The role of households in financing government debt in the euro area

Published as part of the ECB Economic Bulletin, Issue 3/2021.

1 Introduction

The coronavirus (COVID-19) pandemic has reinvigorated interest in how governments finance their spending to an extent not seen since the global financial and euro area sovereign debt crises of 2008-12. Economic crises of such depth require governments to take decisions on how far the crisis-related costs should be financed by spending cuts elsewhere in the budget, by revenue increases and/or by incurring additional debt. At the same time increases in government debt raise questions as to the optimal financing strategy in terms of instruments and maturities, but also the investor base.

The composition of government debt has important financial and economic policy implications. Recent literature has pointed to the fact that the structure of government debt by holder can give insights into issues such as the diversification of risks in government debt issuance. It is also relevant to the strength of the sovereign-bank nexus and overall financial stability, the probability and effectiveness of sovereign debt restructuring, income inequality and the size of fiscal multipliers (see Section 2).

Against this background, the article first provides an overview of the evolution of the structure of public debt by holder in euro area countries since 1995. Literature on government debt composition has traditionally focused on distinguishing shares of domestic and foreign-held debt, with less emphasis on analysing a more detailed disaggregation by domestic holders. In this article we analyse more granular data on domestically held government debt to assess the role of non-bank actors in financial intermediation as well as the effects of the Eurosystem’s purchases of government securities on the composition of government debt by institutional sector (Section 3).

The article then explores in more detail the structure of domestically held government debt with a special focus on the household sector. With increases in the level of government debt and in the share of domestically held debt, an analysis of the public debt composition in terms of institutional sector becomes increasingly relevant, including the role of households as savings providers. For an assessment to be meaningful, the size not only of direct holdings by households should be considered, but also the size of their indirect holdings through investment funds, insurance corporations and pension funds. The aim of the article is not to provide a full picture or normative assessment of the ultimate owners of government debt but rather a factual analysis of the size and evolution of households’ holdings of government debt in the euro area, also in comparison with selected advanced economies (Section 4). For euro area countries this relies on the breakdown in the financial sector accounts ‒ known as the “who-to-whom” data ‒ published by the ECB and euro area countries. Similar datasets are available also for other EU Member States and the other advanced economies.

2 Main implications of the structure of government debt holdings

There is a large body of literature examining government debt composition by holder, but the analysis of holdings of households is more limited. Several studies analyse the holdings of public debt in the euro area by the non-financial sector and by non-residents, but they do not include households or retail government debt programmes.[1] A greater number of studies, using both macro- and microdata, are available for the United States, especially with regard to municipal debt where households traditionally have a key role.[2]

The composition of government debt holdings, including by households, is relevant to economic analysis in several areas covered in the literature.

- Public debt management. Broadening the investor base across domestic investors (residents of the country whose government has issued the debt) and foreign investors as well as across interest-sensitive and insensitive investors is a key tool in diversifying the refinancing risk and reducing borrowing costs.

- Financial stability. Feedback loops originating from domestic holdings and potential cross-border spillovers from foreign government debt holdings are important parameters for financial stability. An increased funding diversification for governments, less dependent on domestic banks and with a larger share of bonds sold to other investors can reduce such risks.

- Safe assets. Higher risk in times of economic crisis increases the demand for safe assets. Government bonds represent the main source of high-quality assets in the euro area.[3] Households are risk-averse investors and hold relatively little government debt directly, but indirect holdings via pension and investment funds and insurance corporations are much more common. Bank deposits are the main safe asset for households. In turn, the safety of bank deposits is underpinned, apart from deposit insurance, by the ability of banks to pledge collateral in the form of government bonds to the central bank. Sovereign debt thus plays a vital role in giving households financial safety.

- Sovereign debt sustainability. On the one hand, domestic debt holdings represent a more stable investor base. They can also make sovereign default less likely because they increase the incentives for debt repayment as the cost of a potential non-repayment is borne by residents.[4] On the other hand, large domestic holdings of government debt can have a destabilising effect because they generate feedback loops between the public and private sectors during crises.[5]

- Income inequality. The impact of public debt on distributional aspects and wealth inequalities is explored in the literature. Although many papers analyse only the redistributive dimension across generations, some papers also cover within-cohort wealth redistribution originating from bond holdings, including government bonds.[6] As households’ holdings of government debt are concentrated among the wealthiest households and government bonds normally offer higher yields than bank deposits, the government debt holding structure can lead to regressive distributional effects.

- Fiscal multipliers. Evidence suggests that a higher share of domestically held government debt may reduce the size of fiscal multipliers owing to stronger crowding-out of private investment.[7]

