Liquidity conditions and monetary policy operations in the period from 31 July to 29 October 2019

Published as part of the ECB Economic Bulletin, Issue 8/2019.

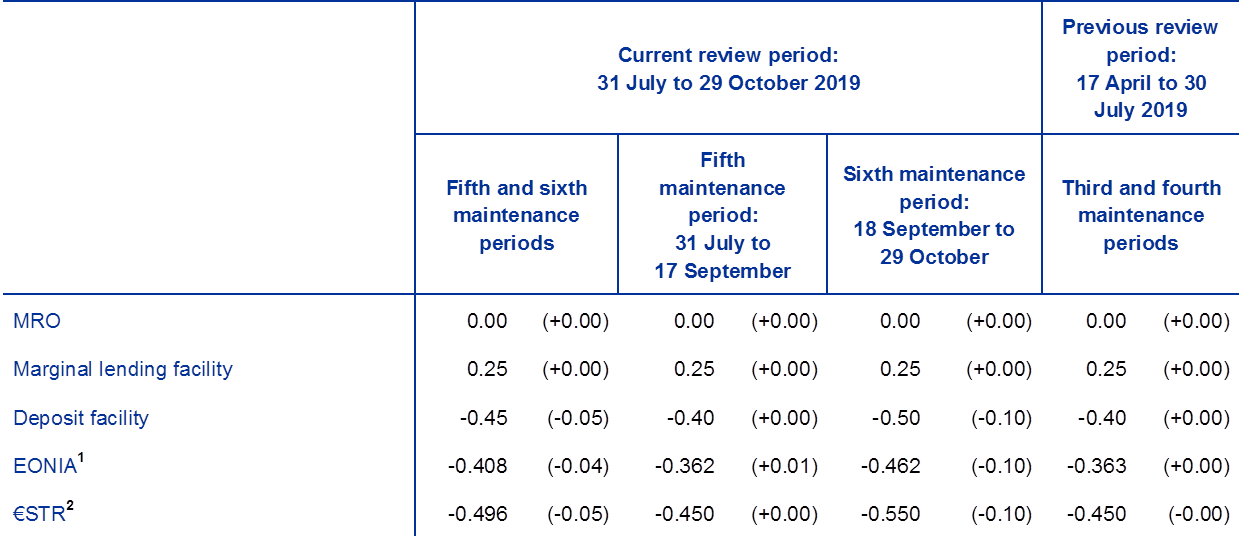

This box describes the ECB’s monetary policy operations during the fifth and sixth reserve maintenance periods of 2019, which ran from 31 July to 17 September 2019 and from 18 September to 29 October 2019, respectively. The review period encompasses the substantial package of monetary policy measures adopted by the Governing Council on 12 September 2019. The package consists of five elements: (i) a reduction in the interest rate on the deposit facility from -0.40% to -0.50%, effective from 18 September, while keeping the interest rates on the main refinancing operations (MROs) and the marginal lending facility unchanged at 0.00% and 0.25%, respectively; (ii) adjustments to the forward guidance on the key ECB interest rates; (iii) the restart of net purchases under the asset purchase programme (APP) from 1 November; (iv) modifications to the modalities of the new series of targeted longer-term refinancing operations (TLTRO III); and (v) the introduction of a two-tier system for reserve remuneration, effective as of the seventh reserve maintenance period starting on 30 October 2019. In parallel, the Eurosystem continued to reinvest, in full, the principal payments from maturing securities purchased under the APP. Furthermore, on 2 October 2019, the ECB started publishing the new overnight unsecured benchmark rate for the euro area, the euro short-term rate (€STR). From that date, the calculation methodology for the euro overnight index average (EONIA) was also changed to calculate EONIA by applying a fixed spread of 8.5 basis points to the €STR.

