Update on economic, financial and monetary developments

Summary

The euro area economy is continuing to recover and the labour market is improving further, helped by ample policy support. But growth is likely to remain subdued in the first quarter of 2022, as the current pandemic wave is still weighing on economic activity. Shortages of materials, equipment and labour continue to hold back output in some industries. High energy costs are hurting incomes of euro area households and earnings of firms and are likely to dampen spending. However, the economy is affected less and less by each wave of the pandemic and the factors restraining production and consumption should gradually ease, allowing the economy to pick up again strongly in the course of the year.

Inflation has risen sharply in recent months and further surprised to the upside in January. This is primarily being driven by higher energy costs that are pushing up prices of goods and services across many sectors, as well as by higher food prices. Inflation is likely to remain elevated for longer than previously expected, but to decline in the course of this year.

The Governing Council therefore confirmed the decisions taken at its monetary policy meeting last December. Accordingly, the Governing Council will continue reducing the pace of its asset purchases step by step over the coming quarters, and will end net purchases under the pandemic emergency purchase programme (PEPP) at the end of March. In view of the current uncertainty, the Governing Council needs more than ever to maintain flexibility and optionality in the conduct of monetary policy. The Governing Council stands ready to adjust all of its instruments, as appropriate, to ensure that inflation stabilises at the ECB’s 2% target over the medium term.

Economic activity

Global economic activity remained resilient in the fourth quarter of last year. Survey data point to robust economic growth towards the end of 2021, although growth in trade continued to be subdued. Supply chain bottlenecks showed tentative signs of easing. However, the emergence of the Omicron variant of the coronavirus (COVID-19) and the potential for pandemic-related employee absences could result in further supply chain disruptions and pose risks to global economic activity in the near term. Global inflation continued to rise, reflecting higher energy prices and a broadening of price pressures across sectors. Global inflationary pressures are expected to ease over the course of 2022, as it is anticipated that energy prices will moderate.

Euro area economic growth weakened to 0.3%, quarter on quarter, in the final quarter of last year. Nevertheless, output reached its pre-pandemic level at the end of 2021. Economic activity and demand will likely remain muted in the early part of this year for several reasons. First, pandemic containment measures are affecting consumer services, especially in the travel, tourism, hospitality and entertainment sectors. Although infection rates are still very high, the impact of the pandemic on economic life is now proving less damaging. Second, high energy costs are reducing the purchasing power of households and the earnings of businesses, which constrains consumption and investment. And, third, shortages of equipment, materials and labour in some sectors continue to hamper the production of manufactured goods, delay construction and hold back the recovery in parts of the services sector. There are signs that these bottlenecks may be starting to ease, but they will still persist for some time.

Looking beyond the near term, growth should rebound strongly in the euro area over the course of 2022, driven by robust domestic demand. As the labour market is improving further, with more people having jobs and fewer in job retention schemes, households should enjoy higher income and spend more. The global recovery and the ongoing fiscal and monetary policy support also contribute to this positive outlook. Targeted and productivity-enhancing fiscal measures and structural reforms, attuned to the conditions in different euro area countries, remain key to complement monetary policy effectively.

Inflation

Inflation in the euro area increased to 5.1% in January 2022, from 5.0% in December 2021. It is likely to remain high in the near term. Energy prices continue to be the main reason for the elevated rate of inflation. Their direct impact accounted for over half of headline inflation in January and energy costs are also pushing up prices of goods and services across many sectors. Food prices have also increased, owing to seasonal factors, elevated transportation costs and the higher cost of fertilisers. In addition, price rises have become more widespread, with the prices of a large number of goods and services having increased markedly. Most measures of underlying inflation have risen over recent months, although the role of temporary pandemic factors means that the persistence of these increases remains uncertain. Market-based indicators suggest a moderation in energy price dynamics in the course of 2022 and price pressures stemming from global supply bottlenecks should also subside.

Labour market conditions are improving further, although wage growth remains muted overall. Over time, the return of the economy to full capacity should support faster growth in wages. Market-based measures of longer-term inflation expectations have remained broadly stable at rates just below 2% since the Governing Council’s previous monetary policy meeting In December. The latest survey-based measures stand at around 2%. These factors will also contribute further to underlying inflation and will help headline inflation to settle durably at the ECB’s 2% target.

Risk assessment

The Governing Council continues to see the risks to the euro area economic outlook as broadly balanced over the medium term. The economy could perform more strongly than expected if households become more confident and save less than expected. By contrast, although uncertainties related to the pandemic have abated somewhat, geopolitical tensions have increased. Furthermore, persistently high costs of energy could exert a stronger than expected drag on consumption and investment. The pace at which supply bottlenecks are resolved is a further risk to the outlook for growth and inflation. Compared with the Governing Council’s expectations in December, risks to the inflation outlook are tilted to the upside, particularly in the near term. If price pressures feed through into higher than anticipated wage rises or the economy returns more quickly to full capacity, inflation could turn out to be higher.

Financial and monetary conditions

Market interest rates have increased since the December 2021 Governing Council meeting. However, bank funding costs have so far remained contained. Bank lending rates for firms and households continue to stand at historically low levels and financing conditions for the economy remain favourable. Lending to firms has picked up across all maturities. Robust demand for mortgages is sustaining lending to households. Banks are now as profitable as they were before the pandemic and their balance sheets remain solid.

According to the latest euro area bank lending survey, loan demand by firms increased strongly in the last quarter of 2021. This was driven by both higher working capital needs – stemming from supply bottlenecks – and increased financing of longer-term investment. In addition, banks continue to hold an overall benign view of credit risks, mainly because of their positive assessment of the economic outlook.

Monetary policy decisions

Against this background, at its monetary policy meeting in February, the Governing Council therefore confirmed the decisions taken at its previous meeting last December.

In the first quarter of 2022 the Governing Council is conducting net asset purchases under the PEPP at a lower pace than in the previous quarter. It will discontinue net asset purchases under the PEPP at the end of March 2022.

The Governing Council intends to reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

The pandemic has shown that, under stressed conditions, flexibility in the design and conduct of asset purchases has helped to counter the impaired transmission of monetary policy and made the Governing Council’s efforts to achieve its goal more effective. Within the Governing Council’s mandate, under stressed conditions, flexibility will remain an element of monetary policy whenever threats to monetary policy transmission jeopardise the attainment of price stability. In particular, in the event of renewed market fragmentation related to the pandemic, PEPP reinvestments can be adjusted flexibly across time, asset classes and jurisdictions at any time. This could include purchasing bonds issued by the Hellenic Republic over and above rollovers of redemptions in order to avoid an interruption of purchases in that jurisdiction, which could impair the transmission of monetary policy to the Greek economy while it is still recovering from the fallout from the pandemic. Net purchases under the PEPP could also be resumed, if necessary, to counter negative shocks related to the pandemic.

In line with the step-by-step reduction in asset purchases decided on in December 2021 and to ensure that the monetary policy stance remains consistent with inflation stabilising at the Governing Council’s target over the medium term, monthly net purchases under the asset purchase programme (APP) will amount to €40 billion in the second quarter of 2022 and €30 billion in the third quarter. From October onwards, the Governing Council will maintain net asset purchases under the APP at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of its policy rates. The Governing Council expects net purchases to end shortly before it starts raising the key ECB interest rates.

The Governing Council also intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates and, in any case, for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The Governing Council will continue to monitor bank funding conditions and ensure that the maturing of operations under the third series of targeted longer-term refinancing operations (TLTRO III) does not hamper the smooth transmission of its monetary policy. The Governing Council will also regularly assess how targeted lending operations are contributing to its monetary policy stance. As announced, it expects the special conditions applicable under TLTRO III to end in June this year. The Governing Council will also assess the appropriate calibration of its two-tier system for reserve remuneration so that the negative interest rate policy does not limit banks’ intermediation capacity in an environment of ample excess liquidity.

The Governing Council also confirmed its other measures to support the ECB’s price stability mandate, namely the level of the key ECB interest rates and the forward guidance on the future path of policy rates. This is crucial for maintaining the appropriate degree of accommodation to stabilise inflation at the ECB’s 2% inflation target over the medium term.

The Governing Council stands ready to adjust all of its instruments, as appropriate, to ensure that inflation stabilises at the ECB’s 2% target over the medium term.

1 External environment

Global economic activity remained resilient in the fourth quarter of last year. Survey data point to robust economic growth towards the end of 2021, although growth in trade continued to be subdued. Supply chain bottlenecks showed tentative signs of easing. However, the emergence of the Omicron variant and potential pandemic-related staff absences pose risks to further supply chain disruptions and global economic activity in the near term. Global inflation continued to rise, reflecting higher energy prices and a broadening of price pressures across sectors. Global inflationary pressures are expected to ease over the course of 2022, as it is anticipated that energy prices will moderate.

