Monitoring the exchange rate pass‑through to inflation

Published as part of the ECB Economic Bulletin, Issue 4/2018.

Exchange rate developments can play an important role in shaping the outlook for HICP inflation. As a change in the exchange rate can affect consumer prices with considerable delays and as the impact can depend on the economic situation at the time, assessing the exchange rate pass-through requires constant monitoring. Between April 2017 and May 2018, the exchange rate of the euro appreciated by about 8% in nominal effective terms and by about 10% against the US dollar. This box briefly recalls how exchange rate changes are transmitted to consumer prices in the euro area. The box also looks at indicators at different stages of the pricing chain to gauge the degree of the pass-through at the current juncture. The focus is on the monitoring of the pass-through to exchange rate-sensitive components of the HICP excluding energy and food.

The exchange rate pass-through works through both direct and indirect channels.[1] For instance, the recent appreciation of the euro has a direct effect on HICP inflation through cheaper imported final consumer goods, which are part of the HICP basket. The direct effect applies for example to cheaper imports of refined oil, which entail a strong dampening impact on the HICP energy component. In addition, there can be an indirect effect as cheaper imported inputs impact domestic producer prices to the extent that these cost decreases are not absorbed by profit margins. An even more indirect effect occurs if the exchange rate appreciation dampens overall price pressures through its adverse impact on net trade and hence overall demand and output. In addition, there may be repercussions on inflation via inflation expectations. While the HICP excluding energy and food is subject to the direct channel, the indirect effects may be even more relevant for this HICP component. Overall, various factors determine the exchange rate pass‑through. These factors include the share of imported final goods and services in the price index, the importance of imported inputs (in particular, of commodities) in domestic production, product characteristics such as the degree of product differentiation, and the intensity of competition in the market. These factors can also lead to variations in the magnitude and timing of the pass‑through across HICP components. The response of prices following a change in the exchange rate may, moreover, depend on the underlying drivers of the exchange rate movement.[2]