Liquidity needs

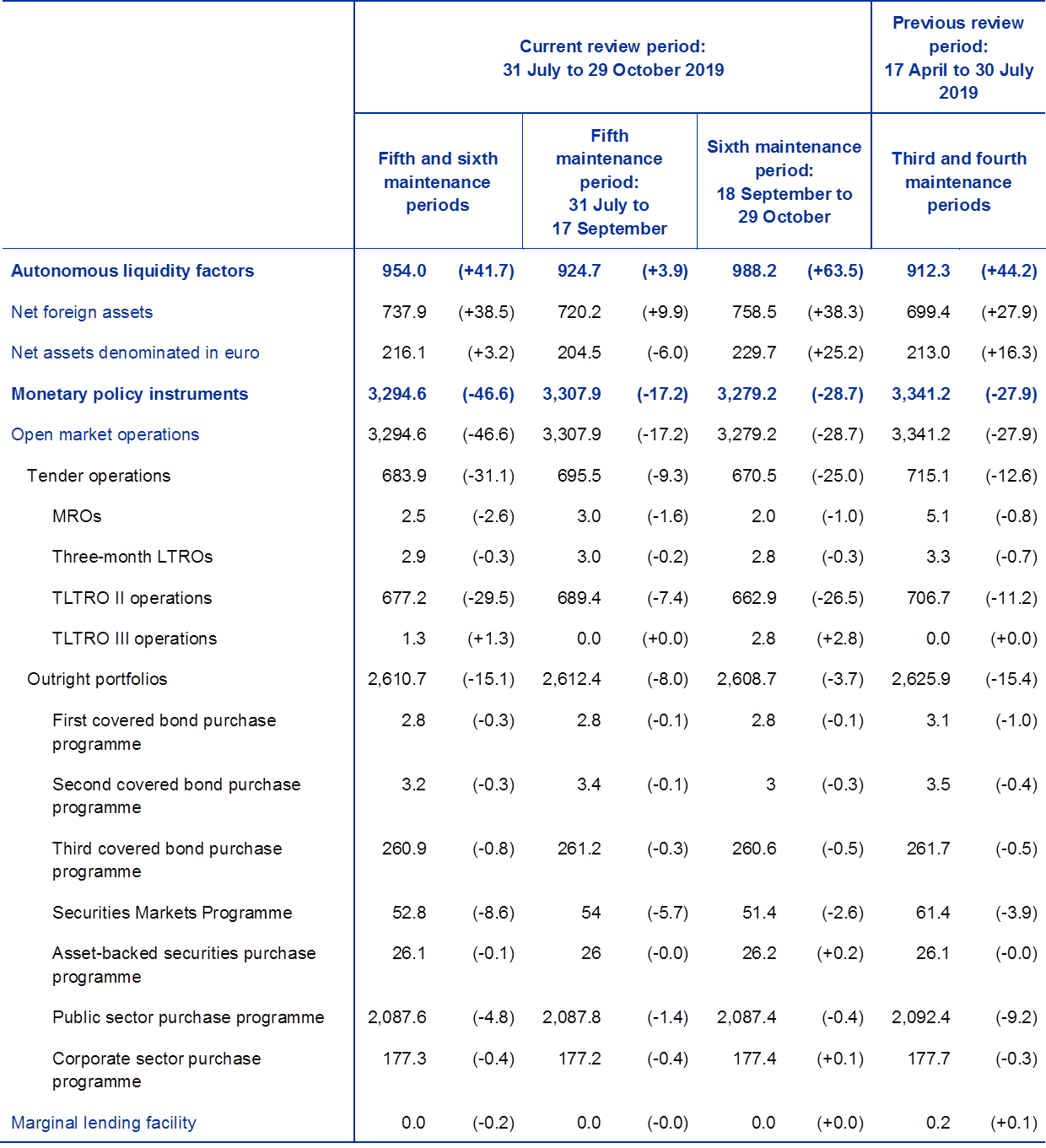

In the period under review, the average daily liquidity needs of the banking system, defined as the sum of net autonomous factors and reserve requirements, stood at €1,559.5 billion, an increase of €48.2 billion compared with the previous review period (i.e. the third and fourth reserve maintenance periods of 2019; see Table A). This change in liquidity needs was largely the result of an increase in net autonomous factors by €45.6 billion to €1,426.9 billion.