Global economic growth remained robust in the fourth quarter of 2021. The global composite output Purchasing Managers’ Index (PMI) – excluding the euro area – remained stable and above its long-term average in the fourth quarter of 2021, reflecting steady demand (Chart 1). Nevertheless, the outbreak of the Omicron variant and its higher transmissibility began to weigh in December on the service sector in key economies, including the United Kingdom. With coronavirus (COVID-19) containment measures becoming significantly more stringent across many countries around the turn of the year, a temporary slowdown in economic activity is expected for the first quarter of 2022, as already signalled by a weakening in the manufacturing PMI for January.

Chart 1

Global output PMI (excluding the euro area)

(diffusion indices)

Sources: Markit and ECB staff calculations.

Note: The latest observations are for December 2021 (composite and services indices) and January 2022 for the manufacturing index.

Global supply bottlenecks show tentative signs of easing amid increased uncertainty due to pandemic developments. Global supplier delivery times improved in November and December. At the same time, some of the improvements reversed in January, and supplier delivery times remain near the extreme values observed during the global lockdown in the second quarter of 2020. Shipping costs along certain major trade routes are falling, and global car production recovered somewhat in the fourth quarter of 2021. Nevertheless, the onset of the highly infectious Omicron variant, and the related prospect of coronavirus-related staff absentee rates amid already tight labour conditions, implies a risk that supply constraints could re-intensify in the near term.

World trade growth remains subdued. While month-on-month growth in global (excluding the euro area) merchandise import volumes increased in November, the growth momentum in global trade remains weak. Meanwhile, the global PMI for manufacturing new export orders (excluding the euro area) again fell into contractionary territory in January 2022, pointing to subdued growth in global trade at the beginning of 2022 (Chart 2).

Chart 2

Surveys and global trade in goods (excluding the euro area)

(left-hand scale: three-month-on-three-month percentage changes; right-hand scale: diffusion indices)

Sources: Markit, CPB Netherlands Bureau for Economic Policy Analysis and ECB calculations.

Note: The latest observations are for November 2021 for global merchandise imports and January 2022 for the PMIs.

Global price pressures remained elevated in November. Annual consumer price inflation in the member countries of the Organisation for Economic Co-operation and Development (OECD) increased to 5.8% in November. While energy price inflation reached the highest level observed over the past four decades, inflation excluding energy and food also rose to 3.8% in November, up from 3.2% in the previous month. Looking ahead global inflationary pressures are expected to ease in the course of the year, as it is anticipated that energy prices will moderate from current high levels.

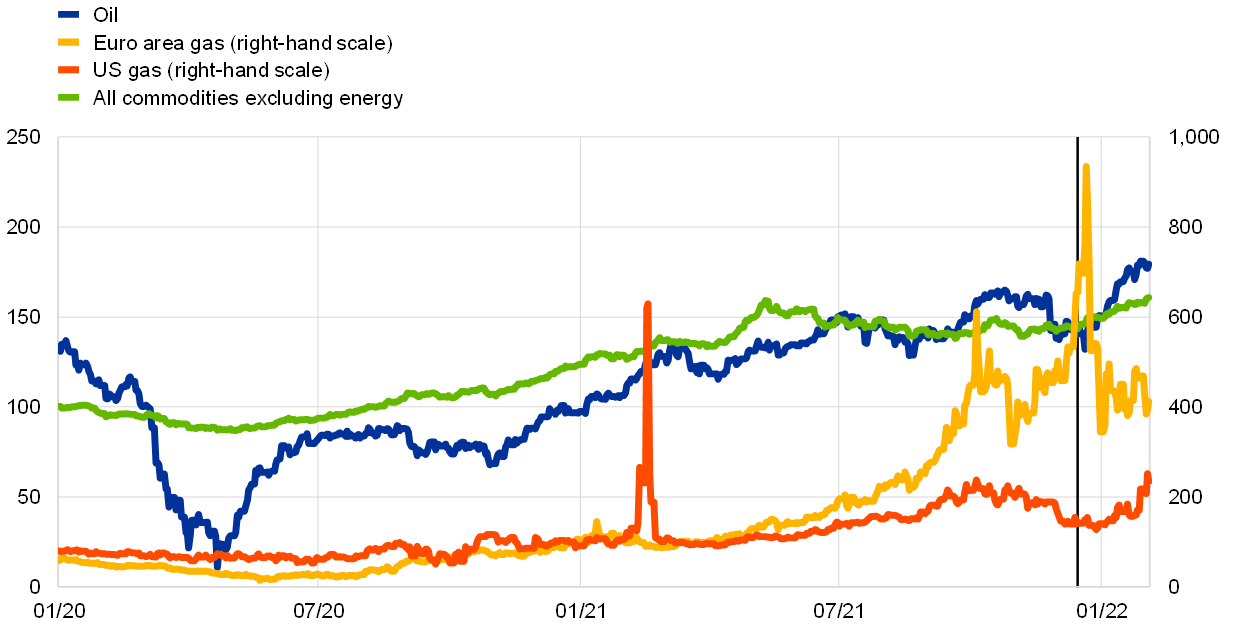

Oil prices increased amid demand and supply factors. Oil prices have rebounded by 28% since the Governing Council meeting in December, as oil markets appear to reflect the prevailing optimism that the Omicron variant will not impact global oil demand as much as previously feared. On the supply side, OPEC+ failed to meet production targets in December and, according to the U.S. Energy Information Administration,[1] is unlikely to reach the 2022 target given the difficulties encountered by some countries in bringing back idled capacity. Non-energy commodity prices have also increased since the Governing Council meeting in December owing to rises in both metal prices (+13%) and food prices (+6%) (Chart 3).

Chart 3

Commodity price developments

(index 2015=100)

Sources: Bloomberg, HWWI and ECB calculations.

Notes: Euro area gas refers to the Dutch TTF gas price, while US gas refers to the Henry Hub Natural Gas spot price. The grey vertical line marks the date of the Governing Council meeting in December 2021. The latest observation is for 3 February 2022.

Economic activity in the United States remained resilient, with increased near-term risks to the outlook from an intensification of the pandemic. Annualised GDP growth increased to 6.9% in the fourth quarter of 2021, driven in part by a strong rise in inventories, and private consumption accelerated to above pre-pandemic growth rates. The increase in consumption was primarily driven by services. At the same time, the emergence of the Omicron variant is expected to weigh on services, although the impact is expected to be largely confined to the first quarter of 2022. Meanwhile, the labour market remains tight amid labour supply shortages. Labour market tightness has translated into intensifying wage pressures. Annual headline consumer price inflation rose to 7.0% in December, its fastest pace since 1982. Energy prices remain an important driver, while persisting supply bottlenecks continue to contribute to higher prices. In response to the tight labour market and high inflation, the Federal Reserve signalled a tighter stance at its December meeting. The pace of tapering of monthly asset purchases accelerated as of January 2022, and interest rates are expected to rise over the course of the year. With regard to fiscal policy, the Build Back Better Act suffered a setback. The bill has been stalled in the Senate since November, and the fiscal impulse to growth is expected to fade much faster than previously anticipated.

In Japan, the economic recovery resumed in the final quarter of 2021. After the contraction observed in the summer of last year, economic activity remained steady in the fourth quarter, supported primarily by pent-up demand. Manufacturing rebounded significantly towards the end of 2021, in part reflecting increased production in the auto sector. While the recovery is expected to continue into the first quarter of 2022, the onset of Omicron has added headwinds to growth. The December PMI levels eased slightly for both manufacturing and services, perhaps signalling some moderation in the recovery amid lingering supply pressures and concerns regarding the spread of the new variant.

In the United Kingdom, economic activity recovered but is expected to remain subdued in the fourth quarter. Real activity surpassed its pre-pandemic level for the first time in November, supported by increasing momentum across all industry sectors. Manufacturing and construction recovered as raw materials became easier to obtain and supply chain disruptions started to ease. With December output expected to show another setback related to the Omicron variant, the pace of recovery in the fourth quarter is likely to remain weak. Meanwhile, inflation increased further in December. Annual consumer price inflation rose to 5.4% in December, from 5.1% in November. Inflation excluding food and energy also increased to 4.2% in December, from 4.0% in the previous month. Inflationary pressures have broadened to most industries and are expected to remain sustained in the coming months. The Bank of England increased its policy rate from 0.1% to 0.25% at its Monetary Policy Committee meeting in December, taking into consideration the growing tightness in the labour market and signs of greater persistence of domestic price pressures.

