Corporate saving ratios during the pandemic

Published as part of the ECB Economic Bulletin, Issue 2/2022.

This box takes stock of the evolution of the saving ratios of non-financial corporations in the euro area and in the largest euro area countries during the pandemic. It focuses on corporate savings as part of the integrated euro area accounts. A distinction is made between savings including “consumption of fixed capital”, also known as depreciation expenses, and net savings, which are often referred to as retained earnings. Corporate saving is the part of entrepreneurial income that is not distributed as dividends to shareholders. Generally, firms accumulate savings because they help protect them in the event of a financial emergency, can be used to pay for operational as well as capital expenditures, help them to access external financing, reduce financial stress, and provide a greater sense of financial freedom. Savings are important as an internal source of funding for investment. The pecking order theory of corporate finance says that firms prioritise their sources of financing, with a preference for internal financing, then debt, and equity as a last resort.[1] In addition, having a high saving ratio can make it easier for firms to borrow funds, to the extent that it suggests a firm pursues sound balance sheet management and has good business prospects. If high savings are sustained over time, however, they may also signal a lack of productive investment opportunities or unwillingness to take business risks.[2]

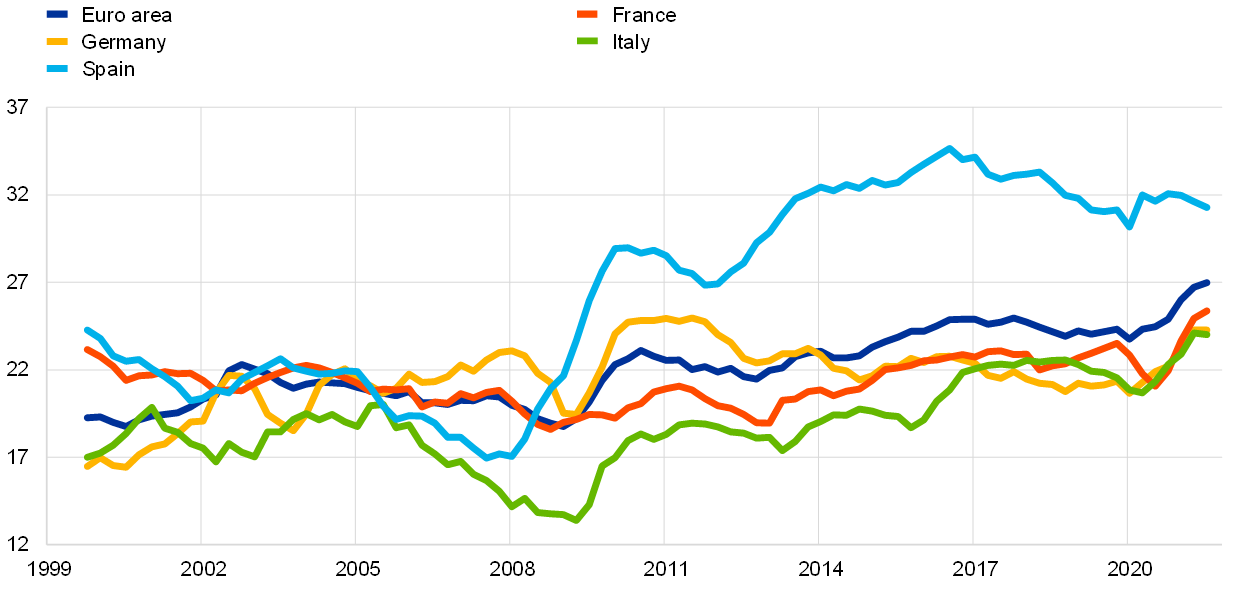

Corporate saving ratios have reached record highs in recent quarters. After previously reaching record highs in 2017, saving ratios of non-financial corporations in the euro area began a declining trend, while staying above historical averages. At the start of the COVID-19 crisis the euro area non-financial corporation gross saving ratio declined further, mainly because of falling revenues. The drop in saving was even stronger when measured in net terms, which excludes the consumption of fixed capital (Chart A, panel a). The main driver of saving was entrepreneurial income, which fell sharply in the second quarter of 2020. Since around mid-2020 saving has rebounded strongly, again predominantly driven by entrepreneurial income developments, and saving ratios have reached levels far above their average since 1999. This rebound has been heavily supported by policy measures and firms’ own efforts to improve their liquidity conditions.[3] These developments have been broad-based across countries. The non-financial corporation gross saving ratio was in recent quarters at or close to record highs in three of the four largest euro area countries, i.e. excluding Spain. Cross-country differences since the start of the pandemic reflect in part different policy support measures.[4] From a longer perspective, however, non-financial corporation saving ratios in Spain have been high compared with other countries since the global financial crisis, reflecting a strong and long-lasting corporate deleveraging process.

Chart A

Non-financial corporation saving ratio in the euro area and largest euro area countries

a) Euro area

(saving as a percentage of value added, four-quarter sums)

b) Gross saving ratio

(saving as a percentage of value added, four-quarter sums)

Sources: Eurostat, ECB and authors’ calculations.

Notes: The difference between gross and net saving is the consumption of fixed capital.