The increase in net autonomous factors was due to an increase in liquidity-absorbing factors, which more than offset the growth in liquidity-providing factors. Liquidity-absorbing factors rose mostly on account of “Other autonomous factors”, which grew on average by €57.6 billion to €846.4 billion. Banknotes in circulation increased on average by €17.8 billion to €1,251.8 billion. Government deposits rose by €11.9 billion to €282.4 billion on average over the period under review and reached a historical high of €298.6 billion in the sixth reserve maintenance period. Among liquidity-providing autonomous factors, net foreign assets grew by €38.5 billion to €737.9 billion, while net assets denominated in euro remained broadly unchanged at €216.1 billion (up by €3.2 billion). Eurosystem liabilities to non-euro area residents declined in the period under review and showed a less pronounced seasonal pattern at the end of September than at the previous quarter-end and at the end of September 2018.[1]

Table A

Eurosystem liquidity conditions

Assets

(averages; EUR billions)

Source: ECB.Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

Other liquidity-based information

(averages; EUR billions)

Source: ECB.Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.1) Computed as the sum of Net autonomous factors and Minimum reserve requirements.2) Computed as the difference between Autonomous liquidity factors on the liability side and Autonomous liquidity factors on the asset side. For the purpose of this table, “items in course of settlement” are also added to the Net autonomous factors.3) Computed as the sum of Current accounts above minimum reserve requirements and the recourse to the Deposit facility minus the recourse to the Marginal lending facility.

Interest rate developments

(averages; percentages)

Liquidity provided through monetary policy instruments

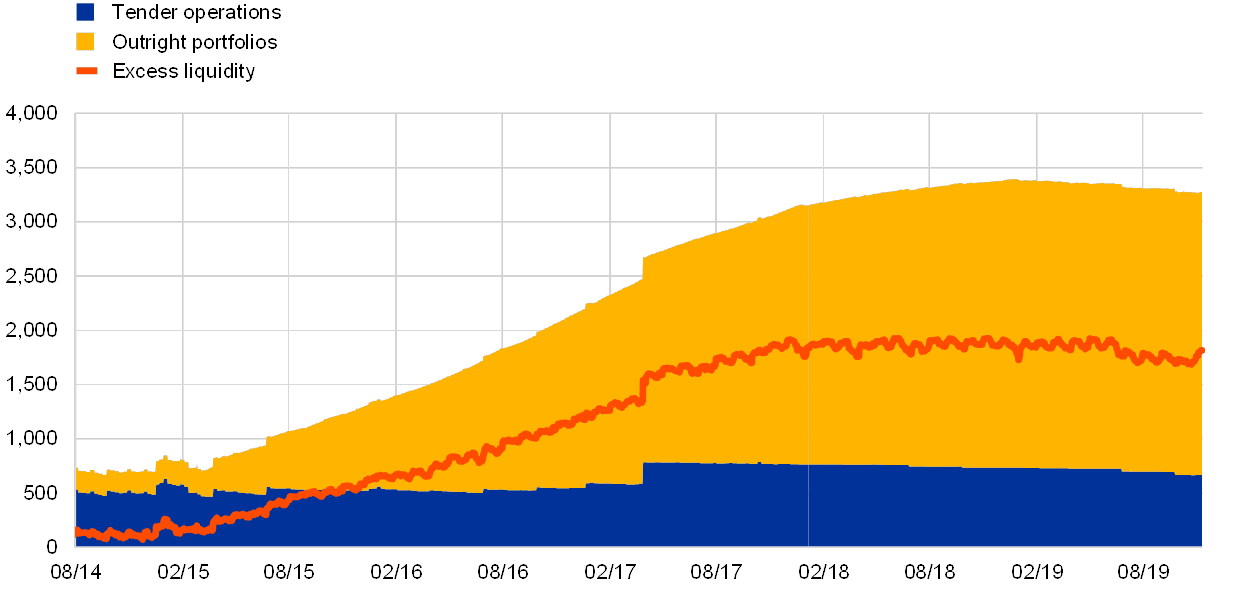

The average amount of liquidity provided through open market operations – including both tender operations and monetary policy portfolios – decreased by €46.6 billion to €3,294.6 billion (see Chart A). This decrease was driven by lower demand in tender operations as well as a smaller liquidity injection stemming from monetary policy portfolios, owing to redemptions of securities purchased in the past under the Securities Markets Programme and a small decline in the book value of the assets acquired in the public sector purchase programme (PSPP).

Chart A

Evolution of liquidity provided through open market operations and excess liquidity

(EUR billions)

Source: ECB.