In China, the growth momentum remains fragile. In the fourth quarter of last year, China’s GDP growth increased to 1.6% quarter on quarter, which brings annual growth for 2021 to 8.1%. However, monthly indicators point to a slowdown in economic activity. Retail sales remained subdued towards the end of last year, underscoring the difficulty of consumption returning to pre-pandemic levels amidst China’s strict COVID-19 containment strategy. The turmoil in China’s residential property industry continued at the end of 2021, with residential real estate sales growth remaining negative in December and house prices weakening further. The emergence of the Omicron variant is posing risks to growth in the near term. Should an intensification of the pandemic lead to rising infection rates, China’s zero-COVID strategy may imply significantly stricter containment measures, which would weigh further on economic activity.

2 Financial developments

Since the December 2021 Governing Council meeting, global financial markets have primarily reflected stronger expectations of global monetary policy tightening. As a result, the euro short-term rate (€STR) forward curve has steepened further, bringing the expected date of a first rate increase forward to August 2022 and indicating that markets also expect a faster pace of rate normalisation after the lift-off. Likewise, longer-term nominal risk-free rates – and with them sovereign bond yields – rose throughout the review period. Equity prices for non-financial corporations decreased on balance, while there was little change in corporate bond spreads. At the beginning of the review period, stock prices were supported by waning concerns about the economic consequences of the Omicron variant of the coronavirus (COVID-19). However, sustained pressure from higher discount rates and, in particular, increasing concerns about the emerging geopolitical risks led to pronounced declines in equity prices towards the end of the review period. The euro depreciated in trade-weighted terms.

The benchmark €STR averaged -58 basis points over the review period. Excess liquidity increased by approximately €143 billion to €4,520 billion, mainly reflecting an increase of around €87 billion[2] in the securities held for monetary purposes under the pandemic emergency purchase programme and the asset purchase programme, as well as the €51.97 billion take-up of the tenth operation under the third series of targeted longer-term refinancing operations (TLTRO III) on 22 December 2021. This growth in excess liquidity was curtailed substantially by early repayments amounting to €60.21 billion worth of funds borrowed under previous TLTRO III operations.

The €STR forward curve has shifted up markedly compared with just before the December Governing Council meeting, suggesting a significant repricing of rate hike expectations by market participants.[3] The €STR overnight index swap (OIS) forward curve has moved up noticeably since the December Governing Council meeting, reflecting waning concerns about the economic impact of the Omicron variant and market participants increasingly pricing in a global tightening of monetary policy, particularly in the United States. Overall, the market-implied rate lift-off date – defined as the time when the €STR forward curve surpasses the current level of the €STR plus 10 basis points – has been brought forward to the third quarter of 2022 as opposed to the end of 2022 as was being priced in at the time of the December Governing Council meeting.

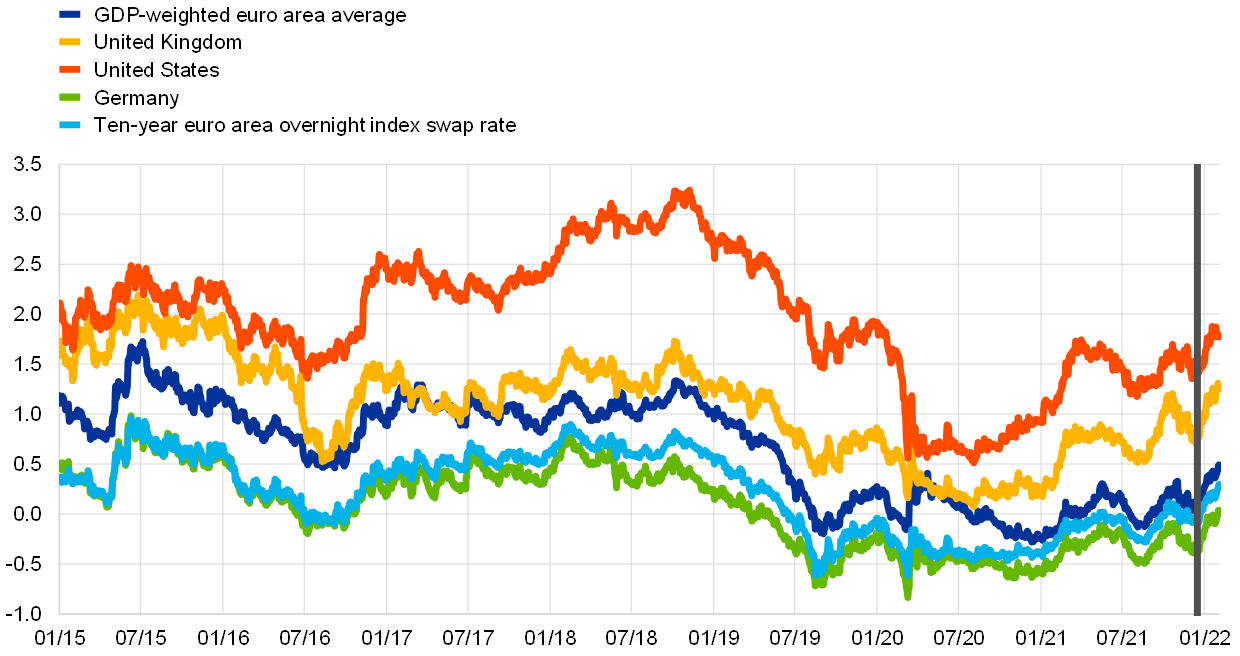

Long-term sovereign bond yields edged up, broadly mirroring the development of nominal risk-free rates (Chart 4). During the period under review, the average GDP-weighted euro area and German ten-year sovereign bond yields increased by 41 basis points and 38 basis points, up to 0.49% and 0.04% respectively. Over the same period, ten-year US government bond yields went up by 35 basis points to 1.77%, while ten-year UK government bond yields rose by 50 basis points to 1.26%.

Chart 4

Ten-year sovereign bond yields

(percentages per annum)

Sources: Refinitiv and ECB calculations.

Notes: The vertical grey line denotes the start of the review period on 16 December 2021. The latest observations are for 2 February 2022.

Long-term euro area sovereign bond spreads relative to OIS rates remained broadly unchanged. The German ten-year sovereign bond spread remained almost unchanged, standing at -0.26% at the end of the review period. Ten-year sovereign bond spreads in France and Spain also moved within a very narrow range, widening by 7 basis points and 3 basis points to 0.16% and 0.5% respectively, and the Italian sovereign bond spread edged up by 7 basis points. Overall, changes in the average sovereign bond spreads relative to risk-free rates were limited, as also reflected in the aggregate ten-year euro area GDP-weighted sovereign bond spread, which widened by only 4 basis points to 0.20%. This overall limited movement may reflect some improvement in risk sentiment amid waning concerns about the Omicron variant.

After temporarily increasing, equity prices of non-financial corporations declined on balance over the review period, likely reflecting pressure from the increase in discount rates and rising geopolitical risks. At the beginning of the review period, stock prices were supported by waning concerns about the economic consequences of the Omicron variant, as lower equity risk premia offset the drag from higher discount rates on the back of global monetary policy tightening expectations. However, towards the end of the review period they declined markedly, owing to sustained pressure from higher discount rates and, in particular, increasing concerns about geopolitical risks in the context of the Ukraine crisis. Against this backdrop, equity prices of euro area and US non-financial corporations fell by 1.8% and 3% respectively. In the United States bank equity prices decreased by 2.2%, while in the euro area they rose by 11.8%. This likely reflects changes in the slope of the yield curve on both sides of the Atlantic, which flattened in the United States and steepened in the euro area.

Both financial and non-financial corporate bond spreads remained broadly unchanged over the review period. Spreads on investment-grade non-financial corporate bonds fell by 2 basis points, reaching 44 basis points. Spreads on financial corporate bonds also moved within a very narrow range, rising by 2 basis points to 57 basis points. Although corporate bond spreads could have been affected by rate increases, they appear to have remained resilient, reflecting positive credit fundamentals and the ECB’s ongoing purchases.

In foreign exchange markets, the euro continued to depreciate in trade-weighted terms (Chart 5), reflecting a broad-based weakening against several major currencies. Over the review period, the nominal effective exchange rate of the euro, as measured against the currencies of 42 of the euro area’s most important trading partners, weakened by 1.1%. In terms of major currencies, the euro weakened only very mildly against the US dollar (by 0.1%) and the Chinese renminbi (by 0.2%), while it depreciated somewhat more strongly against the pound sterling (by 1.7%) and the Swiss franc (by 0.6%). At the same time, the euro depreciated substantially against the currencies of some large emerging economies, notably the Brazilian real (by 7.3%) and the Turkish lira (by 13.0%), as they recovered some of their previous losses, as well as against the currencies of most non-euro area EU Member States.

