial markets (Chart 4). Both the central role of US financial markets and the dominant role of the US dollar amplify the global effects of Fed monetary policy.

Chart 4

Effects of a monetary policy tightening on global financial markets

Syndicated loans outside denomination currency area

(new loan issue volume, 100 x log)

Notes: The solid line shows the median impulse response surrounded by a one-standard-deviation band over a period of 36 months. In the left-hand panel these are the responses to an ECB tightening, in the right-hand panel the responses to a Fed tightening. Sources: Dealogic, ECB calculations.

Dealing with foreign spillovers

Unlike the limited bilateral spillovers between the euro area and the United States, the spillovers to the rest of the world suggest that both ECB and Fed monetary policy actions are relevant for the policy choices of EMEs. In periods of unfavourable spillovers, EME policy trade-offs could arise as a result of more widespread and more pronounced frictions in local financial and product markets, for example due to a less developed local banking sector or rigidly regulated industries. Our empirical perspective does not rule out possible gains from monetary policy co-ordination between advanced and emerging economies. But it might also be possible to mitigate trade-offs locally, for example by assigning a greater role to macroprudential policies, such as regulating the leverage in the financial system (Rey 2016). This might help EME policymakers to preserve financial stability without compromising their intended monetary policy targets.

References

Ca' Zorzi, M., Dedola, L., Georgiadis, G., Jarociński, M., Stracca, L. and Strasser, G. (2020), "Monetary policy and its transmission in a globalised world", Discussion Papers, ECB Working Paper Series, No 2407, ECB, Frankfurt am Main, May.

Dedola, L., Rivolta, G. and Stracca, L. (2017), “If the Fed sneezes, who catches a cold?”, Journal of International Economics, Vol. 108, Supplement 1, pp. S23-S41.

Gerko, E. and Rey, H. (2017), “Monetary policy in the capitals of capital”, Journal of the European Economic Association, Vol. 15 No 4, pp. 721-745.

Iacoviello, M. and Navarro, G. (2019), “Foreign effects of higher U.S. interest rates”, Journal of International Money and Finance, Vol. 95(C), pp. 232-250.

Jarociński, M. and Karadi, P. (2020), “Deconstructing monetary policy surprises – the role of information shocks”, American Economic Journal: Macroeconomics, Vol. 12, No 2, pp. 1-43.

Melosi, L. (2017), “Signalling effects of monetary policy”, Review of Economic Studies, Vol. 84, No 2, pp. 853-884.

Nakamura, E. and Steinsson, J. (2018), “High-frequency identification of monetary non-neutrality: The information effect”, Quarterly Journal of Economics, Vol. 133, No 3, pp. 1283-1330.

Rey, H. (2016), “International channels of transmission of monetary policy and the Mundellian trilemma”, IMF Economic Review, Vol. 64, No 1, pp. 6-35.

- This article was written by Michele Ca’ Zorzi, Georgios Georgiadis and Livio Stracca (all Directorate General International and European Relations, ECB) and Luca Dedola, Marek Jarociński and Georg Strasser (all Directorate General Research, ECB). The authors gratefully acknowledge comments from Michael Ehrmann, Alexander Popov and Zoë Sprokel. The views expressed here are those of the authors and do not necessarily represent the views of the ECB.

- See,for example, Dedola et al. (2017), Gerko and Rey (2017), or Iacoviello and Navarro (2019).

- These are fluctuations in interest rates which reflect changes in the perceived central bank assessment of the economic outlook (see Melosi, 2017; Nakamura and Steinsson, 2018; Jarociński and Karadi 2020). Such shocks have been shown to play a role in driving the business cycle.

- The estimation approach and technical details are described in Ca’ Zorzi et. al. (2020).

- Estimates for shorter periods, such as the period of the expanded asset purchase programme, would not be reliable with the methodology used. Using longer-term swaps for recent years to try to better capture the effect of unconventional monetary policy does not change the results.

- Impulse responses for trade and other variables can be found in Ca’ Zorzi et. al. (2020).