3 Structure of government debt holdings in the euro area

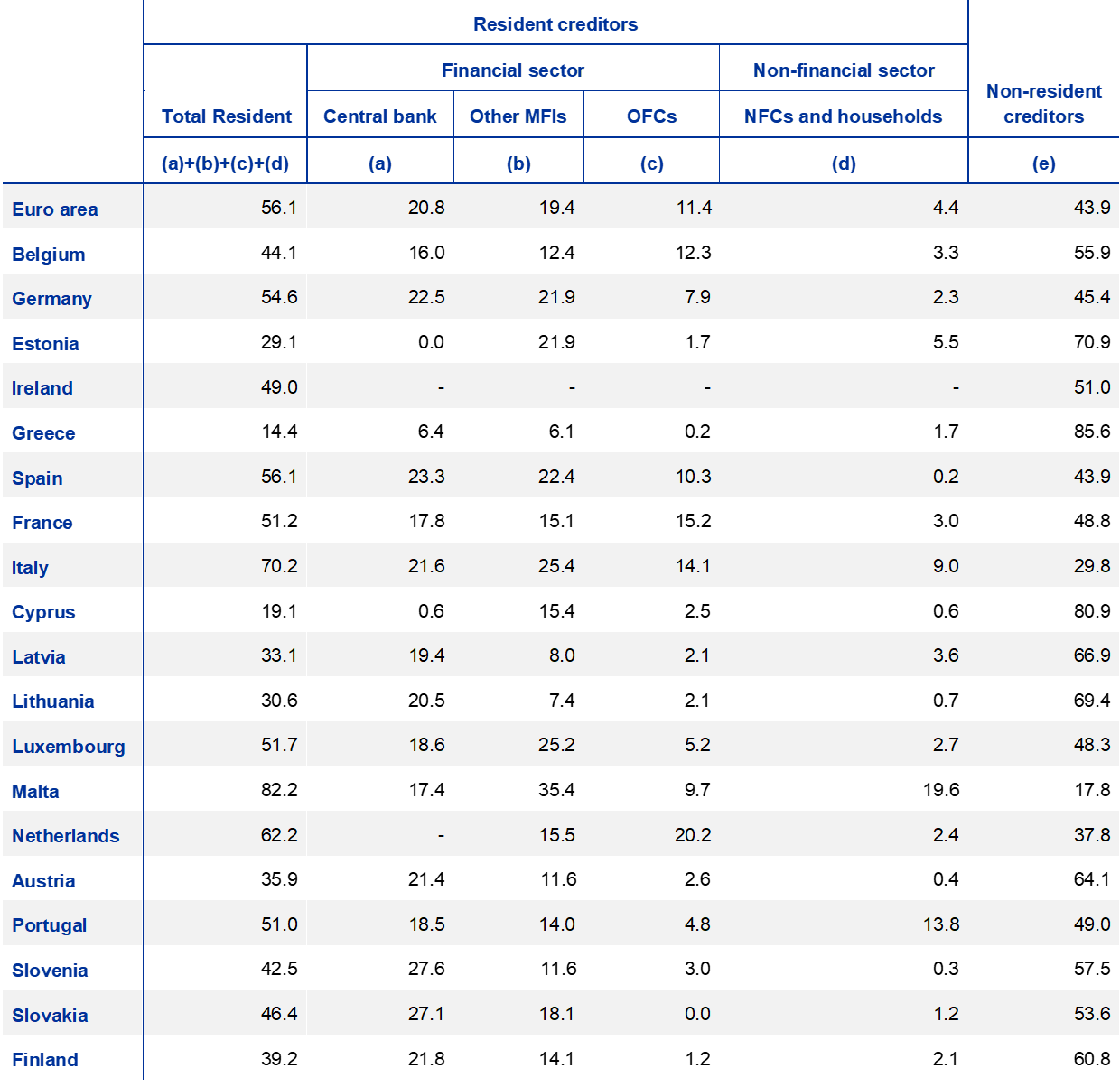

Capturing long-term trends in the structure of government debt holdings in the euro area is not straightforward because of a lack of data. While it is possible to build data on the level of the government debt over a very long period, reporting on government creditors has long been more fragmented and less reliable.[8] The global financial crisis (GFC) triggered many initiatives to cover the data gap and more granular data are now available allowing to better capture the structure of government debt holdings.[9] However, these data cover only a relatively short period of time. In annual government finance statistics, a breakdown of the holders of government debt has been available for most euro area countries since 1995.[10] The category of resident or domestic creditors refers to holders that are resident in the country whose government has issued the debt. Non-residents includes both residents of other euro area countries and residents of countries outside the euro area.[11] The resident creditors include the financial sector and the non-financial sector (Table 1). The financial sector creditors are the central bank, other monetary financial institutions (other MFIs or banks), and the other financial corporations (OFCs). The latter mainly include investment funds (IFs) and insurance corporations and pension funds (ICPFs).[12] Lastly, the non-financial sector (resident creditors) aggregates non-financial corporations (NFCs) and households.[13] The composition of government debt is determined by a number of demand and supply factors, such as the liquidity conditions in the sovereign markets, the marketability of the debt instruments and the institutional framework for debt and inflation management. Table 1 shows significant heterogeneities across the euro area countries. This section focuses on the main drivers behind the shifts in the composition of government debt over 1995-2020.

Table 1

Holders of government debt

(percentage of total government debt; 2020)

Sources: ESCB and ECB calculations.

Notes: Data refer to excessive deficit procedure (EDP) debt. Gross general government debt at nominal value and consolidated between sub-sectors of government. For Ireland domestic holdings are calculated as the total minus the non-resident holdings.

The share of euro area government debt held by residents declined substantially before the GFC and increased again afterwards. With the exception of a few countries in which the government debt-to-GDP ratio is very low in comparison with the euro area average (like Estonia, Lithuania, Luxembourg or Malta), there was an overall increase in the share of non-resident holdings before the GFC (Chart 1). There is evidence of growing financial integration within the euro area after the introduction of the euro.[14] The GFC had a major impact on cross-border portfolio investments, which was compounded by the euro area sovereign debt crisis in 2010-12. Global investors shifted their portfolio investment away from euro area countries that were perceived to be under stress.[15] In Spain and Italy, the share of government debt held by non-residents dropped between 2010 and 2015. Similar trends prevailed in Greece, Ireland and Portugal, and later in Cyprus, after excluding the loans granted by non-resident creditors under the EU/IMF financial assistance programmes. In other countries, like Germany and France, the share of non-resident holdings stabilised. It stood at around 50% in 2015 at euro area level. The overall reduction in the share of non-resident holdings of government debt has mostly been driven by the Eurosystem’s sovereign bond purchases under the public sector purchase programme (PSPP) since 2015 and under the pandemic emergency purchase programme (PEPP) since 2020.[16] By reducing yields on securities, these programmes also prompted investors to shift their investments towards assets with higher expected returns. Foreign investors have rebalanced their portfolios towards more attractive investments.[17]

Chart 1

Euro area government debt structure by debt holder

(percentage of total government debt; 1995-2020)

Sources: ESCB and ECB calculations.