Chart 5

Changes in the exchange rate of the euro vis-à-vis selected currencies

(percentage changes)

Source: ECB.

Notes: EER-42 is the nominal effective exchange rate of the euro against the currencies of 42 of the euro area’s most important trading partners. A positive (negative) change corresponds to an appreciation (depreciation) of the euro. All changes have been calculated using the foreign exchange rates prevailing on 2 February 2022.

3 Economic activity

Following two quarters of strong expansion, euro area real GDP growth slowed in the final quarter of 2021, nonetheless reaching its pre-pandemic level by the end of the year. Economic activity and demand will likely remain muted in the early part of 2022 for several reasons. First, containment measures are affecting consumer services, notably the most contact-intensive. That said, although infection rates are still very high, the impact of the pandemic on economic life is now proving less damaging. Second, high energy costs are reducing the purchasing power of households and the earnings of businesses, which constrains consumption and investment. And third, shortages of equipment, materials and labour in some sectors continue to hamper the production of manufactured goods, delay construction and hold back the recovery in parts of the services sector. There are signs that these bottlenecks may be starting to ease, but these will still persist for some time.

Looking beyond the near term, growth should rebound strongly over the course of 2022, driven by robust domestic demand. As the labour market is improving further, with more people having jobs and fewer remaining in job retention schemes, households should enjoy higher income and spend more freely. The global recovery and the ongoing fiscal and monetary policy support also contribute to this positive outlook. Targeted, productivity-enhancing fiscal measures and structural reforms, attuned to the conditions in different euro area countries, remain key to complement the ECB’s monetary policy effectively.

The risks to the economic outlook continue to be seen as broadly balanced over the medium term. The economy could perform more strongly than expected if households become more confident and save less than expected. By contrast, although uncertainties related to the pandemic have abated somewhat, geopolitical tensions have increased. Furthermore, persistently high energy costs could exert a stronger than expected drag on consumption and investment. The pace at which supply bottlenecks are resolved is a further risk to the outlook for growth.

Following two quarters of strong expansion, euro area real GDP growth slowed in the final quarter of 2021. Economic activity increased by 0.3% in the fourth quarter of last year, representing a clear slowdown compared with the two previous quarters (Chart 6). With the latest increase in output, GDP currently stands on a par with its pre-pandemic level from the fourth quarter of 2019. Moreover, the carry-over effect to growth in 2022 amounts to 1.9%.[4] No breakdown of growth is as yet available, but short-term indicators and released country data suggest that domestic demand provided a positive contribution to growth, while net trade provided a broadly neutral contribution. As a whole, GDP is currently estimated to have risen by 5.2% in 2021, following the fall of 6.4% in 2020.

Chart 6

Euro area real GDP, composite output PMI and ESI

(left-hand scale: quarter-on-quarter percentage changes; right-hand scale: diffusion index)

Sources: Eurostat, European Commission, IHS Markit and ECB calculations.

Notes: The two lines indicate monthly developments; the bars show quarterly data. The European Commission’s Economic Sentiment Indicator (ESI) has been standardised and rescaled to have the same mean and standard deviation as the Purchasing Managers’ Index (PMI). The latest observations are for the fourth quarter of 2021 for real GDP and January 2022 for the PMI and the ESI.

Economic indicators point to GDP enjoying continued albeit slow growth in the first quarter of this year, before gaining momentum again. The deceleration in activity in the fourth quarter of last year and expectations of continued muted growth in the first quarter are in line with the new restrictions implemented on the back of the fast spread of the Omicron variant of the coronavirus. While this has had the largest impact on the services sector, activity in manufacturing and construction continues to be affected by shortages of equipment, materials and labour. In addition, high energy costs are having an adverse effect on households’ purchasing power and are exerting additional headwinds for private consumption and economic activity.[5] Companies operating in the non-financial sector broadly confirm this overall narrative about the short-term outlook, while remaining positive on the future evolution of demand (Box 6).

Turning to the most recent monthly data, industrial production rose by 2.3% month on month in November. However, the average level over October and November is still 1.3% below the average level for the third quarter. The more timely composite output Purchasing Managers’ Index (PMI) declined from 58.4 in the third quarter of 2021 to 54.3 in the fourth quarter and 52.4 in January. This downward movement reflects developments in both manufacturing and services. Manufacturing supply bottlenecks, as captured by the PMI suppliers’ delivery times, continued to increase, albeit at the slowest pace since January of last year. At the same time, the index for manufacturing stocks of purchases declined in January from its record high in the previous month, while the index for stocks of finished goods fell slightly. The European Commission’s Economic Sentiment Indicator (ESI) also declined in January compared with its average in the fourth quarter. This easing was broad-based across both countries and components, with the largest decline recorded for services.

The unemployment rate in the euro area fell in December, amid continued support from job retention schemes. The unemployment rate stood at 7.0% in December 2021, 0.1 percentage points lower than in November (Chart 7) and around 0.4 percentage points lower than before the pandemic in February 2020. The renewed containment measures introduced since November 2021 led to an increase in take-up of job retention schemes to around 1.6% of the labour force in December compared with 1.4% in November. According to the latest employment data, employment and hours worked increased by 1% and 2.2% respectively in the third quarter of 2021. However, total hours worked in the third quarter of 2021 remained 1.9% below the level recorded in the fourth quarter of 2019.

Chart 7

Euro area employment, the PMI employment indicator and the unemployment rate

(left-hand scale: quarter-on-quarter percentage changes, diffusion index; right-hand scale: percentages of the labour force)

Sources: Eurostat, IHS Markit and ECB calculations.

Notes: The two lines indicate monthly developments; the bars show quarterly data. The PMI is expressed as a deviation from 50 divided by 10. The latest observations are for the third quarter of 2021 for employment, January 2022 for the PMI and December 2021 for the unemployment rate.

Short-term labour market indicators have continued to improve. The monthly composite PMI employment indicator, encompassing industry and services, equalled the December level of 54.0 in January (flash release), thus remaining above the threshold level of 50 that indicates an expansion in employment. The PMI employment index has recovered significantly since its all-time low in April 2020 and stood in expansionary territory in January 2022 for the twelfth month in a row.

Household consumption, and especially spending on travel and hospitality services, has weakened amid the spread of the Omicron variant. After increasing by 4.3% in the third quarter of 2021, private consumption likely stagnated heading to the end of the year. The volume of retail sales in October and November increased by an average of 1.0% compared with the third quarter. This suggests ongoing growth in the consumption of goods towards the end of the year, despite a small decline in new car registrations in the fourth quarter (0.7% down on the third quarter). However, resilient spending on consumer goods may not be a reliable signal for overall consumer demand, as consumer confidence fell between September and January, while the new wave of the pandemic and related restrictions are weighing on contact-intensive services in particular. While confidence in the retail sector improved in January following a drop in December, it continued to decline in the services sector for a second consecutive month at the start of 2022. Looking ahead, demand in the services sector is projected to remain weak, particularly in contact-intensive consumer services, such as accommodation, catering and travel. In January 2022 the European Commission’s consumer survey indicated that households expected their financial situation to deteriorate further. All in all, the ongoing pandemic-related uncertainty is likely to continue weighing on the consumption of contact-intensive services over the winter months.

Corporate investment is likely to have grown modestly in the fourth quarter, despite headwinds from supply-side disruptions. In the capital goods sector, production in October and November combined rose by 0.2% over the third quarter, and the output PMI points to an expansion in activity in the fourth quarter. Confidence weakened compared with the third quarter, however, suggesting that the supply of capital goods continues to suffer from bottlenecks. The production of transport equipment remains particularly affected by shortages of semiconductors and congestion in supply chains. As a result, capacity utilisation has fallen, stocks of nearly finished goods have risen and supplier delivery times have continued to lengthen in the sector, albeit to a decreasing extent. Production of other equipment has remained more robust, with capacity utilisation high and stock-building of finished goods contained. On balance, available indicators suggest that business investment grew modestly in the fourth quarter. Looking forward, business investment growth is expected to pick up further, with the European Commission survey for the capital goods sector pointing to both confidence and export order books at record highs in January. Meanwhile, the limitations on production arising from shortages of capital and labour in the sector increased further in January compared with the Commission survey from October. While investment in the near term may suffer from protracted bottlenecks, benign demand and financing conditions should be supportive.