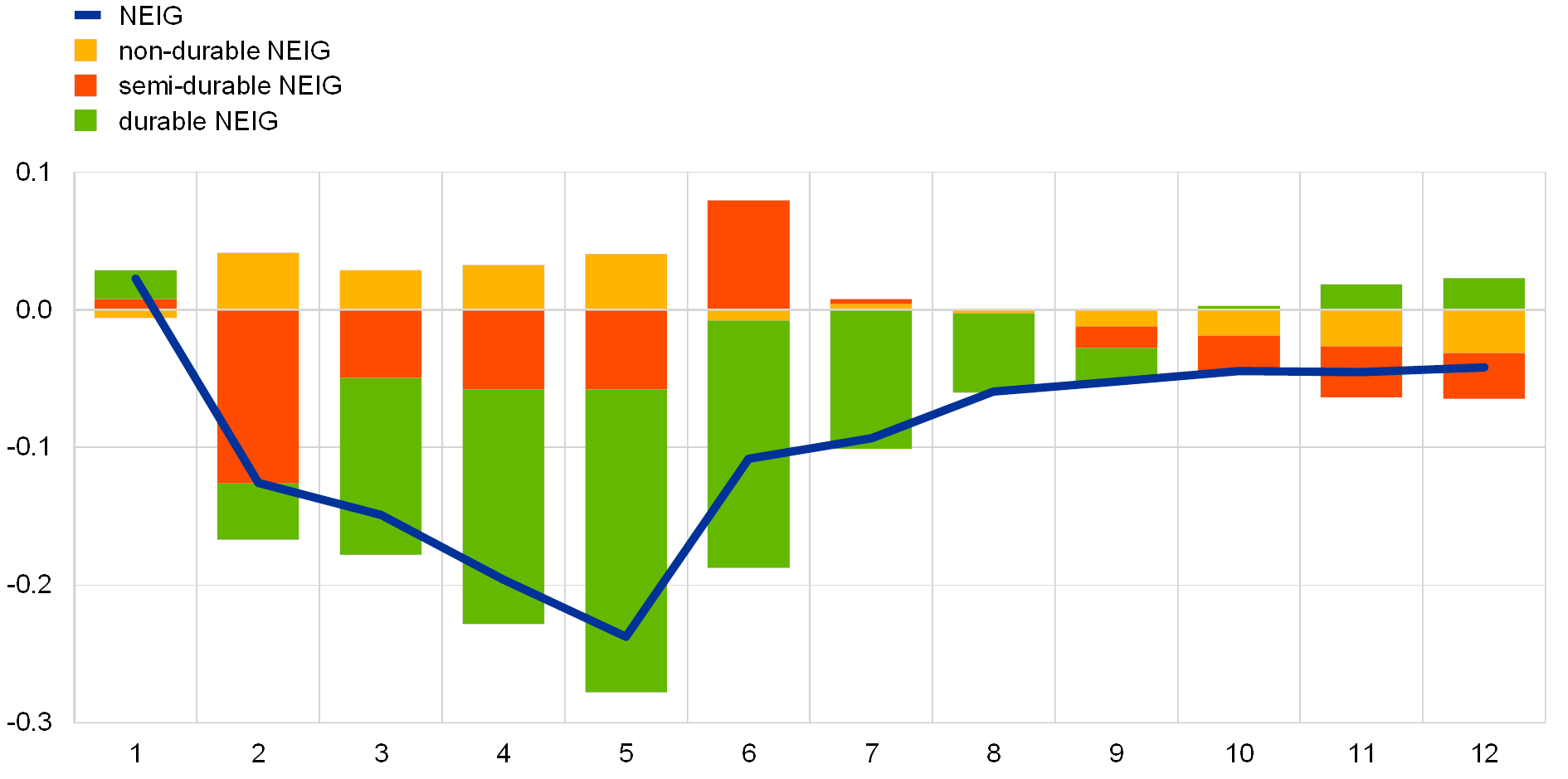

Of the components making up the HICP excluding energy and food, non‑energy industrial goods (NEIG) prices are the most sensitive to movements in the exchange rate. This is due in particular to the durable goods component (see Chart A), although there is also a high degree of heterogeneity in the exchange rate responsiveness of the prices within that component. Until exchange rate impacts become visible in these different consumer goods categories, a series of short-term indicators can be affected along the production and pricing chains and provide relevant signals.

Chart A

Estimated impact of a 10% appreciation of the nominal effective exchange rate of the euro on NEIG inflation

(annual percentage change, percentage point contribution)

Sources: Eurostat and ECB calculations.

Notes: The x-axis refers to the quarters following a change in the exchange rate. Estimates are derived from an amended and updated version of the VAR model presented in Hahn, E., “Pass-through of external shocks to euro area inflation”, Working Paper Series, No 243, ECB, July 2003.

The impact of the past euro exchange rate appreciation has been clearly visible in import price developments. Extra-euro area import prices for non-food consumer goods declined in annual terms from 1.3% in April 2017 to ‑2.0% in April 2018. These imports account for approximately 12% of final non-energy and non-food goods consumption, with only distribution and retail margins separating their prices from consumer prices. Over the same period, extra-euro area import price inflation for industry (excluding energy and construction), which also affect prices earlier in the domestic production chain, decreased from 3.1% to ‑1.7% (see Chart B). These declines reflected to a large extent the influence of the appreciation of the euro effective exchange rate.

Chart B

Import prices and nominal effective exchange rate

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for May 2018 for the nominal effective exchange rate of the euro against 38 of its main trading partners (NEER-38) and April 2018 for the extra-euro area import prices.