Notes: The latest observations are for 2020. For Ireland the breakdown of the domestic holdings is not available, therefore only the total domestic holdings are shown in grey and is calculated as the total minus the non-resident holdings. For the Netherlands the central bank holding is calculated as the residual part (i.e. the total minus the other sub-components). Countries are ranked according to their GDP since its size is likely to influence the structure of the debt. The Eurosystem holdings do not only consist of national central banks’ holdings of domestic bonds. First, the ECB also holds securities issued by government: for each euro area country ‒ the ECB holding is classified as a non-resident holding. Second, for monetary policy purposes, national central banks purchase cross-border EMU bonds. Nevertheless, the national central banks’ holdings of domestic bonds constitute the bulk of the Eurosystem holdings.

The increase in domestic holdings of government debt was mainly driven by non-monetary financial institutions until the euro area sovereign debt crisis and thereafter by monetary financial institutions including central banks. Chart 1 shows the available breakdown of domestic holders. Before the GFC, resident banks and other financial corporations hold the most government debt. Central banks and the other domestic holders are less significant creditors, except for in Ireland, Spain, Italy, Malta and Portugal where households and NFCs’ holdings are more prominent, although their weight is declining. The chart shows that before the GFC, the relative share in government debt of OFCs grew in most countries while the banks’ share declined. Structural factors, including population ageing and institutional factors such as pension reforms encouraging private retirement saving schemes contributed to the increased holdings by OFCs, in particular by ICPFs.[18] During the euro area sovereign debt crisis, the share of government debt held by banks increased in countries that were subject to financial market pressure thus reinforcing the sovereign-bank nexus. Since then, larger capital buffers have strengthened the euro area banks by raising their loss-absorption capacity, and a revised regulatory framework has reduced risks from the sovereign-bank nexus.[19] Finally, the share of government debt held by central banks has increased since 2015 as a result of the Eurosystem purchases under the PSPP and the PEPP to stand at 20.8% at the euro area level at the end of 2020. At the country level, the data show only the holdings of the national central banks, but the total Eurosystem holdings of domestic government debt cannot be identified from the data because the ECB is classified as a non-resident creditor. Besides, the other euro area central banks also have cross-border holdings of sovereign bonds. Although declining, the share of government bonds held by private, price-sensitive investors, also called “free float”, remains substantial in the euro area.

Box 1

The structure of government debt in terms of instruments

Government debt valuation and composition

The government debt or “Maastricht debt” is the total consolidated gross debt at face value in the following categories of government liabilities (as defined in the European System of Accounts[20] (ESA)): currency and deposits, debt securities and loans. The government debt as notified within the excessive deficit procedure (EDP) to Eurostat covers all general government levels: the central government and its federal state entities, local government and social security funds. It is gross debt in the sense that government financial assets are not subtracted from liabilities. It is consolidated by excluding the debt items of a government unit that are held by another government unit (for example, government deposits held with the Treasury).

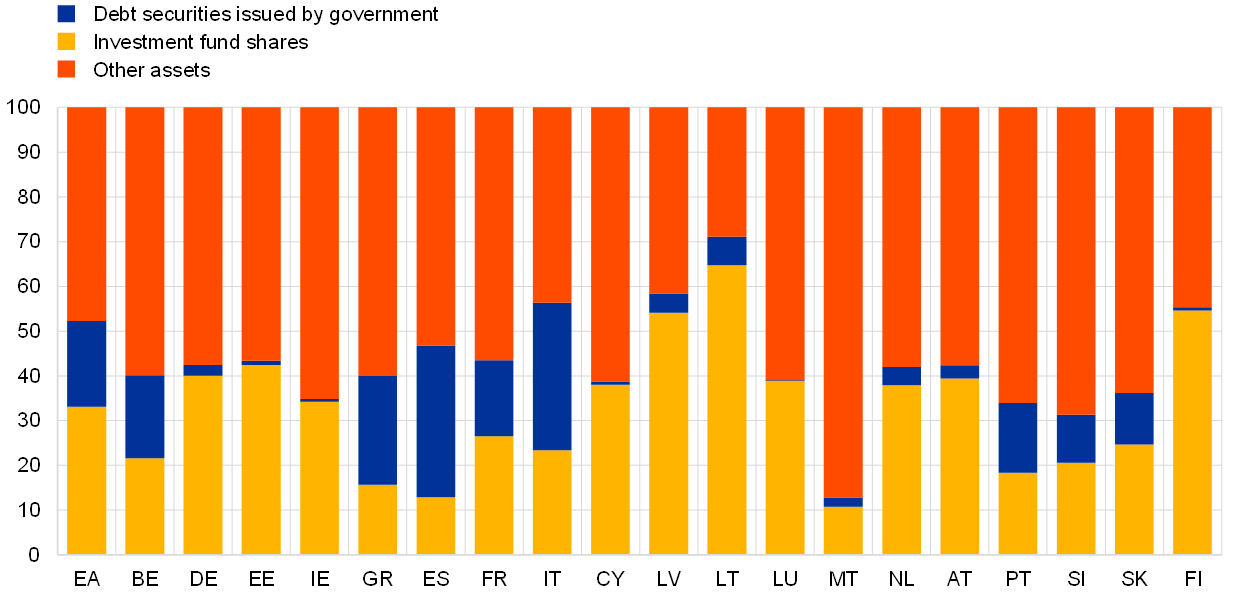

The composition of the Maastricht debt is very heterogeneous across the euro area countries. Chart A illustrates the structure in 2019.[21] Debt securities represent the major share within the euro area aggregate fluctuating between 70.5% and 80.3% in the period from 1995 to 2019.

The relative importance of loans in government debt has evolved over time notably owing to the change in the relative cost of bank loans compared with debt securities. It increased further, for example, in the wake of the euro area sovereign debt crisis with the loans granted under the EU/IMF financial assistance programmes, as illustrated by the case of Greece (where loans represent 80% of the debt in 2019) and to a lesser extent by Ireland, Cyprus and Portugal.