Housing investment rebounded in the fourth quarter, supported by strong demand but also hampered by supply bottlenecks. Following a decline in euro area housing investment in the third quarter of 2021, several short-term indicators point to a rebound in the fourth quarter. Building construction output in October and November stood 1.2% on average above its level in the third quarter. In the fourth quarter, the PMI for residential construction output advanced further into expansionary territory, while the European Commission’s construction survey reported recent trends in activity well above their long-term averages. According to survey data on limits to production, the recovery in the construction sector appears to be driven by demand tailwinds, despite persistent supply headwinds stemming especially from shortages of materials and labour. Looking ahead, the uncertain evolution of the balance between supply and demand, together with the rapid spread of the Omicron variant, makes for a high degree of uncertainty around the outlook for housing investment in the first quarter of 2022. On the one hand, shortages of materials and labour, coupled with other limitations caused by the Omicron-driven surge in COVID-19 infections, increased in January, suggesting tighter constraints on construction output. On the other hand, a large stock of accumulated savings and dynamic house prices could further sustain demand, as shown by households’ intentions to purchase and renovate houses, which stood well above their pre-pandemic levels in the first quarter of 2022.

Exports of goods experienced a mild rebound at the turn of the year, while the recovery in exports of services was held back by the spread of the Omicron variant. After a significant contraction in the third quarter of 2021, volumes of extra-euro area goods exports expanded in October, by 1.2% month on month, and deflated nominal exports suggest a further monthly increase in November. The expansion was particularly pronounced in the machinery and equipment sector and the chemicals industry, possibly reflecting a mild alleviation of supply bottlenecks. As the snarl-ups are not expected to ease significantly in the near term and forward-looking indicators deliver no signs of improvement, it seems likely that the increase in export volumes will only be temporary. At the same time, euro area import volumes rose by 1.6% month on month in October, with particularly strong nominal increases evident in both October and November. On the services side, after having gradually strengthened on the back of a temporary rebound in travel activity, indicators for exports show signs of weakening at the end of the year as the new wave of the pandemic hit exports of high-contact and travel services.

Although economic activity is likely to remain muted in the early part of this year, growth should rebound strongly over the course of 2022. As the labour market improves further, with more people having jobs and fewer remaining in job retention schemes, households should enjoy higher income and spend more freely. The global recovery and the ongoing fiscal and monetary policy support also contribute to this positive outlook. Targeted and productivity-enhancing fiscal measures and structural reforms, attuned to the conditions in different euro area countries, remain key to complement the ECB’s monetary policy effectively. Looking at more medium-term developments, Box 2 investigates potential long-term effects that current supply shortages could have on potential output growth in the euro area. Meanwhile, Box 3 shows that changes in the productivity distribution of firms over time have played a key role in explaining productivity developments in the euro area. The results of the latest round of the Survey of Professional Forecasters (conducted in early January) show that GDP growth forecasts have been revised downwards for 2022 and upwards for 2023 since the previous round, conducted in early October 2021.

4 Prices and costs

Inflation increased to 5.1% in January, from 5.0% in December 2021. It is likely to remain high in the near term. Energy prices continue to be the main reason for the elevated rate of inflation. Their direct impact accounted for over half of headline inflation in January and energy costs are also pushing up prices across many sectors. Food prices have also increased, owing to seasonal factors, elevated transportation costs and the higher price of fertilisers. In addition, price rises have become more widespread, with the prices of a large number of goods and services having increased markedly. Most measures of underlying inflation have risen over recent months, although the role of temporary pandemic factors means that the persistence of these increases remains uncertain. Market-based indicators suggest a moderation in energy price dynamics in the course of 2022 and price pressures stemming from global supply bottlenecks should also subside. Market-based measures of longer-term inflation expectations have remained broadly stable at rates just below 2% since the Governing Council’s last monetary policy meeting In December. The latest survey-based measures stand at around 2%.

HICP inflation increased further to 5.1% in January 2022 (Chart 8). According to Eurostat’s flash estimate, euro area HICP inflation increased to 5.1% in January 2022, from 5.0% and 4.9% in December and November 2021 respectively. The latest outcomes surprised to the upside. Both the further increase and the magnitude of headline inflation in January were largely due to developments in energy prices – accounting for over half of headline inflation. Although the January figure reflected a downward impact due to the base effect of the German VAT rate cut in 2020 dropping out of the inflation rate, this was more than offset by the continued upward pressures. HICP inflation excluding food and energy (HICPX) decreased to 2.3% in January, from 2.6% in December. This reflected a decline in the annual rate of change in non-energy industrial goods prices (to 2.3% in January from 2.9% in December), whereas that for services prices was unchanged at 2.4%.

Chart 8

Headline inflation and its components

(annual percentage changes; percentage point contributions)

Sources: Eurostat, ECB staff calculations and the Narrow Inflation Projection Exercise.

Notes: Components highlighted with * exclude both the impact of the changes in HICP weights in 2021 and the temporary reduction in VAT in Germany in 2020. The impact of the changes in HICP weights is estimated by the ECB. The latest observations are for December 2021. For headline HICP inflation the January 2022 flash estimate is shown.

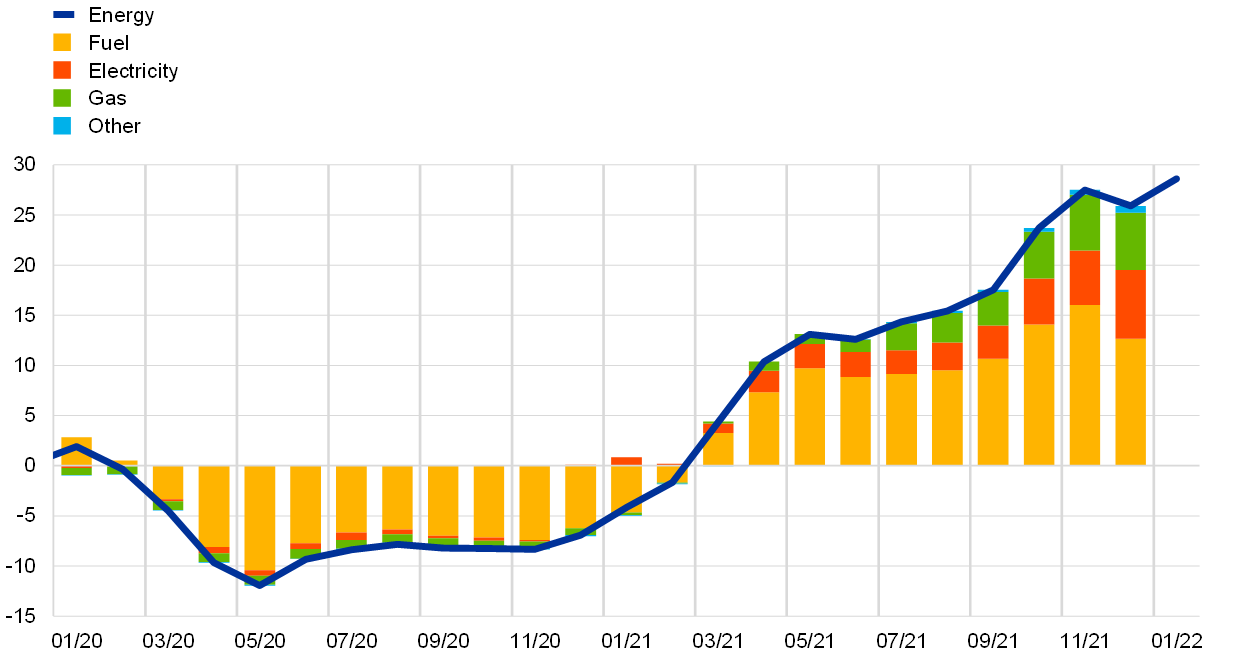

The most volatile components, energy and food, dominated the HICP inflation dynamics. Energy inflation increased in January, following the moderation in December, and reached a new historical high of 28.6%. Components of energy price inflation are available until December, and suggest that gas and electricity prices increasingly explain the overall energy inflation dynamics (Chart 9). The greater contribution from the gas component was driven by the rise in global and European wholesale gas prices (Chart 3 in Section 1). This, in turn, pushed up EU wholesale electricity prices, as electricity prices are based on the short-run marginal costs of power plants. Gas and electricity prices are also likely to have accounted for a large part of the January energy price dynamics, partly because of a surge in the prices of regulated energy products in one of the larger euro area economies. Food inflation rose further to 3.6% in January, from 3.2% in December 2021, reflecting an increase in the rate of change in the prices of both unprocessed and processed food. These dynamics may in part reflect a rise in input and production costs related to the energy price surge, but may also be linked to unfavourable weather conditions and earlier increases in EU internal market prices for food commodities.