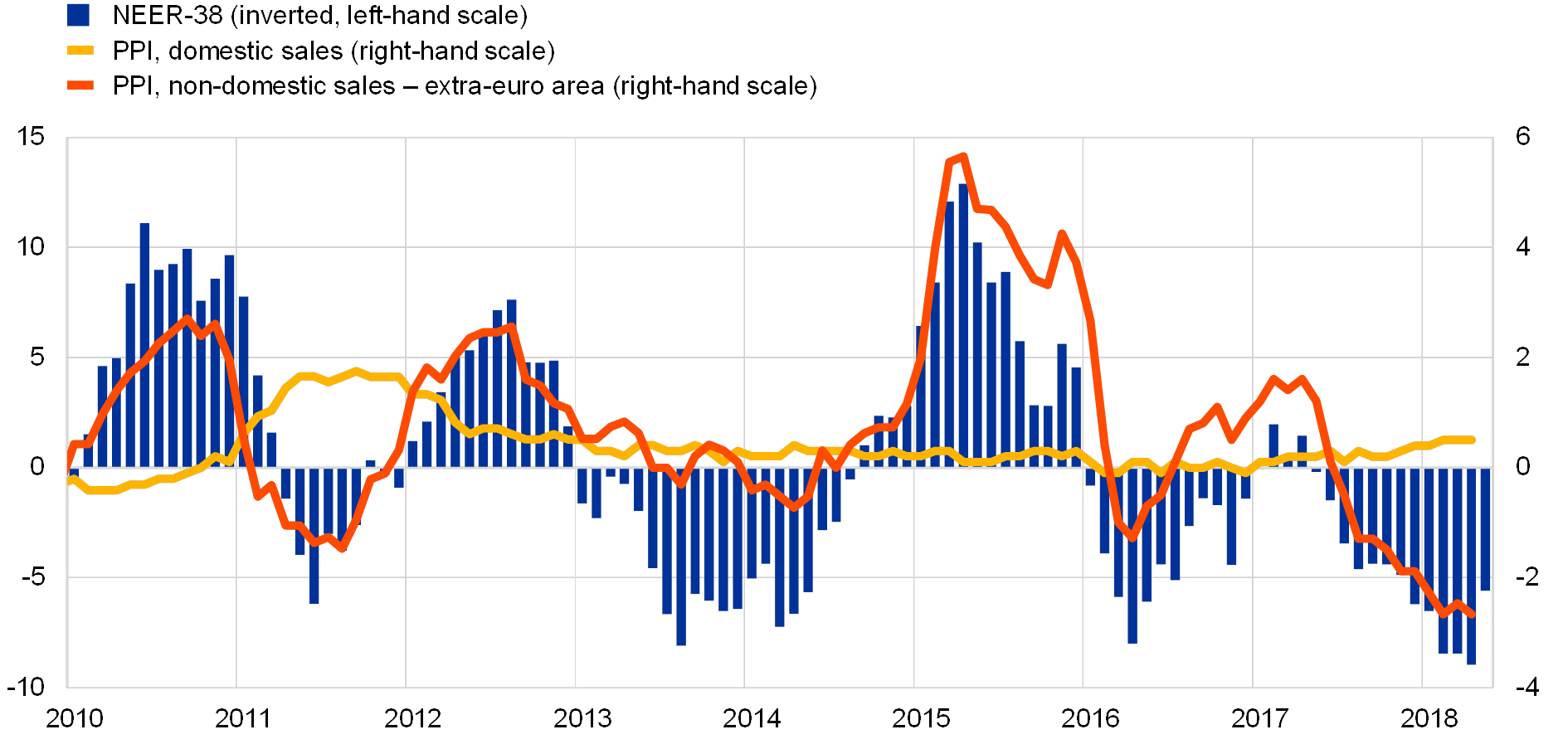

In contrast to import price inflation, euro area producer price inflation has remained resilient to downward pressure from the exchange rate appreciation. Producer price inflation for sales[3] of intermediate goods declined only moderately and annual inflation for producer prices of domestic sales of non-food consumer goods increased from 0.2% in April 2017 to 0.5% in April 2018, with much of the increase occurring since the autumn, i.e. at a point in time when the exchange rate would start to have an effect (see Chart C). Producer prices depend on domestic labour and non-labour cost developments, as well as firms’ behaviour in adjusting their margins. Notably, labour costs rose; annual growth in compensation per employee in the industrial sector excluding construction increased from 1.4% in the first quarter of 2017 to 2.0% in the final quarter of 2017. At the same time, there may have been some increase in pricing power, as suggested by a steady rise to record highs in capacity utilisation in the non-food consumer goods sector. Together, these factors may as yet have offset the downward pressure from the exchange rate.