Chart A

Government debt structure by instrument

(percentage of total government debt; 2019)

Sources: ESCB and ECB calculations.

The currency and deposits component of government debt

The currency and deposits component of the government debt amounted to €363 billion in 2019, i.e. 3.3% of the euro area government debt. It is mostly composed of savings products[22] issued by government and deposits placed by non-government units with the Treasury. The savings notes of central government directly held by households represented a share of 37% of the deposits component in 2019 and the deposits held by the resident (mainly public) financial or non-financial entities with central government a share of 54%. The remaining share of 9% consists of deposits from entities outside the euro area.

There is a high level of heterogeneity across euro area countries in terms of the use and the institutional arrangements for the currency and deposits component. In two countries, savings notes and deposits represented in 2019 more than 10% of the government debt. In Portugal (11.6%), this was mostly accounted for by the savings and Treasury certificates directly held by households, and in Ireland (10.5%) it is common for households to hold savings notes. In Italy, in addition to savings notes directly held by households, deposits also include funds raised by public banks with postal savings bonds. In Malta, the central government has been issuing fixed non-negotiable coupon rate bonds to Maltese citizens aged 62 years or above since 2017. These represented in 2019 approximately 5.1% of the Maltese government debt.

With a lower share of their respective government debt (between 1% and 2% in 2019), savings notes and deposits in Greece,[23] Lithuania, Latvia and France contribute to financing general government. In Lithuania, savings notes issued by the Treasury are mostly held by households. In Latvia, bailiffs or custodians in debt recovery proceedings must hold transferable deposits in Treasury accounts. In France, most deposits held with the government are from public entities (classified as non-government) or are deposits with the Treasury related to the issuance of external currencies pegged at a fixed rate against the euro. For the remaining euro area countries, the share of deposits in government debt is marginal.

Finally, currency has a small share in the liabilities of euro area government (0.3% of an amount close to €30 billion) corresponding to the euro coins in circulation (mainly held by households) when the governments are responsible for its issuance.[24]

4 Holdings of government debt by households

More granular data enable an assessment of the role of households in financing the government debt. The annual government finance statistics used in the previous section do not permit such an analysis. The direct government debt holdings of households cannot be distinguished as households and non-financial corporations are grouped together. Nor is the indirect role of households in financing government debt easily observable, as this requires “looking through” financial intermediaries. The financial sector accounts, however, provide a comprehensive framework for the analysis of the role of households in financing government debt. The breakdown in these accounts ‒ “who-to-whom” data ‒ present the financial positions between sectors and therefore provide a more comprehensive view on how government is financed.[25] Figure 1 illustrates the network of euro area inter-sector claims in the form of deposits, debt securities, investment fund shares and insurance and pension products. It only includes instruments that are relevant for assessing households’ contribution to financing government debt. It does not fully depict how government debt is financed, however, as loans are not included. Moreover, not all financial assets of households are shown, as their holdings in shares and other equities are excluded. [26] Nevertheless, it provides an overview of the complexity of the financing relationships in the euro area.

Figure 1

Government funding by other sectors in the euro area using “who-to-whom” funding relationships (deposits, debt securities, investment fund shares and insurance and pension products)

(outstanding amount; Q3 2020; EUR trillions)

Sources: ECB and ECB calculations.

Notes: For all sectors but government, the size of the nodes is proportional to the combined assets of each sector in the form of deposits, debt securities, investment fund shares and insurance and pension products (excluding intra-sector claims). For government, the size of the node is proportional to its combined liabilities in the form of deposits and debt securities (excluding intra-sector claims). The outstanding amounts of these combined assets and liabilities are indicated in brackets. The width of the arrows linking two sectors indicates the total amount of funding from one sector to another sector when combining those instruments. For all sectors but government the sum of arrows going from the node correspond to the size of the node. For government, the sum of the arrows going to the node corresponds to the size of the node. Only combined funding relationships larger than €100 billion are plotted.

Box 2

Assets of euro area insurance corporations, pension funds and investment funds in the form of euro area government debt securities

The liabilities of euro area insurance corporations, pension funds and, to a lesser extent, investment funds are tilted towards the household sector. Chart A shows that the main liabilities of euro area insurance corporations and pension funds are life insurance technical reserves (ITRs) and pension entitlements respectively. Life ITRs amounted to more than €6 trillion at the end of the third quarter of 2020 and represent approximately 70% of the insurance sector’s total liabilities. Euro area pension funds reported pension entitlements of slightly more than €2.7 trillion at the end of the third quarter of 2020 which account for more than 90% of their total liabilities. More than 98% of these life ITRs and pension entitlements are vis-à-vis euro area residents.[27] The liabilities of euro area investment funds are more diversely distributed. On an estimated basis, only around 17% of the investment fund shares are held by euro area households amounting to approximately €2.3 trillion. Chart B shows the growing share of these products in financial assets held by euro area households over the last 13 years, increasing from 33% in 2008 to a share of 42% in 2020.

Chart A

Liabilities of euro area insurance corporations, pension funds and investment funds

(outstanding amount; Q3 2020; EUR billions)

Sources: ECB and ECB calculations.

Note: Investment funds held by euro area households are reasonably close to investment fund shares issued by euro area investment funds and held by euro area households.

Chart B

Share of insurance, pension and investment fund products in total financial assets of euro area households

(percentage of total financial assets of euro area households)

Sources: ECB and ECB calculations.

Notes: Investment funds held by euro area households are reasonably close to investment fund shares issued by euro area investment funds and held by euro area households. Solvency II valuation of life insurance technical reserves as of 2016.