Chart 9

Energy inflation decomposition

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: “Fuel” refers to the HICP component “liquid fuels and fuels and lubricants for personal transport equipment”. “Other” includes the items “solid fuels” and “heat energy” at the COICOP 5-digit level of aggregation. COICOP stands for classification of individual consumption according to purpose. The latest observation for overall energy is for January 2022, whereas for the contribution it is for December 2021.

Indicators of underlying inflation remained at high levels, but this partly reflects indirect effects of energy prices and temporary pandemic-related factors (Chart 10). The HICPX decreased in January to 2.3%, from 2.6% in December. The range of measures of underlying inflation moved upwards until December – the latest available data. HICP inflation excluding energy, food, travel-related items, clothing and footwear (HICPXX) rose from 2.1% in October to 2.4% in December, while the model-based Persistent and Common Component of Inflation (PCCI) went up from 2.2% to 2.7% over the same period. The Supercore indicator, which comprises cyclically sensitive items, increased for the sixth consecutive month and rose considerably, to 2.5% in December from 2.0% in October. While the whole range of indicators of underlying inflation moved above 2%, this also reflects the indirect effects of the surge in energy prices, and the impacts associated with reopening and supply bottlenecks.[6] The persistence of these increases remains uncertain, as it is unclear when the temporary pandemic factors will fade away.

Chart 10

Indicators of underlying inflation

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The range of indicators of underlying inflation includes the HICP excluding energy, HICP excluding energy and unprocessed food, HICPX (HICP excluding energy and food), HICPXX (HICP excluding energy, food, travel-related items, clothing and footwear), the 10% and 30% trimmed means and the weighted median. The latest observation is December 2021 for all the indicators except the HICPX, which has been obtained from the January 2022 flash estimate.

Pipeline pressures on prices for non-energy industrial goods continued to build up in November (Chart 11). Supply bottlenecks together with surges in global commodity prices – reinforced by the depreciation in the euro – are affecting firms’ production costs. At the earlier stages of the production and pricing chain, the annual rate of change in producer prices for domestic sales of intermediate goods rose sharply once again. It was up from 16.9% in October to 18.3% in November, while the annual rate of change in import prices for intermediate goods edged up from 17.5% in October to 17.6% in November. Pipeline pressures have spread to the later stages of the pricing chain: producer price inflation for domestic sales of non-food consumer goods again reached a new historical high, having risen from 2.7% in October to 3.1% in November. Meanwhile import price inflation for non-food consumer goods rose further from 3.2% in October to 3.7% in November, likely attributable in part to exchange rate depreciation of the euro over the past year. Recent information from the ECB’s Corporate Telephone Survey suggests that prices have been adjusted more frequently than in the past to avoid margins being squeezed and that prices will continue rising through much of 2022.[7] However, under the current pandemic circumstances, there remains considerable uncertainty about the degree of pass-through of pipeline pressures to consumer goods prices.

Chart 11

Indicators of pipeline pressures

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for November 2021.

Market-based indicators of euro area inflation expectations remained broadly unchanged over medium to longer-term horizons, whereas survey-based measures of longer-term inflation expectations edged up at the beginning of 2022. Longer-term market-based indicators of inflation compensation mostly moved sideways over the review period. Amid muted year-end trading activity, the five-year forward inflation-linked swap (ILS) rate five years ahead increased slightly, to around 2% at the beginning of January, before receding again to 1.84% at the end of the review period. This notwithstanding, markets revised up the pricing of euro area year-on-year inflation rates for the coming months. The fact that euro area HICP inflation came in above expectations for the sixth straight month in December 2021 may have further induced market participants to demand somewhat higher inflation compensation over the coming months. According to the ECB Survey of Professional Forecasters for the first quarter of 2022, which was conducted in the first week of January, longer-term inflation expectations increased further to 2.0% from 1.9% and 1.8% in the previous two survey rounds. At the same time the January Consensus Economics forecasts remained at 1.9% (Chart 12), unchanged from October 2021.

Chart 12

Survey-based indicators of inflation expectations and market-based indicators of inflation compensation

(annual percentage changes)

Sources: Eurostat, Refinitiv, Consensus Economics, ECB Survey of Professional Forecasters (SPF), Eurosystem staff macroeconomic projections for the euro area, December 2021 and ECB calculations.

Notes: The market-based indicators of the inflation compensation series are based on the one-year spot inflation rate and the one-year forward rate one year ahead, the one-year forward rate two years ahead, the one-year forward rate three years ahead and the one-year forward rate four years ahead. The latest observations for market-based indicators of inflation compensation are for 2 February 2022. The ECB Survey of Professional Forecasters for the first quarter of 2022 was conducted between 7 and 13 January 2022. The Consensus Economics cut-off date is 10 January 2022. The cut-off date for data included in the projections was 1 December 2021.

5 Money and credit

Money creation in the euro area was supported by policy measures and continued to normalise in December 2021, reflecting base effects. Eurosystem asset purchases remained the dominant source of money creation. Growth in loans to firms increased, benefiting from favourable financing conditions and the improved economic situation, although pandemic-related risks also increased. According to the latest euro area bank lending survey, in the fourth quarter of 2021 loan demand continued to rise, with credit standards tightening very slightly for loans to firms while remaining unchanged for housing loans.

In December 2021 broad money growth continued its moderating trend, which had started at the beginning of 2021. The annual growth rate of M3 declined to 6.9% in December, down from 7.4% in November (Chart 13), affected by a negative base effect linked to the exceptional increase in liquidity in December 2020. The quarterly pace of money growth moved closer to its longer-term average, with shorter-run dynamics of M3 continuing to benefit from the significant support provided by the pandemic-related policy responses. On the components side, the main driver of M3 growth was the narrow aggregate M1, which includes the most liquid components of M3. As growth rates continued to moderate from the high levels observed during 2020 – the first year of the coronavirus (COVID-19) pandemic – the annual growth rate of M1 decreased further to 9.8% in December, reflecting a normalisation in the growth of overnight deposits. Deposits of firms continued to grow solidly, while growth in household deposit flows remained below its pre-pandemic average for the third consecutive month. Other short-term deposits made a negative contribution to M3 growth, reflecting a decline in demand for time deposits, but marketable instruments provided further support owing to robust demand for money market funds.

Money creation continued to be driven by Eurosystem asset purchases. As in previous quarters, the largest contribution to M3 growth came from the Eurosystem’s net purchases of government securities under the asset purchase programme (APP) and the pandemic emergency purchase programme (PEPP) (red portion of the bars in Chart 13). Support for M3 growth also came from a higher contribution of credit to the private sector (blue portion of the bars). However, three factors dampened money creation somewhat: first, bank credit to general government made a negative contribution owing to sales of government bonds (light green portion of the bars); second, net external monetary outflows continued, coinciding with a weakening of the effective exchange rate of the euro (yellow portion of the bars); third, outflows from other counterparts outweighed the inflows from longer-term liabilities (dark green portion of the bars), which benefited from favourable conditions for targeted longer‑term refinancing operations (TLTROs).

Chart 13

M3 and its counterparts

(annual percentage changes; contributions in percentage points; adjusted for seasonal and calendar effects)

Source: ECB.

Notes: Credit to the private sector includes monetary financial institution (MFI) loans to the private sector and MFI holdings of debt securities issued by the euro area private non-MFI sector. As such, it also covers the Eurosystem’s purchases of non-MFI debt securities under the corporate sector purchase programme and the PEPP. The latest observations are for December 2021.

Growth in loans to the private sector increased in December 2021. Lending to firms and households continued to benefit from favourable financing conditions and the ongoing economic recovery. Growth in loans to the private sector rose to 4.0% in December, up from 3.6% in November, driven by lending to firms and reflecting a positive base effect (Chart 14). The annual growth rate of loans to firms rose markedly to 4.2% in December, up from 2.9% in November, supported by an increase in loans in both the short and longer-term segments. The increase in shorter-term loans is explained by the persistence of supply bottlenecks, with increased working capital needs being reinforced by higher energy costs. Robust lending at maturities beyond the short term can instead be explained by rising demand for loans to finance fixed investment. At the same time, the growth rate of loans to households edged up only slightly to 4.2% in December (Chart 14). This was mainly the result of solid mortgage lending, as consumer credit growth remained weak. Overall, loan developments mask differences across euro area countries, which, among other things, reflect the uneven impact of the pandemic and the progress of the economic recovery across countries.[8]

Chart 14

Loans to the private sector

(annual percentage changes)

Source: ECB.