The average amount of liquidity provided through tender operations declined over the review period, by €31.1 billion to €683.9 billion. This decrease was mainly attributable to lower liquidity provided through targeted longer-term refinancing operations (TLTROs). The outstanding amount borrowed under TLTRO II decreased by €29.5 billion on average in the review period as a result of voluntary early repayments of €31.8 billion that settled on 25 September. This was only partially offset by €3.4 billion allotted in the first TLTRO III operation that settled on the same day. Lower demand among counterparties also led to a decline in the provision of liquidity via MROs and via three-month longer-term refinancing operations (LTROs), which fell by €2.6 billion to €2.5 billion on average and by €0.3 billion to €2.9 billion on average, respectively.

Liquidity provided through the Eurosystem’s monetary policy portfolios decreased by €15.1 billion to €2,610.7 billion, owing to redemptions of bonds held under the Securities Markets Programme and a small decline in the PSPP. Redemptions of bonds held under the Securities Markets Programme and the first two covered bond purchase programmes totalled €9.1 billion in the review period. Regarding the APP, while net purchases had paused between 1 January 2019 and 31 October 2019, the principal payments from maturing securities continued to be reinvested. Even with full reinvestment, limited temporary deviations in the overall size and composition of the APP may occur for operational reasons.[2] As a result, the book value of the PSPP declined marginally over the review period by €4.8 billion to €2,087.6 billion on average.

Excess liquidity

As a consequence of the developments detailed above, average excess liquidity declined compared with the previous review period, by €94.5 billion to €1,735.2 billion (see Chart A). This decline reflects higher net autonomous factors and lower liquidity provision through the Eurosystem’s tender operations and monetary policy portfolios. In the sixth reserve maintenance period, recourse to the deposit facility decreased by €99.1 billion, while excess liquidity deposited at current accounts increased by €55.8 billion. The shift suggests that some intermediaries started moving funds from the deposit facility to current accounts anticipating the implementation of the two-tier system for reserve remuneration, which was announced on 12 September 2019, as the zero remuneration applies only to funds held in the current accounts. The two-tier system applies as of the seventh maintenance period starting on 30 October 2019, therefore it does not affect the remuneration of excess liquidity in the period under review. Counterparties’ eligible reserve holdings are computed on the basis of average end-of-calendar-day balances held in the institutions’ current accounts over the maintenance period.

Interest rate developments

During the review period, on 2 October, the €STR was published for the first time. [3] Based on a comparison with pre-publication data, there was no change in the €STR around the time of first publication.

The cut in the deposit facility rate to -0.50% with effect from 18 September has been transmitted to short-term money market rates. In the unsecured money market segment, the 10 basis point reduction in the deposit facility rate was fully passed through to the €STR, as it averaged -0.550% in the sixth reserve maintenance period, compared to -0.450% in the fifth reserve maintenance period.[4] EONIA also declined from -0.362% to -0.462% during the same period. The lower deposit facility rate was also transmitted to secured money market rates. From the fifth to the sixth reserve maintenance period, the average overnight repo rates for the standard and the extended collateral basket in the general collateral (GC) pooling market[5] declined by 0.097% to -0.502% and by 0.094% to -0.491%, respectively.

- Eurosystem liabilities to non-euro area residents mainly consist of euro-denominated accounts held by non-euro area central banks at national central banks of the Eurosystem. At quarter-ends non-euro area central banks generally increase their deposits at national central banks of the Eurosystem because commercial banks are less willing to accept them. Indeed, non-euro area central banks also deposit their cash at commercial banks in the euro area except at reporting dates (i.e. quarter-ends) when commercial banks tend to deflate their balance sheets. On 30 September liabilities to non-euro area residents denominated in euro increased to €252.2 billion, compared to an average of €223.1 billion during the sixth maintenance period. This implied a less pronounced effect than that observed on 30 June 2019, when these liabilities increased to €277.4 billion, compared to an average of €243.7 billion in the fourth maintenance period. A year earlier, on 30 September 2018, the same balance sheet item increased to €301.7 billion, compared to an average of €264.7 billion during the sixth maintenance period of 2018.

- See the article entitled “Taking stock of the Eurosystem’s asset purchase programme after the end of net asset purchases”, Economic Bulletin, Issue 2, ECB, 2019.

- See the box entitled “Goodbye EONIA, welcome €STR!”, Economic Bulletin, Issue 7, ECB, 2019.

- Pre-€STR data are included before 30 September 2019 for the sake of comparison.

- The GC Pooling market allows repurchase agreements to be traded on the Eurex platform against standardised baskets of collateral.