Significant holdings relate to debt securities issued by the euro area government sector. Chart C shows that holdings of debt securities represent the main asset item on the balance sheets of euro area insurance corporations and account for more than 40% of their total financial assets. Investments in euro area government bonds amounted to more than €1.7 trillion. Close to 65% of these holdings were domestic government debt securities at the end of the third quarter of 2020, exhibiting therefore a strong “home bias”.

Euro area pension funds hold more than €770 billion worth of debt securities which account for around 25% of their total assets. Approximately €230 billion worth of these debt instruments have been issued by non-euro area residents. Investments in euro area government bonds represented approximately half of these debt securities holdings, like for euro area insurance corporations, and amounted to more than €400 billion at the end of the third quarter of 2020.

Euro area insurance corporations and pension funds hold also substantial amounts of government debt indirectly via investment fund shares. More than 95% of these holdings were issued by euro area entities and are well covered in the data of euro area investment funds.

Euro area investment funds also invest significantly in debt securities (accounting for around 37% of their total assets). In contrast to insurance corporations and pension funds, investments in debt markets are geographically more widely distributed with debt securities of non-euro area issuers accounting for more than 50% of their total debt securities holdings. Investments in euro area debt instruments were also mainly directed to the government sector and represent approximately €900 billion. However, only less than 25% of these holdings are with domestic government units at the end of the third quarter of 2020.

Chart C

Holdings of euro area debt securities by issuing sector and geographical area

(outstanding amounts; Q3 2020; EUR billions)

Sources: ECB and ECB calculations

Notes: MFIs stands for monetary financial institutions; NFCs for non-financial corporations; OFCs for other financial corporations.

Households contribute both directly and indirectly to the financing of government debt. The households’ direct holdings of government debt correspond to their deposits vis-à-vis the government (see Box 1) plus their holdings of debt securities issued by government entities. Households do not provide loans to governments. However, there is no unique definition of an indirect holding. According to a narrow definition of indirect holding, only indirect holdings via IFs are considered, as individuals select the IF based on the fund’s characteristics and, in particular, the type of assets the fund invests in. In a very broad definition of indirect holding, all financial intermediaries can be considered. For the purposes of this article, we opt for an in-between scope of indirect holdings. ICPFs, as long-term investors, acquire long-term maturity assets, especially sovereign bonds, to match the maturity profile of their liabilities. Their assets can be considered to be held indirectly by households. Conversely, MFI investments in government debt are not considered to be indirect assets of households, as banks do not use the portfolio of assets as collateral to meet their obligations vis-à-vis depositors in fulfilling their transformation function. While households play a significant role in financing government debt through placing deposits in MFIs, which in turn invest in government bonds, this channel is distinguished from indirect holdings of households via resident IFs and ICPFs. This distinction is useful to assess the relative importance of the bank and non-bank financial intermediation.

The indirect holdings still exclude several important channels through which households may contribute to financing government debt. In Figure 1, the channels analysed are highlighted in yellow. Only the direct holdings of resident IFs and ICPFs are taken into account for households’ indirect holdings. For example, there are sizeable financial interlinkages within the resident OFCs (e.g. ICPFs investing in investment funds, with the latter investing in debt securities), which are not considered here as indirect holdings.[28] Moreover, part of the funds invested by households in non-resident funds are re-invested in government debt but are not included here as households’ indirect holdings.[29] To enrich the comparison exercise, other advanced economies ‒ the United States, Canada and the United Kingdom ‒ are included.[30] Quarterly data are available since 1951 (for the United States) and since 2013 (for the euro area countries) until the third quarter of 2020 for all countries. As the outstanding amounts are recorded at market value in financial accounts whereas government debt is reported at face value, the shares of direct and indirect holdings are computed using government debt at market value as a denominator.[31]

Table 2

Households’ direct and indirect holdings of government debt

(percentage of total government debt; 1995-2020)

Sources: ESCB, Federal Reserve System, Statistics Canada, Office for National Statistics and ECB calculations.

Notes: For Ireland and Portugal, households’ direct holdings only include deposits before Q4 2013 and Q1 2013 respectively. For the United States, the deposits correspond to the Savings Securities (mainly Savings bonds: Series EE, Series HH, Series I), and for Canada they correspond to the Canada Savings Bonds (CSBs). The euro area aggregate does not correspond to the weighted average of the Member States as not only the households’ direct and indirect holdings of domestic government debt is considered but also the direct and indirect government debt holdings of other EMU Member States. The indirect holding is derived by multiplying the ICPF and IF direct holdings of domestic sovereign bonds by the share of the claims vis-à-vis the resident households in their total liabilities.

Households’ direct holdings of government debt are relatively low in most euro area countries and have been declining since the introduction of the euro. Table 2 shows for all countries the share of households’ direct holdings of government debt in the form of deposits and debt securities. As highlighted in Box 1, direct holdings in the form of deposits are very specific to several countries in the euro area (mainly Ireland, Italy, Malta and Portugal), but have also been sizeable in the United States, Canada and the United Kingdom. Chart 2 shows an overall declining trend in these forms of savings instruments.[32] This decline might have resulted from the choice of governments to reduce the scope of relatively costly retail debt programmes. These programmes sometimes offer tax exemptions or interest premia, which makes them more costly compared with market funding. The decline can also originate from a reduction in demand in an environment of low interest rates or a shift to private pension systems. Competition from close substitutes issued by banks might also have contributed to the decline. The direct holdings in the form of securities issued by government also show a strong heterogeneity across countries, being very high in Malta and in the United States and relatively high in Italy. As in the case of deposits, the issuance of special retail bonds contributes to higher direct holdings of households in the form of securities.[33] In total, households held directly around 2% of government debt in the euro area in the third quarter of 2020, but this figure was close to 20% in Malta, close to 10% in Ireland and Portugal, and around 7% in Italy. The share of government debt held directly by households was close to 15% in the United States and close to 8% in the United Kingdom.

Chart 2

Households’ direct holdings of government debt

(percentage of total government debt; 1999-2020)

Sources: ESCB, Federal Reserve System, Statistics Canada, Office for National Statistics and ECB calculations.