Notes: Loans are adjusted for loan sales, securitisation and notional cash pooling. The latest observations are for December 2021.

According to the January 2022 euro area bank lending survey, in the fourth quarter of 2021 credit standards for loans to firms tightened very slightly, while those for housing loans remained unchanged (Chart 15). Given an overall positive assessment of the economic outlook, banks continue to hold an overall benign view on firms’ credit risks, despite higher pandemic-related risks, especially those related to supply bottlenecks. Banks reported that risk perceptions had a net easing impact on credit standards, while banks’ risk tolerance had a slight tightening impact. For housing loans, banks’ risk tolerance and their cost of funds had a slight tightening impact, whereas risk perceptions and competition had a broadly neutral impact. For the first quarter of 2022, euro area banks expect broadly unchanged credit standards for loans to firms and a further tightening of credit standards for loans to households for house purchase.

Banks reported that loan demand rose considerably in the fourth quarter of 2021. The increase in firms’ demand for loans – the largest since the extraordinary rise in loan demand in the first half of 2020 – was driven by both greater working capital needs, stemming from the rebuilding of inventories resulting from supply bottlenecks, and the financing of longer-term investment. The further increase in demand for loans to households in the fourth quarter of 2021 was supported by improved consumer confidence and the historically low level of interest rates. For the first quarter of 2022, banks expect a further rise in demand for loans to firms and for loans to households for house purchase.

The survey also suggests that, on balance, the ECB’s unconventional monetary policy measures supported banks’ credit intermediation activities. Euro area banks indicated that their access to retail and wholesale funding continued to improve in the fourth quarter of 2021, while their access to money markets, debt securities funding and securitisation was broadly unchanged. At the same time, they highlighted a continued strengthening of their capital position in 2021 against the backdrop of regulatory and supervisory actions, and a small net tightening of their credit standards for loans to firms and for consumer credit on account of non-performing loan ratios. In addition, government guarantees related to the pandemic continued to support banks’ credit standards for loans to firms in the second half of 2021.

Chart 15

Changes in credit standards and net demand for loans (or credit lines) to enterprises and households for house purchase

(net percentages of banks reporting a tightening of credit standards or an increase in loan demand)

Source: Euro area bank lending survey.

Notes: For the bank lending survey questions on credit standards, “net percentages” are defined as the difference between the sum of the percentages of banks responding “tightened considerably” or “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” or “eased considerably”. For the survey questions on demand for loans, “net percentages” are defined as the difference between the sum of the percentages of banks responding “increased considerably” or “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” or “decreased considerably”. The latest observations are for the fourth quarter of 2021.

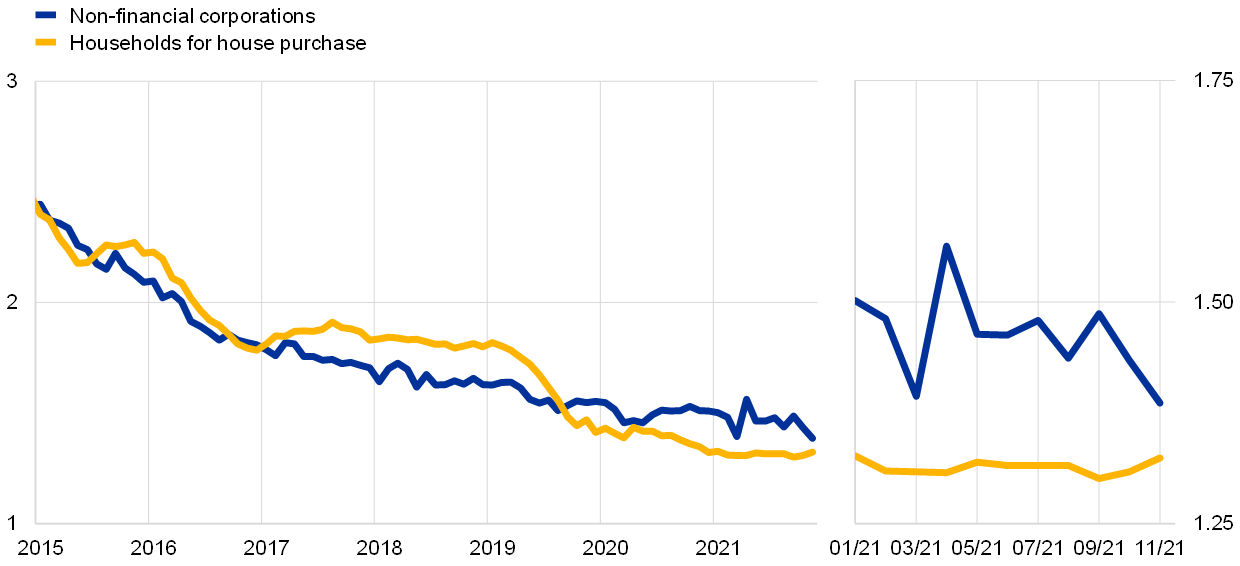

Bank lending rates continue to stand at historically low levels. In November 2021 the composite bank lending rate for loans to non-financial corporations fell back to its historical low of March 2021, when it stood at 1.39%, while the equivalent rate for loans to households for house purchase remained broadly unchanged at 1.32% (Chart 16). The decline in lending rates to firms was widespread across the largest euro area countries. Moreover, the spread between bank lending rates on very small loans and those on large loans increased again but remained below pre-pandemic levels, mainly reflecting declines in rates on large loans. The increase in bond yields is expected to be gradually transmitted to euro area yields, which would put upward pressure on domestic lending rates. The ECB’s policy measures have so far prevented a broad-based tightening of financing conditions, which would have amplified the adverse impact of the new COVID-19 variants on the euro area economy.

Chart 16

Composite bank lending rates for non-financial corporations and households

(annual percentages)

Source: ECB.

Notes: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes. The latest observations are for November 2021.

Boxes

1 Recent inflation developments in the United States and the euro area – an update

After headline inflation had already reached very high levels in the United States in the first half of 2021, euro area inflation also recorded a very rapid increase in the second half of the year but remained much lower than in the United States. Comparing inflation developments in both economic areas could help to separate idiosyncratic factors from those related to the cyclical position, taking into account the fact that the euro area is lagging the US cycle. By December 2021 inflation in the United States, as measured by the US consumer price index (CPI), had reached 7.0% (up by 5.6 percentage points since January 2021), compared with inflation in the euro area, as measured by the Harmonised Index of Consumer Prices (HICP), which stood at 5.0% (up by 4.1 percentage points since January 2021) – see Chart A.[9] Energy inflation made a 2.2 percentage point contribution to headline inflation in the United States and a 2.5 percentage point contribution in the euro area in December, thereby accounting for around half of headline inflation for the euro area and around one-third for the United States in that month.[10] In January 2022 headline inflation in the euro area – according to Eurostat’s flash release – increased slightly further to 5.1%.

More2 How persistent supply chain disruptions could affect euro area potential output

This box investigates potential long-term effects that current supply shortages could have on euro area potential output growth. Although initially assumed to be short-lived and confined to a few products (e.g. microprocessors) or countries (e.g. those that are manufacturing intensive), the supply shortages have been building up over time. Depending on the persistence of global value chain disruptions, firms might consider finding new suppliers, transport routes, locations of production and more broadly new supply chains. If this happens, sectors that have greatly benefited from international exposure and globalisation in terms of productivity growth might experience a decline in trend total factor productivity. All else being equal, this could lead to a trend decline in potential output growth for the most affected countries.

More3 Firm productivity dynamism in the euro area

This box discusses how movements of firms along the productivity distribution over time affect aggregate productivity growth.[11] The analysis is based on firm-level data for six euro area countries; the data have been treated to represent the set of non-financial corporations with employees. Firms move along the productivity distribution in accordance with their capacity to react to shocks and to structural factors that incentivise innovative investment. This applies both to low-productivity firms that are striving to survive in the market and high-productivity firms that are facing the risk of falling behind the times. Firm productivity is very dynamic across all countries, sectors and years: Chart A shows that firms fighting for survival at the bottom of the distribution (at the 5th percentile) were, on average, able to increase their productivity ranking by 30 percentiles over a 12-year period. At the same time, firms initially at the top of the distribution (at the 90th percentile) saw their productivity ranking decrease by 20 percentiles. This is significant as changes in firm productivity account, on average, for more than 60% of annual aggregate productivity growth.[12]

More4 Natural gas dependence and risks to euro area activity

Natural gas is the second most important primary energy resource in the euro area, after petroleum-based products. It is the most important source of energy in the manufacturing sector, and more than 90% of the gas consumed in the euro area is imported. The euro area is heavily dependent on imports of both petroleum-based energy products and natural gas, while renewable energy and nuclear energy are predominantly domestically produced (Chart A, panel a). From an economy-wide perspective, petroleum-based energy is the most consumed, reflecting mainly its use in the transport sector. Gas is, by contrast, the primary energy source most consumed in the industrial sector and by (non-transport) services and households (Chart A, panel b). Gas also acts as the key marginal energy resource in electricity generation, given the flexibility of gas-fired power plants and the overall gas infrastructure (e.g. network interconnections, storage capacity and liquified natural gas terminals) in responding to fluctuations in electricity demand. The transition towards renewables – where supply depends on variable weather patterns – has increased this reliance. This box examines the impact of gas price increases and a possible rationing shock on economic activity in the euro area.