Similarly, measures of saving relative to investment in the non-financial corporate sector have rebounded strongly over recent quarters. If firms save more than they invest, they are net lenders. In the euro area, non-financial corporation net lending, i.e. saving in excess of investment, and the non-financial corporation saving-to-investment ratio have reached new highs in recent quarters (Chart B, panel a). Net lending amounted to €318 billion in the third quarter of 2021. It is unclear how permanent the increase in net lending will turn out to be; this depends on, among other factors, firms’ long-term confidence in their ability to secure external finance.[5] The rebound in net lending has been broad-based across the largest euro area countries, with all countries recording a positive value, of about ½% of GDP in France and around 3% of GDP in the other large euro area countries (Chart B, panel b). It is noteworthy that, on average since 1999, non-financial corporation net lending in the euro area has been close to zero. Similarly, non-financial corporation saving has been close to 100% of business investment, highlighting the importance of savings as a source of internal funding for investment.

Chart B

Ratios of non-financial corporation saving to investment and net lending to GDP in the euro area and largest euro area countries

a) Euro area

(four-quarter sums in percentages)

b) Net lending/borrowing-to-GDP ratio

(four-quarter sums in percentages)

Sources: Eurostat, ECB and authors’ calculations.

Notes: “Saving-to-investment ratio” refers to the ratio of gross saving to gross fixed capital formation. Negative net lending is referred to as “net borrowing”.

At the aggregate euro area level there currently appears to be no lack of internal finance available for corporate investment. Over recent quarters euro area firms have allocated a comparatively large share of their financial assets to liquid assets (Chart C, panel a). In addition, the aggregate euro area debt-to-asset and net debt-to-gross operating surplus ratios for non-financial corporations were in the third quarter of 2021 lower than in the fourth quarter of 2019, i.e. before the pandemic (Chart C, panel b). The latter ratio approximates the ratio of net debt to earnings before interest, taxes, depreciation and amortisation (EBITDA) as commonly used by credit agencies to determine the probability of a company defaulting on its debt. This ratio provides an indication of how long a company would need to operate at its current level to pay off all its debt. Against this background, the ample availability of savings, and thus internal sources of finance, for non-financial corporations at the aggregate euro area level, in combination with continued favourable external financing conditions, should support a strengthening of business investment in the period ahead.[6] On the other hand, the currently high uncertainty and the fading out of fiscal support measures might suggest that firms are maintaining higher corporate savings for precautionary motives.[7]

Chart C

Liquid asset and debt ratios for non-financial corporations in the euro area

a) Liquid assets ratio

(in percentages)

b) Debt ratios

(in percentages)

Sources: Eurostat, ECB and authors’ calculations.

Notes: “Liquid assets ratio” refers to cash and deposits as a percentage of total financial assets. “Debt-to-assets ratio” refers to non-consolidated debt as a percentage of total financial and non-financial assets. “Net debt” refers to consolidated loans plus debt securities plus insurance and pension schemes, minus liquid assets. Gross operating surplus is measured as four-quarter sums.

- For empirical evidence that the availability of internal sources of finance matters significantly for aggregate business investment in the euro area and the United States, see de Bondt, G. and Diron, M., “Investment, financing constraints and profit expectations: new macro evidence”, Applied Economics Letters, Vol. 15(8), 2008, p. 577-581. For panel evidence based on 47 countries that higher business saving is linked significantly to higher business investment, see Bebczuk, R. and Cavallo, E., “Is business saving really none of our business?”, Applied Economics, Vol. 48(24), 2016, p. 2266-2284. This study concludes that business savings and external financing are complementary sources of financing for investment.

- For example, excessive corporate savings in Japan have been linked to a lack of growth opportunities and poor corporate governance. See, for example, Tong, J. and Bremer, M., “Stock repurchases in Japan: A solution to excessive corporate saving?”, Journal of the Japanese and International Economies, Vol. 41(C), 2016, pp. 41-56; Aoyagi, C. and Ganelli, G., “Unstash the Cash! Corporate Governance Reform in Japan”, Journal of Banking and Financial Economics, Vol. 1(7), University of Warsaw, Faculty of Management, 2017, pp. 51-69; Sun, Z. and Wang, Y., “Corporate precautionary savings: Evidence from the recent financial crisis”, Quarterly Review of Economics and Finance, Vol. 56(C), 2015, pp. 175-186; and Dudley, E. and Zhang, N., ”Trust and corporate cash holdings”, Journal of Corporate Finance, Vol. 41(C), 2016, pp. 363-387.

- For more detailed descriptions, see the box entitled “Non-financial corporate health during the pandemic”, Economic Bulletin, Issue 6, ECB, 2021, and the article entitled “Assessing corporate vulnerabilities in the euro area” in this issue of the Economic Bulletin.

- For cross-country differences in the take-up of public loan guarantees, see the box entitled “Public loan guarantees and bank lending in the COVID-19 period”, Economic Bulletin, Issue 6, ECB, 2020.

- See Nakajima, K. and Sasaki, T., “Bank dependence and corporate propensity to save”, Pacific-Basin Finance Journal, Vol. 36, February 2016, pp. 150-165.

- For more disaggregated sector and size effects, see the article entitled “Assessing corporate vulnerabilities in the euro area” in this issue of the Economic Bulletin.

- See also Demary, M., Hasenclever, S. and Hüther, M., “Why the COVID-19 Pandemic Could Increase the Corporate Saving Trend in the Long Run”, Intereconomics – Review of European Economic Policy, Vol. 56, No 1, 2021, pp. 40-44; and Riddick, L.A. and Whited, T.M., “The Corporate Propensity to Save”, The Journal of Finance, Vol. 64, No 4, 2009, pp. 1729-1766. The latter study reports that firms hold higher precautionary cash balances when external finance is costly, income uncertainty is high and/or investments are large and entail costly financing. Firms are also likely to accumulate more liquid assets at times when capital productivity is low.