Notes: For Ireland and Portugal, the households’ direct holdings only include deposits before 2013 and 2013 respectively. Only countries where the direct holding is or has been close to 10% or above are included. The large increase in 2004 in the United States corresponds to a break in the Municipal Bonds data, not to actual transactions. The latest observations are for Q3 2020.

Households’ indirect holdings are lower where banks have a larger share in financial intermediation and higher where financial interlinkages between the other financial corporations are less prevalent. Households held indirectly around 14% of government debt in the euro area in the third quarter of 2020, mirroring the large government securities holdings of IFs and ICPFs (Box 2). The level of indirect holdings depends on the relative importance of IF shares and ICPF products in the households’ total financial assets. In this regard, the relative share of the bank deposits is larger and partly contributes to lower indirect holdings in the euro area than in economies like the United States where the OFCs play a greater role in managing households’ savings. Within the euro area countries, this factor explains lower indirect holdings in Germany, Spain, Cyprus, Malta, Austria, Portugal and Slovakia and the higher level of indirect holdings in the Netherlands where pension funds are particularly developed (Chart 3). The level of indirect holdings is also influenced by the investment strategy of IFs and ICPFs, namely the extent to which they invest directly in assets issued by the non-financial sector to cover their financing needs (such as governments or non-financial corporations), or the extent to which they invest in IFs which ultimately invest in claims issued by the non-financial sector. Chart 4 shows that in the euro area, the intensity of financial interlinkages between OFCs varies across countries and contributes to lower indirect holdings in Germany, the Netherlands, Austria and in Finland as only the direct government debt holdings of IFs and ICPFs is considered.

Chart 3

Composition of households’ financial assets by instrument in euro area countries

(percentage of total financial assets; Q3 2020)

Sources: ECB, Eurostat and ECB calculations.

Note: “Other” includes banknotes, debt securities, shares and other equities, loans granted by households to all institutional sectors and other accounts receivable.

Chart 4

Composition of ICPFs’ financial assets by instrument in euro area countries

(percentage of total financial assets; Q3 2020)

Sources: ECB, Eurostat and ECB calculations.

Note: “Other” includes banknotes, debt securities issued by sectors other than government, shares and other equities, loans granted by ICPFs to all institutional sectors and other accounts receivable.