More5 The role of migration in weak labour force developments during the COVID-19 pandemic

Weaker than expected developments in the labour force during the coronavirus (COVID-19) pandemic may partly reflect weak net immigration. In the third quarter of 2021 the size of the euro area labour force recovered to around its pre-pandemic level in the fourth quarter of 2019.[13] However, it remains substantially below the level expected prior to the COVID-19 outbreak. This reflects the strong impact of the pandemic on the dynamics of both the working age population and the labour force participation rate (LFPR).[14] Subdued net immigration may have been a contributory factor, stemming from moderate migrant inflow and some foreign workers resettling in their home countries. Bringing together the available data on migration for euro area countries, this box examines the role of migration in weak labour force developments during the pandemic and the longer-term implications.

More6 Main findings from the ECB’s recent contacts with non-financial companies

This box summarises the results of contacts between ECB staff and representatives of 74 leading non-financial companies operating in the euro area. The exchanges mainly took place between 10 and 19 January 2022.[15]

More7 Housing costs: survey-based perceptions and signals from price statistics

A recurring theme in the “ECB Listens” event conducted in the context of the monetary policy strategy review was the affordability of housing and the case for including more adequately the related costs in the HICP.[16] More than 80% of all respondents considered the increase in the cost of housing relevant for inflation measurement. This was addressed in the strategy review by suggesting the inclusion of owner-occupied housing (OOH) costs in inflation measurement on the basis of the net acquisition approach.[17]

More8 Public wage and pension indexation in the euro area

If the response of wages – both private and public – and pensions to an increase in inflation leads to second-round effects, then this can make an inflationary shock more persistent. Transmission is more likely where wage and pension indexation is automatic. It can, however, also play an important role in wage negotiations, especially in times of high inflation. The link through wages, particularly in the private sector, is likely to be more prominent and affect prices from both the demand and the production side; pensions are likely to impact demand through disposable income. On private wages, various recent ECB and Eurosystem analyses have concluded that the likelihood of wage-setting schemes triggering second-round effects based on inflation indexation is relatively limited in the euro area.[18] This holds in particular when inflation is driven by higher energy prices.

MoreArticles

1 Owner-occupied housing and inflation measurement

In the context of monetary policy decision-making, consumer price indices (CPIs) are prominently used as measures of inflation. The ECB’s recently published monetary policy strategy review concluded that the Harmonised Index of Consumer Prices (HICP) remains the appropriate measure for assessing price stability in the euro area. However, it also acknowledged that the inclusion of costs related to owner-occupied housing (OOH) would better represent inflation relevant for households. This article elaborates on the treatment of OOH in CPIs in general, and in the HICP in particular, with a focus on the net acquisition approach recommended by the Governing Council. The article also presents the new analytical quarterly HICP combined with the owner-occupied housing price index (OOHPI) based on ECB calculations.[19]

More2 Next Generation EU: a euro area perspective

Next Generation EU (NGEU) is a cornerstone of Europe’s common policy response to the economic challenges raised by the coronavirus (COVID-19) pandemic. The pandemic triggered a severe economic downturn in the EU and a re-intensification of cross-country divergences. In July 2020, the EU responded forcefully by announcing NGEU, an EU-wide investment and reform programme. In the short term, NGEU aims to support the recovery. In the medium term, it is designed to act as a catalyst for the modernisation of the EU economies, with positive effects on their growth, resilience and convergence. To achieve these objectives, NGEU offers financial support to the EU Member States conditional on the implementation of concrete investment and reform projects over the period 2021-26. If implemented effectively, NGEU should thus provide a significant boost to the capital stock and potential output of EU Member States.

MoreStatistics

Statistical annex© European Central Bank, 2022

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

This Bulletin was produced under the responsibility of the Executive Board of the ECB. Translations are prepared and published by the national central banks.

The cut-off date for the statistics included in this issue was 2 February 2022.

For specific terminology please refer to the ECB glossary (available in English only).

ISSN 2363-3417 (html)

ISSN 2363-3417 (pdf)

QB-BP-22-001-EN-Q (html)

QB-BP-22-001-EN-N (pdf)

- See “Short-term Energy Outlook”, U.S. Energy Administration, 8 February 2022.

- From the week ending 17 December 2021 to the week ending 4 February 2022.

- From now on, the €STR overnight index swap (OIS) forward curve will be reported instead of the EONIA OIS forward curve. This is because the EONIA was discontinued on 3 January 2022 as it no longer complied with benchmark rate regulations. The two OIS forward curves were mechanically linked as, from 2 October 2019, the EONIA was computed as the €STR plus a fixed spread of 8.5 basis points. See the box entitled “Goodbye EONIA, welcome €STR!”, Economic Bulletin, Issue 7, ECB, 2019.

- This implies that GDP would grow by 1.9% in 2022 if all quarterly growth rates this year were to have been zero (which is equivalent to the assumption that the quarterly levels of GDP remain unchanged at the same level as in the fourth quarter of 2021).

- Box 4 reviews the role of natural gas in the euro area energy mix and provides an assessment of the impact of gas price increases on activity.

- Trimmed means (which remove around 5% or 15% from each tail of the distribution of annual price changes) stand well above the target of 2% because they include some energy items with currently very high inflation rates. For further information on these and other measures of underlying inflation, see Boxes 2 and 3 in the article entitled “Measures of underlying inflation for the euro area”, Economic Bulletin, Issue 4, ECB, 2018.

- See the box entitled “Main findings from the ECB’s recent contacts with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2022.

- See the box entitled “The heterogeneous economic impact of the pandemic across euro area countries”, Economic Bulletin, Issue 5, ECB, 2021.

- To facilitate a comparison with the euro area, this box focuses on developments in CPI inflation in the United States, rather than developments in the US price index for total personal consumption expenditures (PCE). Although an indicator of HICP inflation is also available for the United States, the CPI is chosen as it allows for a greater level of detail for the analyses.

- For a discussion of developments up to August 2021, see the box entitled “Comparing recent inflation developments in the United States and the euro area”, Economic Bulletin, Issue 6, ECB, 2021.

- See also Work stream on productivity, innovation and technological progress, “Key factors behind productivity trends in EU countries”, Occasional Paper Series, No 268, ECB, September 2021, and the article entitled “Key factors behind productivity trends in euro area countries”, Economic Bulletin, Issue 7, ECB, 2021.

- There is some heterogeneity in the contribution of “within-firm” productivity growth across countries, sectors and time periods. To compute the contribution of within-firm productivity changes to annual aggregate productivity growth, see Melitz, M.J. and Polanec, S., “Dynamic Olley-Pakes productivity decomposition with entry and exit”, The RAND Journal of Economics, Vol. 46, No 2, 2015, pp. 362-375.

- According to EU Integrated European Social Statistics (IESS) data, the labour force was 0.2% smaller in the third quarter of 2021 than in the fourth quarter of 2019, as also indicated by data from the EU Labour Force Survey. The latter data source is used for the remainder of this box as it provides the necessary breakdown.

- With regard to the drivers of the recent changes in the labour force participation rate, see the box entitled “Labour supply developments in the euro area during the COVID-19 pandemic”, Economic Bulletin, Issue 7, ECB, 2021.

- For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.

- See “ECB Listens – Summary report of the ECB Listens Portal”. The survey results were collected between 24 February 2020 and 31 October 2020.

- For more on the outcome of the strategy review and the related price index, see the article entitled “Owner-occupied housing and inflation measurement” in this issue of the Economic Bulletin.

- See, for instance “The prevalence of private sector wage indexation in the euro area and its potential role for the impact of inflation on wages”, Economic Bulletin, Issue 7, ECB, 2021 and the December 2021 Eurosystem staff macroeconomic projections.

- For a more technical exposition, see Ganoulis, I. et al. “Owner-occupied housing and inflation measurement”, Statistical Paper Series, ECB, forthcoming.