Chart C

Producer price index (PPI) for domestic and extra-euro area sales of non-food consumer goods

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for May 2018 for the nominal effective exchange rate of the euro against 38 of its main trading partners (NEER‑38) and April 2018 for the producer price index (PPI).

The appreciation of the euro exchange rate can also be expected to affect domestic price pressures via profits of domestic firms, albeit with a somewhat ambiguous overall sign. Producer price inflation of non-food consumer goods for sales in markets outside the euro area fell sharply from 1.6% in April 2017 to ‑2.7% in April 2018 (see Chart C). This points to some pricing-to-market behaviour of euro area firms in export markets, possibly to mitigate losses in market shares that would otherwise have occurred through the exchange rate appreciation. This behaviour may have squeezed the overall profits of euro area firms. However, this effect may be smaller or even overcompensated given the large decline in import price inflation, as the rest of the world did not fully absorb the euro exchange rate movement. In this regard, firms may in effect cross-subsidise lower revenues in foreign markets by choosing to not pass on lower costs to other firms or consumers in a robust domestic market. The net effect on profits will also depend on the relative size of the exporting sector and the degree to which imports are used as inputs for firms or final products for retailers.

The latest decline in NEIG inflation does not provide a clear sign for significant effects of the exchange rate appreciation. NEIG inflation edged upwards between April 2017 and late 2017 despite the strong deceleration of inflation for imported non‑food consumer goods (see Chart D). It did so at a point when pass-through models, such as are presented in Chart A, would have predicted the onset of the downward impact of the euro exchange rate appreciation. Counterbalancing domestic demand forces may have played a role. These were evidenced by strong growth in the volume of retail trade turnover for non-food consumer goods and in the elevated margins in the non-food retail sector as shown in the Purchasing Managers’ Index survey. The decline in NEIG inflation in recent months was due partly to strong volatility in, for example, the annual rates of inflation for the clothing and footwear sub-component, which likely reflected the impact of changing seasonal sales patterns. Thus far, NEIG inflation has remained somewhat resilient to the downward pressure of the euro exchange rate appreciation, which may reflect the influence of counteracting domestic forces.

Chart D

NEIG inflation and retail margins and turnover

(annual percentage changes, percentage points and diffusion index)

Sources: Eurostat, ECB calculations and Markit.

Note: The latest observations are for May 2018 for retail margins and NEIG HICP (flash estimate) and April 2018 for NEIG components and turnover.

To conclude, monitoring the impact of the past euro exchange rate appreciation on the inflation outlook is an ongoing exercise. First, pass-through models suggest that the impacts are spread out over several quarters, so that the appreciation from mid-2017 might still be relevant for some quarters to come. Second, the exchange rate pass-through may be difficult to detect if it is offset by a confluence of other factors, including increased pricing power for firms. In this regard, continued monitoring and assessing of NEIG prices and their indicators along the pricing chain is warranted.

- See also the article entitled “Exchange rate pass-through into euro area inflation”, Economic Bulletin, ECB, Issue 7, 2016.

- For more details on the underlying drivers of the exchange rate movement, see Box 3 of the article “September 2017 ECB staff macroeconomic projections for the euro area”, ECB, 2017.

- The headline series for euro area producer price index is an aggregate of the series for domestic sales within the individual euro area countries. This abstracts from the sales of one euro area country to another, which from an area-wide perspective can also be considered as domestic sales. Producer price inflation for non‑food consumer goods of these intra-euro area sales declined from 0.2% in April 2017 to ‑0.9% in March 2018. These account for about 28% of the total non-food consumer goods produced and sold in the euro area.

Euroopa Keskpank

Avalike suhete peadirektoraat

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Saksamaa

- +49 69 1344 7455

- media@ecb.europa.eu

Taasesitus on lubatud, kui viidatakse algallikale.

Meediakontaktid