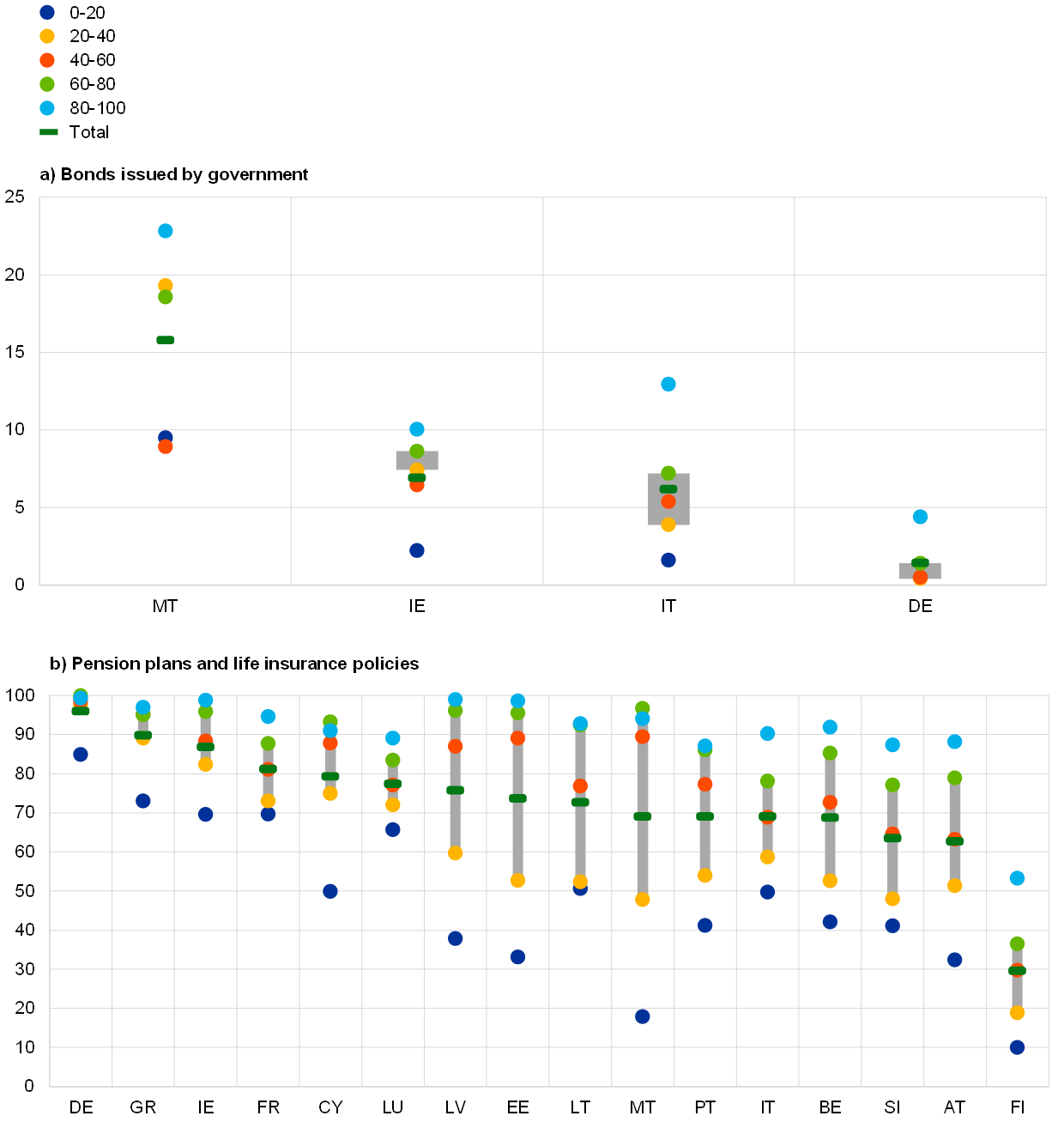

The total holdings by households of government debt are sizeable and concentrated among the wealthiest households. Households held both directly and indirectly around 16% of government debt in the euro area in the third quarter of 2020, but the level was close to 20% in Malta and Italy, close to 15% in Portugal, and 12% in France (Table 2). In the United States households hold around one-third of the government debt, and in Canada and the United Kingdom the share is close to one quarter. For euro area countries, the Household Finance and Consumption Survey[34] (HFCS) shows that within each country holdings of government debt instruments are tilted towards the top of the income distribution[35] (see Chart 5).[36] The households from among the top 20% of income have a higher propensity to own bonds issued by government. The overall propensity to hold this kind of asset is very low in most of the euro area countries, but there is cross-country heterogeneity as the propensity to hold bonds issued by government is relatively high in Ireland, Italy and Malta. Moreover, households from among the top 20% of income have a higher propensity to have at least one pension plan or life insurance policy. This indicates that such indirect holdings are also biased towards the wealthiest households. The financial literacy, financial sophistication, and the use of professional financial advice play an important role in both the composition of households’ wealth and return on households’ investments and are likely to be an important driver of this bias.[37]

Chart 5

Households’ propensity to hold financial assets by income quintile

(propensity to hold in percentages by income quintile)

Source: The Household Finance and Consumption Survey: results from the 2017 wave.

Notes: Panel a) shows the proportion of households holdings bonds issued by central or other government across five income quintiles. Only countries for which the total holdings are above 1% are shown. Panel b) shows the proportion of households holding at least one pension plan or one life insurance policy. Spanish data are not yet available. For the Netherlands and Slovakia, the propensity to hold at least one pension plan or one life insurance policy is virtually 100% for all income quintiles. The vertical grey bars show a range of propensity to hold of middle-income households between the 20th and 80th income quintiles. Countries are ranked according to their total propensity to hold the specific financial assets.

5 Conclusion

Over the last two decades, the structure of government debt by holder has evolved, driven by financial integration, economic crises and policy responses. In the early stages of EMU, growing financial integration led to an increase in cross-border holdings of government debt. The GFC and the euro area sovereign debt crisis led to a sharp reduction of portfolio investment away from euro area countries that were perceived to be under stress, amplifying the feedback loops between sovereigns and banks, as the financial health of banks and sovereigns is intertwined. The importance of OFCs in financing government debt has also grown over time as structural and institutional changes (e.g. population ageing and the establishment of funded pension pillars) have contributed to the increase of investment in pension and life insurance products. Finally, the Eurosystem’s purchases of government securities have contributed to the reduction in the share of non-resident and bank holdings of government debt, which started in 2015.

The share of households’ direct and indirect holdings of government debt is significant and has also evolved. The share of government debt held directly by households is relatively low in the euro area as a whole (2% in the third quarter of 2020), but it is higher in several euro area countries and in other advanced economies, reflecting notably institutional differences and supply policies (e.g. the issuance of specific retail bonds or savings notes). However, the role of households in financing government debt goes beyond direct holdings. Considering indirect holdings through IFs and through ICPFs, the role of households in financing the government debt is more significant in most euro area countries (almost 16% in the third quarter of 2020).

- Among others Merler, S. and Pisani-Ferry, J., “Who’s Afraid of Sovereign Bonds”, Bruegel Policy Contribution, Issue 2012/2, 2012; Andritzky, J.R., “Government Bonds and their Investors: What Are the Facts and Do They Matter?”, IMF Working Paper, No 12/158, 2012; Afonso, A. and Silva, J., “Determinants of non-resident government debt ownership”, Applied Economics Letters, Taylor & Francis Journals, Vol. 24(2), 2017, pp. 107-112.

- See Hager, S.B., “Public Debt, Ownership and Power: The Political Economy of Distribution and Redistribution”, PhD diss., York University, Toronto, 2013.

- Grandia, R., Hänling, P., Lo Russo, M. and Åberg, P., “Availability of high-quality liquid assets and monetary policy operations: an analysis for the euro area”, Occasional Paper Series, No 218, ECB, 2019.

- Guembel, A. and Sussman, O., “Sovereign Debt without Default Penalties”, Review of Economic Studies, Vol. 76, Issue 4, 2009, pp. 1297-1320; Gennaioli, N., Martín, A. and Rossi, S., “Sovereign Default, Domestic Banks, and Financial Institutions”, The Journal of Finance, Vol. 69, Issue 2, 2014, pp. 819-866.

- See Acharya, V., Drechsler, I. and Schnabl, P., “A Pyrrhic Victory? Bank Bailouts and Sovereign Credit Risk”, The Journal of Finance, Vol. 69, Issue 6, 2014, pp 2689-2739; Farhi, E. and Tirole, J., “Deadly Embrace: Sovereign and Financial Balance Sheets Doom Loops”, Review of Economic Studies, Vol. 85(3), 2018, pp 1781-1823.

- Arbogast, T., “Who Are These Bond Vigilantes Anyway? The Political Economy of Sovereign Debt Ownership in the Eurozone”, MPIfG Discussion Paper, 20/2, 2020.

- Broner, F., Clancy, D., Erce, A. and Martín, A., “Fiscal multipliers and foreign holdings of public debt”, Working Paper Series, No 2255, ECB, 2019.

- See Reinhart, C.M. and Rogoff, K.S., “Growth in a time of Debt”, American Economic Review, Vol. 100, Issue 2, 2010, pp. 573-78.

- See the G20 Data Gaps initiative recommendations to enhance economics and financial statistics. The Securities Holdings Statistics offer more breakdowns and a higher frequency than government finance statistics, but are available for a shorter period.

- More information on the dataset is available on the ECB’s website in the Statistical Data Warehouse section on Government Finance Statistics.

- The split of foreign holdings between rest of the euro area and the rest of the world outside the euro area is not available for data shown in Table 1 and Chart 1, which represents a data limitation. Such a distinction would be relevant considering the absence of currency risk for intra-euro area holdings. It would also allow to better assess the contribution of foreign holdings of government debt to financial integration in the Economic and Monetary Union (EMU).

- Other financial intermediaries, financial auxiliaries and captive financial institutions and money lenders are also included in the OFCs.

- The household sector includes non-profit institutions serving households (NPISH).

- See, for instance, Lane, P., “The real effects of European Monetary Union”, Journal of Economic Perspectives, Vol. 20:4, 2006, pp. 47-66.

- See, for example, Merler, S. and Pisani-Ferry, J., op. cit.

- See also Hammermann, F., Leonard, K., Nardelli, S. and von Landesberger, J., “Taking stock of the Eurosystem’s asset purchase programme after the end of net asset purchases”, Economic Bulletin, Issue 2, ECB, 2019.

- See Koijen, R.S.J., Koulischer, F., Nguyen, B. and Yogo, M., “Euro-Area Quantitative Easing and Portfolio Rebalancing”, American Economic Review, Vol. 107, No 5, 2017, pp. 621-627.

- Voluntary schemes or pension systems’ third pillar, see Rodríguez-Vives, M. and Kezbere, L., Social spending, a euro area cross-country comparison, Economic Bulletin, Issue 5, ECB, 2019.

- See Dell’Ariccia, G., Ferreira, C., Jenkinson, N., Laeven, L., Martin, A., Minoiu, C. and Popov, A., “Managing the sovereign-bank nexus”, Working Paper Series, No 2177, ECB, 2018.

- See also “European system of accounts – ESA 2010”, Eurostat, European Commission, 2013.

- Complementary information can be found on the ECB’s website in the Statistical Data Warehouse sections on Government Finance Statistics and Debt securities issuance and service by EU governments.

- According to ESA only negotiable securities qualify as debt securities. Non-negotiable bonds, disregarding their labelling, are classified as deposits. A range of various savings products offered to personal savers such as savings bonds, savings books, savings certificates or deposit accounts are classified as deposits.

- In Greece, savings notes and deposits consist of time deposits held by households since an entity carrying out consignment deposit activities is reclassified in government.

- The government is responsible for coin issuance in all euro area countries, except for Slovakia and the three Baltic States where coins are a liability of the central bank.

- For an overview of data availability, see Guideline of the European Central Bank of 25 July 2013 on the statistical reporting requirements of the European Central Bank in the field of quarterly financial accounts (ECB/2013/24) (OJ L 2, 7.1.2014, p. 34).

- See also Household sector report: 2020 Q3, “Quarterly report of financial and non-financial accounts for the household sector in the euro area”, ECB, 2021.

- For more details on pension fund statistics, see Gutiérrez Curos, J., Herr, J., Quevedo, R., Valadzija, M. and Yeh, M.-L., “New pension fund statistics”, Economic Bulletin, Issue 7, ECB, 2020.

- A real “look-through” would require the method’s reiteration and allow the full removal of intermediation.

- More granular data such as the Securities Holdings Statistics would enable some round-tripping to be identified.

- In the financial accounts of the United States, domestic hedge funds are also classified in the household sector, while in ESA they are classified as IFs. Moreover, the general government debt instruments are recorded at nominal value in the financial accounts balance sheets. For the United Kingdom, the IF balance sheet data are not available on a disaggregated basis. Therefore, indirect holdings are computed using only the direct holding of the ICPFs.

- For the non-EU countries, a public debt is computed using a definition close to European standards, both in terms of instruments and in terms of the government perimeter. The computed data are close to the ones published by the Bank for International Settlements (BIS) (see the section of the BIS website on Credit to the non-financial sector).

- In Portugal, the issuance of new savings certificates (Treasury Certificates Savings Plus) in 2013 has contributed to the rebound of households’ deposit holdings vis-à-vis the government.

- In the United States, without being strictly reserved to retail investors, the associated tax exemptions for local government bonds (Municipal Bonds) make them more attractive to households. In Malta, investors can invest in Malta Government Stocks (MGS) through competitive auctions and non-competitive retail applications. In Italy, the government issued for the first time in 2012 BTPs Italia, which are inflation-indexed bonds specially designed for retail investors. In June 2020 the government also issued a new retail series of GDP-linked bonds.

- The HFCS collects information on the assets, liabilities, income and consumption of households. See Household Finance and Consumption Network, “The Household Finance and Consumption Survey: results from the 2017 wave”, Statistics Paper Series, No 36, ECB, 2020.

- Given the unequal distribution of household wealth and the fact that certain financial instruments are almost exclusively held (and in large quantities) by the wealthiest households, most countries apply some type of oversampling of wealthy households in their survey. Nevertheless, the top tail of the wealth distribution might still be underrepresented in surveys. See Chakraborty, R., Kavonius, I., Pérez-Duarte, S. and Vermeulen, P., “Is the top tail of the wealth distribution the missing link between the Household Finance and Consumption Survey and national accounts?”, Working Paper Series, No 2187, ECB, 2018.

- The HFCS does not contribute to explaining the cross-country differences within the euro area. Given the breakdowns available in the HFCS, only the propensity to hold the relevant instruments can be assessed but the corresponding amounts held are not available. It is therefore impossible to compute direct and indirect holdings based on the survey data.

- See Stolper, O.A. and Walter, A., “Financial literacy, financial advice, and financial behavior”, Journal of Business Economics, Vol. 87, No 5, 2017, pp 581-643.